If you only read one post on this blog, then let it be this one. John Chew

Let me tell you the story of two investors, neither of whom knew each other, but

whose paths crossed in an interesting way.

Grace Groner was orphaned at age 12. She never married. She never had kids. She never drove a car. She lived most of her life alone in a one-bedroom house and worked her whole career as a secretary. She was, by all accounts, a lovely lady. But she lived a humble life. That made the $7 million she left to charity after her death in 2010 at age 100 all the more confusing. People who knew her asked: Where did Grace get all that money?

But there was no secret. There was no inheritance. Grace took humble savings

from a meager salary and enjoyed eighty years of hands-off compounding in the stock market. That was it.

Weeks after Grace died, an unrelated investing story hit the news. Richard Fuscone, former vice chairman of Merrill Lynch’s Latin America division,

declared personal bankruptcy, fighting off foreclosure on two homes, one of which was nearly 20,000 square feet and had a $66,000 a month mortgage.

Fuscone was the opposite of Grace Groner; educated at Harvard and

University of Chicago, he became so successful in the investment industry

that he retired in his 40s to “pursue personal and charitable interests.” But

heavy borrowing and illiquid investments did him in. The same year Grace

Goner left a veritable fortune to charity, Richard stood before a bankruptcy

judge and declared: “I have been devastated by the financial crisis … The

only source of liquidity is whatever my wife is able to sell in terms of personal

furnishings.”

The purpose of these stories is not to say you should be like Grace and avoid

being like Richard. It’s to point out that there is no other field where these

stories are even possible.

In what other field does someone with no education, no relevant experience,

no resources, and no connections vastly outperform someone with the best

education, the most relevant experiences, the best resources and the best

connections? There will never be a story of a Grace Groner performing heart

surgery better than a Harvard-trained cardiologist. Or building a faster chip

than Apple’s engineers. Unthinkable.

But these stories happen in investing.

That’s because investing is not the study of finance. It’s the study of how people behave with money. And behavior is hard to teach, even to really smart people. You can’t sum up behavior with formulas to memorize or spreadsheet models to follow. Behavior is inborn, varies by person, is hard to measure, changes over time, and people are prone to deny its existence, especially when describing themselves.

Grace and Richard show that managing money isn’t necessarily about what

you know; it’s how you behave. But that’s not how finance is typically taught

or discussed. The finance industry talks too much about what to do, and not

enough about what happens in your head when you try to do it.

This report describes 20 flaws, biases, and causes of bad behavior I’ve seen

pop up often when people deal with money.

The above article confirms my bias that all the MBAs, CFAs, CPAs, and study won’t help you unless you understand yourself. Tough. For example, I can see the speck in your eye but not the mud in mine.

The clues and facts add up. Let’s sit and think for a minute:

In what rational universe could someone simply issue electronic scrip — or just announce that they intend to — and create, out of the blue, billions of dollars of value?

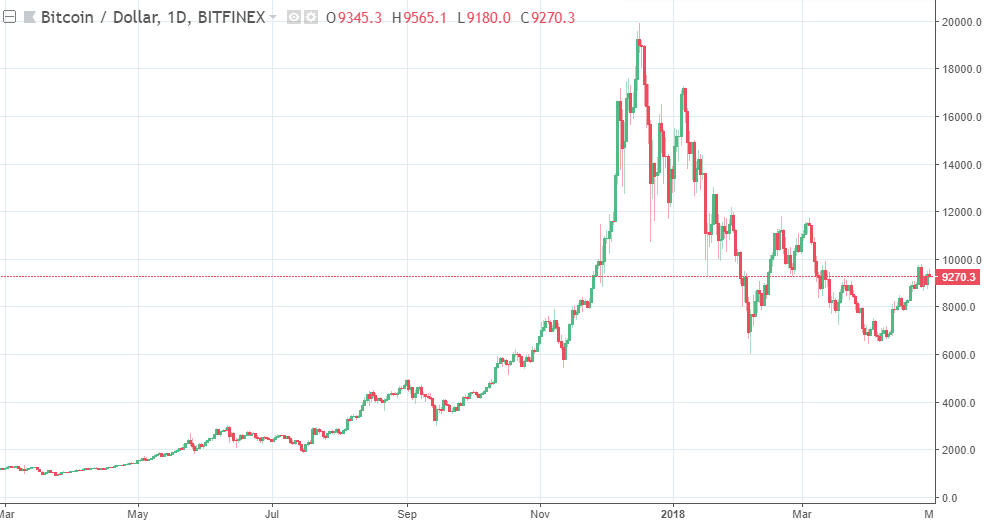

Bitcoin tangent

Did you guys notice something really interesting? The financial guys that really love bitcoin are some of the guys that either blew up or closed funds due to poor performance. The two most prominent fund manager bitcoin boosters are like that. It almost feels like they are so happy to have found their Hail Mary pass. And the most prominent guys that have good performance and didn’t blow up tend to be the guys that don’t like bitcoin and think it’s stupid, a bubble or whatever.

Think about that for a second. Oh, and that former hedge fund guy, after bitcoin plunged put his new bitcoin hedge fund on hold (buying high and selling low?). Now wonder he didn’t do well with his hedge fund; if you’re going to be making decisions based on short term volatility like that, you are bound to get whipsawed and lose money.

This is interesting because we can never really understand and know everything. But it is useful to know who you can listen to and who you should ignore. Sometimes, this saves a lot of time! From http://brooklyninvestor.blogspot.com/

—

Monday, April 30, 2018

Warren Buffett: Bitcoin is Gambling Not Investing

In an exclusive interview with Yahoo Finance in Omaha, Neb., leading up to Berkshire Hathaway’s annual shareholder meeting, which will be held om May 5, Buffett laid out his latest thinking on cryptocurrency investing. He nailed it.

“There’s two kinds of items that people buy

and think they’re investing,” he says. “One really is investing and the other isn’t.” Bitcoin, he says, isn’t.

“If you buy something like a farm, an apartment house, or an interest in a business… You can do that on a private basis… And it’s a perfectly satisfactory investment. You look at the investment itself to deliver the return to you. Now, if you buy something like bitcoin or some cryptocurrency, you don’t really have anything that has produced anything. You’re just hoping the next guy pays more.”

When you buy cryptocurrency, Buffett continues, “You aren’t investing when you do that. You’re speculating. There’s nothing wrong with it. If you wanna gamble somebody else will come along and pay more money tomorrow, that’s one kind of game. That is not investing.”

Buffett’s point is that the assets he lists such as a farm, an apartment house, etc., generate income. Bitcoin does not.

I would add there is another type of asset people hold and that is money. As Ludwig von Mises taught us, money is the most liquid good and people hold because of this liquidity. They know they can instantly exchange it, at a fairly stable price, nearly anywhere for goods and services.

This is where Bitcoin and other cryptocurrencies fail in the money category. They are from an instrument at present that can be exchanged for any good or service and they are far from stable in price. Many people who have purchased Bitcoin over the last 6 months have lost as much as 50% of their purchasing power. That is not a stable asset, not even when compared to the U.S. dollar which is run by the Federal Reserve in crony reckless fashion.

Moreover, the idea of a world where a cryptocurrency is the world’s medium of exchange is a frightening notion. It is quite simply a remarkable way for government to track all transactions and prohibit transactions in specific books and other goods that it doesn’t want individuals to buy.

The idea that the government can’t track Bitcoin is a delusion view held by Bitcoin fanboys.

The Intercept recently reported:

Classified documents provided by whistleblower Edward Snowden show that the National Security Agency indeed worked urgently to target bitcoin users around the world — and wielded at least one mysterious source of information to “help track down senders and receivers of Bitcoins,” according to a top-secret passage in an internal NSA report dating to March 2013. The data source appears to have leveraged the NSA’s ability to harvest and analyze raw, global internet traffic while also exploiting an unnamed software program that purported to offer anonymity to users, according to other documents.

Although the agency was interested in surveilling some competing cryptocurrencies, “Bitcoin is #1 priority,” a March 15, 2013 internal NSA report stated.

-Robert Wenzel

—

What is money Bastiat? If you understand money, then the Bitcoin Scam becomes obvious.

—

Bitcoin is the greatest scam in history

It’s a colossal pump-and-dump scheme, the likes of which the world has never seen.

By Bill Harris Apr 24, 2018

Okay, I’ll say it: Bitcoin is a scam.

In my opinion, it’s a colossal pump-and-dump scheme, the likes of which the world has never seen. In a pump-and-dump game, promoters “pump” up the price of a security creating a speculative frenzy, then “dump” some of their holdings at artificially high prices. And some cryptocurrencies are pure frauds. Ernst & Young estimates that 10 percent of the money raised for initial coin offerings has been stolen.

The losers are ill-informed buyers caught up in the spiral of greed. The result is a massive transfer of wealth from ordinary families to internet promoters. And “massive” is a massive understatement — 1,500 different cryptocurrencies now register over $300 billion of “value.”

It helps to understand that a bitcoin has no value at all.

Promoters claim cryptocurrency is valuable as

(1) a means of payment

Bitcoins are accepted almost nowhere, and some cryptocurrencies nowhere at all. Even where accepted, a currency whose value can swing 10 percent or more in a single day is useless as a means of payment.

2. Store of Value.

Extreme price volatility also makes bitcoin undesirable as a store of value. And the storehouses — the cryptocurrency trading exchanges — are far less reliable and trustworthy than ordinary banks and brokers.

3. Thing in Itself.

A bitcoin has no intrinsic value. It only has value if people think other people will buy it for a higher price — the Greater Fool theory.

Some cryptocurrencies, like Sweatcoin, which is redeemable for workout gear, are the equivalent of online coupons or frequent flier points — a purpose better served by simple promo codes than complex encryption. Indeed, for the vast majority of uses, bitcoin has no role. Dollars, pounds, euros, yen and renminbi are better means of payment, stores of value and things in themselves.

Cryptocurrency is best-suited for one use: Criminal activity. Because transactions can be anonymous — law enforcement cannot easily trace who buys and sells — its use is dominated by illegal endeavors. Most heavy users of bitcoin are criminals, such as Silk Road and WannaCry ransomware. Too many bitcoin exchanges have experienced spectacular heists, such as NiceHash and Coincheck, or outright fraud, such as Mt. Gox and Bitfunder. Way too many Initial Coin Offerings are scams — 418 of the 902 ICOs in 2017 have already failed.

Hackers are getting into the act. It’s estimated that 90 percent of all remote hacking is now focused on bitcoin theft by commandeering other people’s computers to mine coins.

Even ordinary buyers are flouting the law. Tax law requires that every sale of cryptocurrency be recorded as a capital gain or loss and, of course, most bitcoin sellers fail to do so. The IRS recently ordered one major exchange to produce records of every significant transaction.

And yet, a prominent Silicon Valley promoter of bitcoin proclaims that “Bitcoin is going to transform society … Bitcoin’s been very resilient. It stayed alive during a very difficult time when there was the Silk Road mess, when Mt. Gox stole all that Bitcoin …” He argues the criminal activity shows that bitcoin is strong. I’d say it shows that bitcoin is used for criminal activity. In what rational universe could someone simply issue electronic scrip — or just announce that they intend to — and create, out of the blue, billions of dollars of value?

Bitcoin transactions are sometimes promoted as instant and nearly free, but they’re often relatively slow and expensive. It takes about an hour for a bitcoin transaction to be confirmed, and the bitcoin system is limited to five transactions per second. MasterCard can process 38,000 per second. Transferring $100 from one person to another costs about $6 using a cryptocurrency exchange, and well less than $1 using an electronic check.

Bitcoin is absurdly wasteful of natural resources. Because it is so compute-intensive, it takes as much electricity to create a single bitcoin — a process called “mining” — as it does to power an average American household for two years. If bitcoin were used for a large portion of the world’s commerce (which won’t happen), it would consume a very large portion of the world’s electricity, diverting scarce power from useful purposes.

In what rational universe could someone simply issue electronic scrip — or just announce that they intend to — and create, out of the blue, billions of dollars of value? It makes no sense.

All of this would be a comic sideshow if innocent people weren’t at risk. But ordinary people are investing some of their life savings in cryptocurrency. One stock brokerage is encouraging its customers to purchase bitcoin for their retirement accounts!

It’s the job of the SEC and other regulators to protect ordinary investors from misleading and fraudulent schemes. It’s time we gave them the legislative authority to do their job.

William H. Harris Jr. is the founder of Personal Capital Corporation, a digital wealth management firm that provides personal financial software and investment services, where he sits on the board of directors.

Read full article here: https://www.recode.net/2018/4/24/17275202/bitcoin-scam-cryptocurrency-mining-pump-dump-fraud-ico-value

Attached is the program guide, which includes an agenda for the day and bios of all of the speakers. Registration and continental breakfast begin at 7:15am, the first speaker is at 8:15am, there are morning, lunch and afternoon breaks, and the last speaker ends at 4:15pm, followed by a networking cocktail reception until 7:00pm. The NYAC is on the corner of Central Park South and Seventh Avenue, and it has a dress code – no jeans, shorts, sneakers or t-shirts.

This full-day event is the first of its kind dedicated solely to short selling and will feature 22 of the world’s top practitioners who will share their wisdom, lessons learned, and best, actionable short ideas. I’ve seen many of the speakers’ presentations and they’re awesome! Companies that will be pitched include Tesla, Disney, Kraft-Heinz and Stericycle, plus internet ad fraud and gold.

The idea for the conference is rooted in the fact that this long bull market has inflicted absolute carnage on short sellers, and even seasoned veterans are throwing in the towel. This capitulation, however, combined with the increasing level of overvaluation, complacency, hype and even fraud in our markets, spells opportunity for courageous investors, so there is no better time for this conference.

Reporters from all of the major media outlets will be there, and CNBC is covering it as well. I was on their Halftime Report yesterday discussing the conference: www.cnbc.com/video/2018/04/26/kases-whitney-tilson-talks-the-art-and-pain-of-short-selling.html. I also just published the fourth, final (and my favorite) article in a series I’ve written entitled Lessons from 15 Years of Short Selling: https://seekingalpha.com/article/4166837-lessons-15-years-short-selling-veterans-advice

I’d be grateful if you’d help spread the word about the conference among your friends and colleagues, and wanted to pass along a special offer: when they register at http://bit.ly/Shortconf, they can use my friends and family discount code, FF20, to save 20% ($600) off the current rate.

I look forward to seeing you next week!

Sincerely yours,

Whitney Tilson

Founder & CEO

Kase Learning, LLC

5 W. 86th St., #5E

New York, NY 10024

(646) 258-0687

WTilson@KaseLearning.com

I started at page one [of these manuals-Moody’s and Value-Line] and went through every company that traded, from A to Z. When I was done I knew something about every company in the book.

I like businesses that I can understand. Let’s start with that. That narrows it down by 90%. There are all types of things I don’t understand, but fortunately, there is enough I do understand. You have this big wide world out there and almost every company is publicly owned. So you have all American business practically available to you. So it makes sense to go with things you can understand.

First, you need two piles. You have to segregate businesses you can understand and reasonably predict from those you don’t understand and can’t reasonably predict. An example is chewing gum versus software. You also have to recognize what you can and cannot know. Put everything you can’t understand or that is difficult to predict in one pile. That is the too-hard pile. Once you know the other pile, then it’s important to read a lot, learn about the industries, get background information, etc. on the companies in those piles. Read a lot of 10Ks and Qs, etc. Read about the competitors. I don’t want to know the price of the stock prior to my analysis. I want to do the work and estimate a value for the stock and then compare that to the current offering price. If I know the price in advance it may influence my analysis. We’re getting ready to make a $5 billion investment and this was the process I used.

You have to turn over a lot of rocks to find those little anomalies. You have to find the companies that are off the map – way off the map. You may find local companies that have nothing wrong with them at all

Most people get interested in stocks when everyone else is. The time to get interested is when no one else is. You can’t buy what is popular and do well.

I don’t look to jump over 7-foot bars: I look around for 1-foot bars that I can step over.

If we were to do it over again, we’d do it pretty much the same way. The world hasn’t changed that much. We’d read everything in sight about businesses and industries we think we’d understand. And, working with far less capital, our investment universe would be far broader than it is currently.

7 Gems from Buffet on Analyzing Stocks

You don’t need to be an expert in order to achieve satisfactory investment returns. But if you aren’t, you must recognize your limitations and follow a course certain to work reasonably well. Keep things simple and don’t swing for the fences. When promised quick profits, respond with a quick “no.”

There’s nothing different, in my view, about analyzing securities today vs. 50 years ago.

We favor businesses where we really think we know the answer. If we think the business’s competitive position is shaky, we won’t try to compensate with price. We want to buy a great business, defined as having a high return on capital for a long period of time, where we think management will treat us right. We like to buy at 40 cents on the dollar, but will pay a lot closer to $1 on the dollar for a great business.

Munger: Margin of safety means getting more value than you’re paying. There are many ways to get value. It’s high school algebra; if you can’t do this, then don’t invest.

If you’re going to buy a farm, you’d say, “I bought it to earn $X growing soybeans.” It wouldn’t be based on what you saw on TV or what a friend said. It’s the same with stocks. Take out a yellow pad and say, “If I’m going to buy GM at $30, it has 600 million shares, so I’m paying $18 billion,” and answer the question, why? If you can’t answer that, you’re not subjecting it to business tests.

Capital-intensive industries outside the utility sector scare me more. We get decent returns on equity. You won’t get rich, but you won’t go broke either. You are better off in businesses that are not capital intensive.

No formula in finance tells you that the moat is 28 feet wide and 16 feet deep. That’s what drives the academics crazy. They can compute standard deviations and betas, but they can’t understand moats. Maybe I’m being too hard on the academics.

7 Nuggets from Buffett on Valuing Stocks

When Charlie and I buy stocks which we think of as small portions of businesses our analysis is very similar to that which we use in buying entire businesses. We first have to decide whether we can sensibly estimate an earnings range for five years out, or more. If the answer is yes, we will buy the stock (or business) if it sells at a reasonable price in relation to the bottom boundary of our estimate. If, however, we lack the ability to estimate future earnings which is usually the case we simply move on to other prospects. In the 54 years we have worked together, we have never foregone an attractive purchase because of the macro or political environment, or the views of other people. In fact, these subjects never come up when we make decisions.

In 1986, I purchased a 400-acre farm, located 50 miles north of Omaha, from the FDIC. It cost me $280,000, considerably less than what a failed bank had lent against the farm a few years earlier. I knew nothing about operating a farm. But I have a son who loves farming, and I learned from him both how many bushels of corn and soybeans the farm would produce and what the operating expenses would be. From these estimates, I calculated the normalized return from the farm to then be about 10%. I also thought it was likely that productivity would improve over time and that crop prices would move higher as well. Both expectations proved out.

Intrinsic value is terribly important but very fuzzy. We try to work with businesses where we have fairly high probability of knowing what the future will hold. If you own a gas pipeline, not much is going to go wrong. Maybe a competitor enters forcing you to cut prices, but intrinsic value hasn’t gone down if you already factored this in. We looked at a pipeline recently that we think will come under pressure from other ways of delivering gas [to the area the pipeline serves]. We look at this differently from another pipeline that has the lowest costs [and does not face threats from alternative pipelines]. If you calculate intrinsic value properly, you factor in things like declining prices.

Investors making purchases in an overheated market need to recognize that it may often take an extended period for the value of even an outstanding company to catch up with the price they paid.

We use the same discount rate across all securities. We may be more conservative in estimating cash in some situations.

Just because interest rates are at 1.5% doesn’t mean we like an investment that yields 2-3%. We have minimum thresholds in our mind that are a whole lot higher than government rates. When we’re looking at a business, we’re looking at holding it forever, so we don’t assume rates will always be this low.

The appropriate multiple for a business compared to the S&P 500 depends on its return on equity and return on incremental invested capital. I wouldn’t look at a single valuation metric like relative P/E ratio. I don’t think price-to-earnings, price-to-book or price-to-sales ratios tell you very much. People want a formula, but it’s not that easy. To value something, you simply have to take its free cash flows from now until kingdom come and then discount them back to the present using an appropriate discount rate. All cash is equal. You just need to evaluate a business’s economic characteristics.

More Reading

Most of these quotes came from Buffett FAQ which contains the Q&A from shareholder meetings and goes beyond what you’ll find in the annual letters.

Just from these small selection of quotes, you can see how Buffett manages to dance in zone 4.

‘The Floating Kilogram’:

The Editor of the Sun

Talks About His New Book

On the Dollar Crisis

By DAWN BENNETT, Adapted From Financial Myth Busting | April 5, 2015

The following is adapted from an interview by Dawn Bennett, host of the radio show “Financial Myth Busting,” with the editor of The New York Sun, Seth Lipsky. The broadcast aired March 8:

* * *

Ms. Bennett: Seth Lipsky is the author of a book titled “The Floating Kilogram and Other Editorials on Money from The New York Sun.” Before the Sun, he spent 20 years at the Wall Street Journal where he served on the editorial board and helped launch the Asian Wall Street Journal as well as the Wall Street Journal Europe. Recently, Seth authored a column in the New York Post titled “Why does the Federal Reserve Fear a Real Audit,” which is a question much on my mind. Seth, welcome.

Mr. Lipsky: Thanks, Dawn. It’s nice to be with you.

Ms. Bennett: To put it charitably, Janet Yellen appears to be very alarmed that some members of Congress want to conduct a comprehensive audit of the Federal Reserve for the first time since it was created. If the Federal Reserve is doing everything correctly, why should Mrs. Yellen be alarmed and what does she have to hide?

Mr. Lipsky: Well, that’s a great question. The Federal Reserve is already audited, in the sense that an accountant comes in and goes over its books. But what the Congress is talking about is a much broader look by the Governmental Accountability Office of how the central bank forms our monetary policy and what its relations are with foreign banks. The Fed has been fighting this tooth and nail as an intrusion on its independence. What Congress knows is that the Constitution gave the monetary power precisely to Congress.

Congress has a constitutional obligation and power to establish the American monetary system and regulate it, to coin money, regulate its value and that of foreign coinage. This has become a big issue where we have not taken a really systematic look at how the Fed operates in the hundred years that it’s been in existence. We’re starting the second century, and there is growing sentiment in the Congress to take a look at this. The audit of the Fed measure passed the House as recently as of September by a vote of 333 to 92, with 109 Democrats joining the Republicans. So the Fed is certainly growing concerned.

Ms. Bennett: The only reason Janet Yellen has the power to coin money is because Congress delegated its own power to the Federal Reserve in 1913. Isn’t congressional oversight of that power something that should be considered commonsensical by the Federal Reserve?

Mr. Lipsky: The Fed was created in 1913. The Coinage power was first acted on in 1792, and coinage was given not to any Federal Reserve but to the United States Mint. When the second central bank came up to the Supreme Court it was really the tax and the borrowing power that the courts were looking at when they okayed the authority of the central bank.

Ms. Bennett: We are all accountable to someone or something, so what is wrong about the Federal Reserve being accountable to Congress?

Mr. Lipsky: Nothing whatsoever. Even Chairman Yellen acknowledges that Congress has the power. She’s just pleading and warning that it not interfere. Why is Congress growing concerned about this in the first place? It’s because the Great Recession has lasted six years and we still do not feel like we’ve recovered. What is the Fed’s role in this? Could the reason that the Great Recession lasted so long be attributable to monetary policy? The value of the dollar has been allowed to collapse below one 1,100th of an ounce of gold. It was a 265th of an ounce of gold when George W. Bush was sworn in. These are huge questions, and somebody needs to ask them.

Ms. Bennett: It is quite clear to me that the Federal Reserve doesn’t want the rest of us to actually be able to see what they really up to. If we did know what they’re doing, do you think most Americans would just want it shut down? To your point, since 1913, the dollar has actually lost over 97% of its purchasing power. And of course, the economy has been subjected to one painful depression and a series of what I call Fed-created recessions. Despite the poor track record, we continue to support them. At the end of the day, does it matter if we even have a Federal Reserve?

Mr. Lipsky: I think the monetary questions do matter to every American in all positions. My favorite statistic is that between 1947 and 1971 the average unemployment rate was below 5%. From 1971 until today it was above 6%. What happened in 1971, when the unemployment rate began souring? What happened is we abandoned the Bretton Woods Gold Exchange System, under which the dollar was linked to gold, and the money began flowing not in the productive enterprises, but into the money markets and hedge funds and all these sorts of things and not so much into the kind of investment that created the great industrial base in America.

Ms. Bennett: Let’s talk about that type of investment. According to a government report I’ve read, the Federal Reserve made $16.1 trillion in loans to big banks during that financial crisis. In my opinion, [it once] created the dotcom bubble and the housing bubble. Now, I think it has created the financial bubble that our markets are experiencing.

Mr. Lipsky: Asset inflation. The debate over inflation is one of the most important debates in the country. The left wing likes to say there is no inflation, but the dollar is worth only a tiny amount of the constitutional specie, which is gold and silver, compared to what it used to be worth. This is what people feel when they hear the government say there’s no inflation but they try to go to the grocery store and they spend $50 or $100 on a tiny plastic bag with a few items in it.

Ms. Bennett: Yes, I know shelf inflation is huge, but I want to talk about commodities for a bit. The Department of Justice has recently said again that they’re going after the big banks that have been, on an ongoing and continuous basis, manipulating gold and silver. What are your thoughts on that? Will it work this time? And, if so, is there a simple solution to stop them from doing this? They seem to get their hands slapped, apologize, and then come back and do it again, and again.

Mr. Lipsky: The news that the Justice Department is looking at something like ten or twelve major banks for possibly rigging the price of gold broke the same week that Mrs. Yellen was up on Capitol Hill testifying against an audit of the Fed.

Ms. Bennett: That’s right.

Mr. Lipsky: One of the questions that The New York Sun raised is what is she afraid of then? Is it the danger that the Fed has been meddling in the gold market the way the Justice Department is alleging commercial banks have been doing it? It’s the Fed that regulates commercial banks after all. I don’t want to carry that argument too far. I asked it then in an editorial more in the nature of a question. But there is a movement in Congress to open up what is called a Centennial Monetary Commission that after the first hundred years of the Fed, would just take a look at how the whole system is working.

We’ve been in a period of fiat money, meaning dollars that have no connection in law to any gold or silver or other constitutional money. We’ve been in a fiat system since 1971. Previously, our dollars were always defined in terms of gold and silver, suddenly they’re not. The unemployment average is much higher; the bankruptcy rate is much higher; the inequality rate has been much higher since the mid 1970’s. Could this be related to the fact that we abandoned sound money in the mid 1970s?

Ms. Bennett: De-dollarization has been going on now for the last few years, and I think it’s because the dollar is continuing to get weaker. Our political system and economic system aren’t what they used to be. Do you think it’s possible that if China, for example, standardizes the renminbi it will start taking power away from the U.S. dollar?

Mr. Lipsky: The abandonment of sound money by the U.S. has brought forth a whole chain of foreign governments that are alarmed and wonder whether a new system should be set up. China. There is talk of Russia going on a gold standard; the European Union is having its own catastrophe with the Euro, and it’s wondering whether the dollar ought to be replaced as the international reserve. The United Nations, for crying out loud, has gotten involved in this.

One of my favorite moments happened in 1965, when the President of France, Charles de Gaulle, called a thousand reporters into the presidential palace sat them down and addressed them on the importance of restoring gold as the international standard. His argument was that it puts all countries on the same basis: America, France, England, China, little countries, and it takes a lot of the partisanship out of the monetary question internationally, or it takes the politics out of money. It’s ironic that Fed loves to talk about how we shouldn’t politicize the monetary system. If one really wants to de-politicize the monetary system, restoring a gold standard or something like it is exactly the way to do it.

Ms. Bennett: Mrs. Yellen claims that opening the Fed to an outside audit would “politicize” — her word — monetary policy.

Mr. Lipsky: Right.

Ms. Bennett: Isn’t it political when Senator Schumer, for example, tells her to keep rates low every time she testifies before the Senate Banking Committee? Isn’t it already happening?

Mr. Lipsky: You’re exactly right. Why is it always the conservatives that are doing the politicizing and not the liberals? The big politicization of monetary policy happened in 1978 with the passage of Humphrey-Hawkins, which said that the Fed has to have a second mandate of increasing the employment rate or decreasing unemployment, in addition to affecting the value of our dollar. That opened the door to an enormous political interference in monetary policy.

Ms. Bennett: I know you’re not a gold trader or silver trader…

Mr. Lipsky: I’m a newspaperman.

Ms. Bennett: There you go. But I’m certain you follow the markets. What do you think would be a simple solution to fix the ongoing and continuous manipulation of gold and silver so that we can get more stability? It does seem, whether it’s a Federal Reserve or some other central bank, that they’re interfering with it in order to make the fiat currency look stronger than it really is.

Mr. Lipsky: I favor a definition by law, enacted by Congress under its constitutional powers to coin money and regulate its value, and fix the standards of weights and measures — a law passed by Congress defining the dollar as a fixed amount of gold or silver. Silver was the main specie used in early years of our republic. The debate over whether gold or silver was better went on through the 19th century, and we basically decided in 1900, with the passage of the Gold Standard Act, to make gold the true national money. I think that would go a long way toward solving this problem. There are a lot of questions as to exactly how to do it, whether there should be a system like Bretton Woods, which said dollars had to be redeemed in gold if they were held by foreign governments.

Ms. Bennett: In physical gold, not paper gold. In physical gold.

Mr. Lipsky: Right.

Ms. Bennett: There’s a big difference there.

Mr. Lipsky: Therefore the price at which one fixes the dollar, the value, the amount of gold, has to be carefully worked out. But the gold standard is not some flaky thing. This was believed in by George Washington, Thomas Jefferson, James Madison, Alexander Hamilton, and almost every president since, up until Richard Nixon. John Kennedy, Woodrow Wilson, Grover Cleveland — they all believed in it.

Mr. Lipsky: The New York Sun is an online newspaper that I edit. We published in print until several years ago. It’s a leading voice in journalism for a sound dollar. It supports a sound dollar, limited government, and a restoration of constitutional dollar based on gold or silver. This is the first radio interview about the book.

Ms. Bennett: Thank you.

Mr. Lipsky: This book contains on this issue 130 editorials that have been issued in the Sun in recent years. Steve Forbes calls them “brilliant,” “irrefutable,” and “the Federalist Papers for the gold standard.” James Grant calls the book both “persuasive” and “unfailingly entertaining.” It’s a book for every person, not just the experts, and it’s available on Amazon.com, the online bookstore, and you’ll have a copy in a day or two if you place your order. “Pure gold” is the way the economist Judy Shelton described this book. The title, Dawn, comes from the discovery that the kilogram, which is the last metric weight measure based on a physical object, has been losing mass — atom by atom. The Sun in one of its editorials said, “Why don’t we float the kilogram just like we float the dollar?” That’s from where the title of the book comes.

Ms. Bennett: If President Obama, or our next president, were to become motivated to make reforms, what do you think the takeaway from this book would to be? Definitely a gold standard?

Mr. Lipsky: So I think the takeaway is going to be that in our monetary system at some point, the dollar has to be defined in terms of something real rather than just another dollar. At the moment, if you take your dollar to the central bank to redeem it, they’ll give you another dollar. There’s no reference to anything real and no classical measure of value. We have what Jim Grant likes to call the Ph.D. standard, and I think we need to move away from that to the kind of standard that sustained our country during its periods of greatest growth and strongest employment.

Ms. Bennett: We always seem to make changes in the United States when things break down, but not beforehand. What is going to be the instigator to standardize our currency?

Mr. Lipsky: People say things could become a disaster. The last six years have been a disaster.

Ms. Bennett: Exactly.

Mr. Lipsky: Huge amounts of unemployment, not just for a short period, but for six years. It’s consumed almost the entire Obama presidency. People are still trying to figure out their homes, still trying to figure out how the price of college got more than halfway to $100,000 a year — you know, all these things. We’ve been living through this, and I think events have energized Congress to start looking at this. The Sound Dollar Act, or Centennial Monetary Commission Act, or Audit the Fed Act, or Free Competition in Currency Act. This is why Janet Yellen — to bring it back to where we came in — is fighting so hard against the Congress doing this. We’re in a constitutional moment here where Congress is going to take a look at this, I predict.

Ms. Bennett: Do you think they’re going to have the guts to do it?

Mr. Lipsky: I think the American people have a lot of guts.

Ms. Bennett: Me, too.

Mr. Lipsky: And at the end of the day, the Congress has to listen to the American people.

From James Grant: Money is information, says Gilder. It’s a measuring stick, not a magic wand.” Wealth is knowledge and growth is learning. Prices should always trend down over the long-term in a capitalist economy to reflect continuous improvements in the technique of production. ….Researchers in Bitcoin and other digital currencies have shown that the real source of the value of any money is its authenticity and reliability as a measuring stick of economic activity. A measuring stick cannot be part of what it measures.

For more than a century, the U.S. Federal Reserve has manipulated the money supply, ostensibly with the goal of steering the economy away from extreme booms and busts. In practice, however, central banks exacerbate the very problems they purport to fix, spurring the misallocation of capital in the wrong sectors of the economy, inflating speculative bubbles, and doubling down on their mistaken strategy after the inevitable collapse and ongoing stagnation. At a recent event hosted by Atlas Network partner the American Principles Project (APP), renowned author George Gilder presented a strong case for replacing Fed meddling with a 21st century gold standard.“Government efforts to control money destroy wealth by inhibiting learning,” Gilder explained, noting that money serves as a channel that carries information about supply and demand to every market participant in every corner of the economy. Gilder’s new book, The 21st Century Case for Gold: A New Information Theory of Money, expands on that theme.“Manipulating the value of money, whether by printing currency or artificially suppressing interest rates, does not create wealth,” Gilder wrote. “Instead, it is the equivalent of manipulating the data of a scientific experiment after it takes place, distorting the information economic actors need to create new wealth. Understanding the new economic paradigm of information theory leads us to recognize that inflation is only one of many bad economic results of monetary policy that distorts the value of money.”

Atlas Advisory Council member and APP Chairman Sean Fieler introduced Gilder’s remarks and helped to frame the ensuing discussion, which also included financial publishers Steve Forbes and Jim Grant. The event highlighted how Gilder’s fresh take on the currency debate could help make the need for sound money politically salient in the coming year.

Ecclesiastes tells us: “The thing that hath been, it is that which shall be; and that which is done is that which shall be done: and there is no new thing under the sun.” Myrmikan Research applies this principle to the subject of credit bubbles.

The ancient Greeks discovered that debt could magnify wealth. The debtor feels richer from the use of the borrowed property, while the lender feels richer from the compounding interest yielded by his claim. Both indulge in consumption more freely. As long as the accumulating claims remain contingent, the bubble grows. But, eventually, someone asks to be paid, and the expandingclaims on wealth must be reconciled to tangible wealth, much of which has been consumed.

The first recorded credit bubble popped in 594 B.C. Athens. Threatened with a civil war of creditor versus debtor, the Athenian ruler Solon pulled down the mortgage stones to free the debtors and devalued the drachma by 27% to relieve the bankers. Every credit collapse since – from the Panic of A.D. 33 to John Law’s Mississippi Bubble to the Great Depression and many others besides – has followed Solon’s template of debt default and currency devaluation.

“The natural remedies, if the credit-sickness be far advanced, will always include a redistribution of wealth: the further it is postponed, the more violent it will be. Every collapse of a credit expansion is a bankruptcy, and the magnitude of the bankruptcy will be proportionate to the magnitude of the debt debauch. In bankruptcies, creditors must suffer.” – Freeman Tilden, 1936

And against what is currency and debt devalued? Carl Menger, founder of the Austrian School of economics, was the first to explain that money is liquidity and that gold is the most liquid asset. Thus, gold has served as the reference point of value since the origins of money and is that against which currency must be devalued to relieve debts. Paper promises depreciate.

“The faith is lost. All with one impulse people rush to seize the gold itself as the only reality left—not only people as individuals; banks, also, and the great banking systems and governments do it, in competition with people. This is the financial crisis.”

– Garet Garrett, 1932

Myrmikan Research chronicles the collapse of the current, global credit bubble – the largest and broadest in history – analyzing current events from the perspective of Austrian economics and placing them in historical context. Many links to books:http://www.myrmikan.com/research/

A Value Investor/Analyst, http://www.hacketts.com/ Click on Sampleslink on the left and read examples of company research. If you want to be a professional analyst, his research sets a high standard. Note the format: Thesis stated right up front. He eats his own cooking too.

BITCOIN

Gavin Andresen, Chief Scientist of the Bitcoin Foundation, talks with EconTalk host Russ Roberts about where Bitcoin has been and where it might be headed in the future. Topics discussed include competing cryptocurrencies such as Dogecoin, the role of the Bitcoin Foundation, the challenges Bitcoin faces going forward, and the mystery of Satoshi Nakamoto.

“Find the trend whose premise is false,” says George Soros, “and bet against it.”

Gold bugs seem schizoprenic. Gold prices are manipulated downward; buy more gold!I think the recent fall in gold has to do with increasing recessionary conditions and "disinflation". But when people realize that real money (financial reserves) can not be replaced by credit and debt then the price decline will reverse.

Imagine you are a major holder of new Lexus cars. Imagine you are in financial trouble. The market for Lexus cars anticipates the upcoming supply. Prices of drop. OK… but are Lexus the same as gold?

Imagine that, instead of Lexus cars, you held cash — a big wad of cash in your vault. Then, in financial trouble, you need get out your cash and use it to pay your creditors. Does the market for cash go down? Does the value of your cash decline because people know you will have to give it to someone else?

The premise is false. Real cash does not become less valuable when people find themselves in financial difficulty; it becomes more valuable. The demand for cash goes up, not down.

But wait. Today’s bills are payable in paper cash…not gold. Debtors must raise paper cash by selling their gold for paper. It’s paper they need… not real money.

Our current system runs on irredeemable, fiat, paper money. People spend it. People borrow it. Now people need more of it to pay their bills. So they sell their valuables — namely, gold — to get more paper money. The Gold price in dollars goes down, while central banks print up more paper money — just to make sure there’s plenty to go around.

One day people will stop worrying about the quantity of the paper and begin worrying about the quality of it. I am saying gold is commodity money–real money with no liabilities (promise of acceptance). But I haven’t proven anything, I am putting down thoughts. Next week I will need to prove why I believe that idea has merit. Our goal is to improve our understanding of reality.

I will need to define my terms and prove my premises to debate the reader who provided his thoughts on gold.

First, What is inflation?

The reader in his comments below says inflation is rising consumer prices.

I define inflation as any increase in the economy’s supply of money not consisting of an increase in the stock of the money (gold) metal.

Money is a commodity serving as a medium for exchanges, and–because there has been a recent prior history of exchanges–money can serve as a store of value for future exchanges.

Here is another description: Inflation is tn extension of the nominal quantity of any medium of exchange beyond the quantity that would have been produced on the free market. This definition corresponds to the way inflation had been understood until WWII. The 1941 Funk and Wagnalls Dictionary defined inflation as an “expansion of extension beyond natural or proper limitsor so as to exceed normal or just value, specifically over issue of currency.”

A free market is social cooperation conditioned by the respect of private property rights,” Therefore the meaning of inflation is that it extends the nominal money supply through a violation of property rights. In this sense, inflation can also be called a forcible way of increasing the money supply (by fractional reserve banking, by monetization of government debt, by counterfeiting, by forgery, etc.) as distinct from the “natural” production of money through mining and minting.

The difference is vast and important. Friedrich A. Hayek stated that his chief objection against monetarist theory is that it pays attention only to the effects of changes in the quantity of money on the general price level and not to the effects on the structure of relative prices. In consequence, it tends to disregard what seems to me the most harmful effects of inflation: the misdirection of resources it causes and the unemployment which ultimately results from it.

So next week I will lay out my premises and show why the distinction is important. A debate without definition and/or agreement of terms is like having a contest to nail jello to a wall.

—

Pop Quiz: If the FED wanted to increase the velocity of money what could it do? Hint, the effect would be immediate. Why do you think the FED is not doing that? Where are the errors in this report: HIM2013Q1NP

—

A Reader Discusses Gold

I was a bull on gold for years, but switched bearish during the mania of summer 2011 and have been bearish ever since.I don't think anybody can argue that central banks are flooding the world with money.Everyone knows this is occurring and laments about it, and professional investors keep pushing gold.You'd be hard pressed to find a big name manager who doesn't like gold.

The problem is that gold doesn't actually protect you from anything - unless everyone else thinks

it does.When Greece imploded back in 2010, almost all assets went down except gold and the

US dollar.

People thought that gold was a safe haven, and therefore it was a safe haven.Now, the situation is

almost the exact opposite.Gold bulls have gotten everything they wanted in terms of bullish gold

fundamentals, yet the price keeps going down.

The problem is that gold is purely a psychological asset, and it's only worth what

the next guy is willing to pay for it.With most senior miners cash cost well south of

$1000/oz, gold is clearly more expensive than pure marginal cost analysis would suggest.That premium is the amount that people are willing to pay for "protection" against inflation,

the collapse of fiat currencies, or whatever other event they think they are being shielded from.But that premiumis now falling because investors realize that other assets protect them

from these events much better.

If concerned about inflation, I would much rather own multifamily real estate than gold.Rents reset every year, so they should be well-indexed to inflation, and real estate is traditionally

favored in inflationary times.Moreover, real estate produces substantial current yield, something

that gold does not.

If worried about sociopolitical unrest, the US dollar or US treasuries are a much better alternative

than gold.The US dollar is being debased at a much lower rate than other competing currencies

(i.e. GBP or JPY, and likely soon EUR), and remains the world reserve currency, making it an

attractive safe haven.US treasuries also produce yield, and I believe are unlikely to fall much in

value over the next few years because inflation will need an increase in the velocity of money,

which will take much more time.

I also agree with you that the stock market is fundamentally overvalued (although I have thought

this for over a year now and been wrong), but I would even buy equities rather than gold if I was

worried about inflation.In an inflationary stance, companies should have pricing power and

grow their earnings near the rate of inflation, so equities should be able to keep pace with inflation

over a longer run.

I believe gold owners are figuring out this argument, especially as it pertains to the nascent bull

market in real estate, and that is why they are selling. I also think the "gold is just another currency"

argument is terribly flawed, as I have yet to go to a country where I can walk into Subway and buy

a foot-longwith gold or silver.Moreover, if gold were a currency, it would be viewed with a great

deal of skepticism considering it has fallen over 10% in one day before, something that has never

happened with a major currency.

I think as gold ETF holders continue to turn elsewhere to hedge their fears, the price of gold will

continue to fall, regardless of what happens in the risk market.If stocks continue to rise, people

will sell gold and buy stocks.If stocks fall, people will sell gold and buy real estate or treasuries.I strongly believe the bull market in gold is over, and over the course of the next couple years, we

will see substantially lower prices, eventually falling well below $1000/oz.

My definition of inflation is rising prices, with a bias towards consumer

prices vs. asset prices.In the past few years, US consumer prices have been flat or falling in my

estimation, while asset prices have been going through the roof.I believe a large part of the gold bull

market was an expectation of CPI inflation, that has simply failed to materialize.

I agree that gold prices have never tracked the CPI.Gold prices have risen and fallen for many

different reasons over the past few decades, but that is largely my point: gold's price is purely a

psychological function.That would also be my answer to your question about gold's utility,

its utility is simply what the next buyer is willing to pay, or said another way, its utility is the

reason the next buyer is buying it.That price had risen for a decade straight because of fears over

monetary debasement, inflation, and general pessimism on the effectiveness of central banking,

but it appears there are no more marginal buyers left.

The advent of gold ETFs brought a huge number of new players in the market, and they were

largely responsible for the run-up in prices from 2008 to 2011.However, many of these players

were simply allocating to gold because their advisors were telling them to, without truly

understanding why they were doing it.They were doing what investors do in any mature bull

market, they buy because the price is rising. Now, these same investors are selling because the

price is falling. Teoretically, they could turn around and start buying again, but the problem is,

what would actually cause this?What positive surprise is there left for gold that has not already

been disclosed?

When gold prices ran up to $1900/oz in September 2011, it was not quantitative easing that caused

it, but rather the expectation of QE3.At this point, the Fed has already indicated they will print

an unlimited amount of money, only varying the size of their asset purchases, with no time limit set.

It is already on the table that the Fed will print unlimited, so what positive surprise is left?Every

other central bank has stepped up their liquidity too over the past 1.5 years, yet the price of gold

continues to drop. My point is that, in the past, gold has served as protection against future currency

debasement, but it has now ceased to serve that function.This is a problem because gold only protects

us from anything if the rest of the market thinks it does.This key change in sentiment and market

thought on gold is why I believe the price is falling.

As I said before, with marginal cost on gold way below where it is now, there is plenty of room

for the metal to fall.In the long run, commodities must return to their marginal cost, even after

moving up or down according to demand shocks.As for central banks, I do not believe them to be a

reliable indicator of anything.If they knew what they were doing, the GFC would never have

happened in the first place.Also, central banks were massive net sellers of gold at the bottom i

in 2000, yet are big buyers of gold now that prices are near their all-time high.If anything,

they are a contrarian indicator.

Lastly, countries like Germany will probably continue to repatriate their gold because they

are broke.European countries are some of the largest holders of gold inthe world, and\

considering how high the price of gold is, I would want mine back too if I were them.

With their failing economies and possibly soon to be failing currency, gold is their asset of highest

worth.If Germany, Italy, and the EU were to sell their gold or have less of it, the credit of these

countries would almost certainly drop, in the same way that if they had less currency reserves.However, with the Cypriot central bank selling gold to finance their bailout recently, the writing

is on the wall that gold reserves may be tapped.This would turn the EU into net sellers of gold,

potentially dumping huge amounts onto the market if their debt crisis ever flares up again. END

…..So Ackman vs. Herbalife has no heroes. Both parties, in their own way, take advantage of the goodwill and trust that underlie capitalism. Herbalife recruits sales people with the knowledge–based on mathematical certainty but undisclosed to its recruits–that the vast majority will lose money. Mr. Ackman, for his part, has gotten rich betting against bad companies. One party is possibly immoral, the other party at best amoral. Who do you cheer for? –Mr. Karlgaard, publisher of Forbes (A Short Seller Takes on a Vitamin Vendor, WSJ Jan 4, 2013)

Yes this battle will be gruesome, bloody and long (perhaps) but our purpose is to understand whether Herbalife which–as of the last filing–sported franchise-like financials of high ROA, ROE and ROIC with growing sales. Copious cash flow. On the surface, the company seems to have a franchise. Why can’t other companies do the same thing. What barriers to entry are there? Product patents, customer captivity, economies of scale and scope, network effects, etc. This battle will allow us to understand what drove Herbalife’s success. Will it be fleeting or lasting. My bet is that Herbalife does NOT have a lasting competitive advantage.

The quote above by Mr. Karlgaard is disappointing because as a publisher of a business magazine, he should understand Mr. Ackman’s purpose. A good investor should invest in companies that will use owner’s capital wisely and should not invest or even warn against investing in companies that mis-allocate capital for the long-term. Short sellers are just as important as having a Warren Buffett in the market. An Ackman does more for future growth than any government program because–like him or not–Mr. Ackman is trying to take capital away from poorly managed, potential frauds, unsustainable businesses while allocating capital to companies that will use his investors’ capital beneficially. He may be proven wrong but that is for the market to decide.

UPDATE: MONEY SUPPLY EXPLOSION--We are now officially in double digit territory for non-seasonally adjusted 13 week annualized money supply (M2) growth. Here is the amazing ascent in growth over recent weeks: 5.1%, 5.6%, 6.6%, 7.1%, 7.5%, 7.8%, 8.2%, 8.4%, 8.7%, 9.0%, 9.3%, 9.6%, 9.9%, 10.7%. It is this growth that is going to fuel the U.S. economy, the U.S. stock market and commodities. www.economicpolicyjournal.com

Investing in Banks

I find investing in global banks like Bank of America or Citibank impossible because I have no way to value or understand their businesses. How much “shadow” banking do these entities engage in? I don’t want to find out the hard way. See the article below

Some four years after the 2008 financial crisis, public trust in banks is as low as ever. Sophisticated investors describe big banks as “black boxes” that may still be concealing enormous risks—the sort that could again take down the economy. A close investigation of a supposedly conservative bank’s financial records uncovers the reason for these fears—and points the way toward urgent reforms.

The financial crisis had many causes—too much borrowing, foolish investments, misguided regulation—but at its core, the panic resulted from a lack of transparency. The reason no one wanted to lend to or trade with the banks during the fall of 2008, when Lehman Brothers collapsed, was that no one could understand the banks’ risks. It was impossible to tell, from looking at a particular bank’s disclosures, whether it might suddenly implode. Red the whole article:

The authors of the above article don’t grasp the true cause of the banking panic. Yes, transparency is a problem, but that would ALWAYS be true under our current fractional reserve banking system–it’s inherently a Ponzi scheme that functions on public gullibility and government edict–banks get to violate private property rights.

PS: can anyone fill in the blanks? All panics arise from excess _______ over and above ___________. Correct answer wins this prize:

This was published on January 2, 2013, in Ron Paul’s Monetary Policy Anthology: Materials From the Chairmanship of the Subcommittee on Domestic Monetary Policy and Technology, US House of Representatives, 112th Congress. All the books mentioned in this article are free on the web, go to www.mises.org and do a book search by title.

The scholarly contributions of Murray N. Rothbard span numerous disciplines, and may be found in dozens of books and thousands of articles. But even if we confine ourselves to the topic of money, the subject of this volume, we still find his contributions copious and significant.

As an American monetary historian Rothbard traced the party politics, the pressure groups, and the academic apologists behind the various national banking schemes throughout American history. As a popularizer of monetary theory and history he showed the public what government was really up to as it took greater and greater control over money. As a business cycle expert he wrote scholarly books on the Panic of 1819 and the Great Depression, finding the roots of both in artificial credit expansion. And while the locus classicus of monetary theory in the tradition of the Austrian School is Ludwig von Mises’ 1912 work The Theory of Money and Credit, the most thorough shorter overview of Austrian monetary theory is surely chapter 10 of Rothbard’s treatise Man, Economy and State.

Rothbard placed great emphasis on the central monetary insight of classical economics, namely that the quantity of money is unimportant to economic progress. There is no need for the money supply to be artificially expanded in order to keep pace with population, economic growth, or any other factor. As long as prices are free to fluctuate, changes in the purchasing power of money can accommodate increases in production, increases in money demand, changes in population, or whatever. If production increases, for example, prices simply fall, and the same amount of money can now facilitate an increased number of transactions commensurate with the greater abundance of goods. Any attempt by “monetary policy” to keep prices from falling, to accommodate an increase in the demand for money, or to establish “price stability,” will yield only instability, entrepreneurial confusion, and the boom-bust cycle. There is no way for central bank policy or any form of artificial credit expansion to improve upon the micro-level adjustments that take place at every moment in the market.

With the exception of the Austrian School of economics, to which Rothbard made so many important contributions throughout his career, professional economists have treated money as a good that must be produced by a monopoly – either the government itself or its authorized central bank. Rothbard, on the other hand, teaches that money is a commodity (albeit one with unique attributes) that can be produced without government involvement. Rothbard’s history of money, in fact, is a history of small steps, the importance of which are often appreciated only in hindsight, by which government insinuated its way into the business of money production.

It was Carl Menger who demonstrated how money could emerge on the free market, and Ludwig von Mises who demonstrated that it had to emerge that way. In this as in so many other areas, Mises broke with the reigning orthodoxy, which in this case held that money was a creation of the state and held its value because of the state’s seal of approval. A corollary of the Austrian view was that fiat paper money could not simply be created ex nihilo by the state and imposed on the public. The fiat paper we use today would have to come about in some other way.

It was one of Rothbard’s great contributions to show, in his classic What Has Government Done to Our Money? and elsewhere, the precise steps by which the fiat money in use throughout the world came into existence. First, a commodity money (for convenience, let’s suppose gold) comes into existence on the market, without central direction, simply because people recognize that the use of a highly valued good as a medium of exchange, as opposed to persisting in barter, will make it easier for them to facilitate their transactions. Second, money substitutes began to be issued, and circulate instead of the gold itself. This satisfies the desires of many people for convenience. They would rather carry paper, redeemable into gold, than the gold itself. Finally, government calls in the gold that backs the paper, keeps the gold, and leaves the people with paper money redeemable into nothing. These steps, in turn, were preceded by the seemingly minor – but in retrospect portentous indeed – government interventions of monopolizing the mint, establishing national names for the money in a particular country (dollars, francs, etc.), and imposing legal tender laws.

Rothbard also brought the Austrian theory of the business cycle to a popular audience. Joseph Salerno, who has been called the best monetary economist working in the Austrian tradition today, was first drawn to the Austrian School by Rothbard’s essay “Economic Depressions: Their Cause and Cure.” There Rothbard laid out the problems that business cycle theory needed to solve. In particular, any theory of the cycle needed to account, first, for why entrepreneurs should make similar errors in a cluster, when these entrepreneurs have been chosen by the market for their skill at forecasting consumer demand. If these are the entrepreneurs who have done the best job of anticipating consumer demand in the past, why should they suddenly do such a poor job, and all at once? And why should these errors be especially clustered in the capital-goods sectors of the economy?

According to Rothbard, competing theories could not answer either of these questions satisfactorily. Certainly any theory that tried to blame the bust on a sudden fall in consumer spending could not explain why consumer-goods industries, as an empirical fact, tended to perform relatively better than capital-goods industries.

Only the Austrian theory of the business cycle adequately accounted for the phenomena we observe during the boom and bust. The cause of the entrepreneurial confusion, according to the Austrians, is the white noise the Federal Reserve introduces into the system by its manipulation of interest rates, which it accomplishes by injecting newly created money into the banking system. The artificially low rates mislead entrepreneurs into a different pattern of production than would have occurred otherwise. This structure of production is not what the free market and its price system would have led entrepreneurs to erect, and it would be sustainable only if the public were willing to defer consumption and provide investment capital to a greater degree than they actually are. With the passage of time this mismatch between consumer wants and the existing structure of production becomes evident, massive losses are suffered, and the process of reallocating resources into a sustainable pattern in the service of consumer demand commences. This latter process is the bust, which is actually the beginning of the economy’s restoration to health.

The concentration of losses in the capital-goods sector can be explained by the same factor: the artificially low-interest rates brought about by the Fed’s intervention into the economy. What Austrians call the higher-order stages of production, the stages farthest removed from finished consumer goods, are more interest-rate sensitive, and will therefore be given disproportionate stimulus by the Fed’s policy of lowering interest rates.

Equipped with this theory, Rothbard wrote America’s Great Depression(1963). There Rothbard did two things. First, he showed that the Great Depression had not been the fault of “unregulated capitalism.” After explaining the Austrian theory of the business cycle and showing why it was superior to rival accounts, Rothbard went on to apply it to the most devastating event in U.S. economic history. In the first part of his exposition, Rothbard focused on showing the extent of the inflation during the 1920s, pointing out that the relatively flat consumer price level was misleading: given the explosion in productivity during the roaring ’20s, prices should have been falling. He also pointed out how bloated the capital-goods sector became vis-a-vis consumer goods production. In other words, the ingredients and characteristics of the Austrian business cycle theory were very much present in the years leading up to the Depression.

Second, Rothbard showed that the persistence of the Depression was attributable to government policy. Herbert Hoover, far from a supporter of laissez-faire, had sought to prop up wages during a business depression, spent huge sums on public works, bailed out banks and railroads, increased the government’s role in agriculture, impaired the international division of labor via the Smoot-Hawley Tariff, attacked short sellers, and raised taxes, to mention just a portion of the Hoover program.

Rothbard had been interested in business cycles since his days as a graduate student. He had intended to work on a history of American business cycles for his Ph.D. dissertation under Joseph Dorfman at Columbia University, but he found out that the first major cycle in American history, the Panic of 1819, provided ample material for study in itself. That dissertation eventually appeared as a book, via Columbia University Press, called The Panic of 1819: Reactions and Policies (1962). In that book, which the scholarly journals have declared to be the definitive study, Rothbard found that a great many contemporaries identified the Bank of the United States – which was supposed to be a source of stability – as the primary culprit in that period of boom and bust. American statesmen who had once favored such banks, and who thought paper money inflation could be a source of economic progress, converted to hard money on the spot, and proposals for 100-percent specie banking proliferated.

In A History of Money and Banking: The Colonial Era to World War II, a collection of Rothbard’s historical writings published after the author’s death, Rothbard traced the history of money in the United States and came up with some unconventional findings. The most stable period of the nineteenth century from a monetary standpoint turns out to be the period of the Independent Treasury, the time when the banking system was burdened with the least government involvement. What’s more, the various economic cycles of the nineteenth century were consistently tied to artificial credit expansion, either participated in or connived at by government and its privileged banks. Rothbard further showed that the traditional tale of the 1870s, when the United States was supposed to have been in the middle of the “Long Depression,” was all wrong. This was actually a period of great prosperity, Rothbard said. Years later, economic historians have since concluded that Rothbard’s position had been the correct one.

Rothbard’s treatment of the Federal Reserve System itself, which he dealt with in numerous other works, involved the same kind of analysis that historians like Gabriel Kolko and Robert Wiebe applied to other fruits of the Progressive Era. The conventional wisdom, as conveyed in the textbooks, is that the Progressives were enlightened intellectuals who sought to employ the federal regulatory apparatus in the service of the public good. The wicked, grasping private sector was to be brought to heel at last by these advocates of social justice.

New Left revisionists demonstrated that this version of the Progressive Era was nothing but a caricature. The dominant theme in Progressive thought was expert control over various aspects of society and the economy. The Progressives were not populists. They placed their confidence in a technocratic elite administering federal agencies removed from regular public oversight. What’s more, the resulting regulatory apparatus tended to favor the dominant firms in the market, which is why the forces of big business were in sympathy with, rather than irreconcilably opposed to, the Progressive program. “With such powerful interests as the Morgans, the Rockefellers, and Kuhn, Loeb in basic agreement on a new central bank,” Rothbard wrote, “who could prevail against it?”

It is with these insights in mind that Rothbard scrutinized the Federal Reserve. He would have none of the idea that the Fed was the creation of far-seeing public officials who sought to subject the banking system to wise regulation for the sake of the people’s well-being. The Fed was created not to punish the banking system, but to make its fractional-reserve lending operate more smoothly. In The Case Against the Fed, What Has Government Done to Our Money?, and The Mystery of Banking, Rothbard took the reader through the step-by-step process by which the banks engaged in credit expansion, earning a return by lending money created out of thin air. Without a central bank to coordinate this process, Rothbard showed, the banks’ position was precarious. If one bank inflated more than others, those others would seek to redeem those notes for specie and the issuing bank would be unable to honor all the redemption claims coming in.

The primary purpose of the central bank, therefore, in addition to propping up the banks through its various liquidity injections and its position as the lender of last resort, is to coordinate the inflationary process. When faced with the creation of new money by the Fed, the banks will inflate on top of this new money at the same rate (as determined by the Fed’s reserve requirement for banks). Therefore, the various redemptions will tend, on net, to cancel each other out. This is what Rothbard meant when he said the central bank made it possible to “inflate the currency in a smooth, controlled, and uniform manner throughout the nation.”

Although Rothbard distinguished himself as a monetary theorist and as a monetary historian, he did not confine himself to theory or history. He devoted plenty of attention to the here and now – to critiques of Federal Reserve policy, for example, or to criticisms of government responses to the various fiascoes, the Savings and Loan bailout among them, to which our financial system is especially prone. He likewise looked beyond the present system to a regime of sound money, and in The Case for a 100 Percent Gold Dollar and The Mystery of Banking laid out a practical, step-by-step plan to get there from here.

In his work on monetary theory and history, as in his work in so many other areas, Rothbard showed from both an economic and a moral point of view why a system of liberty was preferable to a system of government control. At a time when the political class and the banking establishment are being subjected to more scrutiny than ever, the message of Rothbard takes on a special urgency.

For that reason we should all be grateful that his monetary work, and that of the other great Austrian economists, is being carried on by Murray Rothbard’s friend and colleague Ron Paul. By my reckoning, no one in history has brought true monetary theory and history to a larger audience.

Mr. Viera says, “We have an irredeemable paper (electronic) currency coming out of a private banking cartel for which the American people are on the hook for some type of bailout. Of course, the banking cartel will always go to the public and say we made terrible mistakes–that if you don’t bail us out, the result will be total collapse. And by the way, next time will be worse. This cycle just perpetuates until the end—a hyperinflationary collapse of 50% monthly depreciation of the U.S. dollar. Ugly.

A reader, Mohammed Al-Alwan, graciously pointed out an interesting web-site for value investors. Some interesting articles here: http://www.valueinstitute.org/default.asp

We mentioned the struggles of Fairholme Funds holding concentrated positions in financial companies like Bank of America (BAC) and American International Group (AIG) here: http://wp.me/p1PgpH-dT

You will understand the risks from reading What has the Government Done to Our Money? Posted here: http://wp.me/p1PgpH-dX. From pages 56 and 57:

A bank, then, is not taking the usually business risk. It does not, like all businessmen, arrange the time pattern of its assets proportionately to the time pattern of liabilities, i.e., see to it that it will have enough money, on due dates, to pay its bills. Instead, most of its liabilities are instantaneous, but its assets are not.

The bank creates new money out of thin air, and does not, like everyone else, have to acquire money by producing and selling its services. In short, the bank is already and at all times bankrupt; but its bankruptcy is only revealed when customers get suspicious and precipitate “bank runs.” No other business experiences a phenomenon like a “run.” No other business can be plunged into bankruptcy overnight simply because its customers decide to repossess their own property. No other business creates fictitious new money, which will evaporate when truly gauged.

Today I read a very technical article on credit derivatives as used by banks (and other institutions), and in the end I came away thinking “this is madness.” There are so many hairy problems involved here in attempting to price these things and no one knows the answers. I think answers are unobtainable. The assumptions being made about measuring risks are untenable. In an “Austrian” world, no one can predict them and past distributions do not suffice. Banks doing large amounts of trading in derivatives do not know what their risks are. However, astoundingly, huge sums of money are recorded as gains and losses on accounting statements based on estimates of risk parameters that no one actually is sure of.