Please put a check mark by the letter you choose or write it down next to the number of the question.

You will be compared to a Chimp who—on each question—will be thrown bananas labeled A, B, or C.

The Chimp will answer correctly about 33% of the questions.

GOOD LUCK!

In all low-income countries across the world today, how many girls finish primary school?

A. 20 percent

B. 40 percent

C. 60 percent

Where does the majority of the world population live?

A. low-income countries

B. middle-income countries

C. high-income countries

In the last 20 years, the proportion of the world population living in extreme poverty has….

A. Almost doubled

B. Remained more or less the same

C. Almost halved

What is the life expectancy of the world today?

A. 50 years

B. 60 years

C. 70 years

There are 2 billion children in the world today, aged 0 to 15 years old. How many children will there be in the year 2100, according to the United Nations?

A. 4 billion

B. 3 billion

C. 2 billion

The UN predicts that by 2100 the world population will have increased by another 4 billion. What is the main reason?

A. There will be more children age below 15

B. There will be more adults age 15 to 74

C. There will be more very old people aged 75 and older.

How did the number of deaths per year from natural disasters change over the last hundred years?

A. More than doubled

B. Remained about the same

C. Decreased to less than half

How many of the world’s 1-year-old children today have been vaccinated against some disease?

A. 20 percent

B. 50 percent

C. 80 percent

9 World-wide, 30-year-old men have spent 10 years in school, on average, how many years have women of the same age spent in school?

A. 9 years

B. 6 years

C. 3 years

10 In 1996, tigers, giant pandas, and black rhinos were all listed as endangered. How many of these three species are more critically endangered today?

A. Two of them

B. One of them

C. None of them

11. How many people in the world have some access to electricity?

A. 20 percent

B. 50 percent

C. 80 percent

Global climate experts believe that, over the next 100 years, the average temperature will……

A. Get warmer

B. Remain the same

C. Get colder

Email: Aldridge56@aol.com with the subject heading: CHIMPSand I will email you the answers. Did you beat the chimps?

A reader shares his investment conference in Cyprus

I wonder if this crowd could beat the chimps? Bets?

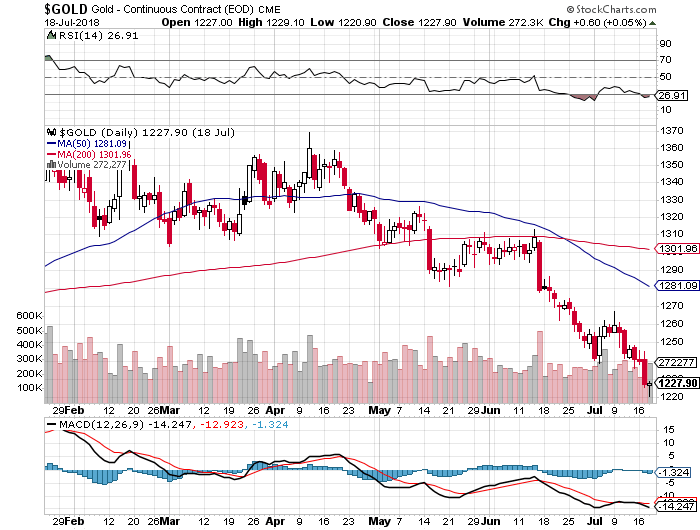

On April 11, 2018, the price of gold in US Dollars was $1,370. This morning on July 19th, the price was $1,2110.90 for a decline of $159 in 99 days. If current trends continue, then in 712 days or less than two years, the Gold price in USD terms will be about $0.00. The trend is your friend!

The single greatest mistake investors make is to extrapolate recent history out into the future. They take the financial returns of the past 5 days or 5 years or even 50 years and assume the next few days or years will look just the same without any consideration for the historical context or conditions that provided for those returns.

They forget that, while ‘history may rhyme, it doesn’t repeat itself’ (Twain). Or that, “the only thing that is constant is change” (Heraclitus). These two famous quotes apply to the financial markets as much as anything.

Ignoring these truths and instead simply extrapolating is why investors are suckered into pouring money into the stock market only after a run of great performance. They believe that the recent gains are about to repeat to their great benefit when they should be thinking about what conditions allowed for those gains to take place and analyzing whether they are still relevant or not.

This is also why they are suckered into selling only after a painful decline as they did at the lows made during the financial crisis. They believe that they are about to suffer another 50% decline on top of the one they just endured when they should really be reminding themselves that change is the only guarantee in life.

I believe this is one of the biggest problems with so-called “passive” investing. It is built upon the faulty premise that it is ‘impossible to forecast’ the future returns of any asset class over any period of time so we should just own all of them all the time. My response to this is that while ‘ignorance may be bliss’ it’s not a valid investment strategy.

In his 1992 letter to Berkshire Hathaway shareholders, Warren Buffett wrote:

We’ve long felt that the only value of stock forecasters is to make fortune tellers look good. Even now, Charlie and I continue to believe that short-term market forecasts are poison and should be kept locked up in a safe place, away from children and also from grown-ups who behave in the market like children. However, it is clear that stocks cannot forever overperform their underlying businesses, as they have so dramatically done for some time, and that fact makes us quite confident of our forecast that the rewards from investing in stocks over the next decade will be significantly smaller than they were in the last.

Much can be learned from this short passage. First, short-term stock market forecasts are, indeed, nearly worthless – essentially a guessing game. Second, long-term forecasts, on the other hand, can be made with ‘confidence.’ “How?” you ask.

It’s actually very simple. Rather than fixate on recent history and extrapolate it into the future you must abandon this natural tendency. And as I said earlier you also need to analyze the conditions that allowed for those returns to see whether they are still relevant to today’s market.

In Buffett’s example he’s referring to the wonderful returns equity investors experienced from 1982-1992. During that span investors roughly quadrupled their money. Over the coming decade they merely doubled their money so Buffett was right that the decade beginning in 1993 would fall far short of the return of the prior decade even if they were still very good.

sc-22

But Buffett made another prescient forecast in November 1999 when he wrote:

Today, staring fixedly back at the road they just traveled, most investors have rosy expectations. A Paine Webber and Gallup Organization survey released in July shows that the least experienced investors–those who have invested for less than five years–expect annual returns over the next ten years of 22.6%. Even those who have invested for more than 20 years are expecting 12.9%. Now, I’d like to argue that we can’t come even remotely close to that 12.9%… you need to remember that future returns are always affected by current valuations and give some thought to what you’re getting for your money in the stock market right now.

You probably already know that stock market returns from 1999 to 2009 were not very kind to investors.

And Buffett tells us how he was so confident that this would be the case. He examined the conditions that allowed for returns to be so wonderful from 1982-1999 but were no longer present in 1999: wonderful valuations. Stocks were so cheap in 1982 that the coming decade was virtually guaranteed to be better than the decade that preceded it. (1972-1982 was another decade that was not fun for investors.) Then in 1999 valuations were so expensive that there was almost no possibility of decent returns going forward.

So let’s take a look at Buffett’s favorite valuation yardstick which he refers to on both of those prior writings. It tracks the total value of the stock market in relation to Gross National Product.

From the chart, it’s plain to see that valuations were extremely attractive back in the early 1980’s. This is why stocks performed so well over the next 20 years. However, I find it absolutely fascinating that stock market valuations today are essentially equivalent to valuations in November 1999 when he wrote that latter passage. Yeah, go back and read that last line again. It’s a doozy and it’s absolutely fact.

This is also why the past 5 years or even the past 50 years are totally irrelevant to equity investors in today’s market. There is almost zero possibility today of achieving a return anywhere close to what those historical returns represent. So shun forecasts if you want. Plead ignorance if it makes you feel blissful. But at today’s valuations you should at least be aware of the fact that it’s exceedingly dangerous to fall into the trap of extrapolating without analyzing.

What The Buy-And-Hold Cult Doesn’t Want You To Know

Buy-and-hold, and all of its related strategies like BTFD, garnered a cult following a long time ago and it’s only gotten even more popular in recent years. (There may be no better evidence of this than the StockTwits merch store – which I love, btw). And after one of the longest and strongest equity bull markets in history this should not come as any surprise. Investors are always influenced by recency bias and prone to extrapolation.

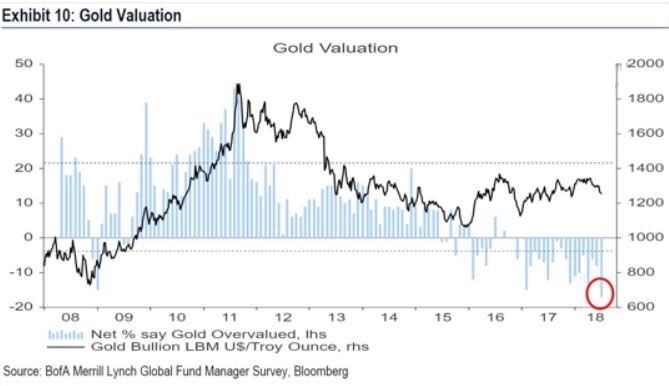

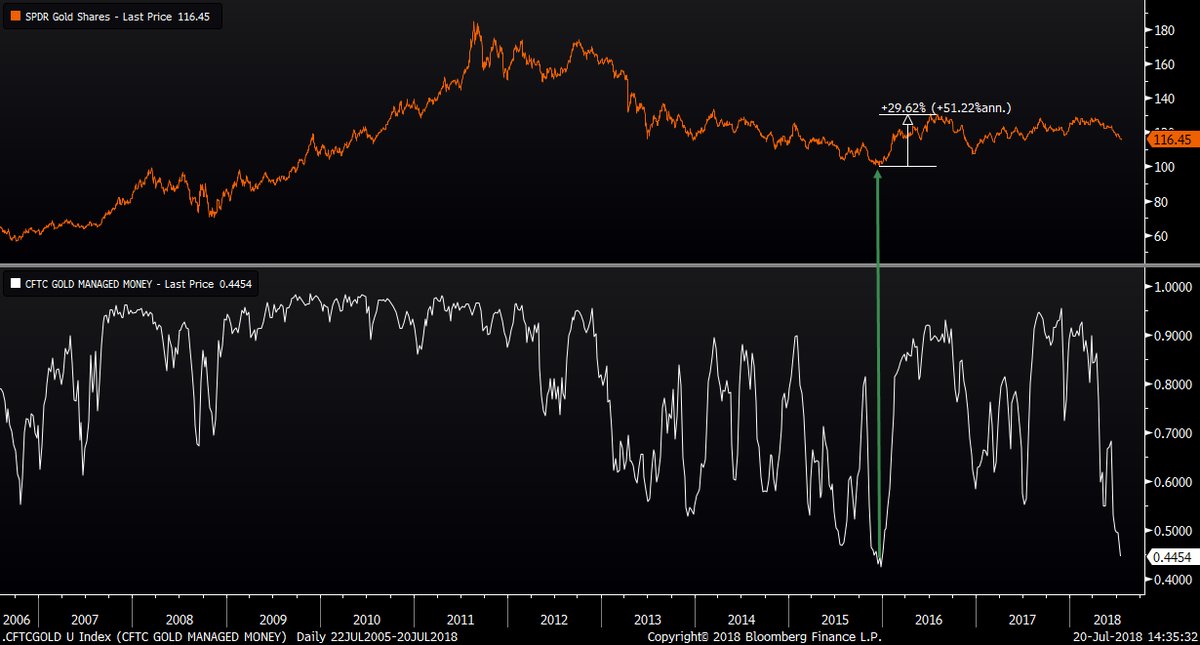

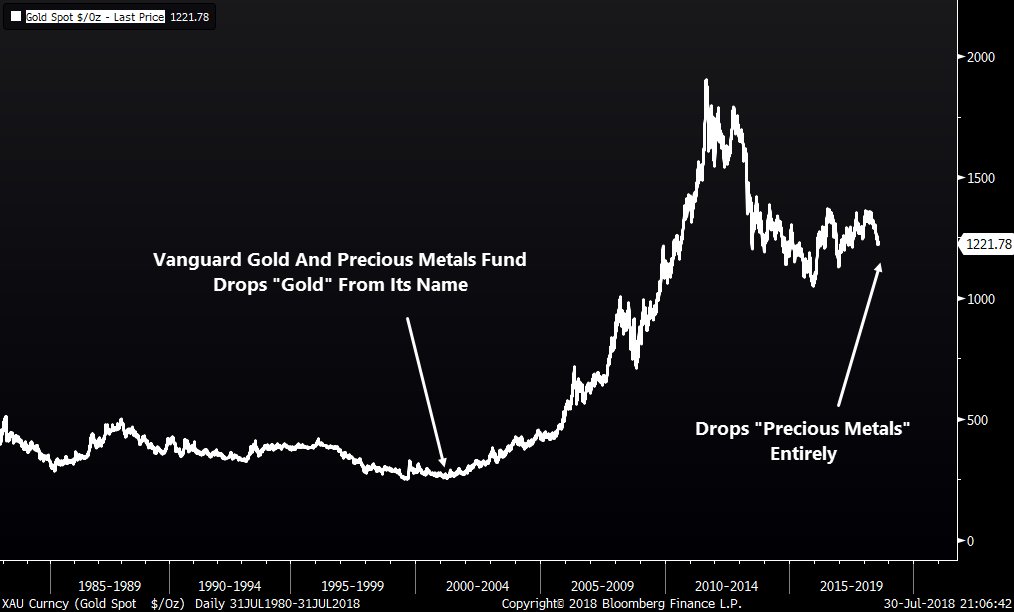

What is surprising, however, is that, despite that fact that it’s long-term (20-year) performance still crushes that of the broad stock market, gold has become so maligned among investors of all stripes, including gold bugs themselves. Yes, the past few years have favored equities over precious metals and I guess that’s where the recency bias kicks in again. But the truth is it has paid far better to be gold bug over the past two decades than to be an equity bull.

The point being to understand your time preference and time reference!

Update:

fred hickey @htsfhickey 20/July 2018 5 PM

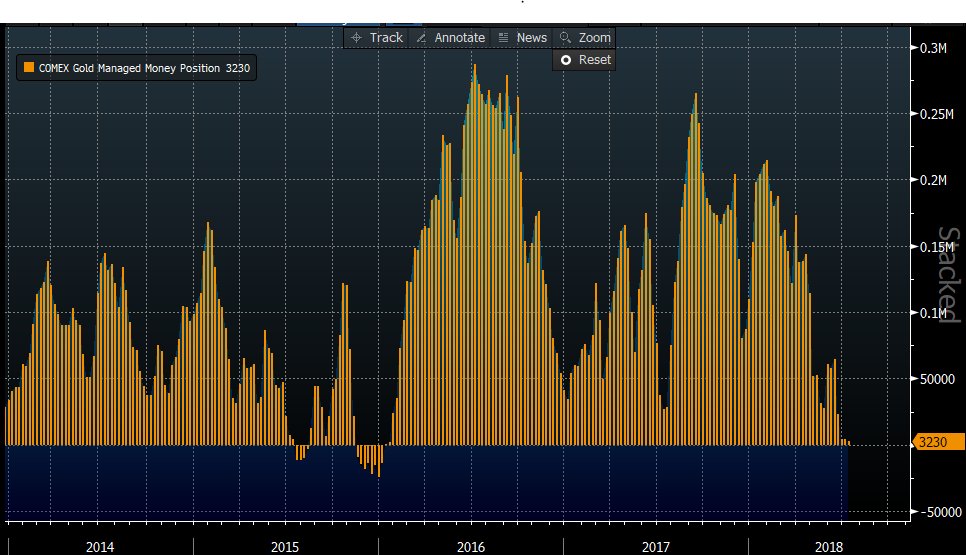

Here’s Managed Money(mostly hedge funds) COT details: 134.2K short, 11% higher than highest level (gold’s bottom) seen in 2015, so likely a record.. Net short -26.5k contracts-essentially equal to Dec. 2015 gold bottom. For comparison, at gold’s mid-2016 top they were net 270K long ago

The setup: Gold bugs totally demoralized. Gold sentiment(DSI)down to just 7% with extreme dollar bullishness(92% DSI). Trump beginning to talk $ down (will continue). FY ’19 $1T+ budget deficit. Gold seasonal demand (starts now). Managed Money (hedge funds) net short& have to cover.

It’s likely these are record level shorts. That means there are more shorts than at the bottom in late-2015 – before gold exploded 30% & miners +160% in 6 months and more shorts than at late-2008 bottom before gold soared over 75% in 1 year. Perfect setup-assuming gold’s bottomed.

Whoa Nelly! Just as I suspected it was short traders driving gold down. Thru Tuesday (likely even worse now), a slight increase in longs& another massive 27.7K jump in large spec. futures shorts. In past 5 weeks +121% jump in short contracts to 161K -highest level in at least 11yrs.

BUT, ALWAYS STUDY THE OTHER SIDE–GOLD TO KEEP FALLING.

Who earned their wingtips? That case was about approaching the problem as a business person. First you had to notice the two businesses, then break them out. Stop the bleeding, then leave the rest. Often, the smartest students struggle to resurrect the uncompetitive business. (Buffett at Berkshire Hathaway!)

Next, I will post some questions and supplementary readings for Chapter Two in DEEP VALUE (the book) over the weekend.