https://www.tollymorepartners.com/letters

https://www.tollymorepartners.com/insights

Spotlights

https://www.tollymorepartners.com/insights

Spotlights

Posted in Uncategorized

https://www.youtube.com/channel/UCyjyUPbLw38tG9iAw0p7nxg

Special Investigation: The Dirty Secret Behind Warren Buffett’s Billions

America’s favorite investor loves monopoly, not free markets.

By David Dayen

Surprise! Buffett craves monopolies. Who wouldn’t want to invest in them? How about helping citizens by doing away with government controlled monopolies like the US Post Office or the Fed?

Posted in Uncategorized

BUFFETT INTERVIEW on FINANCIAL CRISIS and MOODY’s Moody Analysis and Transcript-of-Warren-Buffett-Interview-With-FCIC

The Above Book is a good primer on investing. See course by the author.

http://www.advancedvalueinvestingworkshop.com/register.html

https://monetary-metals.com/category/supply-demand-report-public/

The first line of Epictetus’ manual of ethical advice, the Enchiridion—“Some things are in our control and others not”—made me feel that a weight was being lifted off my chest. For Epictetus, the only thing we can totally control, and therefore the only thing we should ever worry about, is our own judgment about what is good. If we desire money, health, sex, or reputation, we will inevitably be unhappy. If we genuinely wish to avoid poverty, sickness, loneliness, and obscurity, we will live in constant anxiety and frustration. Of course, fear and desire are unavoidable. Everyone feels those flashes of dread or anticipation. Being a Stoic means interrogating those flashes: asking whether they apply to things outside your control and, if they do, being “ready with the reaction ‘Then it’s none of my concern.’ ”

https://www.newyorker.com/magazine/2016/12/19/how-to-be-a-stoic

Barrons-interview-Bruce-Greenwald-13052017 (1)

Posted in Uncategorized

Two letters from a WWII veteran who won the Silver Star (disturbing descriptions of war) Letter 5 Silver Star Letter Feb 24th 1944

February 1, 1944 Letter rpc to Dash and Mother Flame Thrower

Facing Death

Know what you are doing IF you buy index funds! You can learn a lot by studying Horizon Kinetics. The video provides a valuation of the index and how to think about investing or not in indexes.

http://horizonkinetics.com/market-commentary/2nd-quarter-2017-commentary/

Also, more on indexing here:

Q2-2017-Commentary_APPROVED_FINAL

Posted in Free Courses, Risk Management, Uncategorized

Tagged FANG, Horizon Kinetics, Indexing

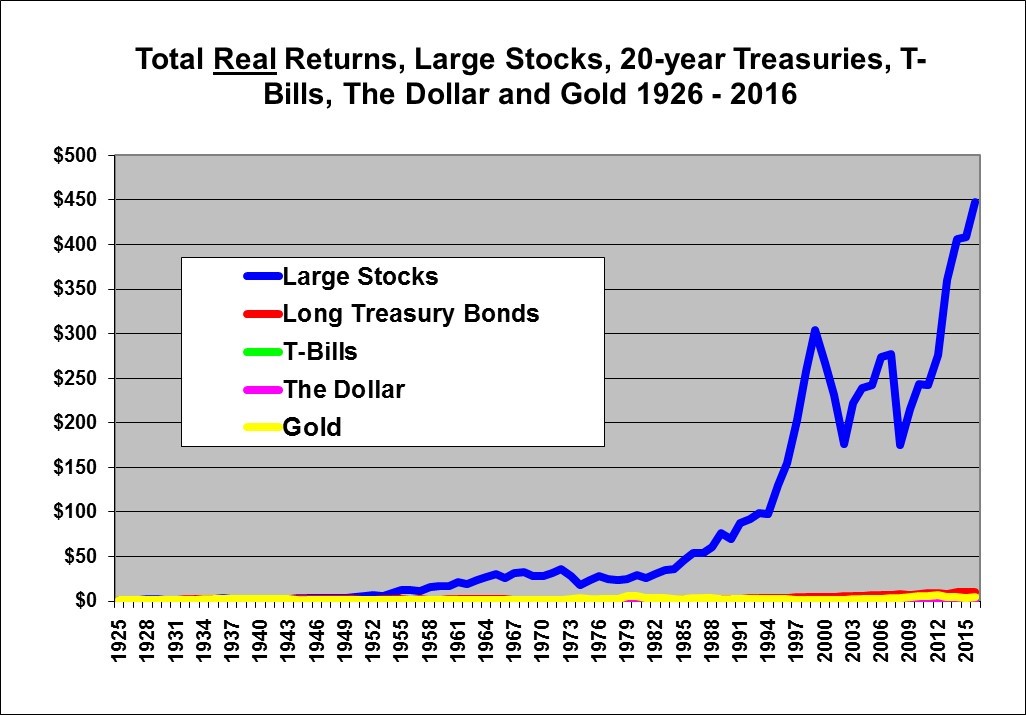

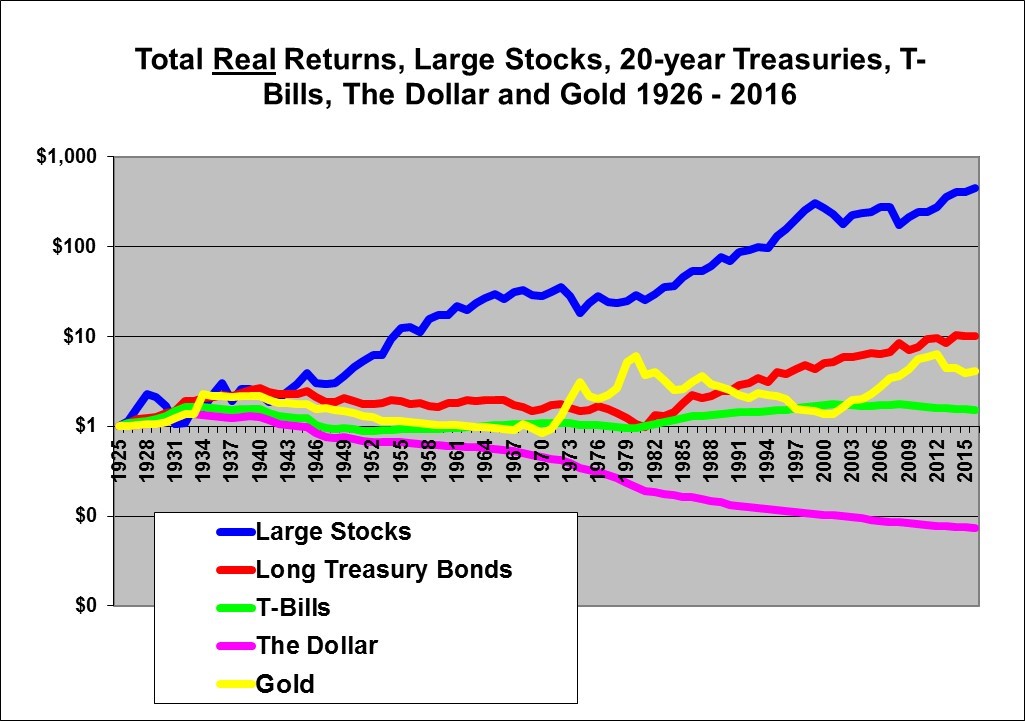

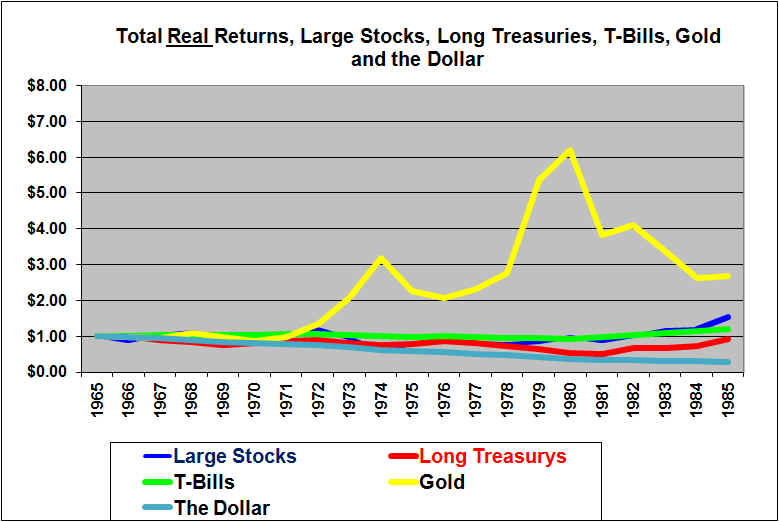

The above seems to answer the question above. But what if the returns are heavily skewed to only a few stocks? Look deeper: Bessembinder Do Stocks Outperform Treasury Bills

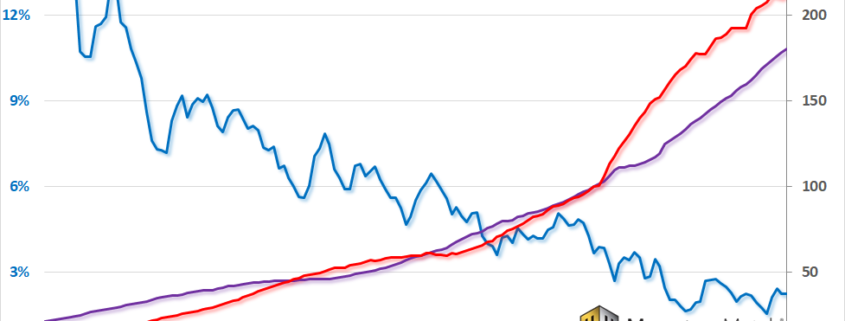

The chart above shows gold “outperforming” stocks, but note the time period. 1971 was when President Nixon unhinged the dollar from gold. Be careful when assessing performance over a set time period.

Posted in Uncategorized

Hunt for value in high priced stocks: http://otcadventures.com/?p=1912

Posted in Search Strategies, Uncategorized

Tagged Bruce Lee, High Priced Stocks, Search Strategy, Shorting

The Little Newsletter That Crushed the Market

The Prudent Speculator has more than tripled the broad stock market since 1980. What’s its secret?

Feb. 23, 2017 5:48 a.m. ET

|

|

It pays to have nerves of steel.

That’s the most important lesson to emerge from the Prudent Speculator’s position as one of this country’s most successful investment newsletters of the past four decades.

The advisory service, which celebrates its 40th birthday March 10, has pursued a riskier strategy than almost all other newsletters—far riskier than many investors can tolerate. But those who could and did were richly rewarded. Its advice has made more money over the past 40 years than any of the nearly 200 other services monitored by the Hulbert Financial Digest.

CSInvestor: the author defines risk as volatility!

Since mid-1980, when we began monitoring the investment newsletter industry, through the end of January, the Prudent Speculator’s model portfolios on average produced a 16,937% gain, versus 4,952% for buying and holding the broad stock market (as measured by the Wilshire 5000 index).

That’s equivalent to the difference between 15.1% and 11.3%, annualized. (These performance numbers assume all model-portfolio transactions were executed on the day a subscriber would have been able to act on the newsletter’s advice; dividends and transaction costs, but not taxes, were taken into account.) To put this into perspective, consider that the best-performing U.S. equity mutual fund over this same period produced an annualized return of 13.6%, or 1.5 percentage points per year less than the Prudent Speculator. (The fund, according to Thomson Reuters Lipper, was Waddell & Reed Advisors Science & Technology [ticker: UNSCX]).

The Prudent Speculator newsletter, which was founded in March 1977 by Al Frank and is based in Aliso Viejo, Calif., was initially named the Pinchpenny Speculator. Frank had become interested in investing several years earlier while working toward his Ph.D. in educational philosophy at the University of California, Los Angeles. He started the newsletter in part to report on the performance of his personal portfolio. From the start, his strategy was to purchase undervalued stocks and hold them through for the very long term. The newsletter’s current yearly subscription rate is $295.

In the 1990s, Frank—who died in 2002—began handing the newsletter over to an associate, John Buckingham, now 51, who had been with the firm since 1987. The transition to Buckingham has been unusually successful; the norm in the newsletter business is for services to either languish or close down completely upon the death of their founders. Not in this case. On a risk-adjusted basis, the newsletter’s model portfolios have performed even better over the past two decades than in the first two.

It’s definitely not market timing, since it has actively argued against market timing throughout its history. Most commentators assume that the newsletter must owe its success to superior stock selection. But though the newsletter’s stock-picking has been commendable, many other advisors favor stocks with similar characteristics.

|

Not for the Faint of Heart

Source: www.HulbertRatings.com |

Recent examples of the newsletter’s picks include Zimmer Biomet Holdings (ZBH),Williams-Sonoma (WSM), Nike (NKE), Schlumberger (SLB), and Digital Realty Trust (DLR). In an interview, Buckingham insisted that he pursues value wherever he can find it. But my computer’s statistical software shows that the newsletter’s recommended stocks tilt to the value end of the value-versus-growth spectrum and the quality end of the so-called quality-versus-junk spectrum, and tend to have smaller market values than the components of broad market averages such as the Standard & Poor’s 500 index.

If neither market timing nor stock selection is the key to the Prudent Speculator’s outstanding long-term record, what is? In my opinion, it’s those nerves of steel I referred to above.

Almost all other advisors who recommend smaller-cap, higher-quality value stocks are unwilling to hold them through thick and thin. Though these value-oriented advisers have longer holding periods than most others, their average currently is 18 months. The average holding period of the Prudent Speculator’s currently held stocks, by contrast, is four years. And there have been many times during the newsletter’s history when its average holding period was even longer than four years. Its current holding period is this short because the market’s extraordinary strength has propelled many of its previously recommended stocks above their target prices.

By selling out too early, Buckingham told Barron’s, other advisors find themselves with either one or two strikes against them. The first strike applies even if those advisors immediately reinvest the proceeds of their premature sales in other undervalued stocks: They still leave too much money on the table, since

The second strike is when advisors go to cash after selling. These advisors often end up bailing out of stocks near the bottom of bear markets. Because it almost always takes them a long time to get back into equities after the market begins to recover, they enjoy only some of the market’s recovery after suffering the bulk of its decline—and therefore lag the market over the long term.

By not deviating from its commitments to equities, the Prudent Speculator sidesteps both of these strikes.

Consider Frank’s reaction to the 1987 crash—the biggest one-day drop in U.S. stock-market history, during which Frank’s model portfolio lost nearly 60%. Far from cashing in his chips and going home, as most of us would have been tempted to do in the wake of a one-day loss that big, Frank said he saw no reason to alter the basics of his long-term strategy.

Similarly, consider Buckingham’s advice to clients on March 9, 2009, the day that turned out to be the bottom of the 2007-09 bear market—though of course no one at that time could have known that. Buckingham’s average model portfolio was sitting with a loss of more than 60% since the 2007 high, and yet his message to clients that day—as it had been every other day during that bear market—was that “our long-term enthusiasm [for stocks] remains intact.”

Many investors no doubt find it boring to remain fully invested to stocks through thick and thin and to hold stocks for many years. In fact, Buckingham says, one of the most challenging parts of his job as newsletter editor is continually finding new and interesting ways of saying the same thing: Remain focused on the long term with patience and discipline.

Easier said than done–90% of investing is character.

Note: He leans toward smaller (more apt to be mispriced) stocks, value more than growth (so he faces lest risk of overpaying for growth), quality over junk (so less chance of bankruptcy risk), and then allows AT LEAST four years for value to come out or be recognized. His edge is his patient, long-term perspective.

Recent Munger Transcript 340444245-Munger-2017-DJCO-Transcript340444245-Munger-2017-DJCO-Transcript

Posted in Investing Gurus, Investor Psychology, Uncategorized, YOU

Tagged charlie munger

{kind=link}