This time, the Fiat Chrysler CEO went a step further than usual by declaring that the latest plan for the company is essentially a one-way bet on cheap gas. Production of compact cars will end to free up production capacity for high-margin, low-mileage Jeeps and RAM trucks.

This, combined with Fiat’s more or less complete lack of a fuel economy or electrification strategy beyond buying emissions credits from other manufacturers “foolish” enough to produce electric and hybrid “compliance cars,” is quickly making Marchionne, if not an industry joke, then certainly yesterday’s man.

At least, that is what people are saying. I have an alternate hypothesis. The Auto Industry Is Not Heading to a Good Place (The author, in my opinion, has the correct thesis. Ride sharing, Uber, Tesla, more complex electronics mean less demand and more investment to run in place).

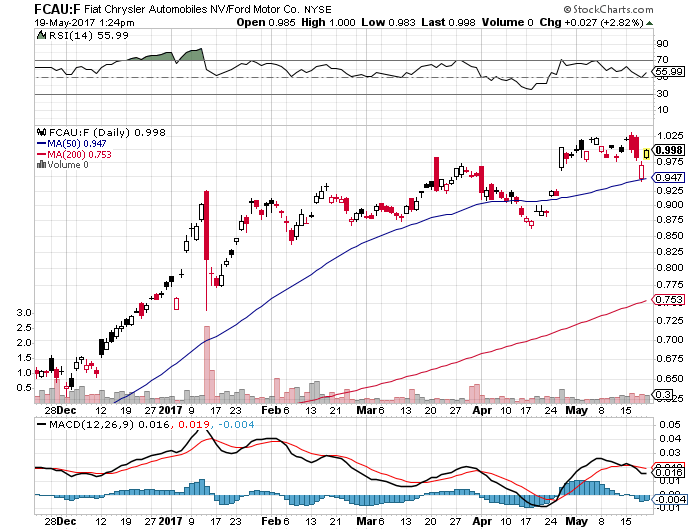

Fiat vs. Ford above

Fiat (FCAU) has done slightly better than GM and much better than Ford (F). However, the auto industry is in a bad place that will worsen.

The context is frightening. Global fuel economy and emissions regulations are becoming so strict that it is possible to meet them only with partial or full electrification of the automobile. And the existing automobile production system, based primarily on stamping sheet metal and amortizing heartbreaking development costs and capital expenditures over millions of units, is incredibly capital inefficient.

What’s more, the industry’s move towards electric vehicles represents a significant challenge to the traditional strategic landscape an automaker faces. An electric vehicle has drastically fewer moving parts than an internal combustion vehicle and is, by design, far more modular, meaning that barriers to new entrants are significantly lower.

Electric vehicles are also far more uniform in their driving dynamics, because there is little scope for refining an electric motor with one moving part. Swathes of engineering and marketing investments become irrelevant. And both ride-sharing enterprises and developments in automation seem increasingly likely to grow beyond niche markets into something properly disruptive to the car ownership business model.

Marchionne Knows This

Last year, Marchionne presented a uniquely critical slide deck about the way the auto industry destroys capital. His argument was that, unless the industry consolidates and stops duplicating engineering costs (e.g., every car manufacturer has its own separately developed but fundamentally identical 2.0L 4-cylinder petrol engine), then the market will eventually force its hand, having gotten sick of miserly returns on billions in investments.

The industry response to this slide deck was more or less complete agreement, with the caveat that competitors would not have to outlast the market so much as merely outlast Fiat Chrysler. Marchionne then pursued an odd and ultimately unsuccessful merger with GM’s Mary Barra, who confidently rejected Fiat Chrysler’s plan, noting, “We are merging with ourselves.” (This presumably referred to GM’s decades-long quest to bring rationality to its stable of brands.)

GM is not only merging with itself, it is also “disrupting” itself — as evidenced by their recently announced Chevy Bolt long-range, affordable electric car. The company claimed the Bolt was designed to be the perfect car for ride-sharing apps. Just before launching the Bolt, GM announced a $500 million investment into Lyft, the main competitor to Uber.

This no doubt surprised competitors who have been making efforts to disabuse markets and investors of the notion that they would become mere providers of hardware to ride-sharing companies like Uber or autonomous car suppliers like Google. Dieter Zetsche, CEO of Daimler, remarked “We do not plan to become the Foxconn of Apple.”

Manufacturers Are Going to Have to Invest

In fact, the bosses of Daimler, BMW, and Audi went looking behind the couch for some spare change to buy joint ownership of Nokia’s (remember them?) mapping service HERE, and did so primarily to stop their rival bidder – Uber – from buying it. High-resolution maps are crucial to autonomous cars; Uber’s CEO has said that, if Tesla can make good on their promise of a long-range, autonomous electric car, he would buy “all” of them.

The Germans are thus investing billions into electric vehicles made out of carbon fiber that pilot themselves using super-high resolution maps, all the while fighting back against Apple and Google’s requests for access to their cars’ infotainment systems. Their global leadership of the auto industry will have to be pried from their cold, dead hands.

Meanwhile, all the difficult bits of the Chevy Bolt (“custom-built” for Lyft, remember) are built in large part by Korea’s LG. One wonders why Lyft (or Uber) would not simply buy the next model directly from LG? I guess even if there is no Foxconn for cars yet, there may be soon. Remember, electric cars are far more modular than internal combustion cars.

Marchionne Says “No Thanks”

Or, if not him, then certainly the Agnelli family. A sort of Italian royalty who control Fiat Chrysler (and Marchionne) via their ownership of the Exor holding company, the Agnellis have been showing signs that they are tiring of the endless drama surrounding Fiat and the auto industry in general. They bought a stake in The Economist in 2015 in a move towards media, but the recent de-conglomeration of Fiat has been noticeable in other ways.

First, in 2013, Fiat’s industrial division was de-merged and combined with CNH Global (maker of tractors under the Case IH and New Holland brands) into a separate company, CNH Industrial. Most recently, Ferrari, the jewel in the Fiat Chrysler stable of brands, was floated in New York.

Speaking of Ferrari, Marchionne took advantage of a recent dip in the fortunes of Ferrari’s eponymous Formula 1 team to unceremoniously eject Luca di Montezemolo as president and chairman of Ferrari and replace him with . . . himself. It should be noted that di Montezemolo was appointed by Gianni Agnelli himself after the death of the founder, Enzo Ferrari, and is a bona fide business superstar in Italy. Marchionne has been playing an increasingly active part in the politics of Formula 1 recently, something that will no doubt continue to make for a less stressful (but still stimulating) retirement when Marchionne puts on his famous blue sweater for the last time in 2018.

But for now, Marchionne has seen the future. Large subcontractors will produce partially or fully autonomous electric vehicles, with the sole differences between them being brand value and design. The car makers that survive may well simply produce cars for Google (Ford recently signed an agreement along these lines), Apple, or Uber. Some, like BMW or Mercedes-Benz, may survive because of their brand and design qualities. Fiat Chrysler does not have this.

Marchionne doesn’t care about expensive gas or electric vehicles because his plan is simple:

Sell the profitable Jeep/RAM brands to another conglomerate that does not compete in these segments (for example, Hyundai KIA).

Sell the unprofitable Fiat to anyone who will take it. Perhaps synergies in the lucrative European light commercial vehicle segment will attract another European maker, such as PSA Peugeot Citroën, whose CEO, Carlos Tavares, has ambitions that were thwarted at his previous employer, Renault.

Sell Alfa Romeo and Maserati to someone who could use a strong brand. Perhaps Volkswagen will finally get hold of its prized Italian trophy if they can sort out their global legal woes.

Retire to play with his giant Formula 1 Scalextric set. Marchionne has been mocked for his firms’ strategy, which has been attributed to hubris. But perhaps he is the one seeing clearest of all.

Is the best way to deal with disruption simply to step out of the way?

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

Tit-for-Tat Competitive Analysis

Question: Who wins when–in a perfectly competitive market–competitors fight each other? Prize awarded for best answer.

May 8, 2017This Time is Not Different, Because This Time is Always Different John P. Hussman, Ph.D.

All rights reserved and actively enforced. Reprint Policy

“History repeats – the argument for abandoning prevailing valuation methods regularly emerges late in a bull market, and typically survives until about the second down-leg (or sufficiently hard first leg) of a bear. Such arguments have included the ‘investment company’ and ‘stock scarcity’ arguments in the late 20’s, the ‘technology’ and ‘conglomerate’ arguments in the late 60’s, the nifty-fifty ‘good stocks always go up’ argument in the early 70’s, the ‘globalization’ and ‘leveraged buyout’ arguments in 1987 (and curiously, again today), and the ‘tech revolution’ and ‘knowledge-based economy’ arguments in the late 1990’s. Speculative investors regularly create ‘new era’ arguments and valuation metrics to justify their speculation.”

– John P. Hussman, Ph.D., New Economy or Unfinished Cycle?, June 18, 2007. The S&P 500 would peak just 2% higher in October of that year, followed by a collapse of more than -55%.

“Old ways of valuing stocks are outdated. A technological revolution has created opportunities for continued low inflation, expanding profits and rising productivity. Thanks to these factors, the United States may be able to enjoy an extended period of expanding stock prices. Jumping out now would leave you poorer than you might become if you have some faith.”

– Los Angeles Times, May 11, 1999. While it’s tempting to counter that the S&P 500 would rise by more than 12% to its peak 10 months later, it’s easily forgotten that the entire gain was wiped out in the 3 weeks that followed, moving on to a 50% loss for the S&P 500 and an 83% loss for the tech-heavy Nasdaq 100..

“Stock prices returned to record levels yesterday, building on the rally that began in late trading on Wednesday… ‘It’s all real buying’ [said the head of index futures at Shearson Lehman Brothers], ‘The excitement here is unbelievable. It’s steaming.’ The continuing surge in American stock prices has produced a spate of theories. [The] chief economist of Kemper Financial Services Inc. in Chicago argued in a report that, contrary to common opinion, American equities may not be significantly overpriced. For one thing, [he] said, ‘The market may be discounting a far-larger rise in future corporate earnings than most investors realize is possible, [and foreign investment] may be altering the traditional valuation parameters used to determine share-price multiples.’ He added, ‘It is quite possible that we have entered a new era for share price evaluation.’”

– The New York Times, August 21, 1987 (the S&P advanced by less than 1% over the next 3 sessions, and then crashed)

“The failure of the general market to decline during the past year despite its obvious vulnerability, as well as the emergence of new investment characteristics, has caused investors to believe that the U.S. has entered a new investment era to which the old guidelines no longer apply. Many have now come to believe that market risk is no longer a realistic consideration, while the risk of being underinvested or in cash and missing opportunities exceeds any other.”

– Barron’s Magazine, February 3, 1969. The bear market that had already quietly started in late-1968 would take stocks down by more than one-third over the next 18 months, and the S&P 500 Index would stand below its 1968 peak even 14 years later.

“The ‘new-era’ doctrine – that ‘good’ stocks (or ‘blue chips’) were sound investments regardless of how high the price paid for them — was at bottom only a means for rationalizing under the title of ‘investment’ the well-nigh universal capitulation to the gambling fever.”

– Benjamin Graham & David Dodd, Security Analysis, 1934, following the 1929-1932 collapse

“The recent collapse is the climax, but not the end, of an exceptionally long, extensive and violent period of inflation in security prices and national, even world-wide, speculative fever. This is the longest period of practically uninterrupted rise in security prices in our history… The psychological illusion upon which it is based, though not essentially new, has been stronger and more widespread than has ever been the case in this country in the past. This illusion is summed up in the phrase ‘the new era.’ The phrase itself is not new. Every period of speculation rediscovers it.”

– Business Week, November 1929. The market collapse would ultimately exceed -80%.

This time is not different, because this time is always different.

Throwing in the towel

When a boxer is taking a beating, to avoid further punishment, a towel is sometimes thrown from the corner as a token of defeat. Yet even after the towel is thrown, a judicious referee has the right to toss the towel back into the corner and allow the fight to continue.

For decades, Jeremy Grantham, a value investor whom I respect tremendously, has championed the idea, recognized by legendary value investors like Ben Graham, that current profits are a poor measure of long-term cash flows, and that it is essential to adjust earnings-based valuation measures for the position of profit margins relative to their norms. In Grantham’s words, “Profit margins are probably the most mean-reverting series in finance, and if profit margins do not mean-revert, then something has gone badly wrong with capitalism.”

He learned this lesson early on, during the collapse that followed the go-go years of the late-1960’s. Grantham once described his epiphany: “I got wiped out personally in 1968, which was the last really crazy, silly stock market before the Internet era… I became a great reader of history books. I was shocked and horrified to discover that I had just learned a lesson that was freely available all the way back to the South Sea Bubble.”

In recent weeks, Grantham has essentially thrown in the towel, suggesting “this time is decently different”:

“Stock prices are held up by abnormal profit margins, which in turn are produced mainly by lower real rates, the benefits of which are not competed away because of increased monopoly power… In conclusion, there are two important things to carry in your mind: First, the market now and in the past acts as if it believes the current higher levels of profitability are permanent; and second, a regular bear market of 15% to 20% can always occur for any one of many reasons. What I am interested in here is quite different: a more or less permanent move back to, or at least close to, the pre-1997 trends of profitability, interest rates, and pricing. And for that it seems likely that we will have a longer wait than any value manager would like (including me).”

I’ve received a flurry of requests for my views on Grantham’s shift.

My simple response is to very respectfully toss Grantham’s towel back into the corner.

Here’s why.

First, Grantham argues that much of the benefit to margins is driven by lower real interest rates. The problem here is two-fold. One is that the relationship between real interest rates and corporate profit margins is extremely tenuous in market cycles across history. Second, the fact is that debt of U.S. corporations as a ratio to revenues is more than double its historical median, leaving total interest costs, relative to corporate revenues, no lower than the post-war norm.

—

The last three months of 1999 were just about the sickest thing I’d ever seen. It was an orgy, but I simply couldn’t bring myself to buy a stock that was up $10m, hoping it would go up $15, even though it was overvalued by $100. But by choosing to sit out most of the ramp, determined to wait for the inevitable implosion, I was the Greatest Fool of All, as those around me made mind-numbing profits as, day after day. YHOO, AMZN and CGMI would gap $10 a day, immune to gravity as the Nazz, aka NASDAQ, ripped right past 3000 and didn’t even blink rocketing past 4,000. At the end of the year, the Nazz was up 83 percent, a far cry from the 5 to 7 percent stocks had returned historically. People were too busy celebrating and shouting “It’s different this time.” to realize such an adjustment was unsustainable. It is like a guy who averages five home runs a year suddenly hitting fifty. Something is not right in Mudville. —Confessions of a Wall Street Insider: A Cautionary Tale of Rats, Feds, And Banksters by Michael Kimelman

Expanding your circle of competence-Platforms and Networks

Note what Prof. Greenwald says about Amazon and Apple. If Apple is JUST a product company then I would agree, but what if Apple has network effects with its music and iPods for example?

The second major category of investments involves assets that will never produce anything, but that are purchased in the buyer’s hope that someone else – who also knows that the assets will be forever unproductive – will pay more for them in the future. Tulips, of all things, briefly became a favorite of such buyers in the 17th century.

This type of investment requires an expanding pool of buyers, who, in turn, are enticed because they believe the buying pool will expand still further. Owners are not inspired by what the asset itself can produce – it will remain lifeless forever – but rather by the belief that others will desire it even more avidly in the future.

The major asset in this category is gold, currently a huge favorite of investors who fear almost all other assets, especially paper money (of whose value, as noted, they are right to be fearful). Gold, however, has two significant shortcomings, being neither of much use nor procreative. True, gold has some industrial and decorative utility, but the demand for these purposes is both limited and incapable of soaking up new production. Meanwhile, if you own one ounce of gold for an eternity, you will still own one ounce at its end.

What motivates most gold purchasers is their belief that the ranks of the fearful will grow. During the past decade that belief has proved correct. Beyond that, the rising price has on its own generated additional buying enthusiasm, attracting purchasers who see the rise as validating an investment thesis. As “bandwagon” investors join any party, they create their own truth – for a while.

Over the past 15 years, both Internet stocks and houses have demonstrated the extraordinary excesses that can be created by combining an initially sensible thesis with well-publicized rising prices. In these bubbles, an army of originally skeptical investors succumbed to the “proof” delivered by the market, and the pool of buyers – for a time – expanded sufficiently to keep the bandwagon rolling. But bubbles blown large enough inevitably pop. And then the old proverb is confirmed once again: “What the wise man does in the beginning, the fool does in the end.”

Today the world’s gold stock is about 170,000 metric tons. If all of this gold were melded together, it would form a cube of about 68 feet per side. (Picture it fitting comfortably within a baseball infield.) At $1,750 per ounce – gold’s price as I write this – its value would be $9.6 trillion. Call this cube pile A.

Let’s now create a pile B costing an equal amount. For that, we could buy all U.S. cropland (400 million acres with output of about $200 billion annually), plus 16 Exxon Mobils (the world’s most profitable company, one earning more than $40 billion annually). After these purchases, we would have about $1 trillion left over for walking-around money (no sense feeling strapped after this buying binge). Can you imagine an investor with $9.6 trillion selecting pile A over pile B?

Beyond the staggering valuation given the existing stock of gold, current prices (In 2011, gold traded at an average price of $1,700 in $US) make today’s annual production of gold command about $160 billion. Buyers – whether jewelry and industrial users, frightened individuals, or speculators – must continually absorb this additional supply to merely maintain an equilibrium at present prices.

A century from now the 400 million acres of farmland will have produced staggering amounts of corn, wheat, cotton, and other crops – and will continue to produce that valuable bounty, whatever the currency may be. Exxon Mobil will probably have delivered trillions of dollars in dividends to its owners and will also hold assets worth many more trillions (and, remember, you get 16 Exxons). The 170,000 tons of gold will be unchanged in size and still incapable of producing anything. You can fondle the cube, but it will not respond.

Admittedly, when people a century from now are fearful, it’s likely many will still rush to gold. I’m confident, however, that the $9.6 trillion current valuation of pile A will compound over the century at a rate far inferior to that achieved by pile B.

Our first two categories enjoy maximum popularity at peaks of fear: Terror over economic collapse drives individuals to currency-based assets, most particularly U.S. obligations, and fear of currency collapse fosters movement to sterile assets such as gold. We heard “cash is king” in late 2008, just when cash should have been deployed rather than held. Similarly, we heard “cash is trash” in the early 1980s just when fixed-dollar investments were at their most attractive level in memory. On those occasions, investors who required a supportive crowd paid dearly for that comfort.

My own preference – and you knew this was coming – is our third category: investment in productive assets, whether businesses, farms, or real estate. Ideally, these assets should have the ability in inflationary times to deliver output that will retain its purchasing-power value while requiring a minimum of new capital investment. Farms, real estate, and many businesses such as Coca-Cola, IBM and our own See’s Candy meet that double-barreled test. Certain other companies – think of our regulated utilities, for example – fail it because inflation places heavy capital requirements on them. To earn more, their owners must invest more. Even so, these investments will remain superior to nonproductive or currency-based assets.

Whether the currency a century from now is based on gold, seashells, shark teeth, or a piece of paper (as today), people will be willing to exchange a couple of minutes of their daily labor for a Coca-Cola or some See’s peanut brittle. In the future the U.S. population will move more goods, consume more food, and require more living space than it does now. People will forever exchange what they produce for what others produce.

Our country’s businesses will continue to efficiently deliver goods and services wanted by our citizens. Metaphorically, these commercial “cows” will live for centuries and give ever greater quantities of “milk” to boot. Their value will be determined not by the medium of exchange but rather by their capacity to deliver milk. Proceeds from the sale of the milk will compound for the owners of the cows, just as they did during the 20th century when the Dow increased from 66 to 11,497 (and paid loads of dividends as well). Berkshire’s goal will be to increase its ownership of first-class businesses. Our first choice will be to own them in their entirety – but we will also be owners by way of holding sizable amounts of marketable stocks. I believe that over any extended period of time this category of investing will prove to be the runaway winner among the three we’ve examined. More important, it will be by far the safest.

CSInvesting: I agree with all the above except that comparing gold as an investment to productive companies is not comparing like-with-like. Of course, owning a highly productive company or business that can compound over time will beat a sterile asset like cash or gold, but even Buffett will hold cash if he can’t buy great businesses at a good price. Gold is “money” that can’t be created by governments—by fiat.

If you enjoy learning about management (founders beat bureacrats every time) and business–especially one of the greatest franchises of all time–then this movie is for you:

This address considers the epidemiology of narratives relevant to economic fluctuations. The human brain has always been highly tuned towards narratives, whether factual or not, to justify ongoing actions, even such basic actions as spending and investing. Stories motivate and connect activities to deeply felt values and needs. Narratives “go viral” and spread far, even worldwide, with economic impact. The 1920-21 Depression, the Great Depression of the 1930s, the so-called “Great Recession” of 2007-9 and the contentious political-economic situation of today, are considered in view of the popular narratives of their respective times. Though these narratives are deeply human phenomena that are difficult to study in a scientific manner, quantitative analysis may help us gain a better understanding of these epidemics in the future.

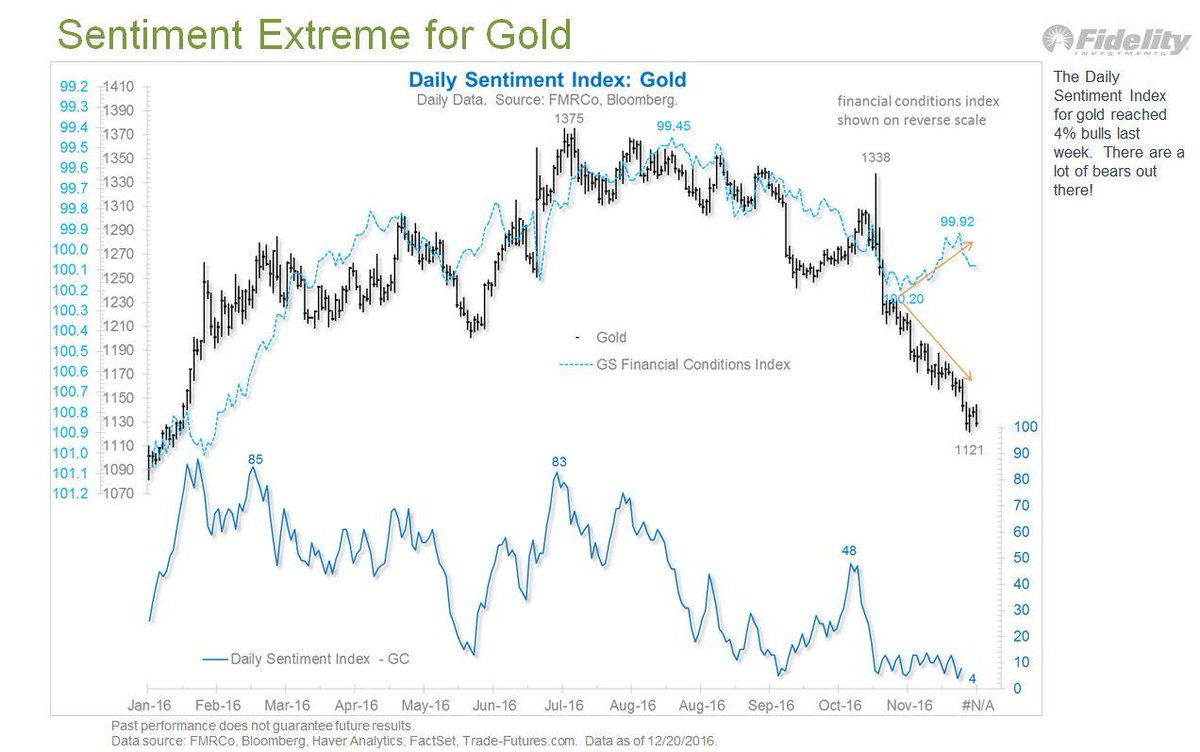

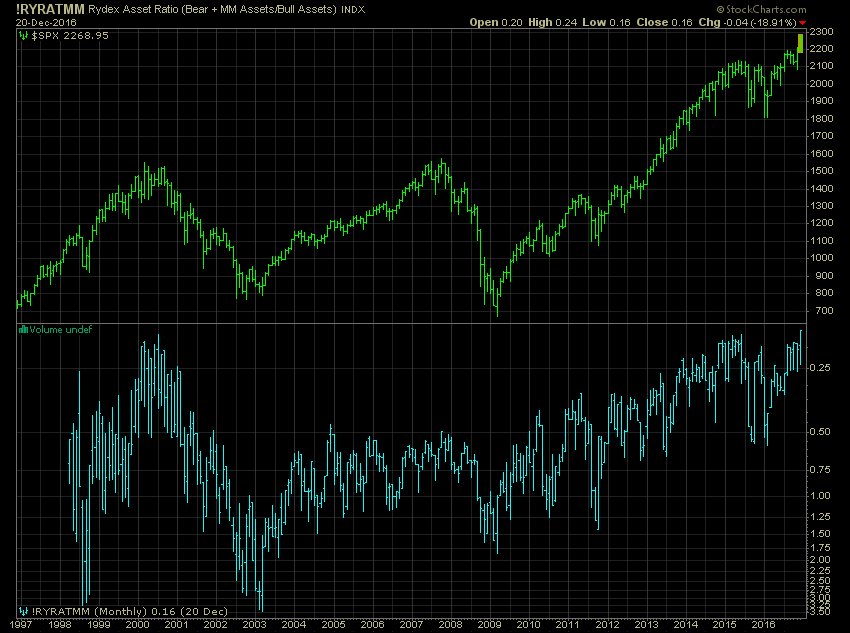

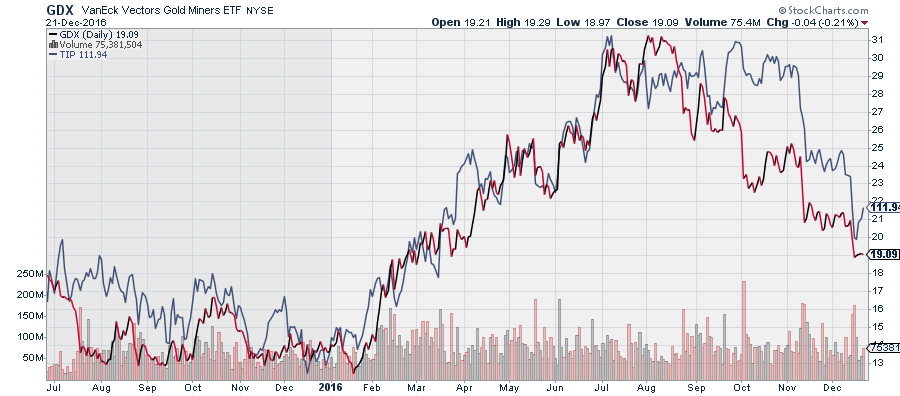

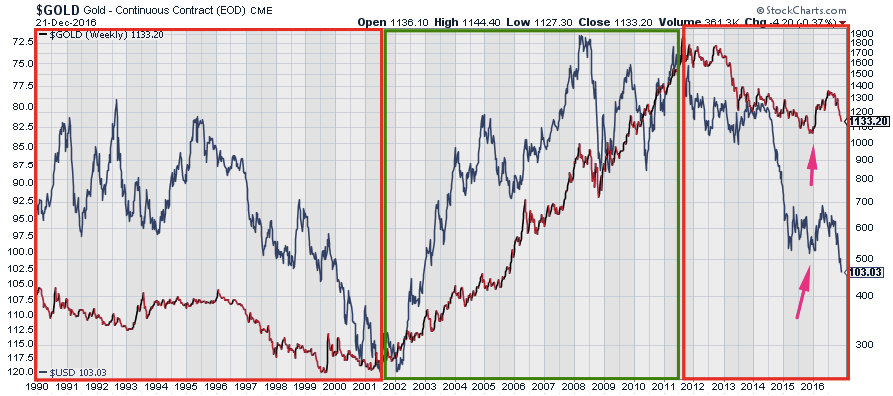

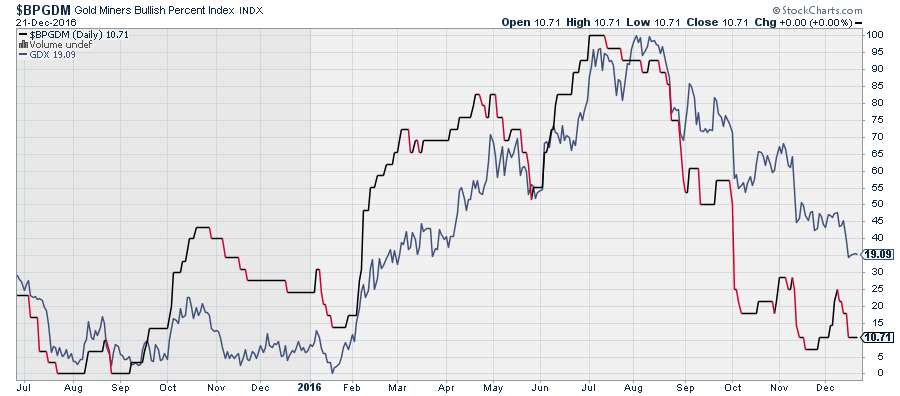

I like to have a reference to refer back to a year or five years from now capturing certain points in time. The market seems to be placing peak confidence in financial assets (stocks) vs. gold.

Even bullish mining investors expect “waterfall declines” and gold going below $1,100. Momentum creates the news: http://www.kitco.com/news/video/show/Gold–Silver-Outlook-2017/1456/2016-12-22/Mining-Stocks-Could-See-Waterfall-Declines—David-Erfle To be fair, he is long-term bullish, but note the “certainty, inevitability” of gold falling in USD below $1,100 or even to $1,000. Since he is probably considered strong hands (better capitalized with more experience in precious metals miners) his view indicates VERY bearish near-term (1 day to two/three months sentiment). As I interprete this news.

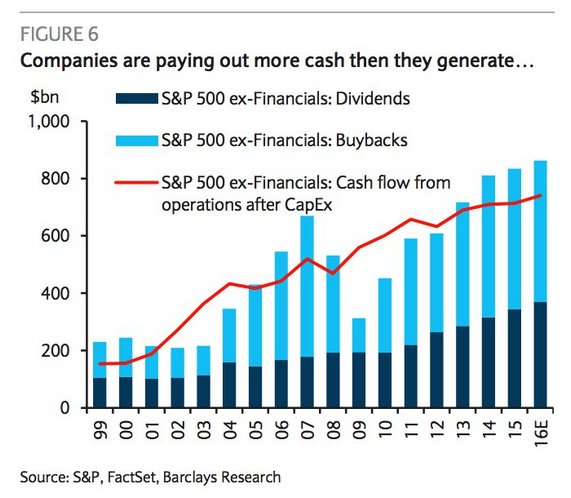

Financial risk is increasing on US company balance sheets, but then who cares while confidence is high?

—

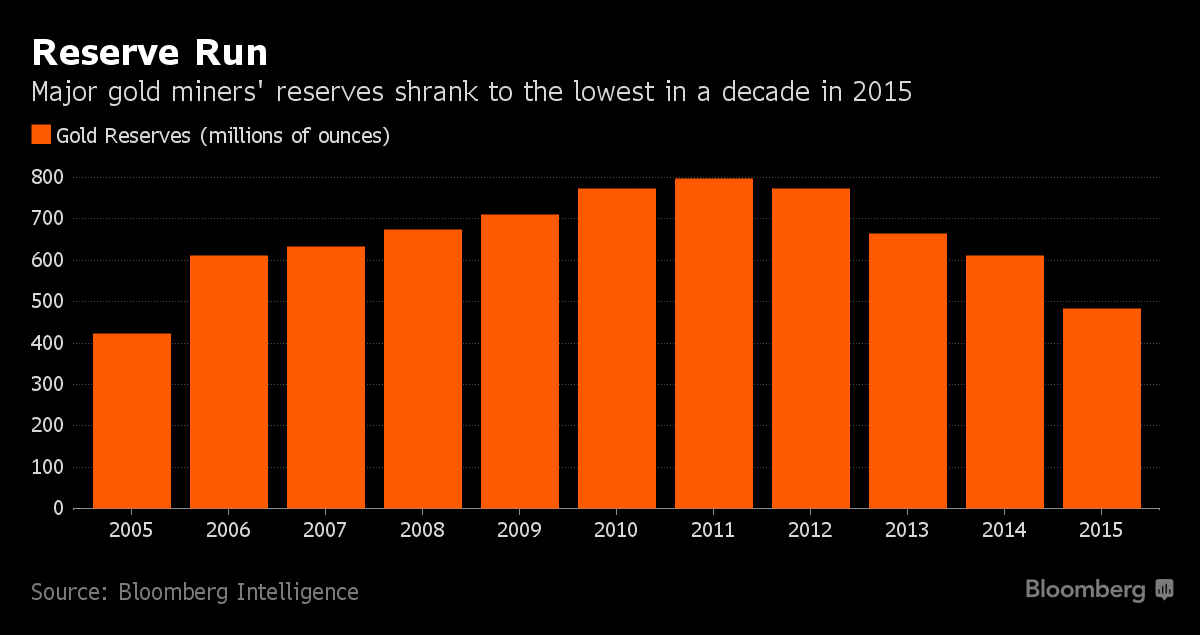

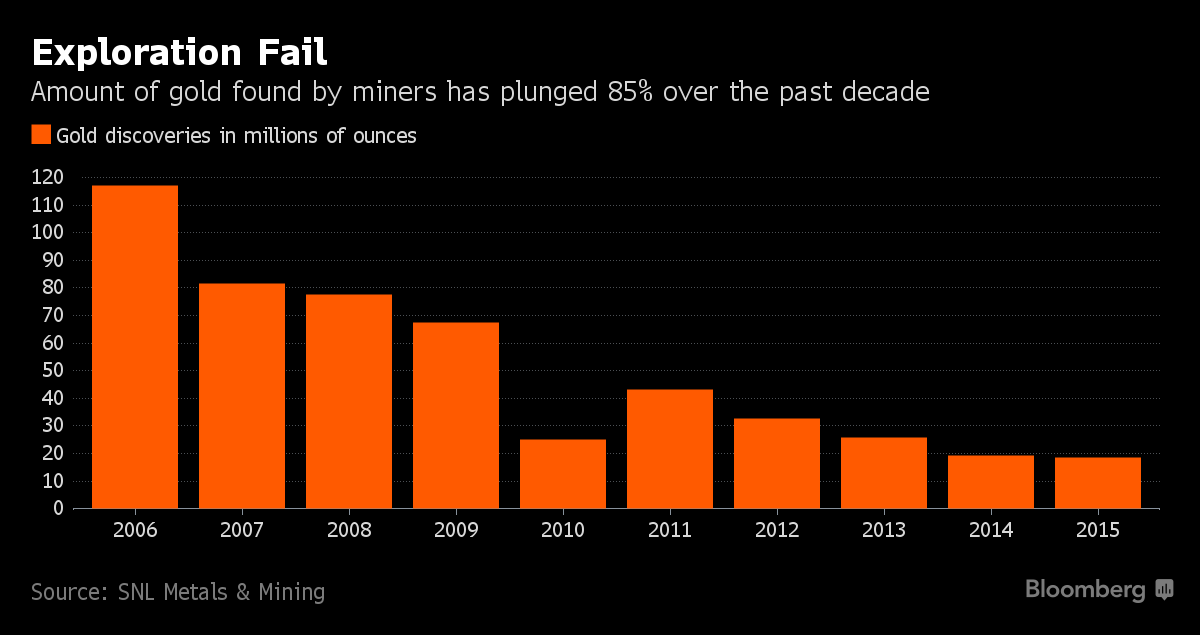

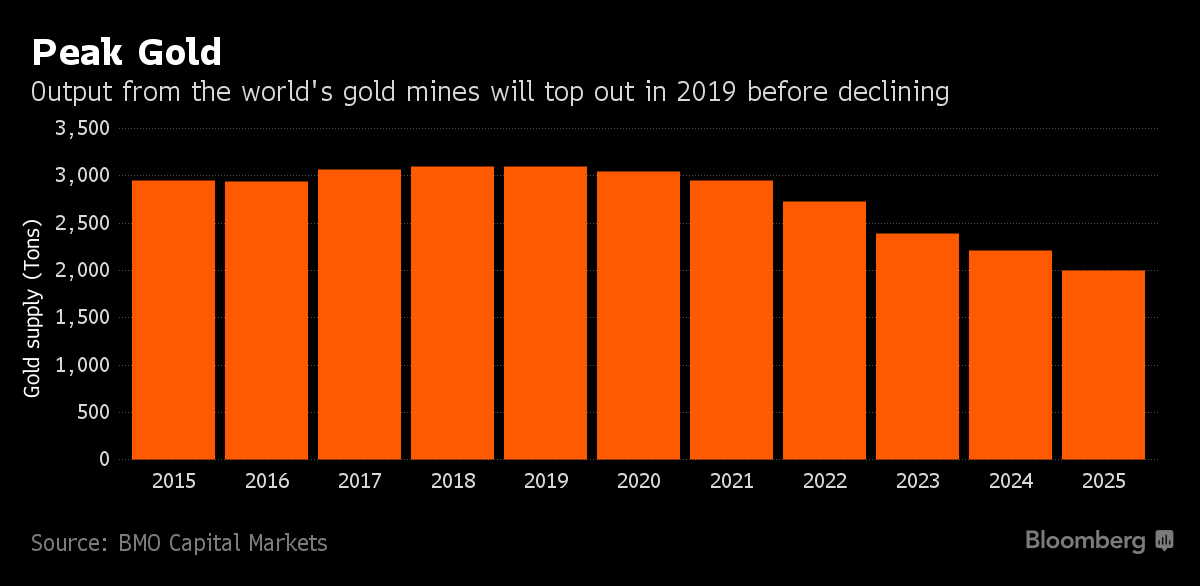

As an investor, you want to monitor the amount of capital (especially in a capital intensive business!) going into and out of a business. An industry starved of capital augurs well for future returns!

–

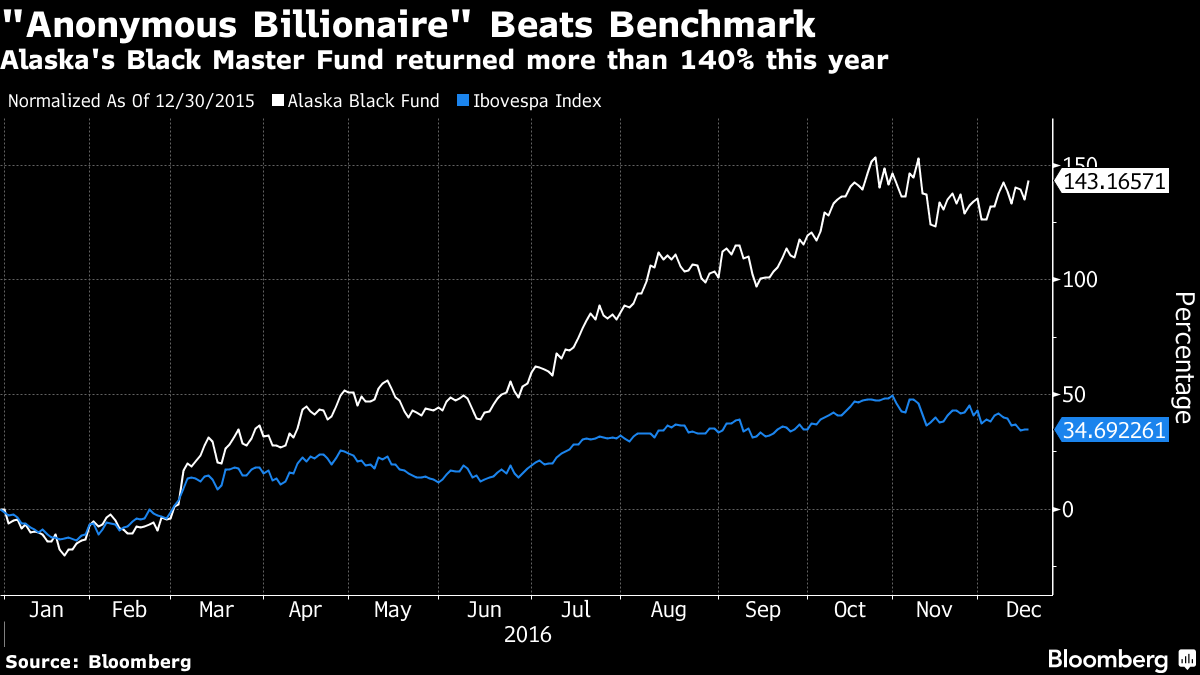

‘Anonymous Billionaire’ in the Spotlight After 1,000% Rally

by Paula Sambo and Jessica Brice

Alaska fund is No.2 fund focused on Brazilian equities

Barros’s fund is now buying up Fibria, Marcopolo, Vale

Luiz Alves Paes de Barros is something of an enigma in Sao Paulo’s financial circles. At 69, he’s known around town as the “anonymous billionaire” for quietly amassing a fortune by wagering on stocks almost no one else seemed to want.

In Magazine Luiza SA, Barros may have made one of his best bets yet.

Starting in late 2015, Barros’s Alaska Investimentos Ltda. made the battered retailer one of its biggest holdings, a brazen move in a nation stuck in the middle of its worst recession in a century. It paid off. Magazine Luiza has surged more than 1,000 percent since reaching a record low about a year ago, making it the top stock in one of the world’s top-performing markets. That turned Alaska’s Black Master, which Barros co-manages with Henrique Bredda and Ney Miyamoto, into the No. 2 fund among 569 peers focused on Brazilian equities, according to data compiled by Bloomberg.

Barros’s latest success only adds to the intrigue surrounding one of Brazil’s most storied, but media-shy, individual investors. Early in his career, he traded commodities and was a partner of star fund manager Luis Stuhlberger at what is now Credit Suisse Hedging-Griffo. Barros then spent the next half century investing only his own cash, almost exclusively in Brazilian stocks, and regulatory filings show he personally holds 1.2 billion reais in equities.

When it comes to managing other people’s money, Barros is a rookie, having co-founded Alaska in July 2015. But his investing method remains the same. He only holds a handful of stocks, favors companies with bottom-of-the-barrel valuations and usually jumps in as everyone else is bailing.

“Perfecting patience is all I’ve done over the past 50 years,” Barros says. “I love when things get bad. When it’s bad, I buy.”

During two interviews, first in Alaska’s shoebox office in the heart of Sao Paulo’s financial district and then at his personal office on the city’s oldest business thoroughfare, the silver-haired asset manager explained what drew him to Magazine Luiza and went over the stocks he likes now: Fibria Celulose SA, Braskem SA, Marcopolo SA and Vale SA.

“The market has forgotten these stocks,” he says.

Alaska started building a stake in petrochemicals maker Braskem about four months ago (the stock has surged 48 percent since mid-August after tumbling 20 percent this year before then) and pulpmaker Fibria a few months later. Barros likes both companies because they’re fundamentally sound — and valuations are low. Braskem’s price-to-earnings ratio is 8.3, less than half the level three years ago. Fibria’s valuation is less than half the average of the past two years.Marcopolo, a maker of trucks and buses, is a play on Brazil’s rebound from recession, while miner Vale will benefit as global investors start seeking value again over safety. There’s no economic expansion in Brazil without infrastructure investments, he says.

“Vale won’t be a disaster for anyone. When iron-ore prices rise again, Vale will fly,” he said.

If those stocks return just a fraction of what Magazine Luiza did, they’d count as stellar investments. In all, Alaska acquired almost 40 percent of Magazine Luiza’s free-floating shares, regulatory filings show. In 2016’s third quarter, Alaska unloaded half its stake. What’s left of Alaska’s holdings in Magazine Luiza is now worth about 111 million reais ($33 million).

Asked how he knew Magazine Luiza would do as well as it did, he says he didn’t. “I just knew it was cheap.” The fact that the retailer of appliances and electronics had a market value of 180 million reais even though a bank had offered to pay 300 million reais for the right to offer extended guarantees on Magazine Luiza products made that clear.

“Either the bank was crazy or there was value there,” Barros says.

Alaska’s Black Master fund has returned 143 percent in 2016, compared with a 33 percent gain for Brazil’s benchmark Ibovespa stock index. The gains were also driven by a stake in Cia. de Saneamento do Parana, the water utility known as Sanepar that’s almost tripled this year.

Alaska is still a relatively small player in Brazil’s 2.38 trillion-real stock market. The asset manager employs 11 people (“That includes the lady who serves the coffee,” Barros says). While Alaska oversees about 1.6 billion reais, three-quarters of that is Barros’s own cash. But the fund is actively seeking new clients.

Why now, after 50 years of going it alone?

“Because I’m positive that the market is going to rise,” he says.

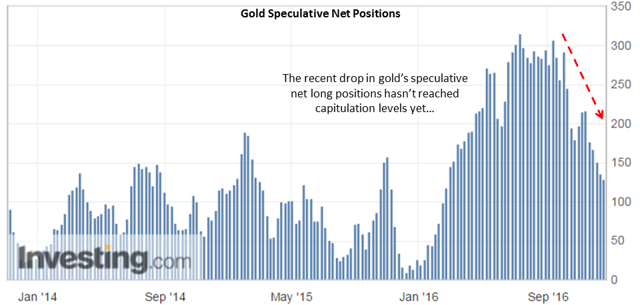

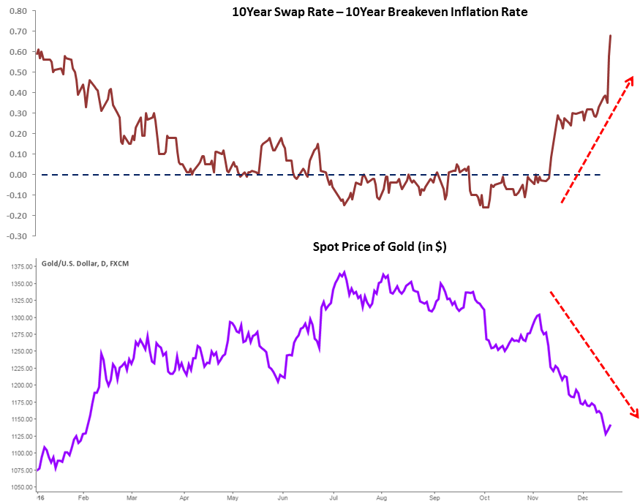

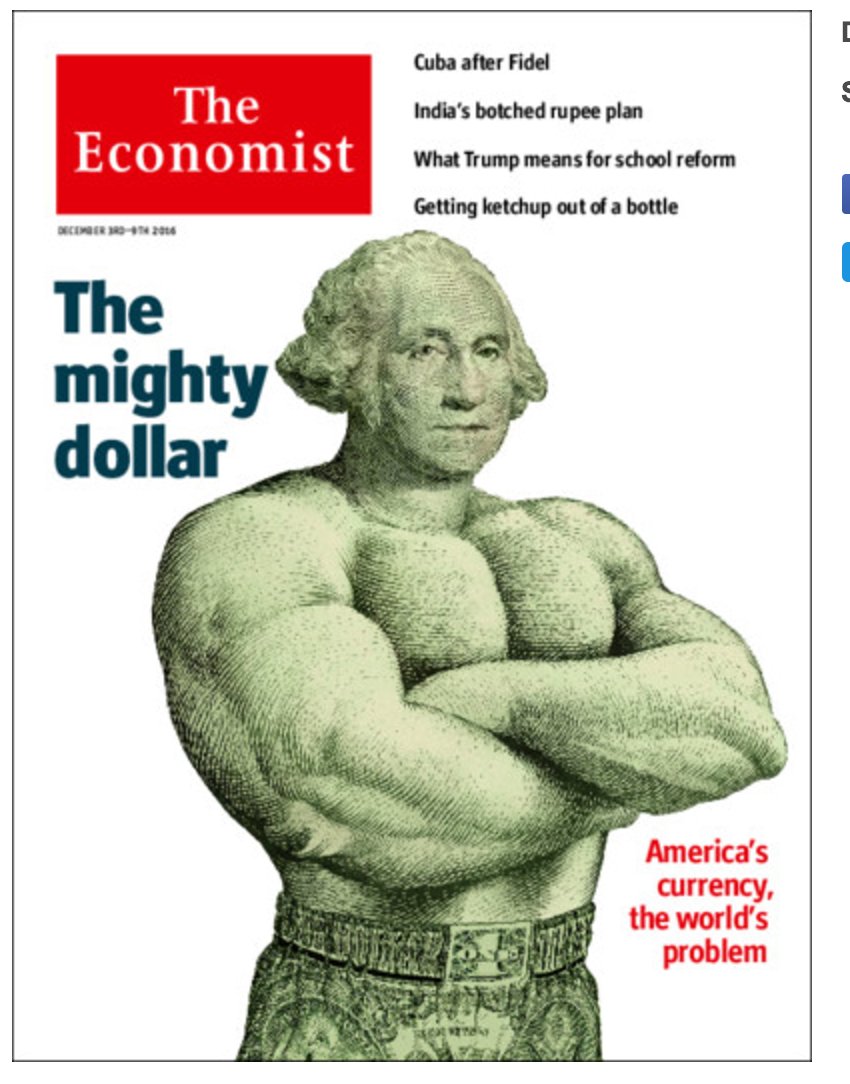

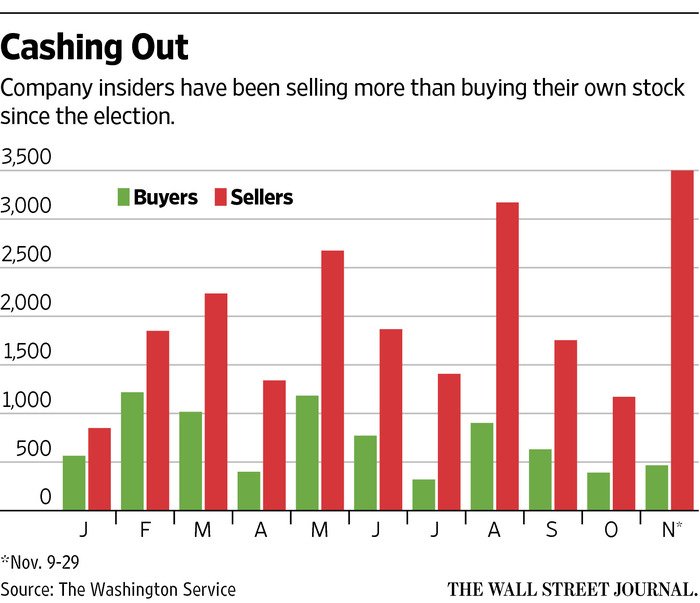

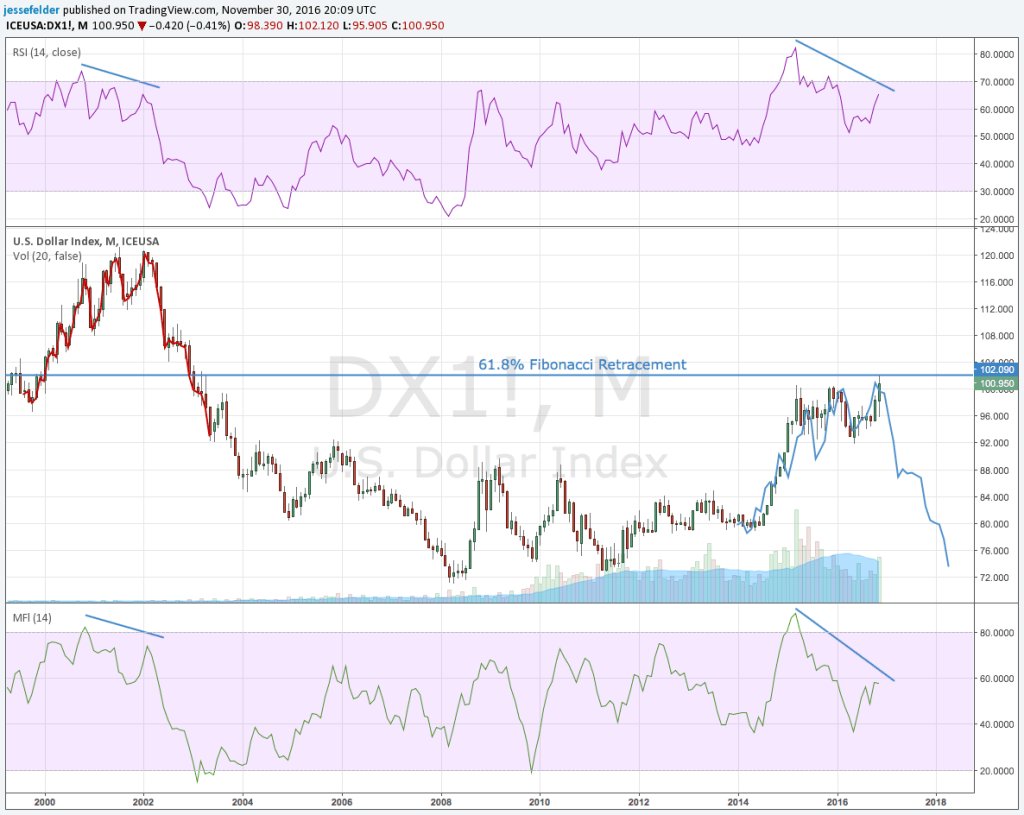

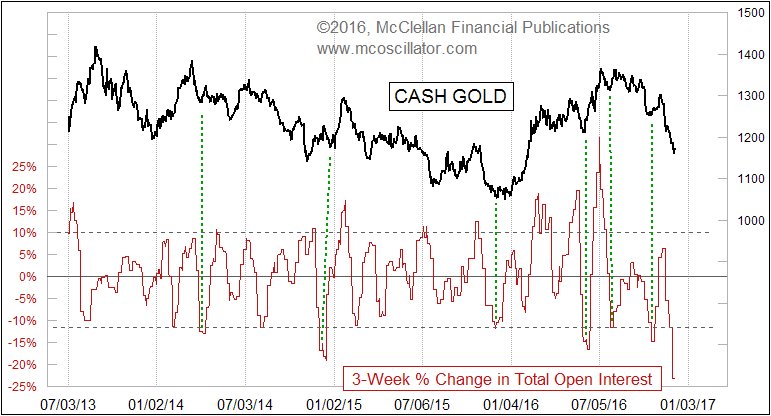

Specs liquidating at a furious pace in gold. US Dollar on the cover of the Economist, insider selling in stocks–all lend support to real asset undervaluation.

Who wants gold?

The Dow in dollar terms (yellow) and the Dow in gold terms.

Remember that you don’t have a good contrarian trade UNLESS this happens:

Indian Prime Minister Nahendra Modi has declared 500 and 1,000 rupee notes illegal for exchange. Since these are worth a mere $7.26 and $14.53, he has de facto ended paper currency for use in all major transactions.

Half the population do not have bank accounts, and consumer trade has come to a screeching halt. That is because the highest permitted denomination fetches only about one US dollar, and exchanging the larger notes requires long waits and government identification, which a quarter of Indians do not possess.

Beyond the self-inflicted economic crisis, Jayant Bhandari says India is becoming a police state. She is on a fast track to banana-republic status, before fragmentation into smaller political units.

The gold market in India is in chaos, as people rid themselves of the domestic fiat currency: the price per ounce has skyrocketed to above $2,000, and tax authorities are blocking the retailers. This means the black market is set to boom, as smugglers adapt to the new opportunity, but import demand from India has dropped momentarily, since the formal markets are under the gun.

Another dent in confidence of fiat currencies. What are YOUR thoughts. Lessons? I will pay $1 million dollars to ANYONE who can tell me how central planning helps people increase wealth over time vs. free exchange.

—

The balance between quantitative and qualitative research

“There’s so much you can tell in a 10-minute tour of a plant.

I can tell you right away whether we’re making money, if we have quality or delivery issues (so customer issues) and if there’s a morale problem. It’s easy to tell.

But you can’t tell until you go there.”

– Linda Hasenfratz, CEO Linamar Corporation, in conversation with The Women of Burgundy, September 21, 2016

One of the familiar tensions underlying the quality-value investment discipline is the balance between quantitative and qualitative research. Many investors intuitively understand the importance of assessing the quantitative aspects of a business. We analyze the numbers to understand what level of return the business is generating for its shareholders, what level of debt sits on the balance sheet, and whether the cash flows into the business are stable and recurring, for example.

While a quantitative assessment is vital to an investment decision, it is not complete without a qualitative framework to guide its meaning. For instance, it is not just the level of debt on the balance sheet that matters, but whether those debt levels are appropriate for the business. It’s not just a historical record of stable cash flows that gives us confidence, but rather an understanding of the economic moat that protects those cash flows from future competition.

It is with this background that I find Linda Hasenfratz’s quote truly compelling. As CEO of Linamar, she is responsible for running a global manufacturing business that spans 13 countries around the world. She may be able to look at the financial metrics to assess how her business is doing, but for Hasenfratz it is clear that a true, holistic understanding of the business comes from walking the halls of manufacturing plants and speaking face-to-face with her management teams around the world.

Her words were a welcome reminder about the importance of being there, on the ground, to gain a complete qualitative understanding of the operations. As I listened, I felt as if a member of our Investment Team had been dropped into her seat. Take, for instance, the excerpt below from the June 2016 issue of The View from Burgundy, “Boots on the Ground,” which brings us along on a site tour of a Chinese flavour and fragrance company’s R&D facility:

“Normally lab environments are tightly controlled, but in this case, rooms labelled ‘temperature controlled’ had open windows, letting in both the hot summer air and a fair share of local insects. What’s more, the facility was curiously devoid of employees, and the few research staff we did encounter were surly and unapproachable. It seemed odd to us that a company could have its main R&D facility in such a state of inactivity and disrepair, while reporting seemingly world-leading profitability in a highly competitive research-driven industry.

Our negative impression from the site tour provided useful information that would have been difficult, if not impossible, to acquire had we not done the on-the-ground work. It prevented us from making an investment in what had appeared on paper to be an attractive business, provided one didn’t scrutinize its operations – an example of why relying on company-produced financial statements alone is not sufficient when conducting due diligence.”

In other words, the science of investing is never complete without the art.

—

PS:

India Confiscates Gold, Even Jewelry, in Raids on Hidden Money

Large denomination means 500-rupee ($7.30) and 1,000-rupee notes ($14.60), which account for more than 85 percent of the money supply. They are no longer legal tender, effective immediately.

As one might imagine, chaos ensued. And it continues.

The chaos accompanying “demonetization” hasn’t eased up noticeably. It seems likely the disruption to the economy, especially in cash-centric rural India, will hit growth sharply for at least a few quarters. It’s tough to say for how long and by how much; we are in uncharted territory here and guesses have varied widely. But many analysts agree with former Prime Minister Manmohan Singh, who’s predicting the new policy will knock 2 percentage points off that world-beating GDP growth rate.

Demonetization was originally sold as a “surgical strike on black money”— the illicit piles of cash many rich Indians have accumulated out of sight of the taxman. It’s now clear the policy has been anything but surgical. Worse, uncomfortable questions are being asked about whether the complicated rules and exemptions that have accompanied demonetization have allowed black-money holders to launder most of their cash. Of late, Modi’s chosen to focus instead on demonetization as means of advancing a cashless economy.

Yet the idea of a war on unaccounted-for wealth remains central to demonetization’s popular appeal, which means Modi will have to find other ways to keep that narrative going. So the government has now begun to push income-tax officials to conduct raids on those who might be concealing assets in forms other than cash, such as gold.

There’s already enough fear of such raids becoming common again that the government felt the need to step in to quell some of the anxiety. That didn’t help much. The government “clarified,” among other things, the rules governing when tax officials could seize gold: Nothing would happen “if the holding is limited to 500 grams per married woman, 250 grams per unmarried woman and 100 grams per male.” It also said that there would be no limits on jewelry “provided it is acquired… from inheritance.” Also, the “officer conducting [the] search has discretion to not seize [an] even higher quantity of gold jewelry.”

What this means, unfortunately, is that India’s income tax officers have just won the lottery. During a raid, they can, on the spot, decide whether or not to confiscate a family’s gold holdings. And remember, India has an enormous amount of gold — 20,000 metric tons, much of it inherited. (The rules governing simple searches are different, but few know that.) Rather than cleaning up tax administration, the government has handed tax officials more power than they’ve had for decades. The rich will pay what they need to escape harassment; the rest will suffer.

Rich Escape, Poor and Middle Class Suffer

The last line in the preceding article says all you need to know about what’s happening: “The rich will pay what they need to escape harassment; the rest will suffer.”

Evidence suggests the politically connected, and their friends, knew about the ban on cash and acted in advance. Everyone else is stuck.

India’s raid on gold reinforces its ban on cash. Short term aside, these kinds of actions will increase demand for gold.

What’s Next?

I keep wondering: what’s next? People pretend they know, I admit I do not. However, I am quite sure a currency crisis is coming. Where it strikes first is unknown, but the list of likely candidates increases every year.

My spotlight has been on Japan, China, and the EU. India caught me off guard, but it adheres to my general theory this pot will eventually boil over in a cascade from an unexpected place, outside the US.

US actions may cause a currency crisis, but I believe a crisis will hit elsewhere first. If I am correct, gold will be the safe haven, regardless of currency, but especially where the crisis hits.