More commentary on the 2014 Berkshire Letter

Did-warren-buffett-move-the-goalposts-in-the-latest-letter

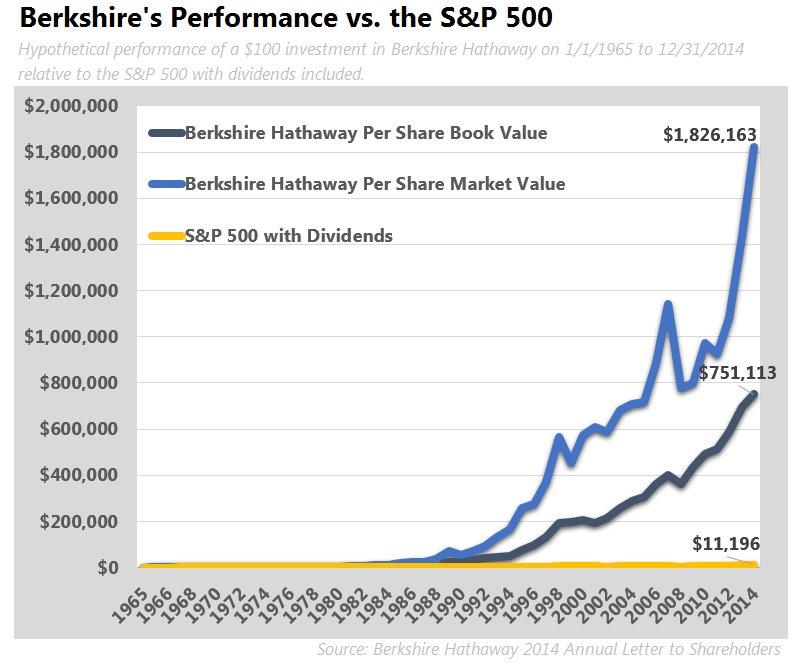

Berkshire-hathaway-2015-coverage

Buffett is a Lucky Coin-flipper?

I enjoyed reading Berkshire -Past, Present and Future, pages 24-28 2014ltr

Mr. Buffett’s anger at Stanton’s chiseling cost dearly because he didn’t sell at the first puff of the “cigar-butt” (Berkshire’s Textile Division). Buffett suffered in a value trap.

Notably, Buffett’s cigar-butt strategy worked well when managing small sums–the best of Buffett’s life in terms of relative and absolute investment performance. However, cigar-butt investing was not scalable or enduring with larger sums. Buffett then turned towards buying wonderful businesses at fair prices or, in other words, franchises with honest and able management.

His investment in See’s Candies was a turning point because the company generated high returns on invested capital which Buffett could then redeploy into other businesses. Note that See’s could only grow profitably within a defined region (Calif.?). A powerful brand coupled with economies of scale makes for a great business.

Berkshire Today (page 29) provides a description of Conglomerates and the mania that occurred in the 1960s with ponzi-scheme pooling of interests accounting and ever-rising P/E multiples–until the game crashed.

Buffett points out the folly of spin-offs, whereby the owning company loses purported “control-value” without any compensating payment. Investment bankers and private equity buccaneers were heartily savaged by Mr. Buffett’s pen.

Articles and Videos of Interest

25-old-investor-spurred-lumber A short-sellers uncovers Lumber Liquidators.

shark-tank-the-speculators-guide-to-junior-mining-investment-session-1-with-rick-rule/ A series of talks on speculating in junior miners.

—

Back to Deep Value

Before we dig deeper into Chapter Five in Deep Value, I thought we should read Chapter 2 in Quantitative Value so as to not skip over several important points. I will make sure new students receive a link to the books in the course.

2 responses to “Berkshire: Part 2”