I’m sorry, if you were right, I’d agree with you.–Robin Williams

CAPATCOLUMBIA

Free Value Investing Course Work here: www.Capatcolumbia.com

Kahneman Podcast on Uncertainty

Professor Kahneman uses a variety of examples to discuss the inside/outside view, statistics and stories and prediction. (1:02:45). This radical pessimist says, “The world makes more sense to us than it really is.” Excellent Podcast! http://www.thoughtleaderforum.com/default.asp?P=909655&S=945705

Other interesting lectures as well at www.thoughtleaderforum.com

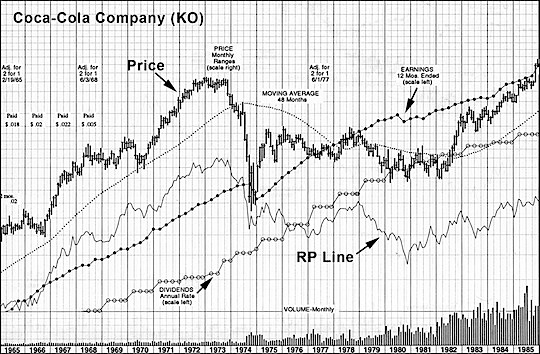

Key takeaway: As a value investor when investing in a franchise with a winner take all market-BE PATIENT.

Federal Reserve Lectures

Bernanke Lectures on the Federal Reserve: http://www.federalreserve.gov/newsevents/press/other/20120126a.htm

Counterpoint to Bernanke’s Lectures: http://www.economicpolicyjournal.com/2012/01/march-madness-bernanke-versus-rothbard.html

Austrian Value Investor, Jim Rogers

A value investor who incorporates “Austrian” economics into his investing: http://en.wikipedia.org/wiki/Jim_Rogers

The State of America Today

Oglala Sioux, Russell Means gives a State of the Union Address. http://www.economicpolicyjournal.com/2012/01/russell-means-endorses-ron-paul.html More informative than Obama’s recent address to the nation last week. Forget the Paul endorsement and instead ask as an investor–if change occurs at the margin, does the Patriot Act and Obama’s recent rejection of the Keystone Pipeline (http://www.washingtonpost.com/opinions/obamas-keystone-pipeline-rejection-is-hard-to-accept/2012/01/18/gIQAf9UG9P_story.html) raise the cost of capital for American companies in general (P/E multiples become compressed).

Russell Charles Means (born November 10, 1939) is an Oglala Sioux activist for the rights of Native American people. He became a prominent member of the American Indian Movement (AIM) after joining the organisation in 1968, and helped organize notable events that attracted national and international media coverage. The organization split in 1993, in part over the 1975 murder of Anna Mae Aquash, the leading woman activist in AIM.[1]

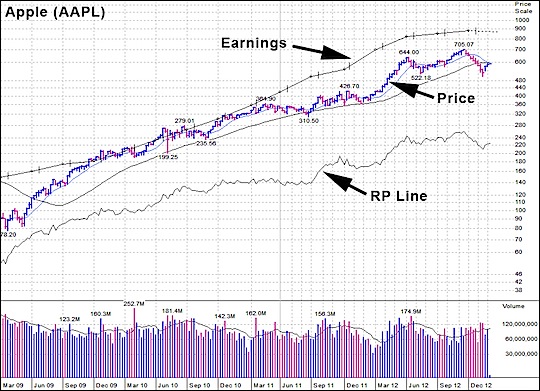

Greenwald Student Discusses Apple’s Success

From his email: This is what Greenwald will probably say, which is partly true. But you can put anything to his framework (once successful), and say that is their core competency.

1. Apple’s core expertise is in design, and they extend this design to all products.

2. They don’t manufacture the hardware. They assemble them and wrap it in a much better design. Everything that goes into the hardware, CPU, Hard disks, Memory is not made by them.

3. They do software – some of it, like the OS, etc. They don’t do everything. Even steve jobs says, Focus, Focus, get rid of the things that we don’t want. He gave the Google guys the same advice. Don’t become like Microsoft – don’t try to do a lot of things. Stick to four or five things.

You can also think about Steve Jobs as someone who has come and reduced the inefficiencies. I mean when each person has three/four devices that he can access information from – it will be so much better if someone integrates the content. If you take a picture, and you can seamlessly see it on your iPad, Itouch, Mac, Apple TV (not yet released), customers would benefit. Same applies to email, contacts, etc. (rather than taking a usb stick and moving it around all the time).

They are creating products where there is a need like any entrepreneur.

Reader Question on Real Savings

In “Other Views on Inflation and Stocks” section from this post:http://wp.me/p1PgpH-kz, the Mises links talk about the pool of real savings. What is the author referring to? Does the real pool of savings track real changes in the exchange of goods and services?

My reply: Not exactly……see below. Savings is not the transfer of REAL goods and services being exchanged back and forth, but the postponement of present consumption for the future.

Why Government Data on Saving is Misleading

The nature of the market economy is such that it allows various individuals to specialize. Some individuals engage in the production of final consumer goods, while other individuals engage in the maintenance and enhancement of the production structure that permits the production of final consumer goods.

We suggest that it is the producers of final consumer goods that fund — that is, sustain — the producers in the intermediary stages of production. Individuals who are employed in the intermediary stages are paid from the present output of consumer goods. The present effort of these individuals is likely to contribute to the future flow of consumer goods. Their present effort however, does not make any contribution to the present flow of the production of these goods.

The amount of consumer goods that an individual earns is his income. The earned consumer goods, or income, supports the individual’s life and well-being.

Observe that it is the producers of final consumer goods that pay the intermediary producers out of the existing production of final consumer goods. Hence, the income that intermediary producers receive shouldn’t be counted as part of overall national income — the only relevant income here is that which is produced by the producers of final consumer goods.

For instance, John the baker has produced ten loaves of bread and consumes two loaves. The income in this case is ten loaves of bread, and his savings are eight loaves. Now, he exchanges eight loaves of bread for the products of a toolmaker. John pays with his real savings — eight loaves of bread — for the products of the toolmaker.

One may be tempted to conclude that the overall income is the ten loaves that were produced by the baker, plus the eight loaves that were earned by the toolmaker. In reality, however, only ten loaves of bread were produced — and this is the total income.

The eight loaves are the savings of the baker, which were transferred to the toolmaker in return for the tools. Or, we can say that the baker has invested the eight loaves of bread. The tools, in turn, will assist at some point in the future to expand the production of bread. These tools, however, have nothing to do with the current stock of bread.

While the producers of final consumer goods determine the present flow of savings, other producers could have a say with respect to the use of real savings. For instance, the toolmaker can decide to consume only six loaves of bread and use the other two loaves to purchase some materials from material producers.

This additional exchange, however, will not alter the fact that the total income is still ten loaves of bread and the total savings are still eight loaves. These eight loaves support the toolmaker (six loaves) and the producer of materials (two loaves). Note that the decision of the toolmaker to allocate the two loaves of bread towards the purchase of materials is likely to have a positive contribution toward the production of future consumer goods.

The introduction of money will not alter what we have said. For instance, the baker exchanges his eight saved loaves of bread for eight dollars (under the assumption that the price of a loaf of bread is one dollar).

Now, the baker decides to exchange eight dollars for tools. This means that the baker transfers his eight dollars to the toolmaker. Again, what we have here is an investment in tools by the baker, which at some point in the future will contribute toward the production of bread. The eight dollars that the toolmaker receives are on account of the baker’s decision to make an investment in tools.

Note once more that the tools the toolmaker sold to the baker didn’t make any contribution toward the present income — that is, the production of the present ten loaves of bread. Likewise, there is no contribution to the total present income if the toolmaker exchanges two dollars for the materials of some other producer. All that we have here is another transfer of money to the producer of materials.

Obviously, then, counting the amount of dollars received by intermediary producers as part of the total national income provides a misleading picture as far as total income is concerned.

Yet this if precisely what the NIPA framework does. Consequently, savings data as calculated by the NIPA is highly questionable.

The NIPA Follows the Keynesian Model

The NIPA framework is based on the Keynesian view that spending by one individual becomes part of the earnings of another individual. Each payment transaction thus has two aspects: the spending of the purchaser is the income of the seller. From this it follows that spending equals income.

So, if people maintain their spending, they keep income levels from falling. And this is why consumer spending is viewed as the motor of an economy.

The total amount of money spent is driven by increases in the supply of money. The more money that is created out of thin air, the more of it will be spent — and therefore, the greater the NIPA’s national income will measure (see Figure 2). Thus, an increase in the money supply on account of central bank policies and fractional-reserve banking makes the entire calculation of the total income even more questionable.

Since this money was created out of thin air, it is not backed by any real goods; income in terms of dollars cannot reflect the true income. In fact, the more a central bank pumps additional money into the economy, the more damage is inflicted on the real income. As a result, money income rises while real income shrinks.

Real Savings mentioned http://mises.org/daily/3640

Is there a glut of real savings? Money is not savings: http://mises.org/daily/1882

Good and bad credit: http://mises.org/daily/3151

From Frank Shostak: Do People Save Money?

Is it true that individuals are saving a portion of their money income? Do people save money?

Out of a given money income, an individual can do the following:

he can exchange part of the money for consumer goods;

he can invest;

he can lend out the money (i.e., transfer his money to another party in return for interest);

he can also keep some of the money (i.e., exercise a demand for money).

At no stage, however, do individuals actually save money.

In its capacity as the medium of exchange, money facilitates the flow of real savings. The baker can now exchange his saved bread for money and then exchange the money for final or intermediary goods and services.

What is commonly called “saving” is nothing more than exercising demand for the medium of exchange (i.e., money). This means that people don’t actually save money but rather exercise demand for it. And, when an individual likewise exchanges his real savings for money, he in fact only increases demand for money. The money he receives is not income; it is a medium of exchange that enables the individual to secure goods. In the absence of final consumer goods, all of the money in the world would be of little help to anyone.

My reply: The extent to which an individual will save is explained by his time preference. Savings is deferred consumption. Deferred consumption allows for resources to be used for longer stages of production which should boost productivity.

Read chapter 14 in Capitalism especially pages: 622-651.

For a graphical discussion of real savings read Man, Economy and State pages: 367 to 451 and 517 to 521.

I will speak to a real Austrian economist this week and ask what are REAL savings and see if I can give you a more concise answer.

Another Reader Question:

Also, let’s say that we have a world currency (dollars) and a world Federal

Reserve. If money is dropped from a helicopter into a jungle and every dollar is picked up by a group of 10 individuals, then those 10 individuals would benefit from essentially receiving free money, correct? Their savings would increase and they could use their new found money to purchase capital goods. Society as a whole would lose because REAL savings and REAL capital goods and services exchange would not increase. There would be more money in circulation chasing the same amount of goods, which would cause prices to rise and/or the value of the currency to decline? Does that sound correct?

My reply: Yes, they would benefit as would any counterfeiter would benefit spending the money first before prices can adjust fully. The gain of the early beneficiaries is matched by the losses in real purchasing power of the people who are the last to receive the money AFTER prices have adjusted. You are correct that real savings would NOT increase. In fact, the structure of production is thrown off which in the end hurts society (boom and bust) in addition to the unfairness of inflation. The money printing distorts production causing mal-investment which depletes REAL savings.

Frank Shostak comments: Consider the so-called helicopter money case: the Fed sends every individual a check for one thousand dollars. According to the NIPA accounting, this would be classified as a tremendous increase in personal income. It is commonly held that, for a given consumption expenditure, this would also increase personal savings.

However, we maintain that this has nothing to do with real income and thus with saving. The new money didn’t increase total real income.

What the new money has done is set in motion the diversion of real income from wealth generators to the holders of new money. The new money that the Fed has created out of thin air prompts exchanges of nothing for something. Consequently, wealth generators have less real wealth at their disposal — which means that the process of real wealth and savings formation has weakened.

In the helicopter example we have a situation in which, for a given pool of real savings, an increase in nonproductive consumption took place. (By nonproductive consumption we mean consumption that is not backed up by the production of real wealth.) This means that the real savings of wealth generators, rather than being employed in wealth generation, is now being squandered by nonproductive consumption.

From this, we can also infer that the policies aimed at boosting consumer spending do not produce real economic growth, but in fact weaken the bottom line of the economy.

In the NIPA framework, which is designed according to Keynesian economics, the more money people spend, all else being equal, the greater total income will be. Conversely, the less money is spent (which is labeled as savings), the lower the income is going to be. This means that savings is bad news for an economy.

We have, however, seen that it is precisely real savings that pays — i.e., that which supports the production of real wealth. Hence, the greater the real savings in an economy, the more are the activities that can be supported.

What keeps the real economic growth going, then, is not merely more money, but wealth generators — those who invest a part of their wealth in the expansion and the maintenance of the production structure. It is this that permits the increase in the production of consumer goods, which in turn makes it possible to increase the consumption of these goods.

Only out of a greater production can more be consumed.

Can the State of Savings be Quantified?

What matters for economic growth is the amount of total real savings. However, it is not possible to quantify this total.

To calculate a total, several data sets must be added together. This requires that the data sets have some unit in common. There is no unit of measurement common to refrigerators, cars, and shirts that makes it possible to derive a unified “total output.”

The statisticians’ technique of employing total monetary expenditure adjusted for prices simply won’t do. Why not? To answer this, we must ask: what is a price? A price is the amount of money asked per unit of a given good.

Suppose two transactions were conducted. In the first transaction, one TV set is exchanged for $1,000. In the second transaction, one shirt is exchanged for $40. The price, or the rate of exchange, in the first transaction is $1,000 per TV set. The price in the second transaction is $40 per shirt. In order to calculate the average price, we must add these two ratios and divide them by 2. However, it is conceptually meaningless to add $1,000 per TV set to $40 per shirt. The thought experiment fails.

The Real Culprit

Rather than attempting the impossible, as far as calculating real savings is concerned, one should instead focus on the factors that undermine real savings. We suggest that the key damaging factors are central bank’s and government’s loose monetary and fiscal policies.

These policies are instrumental in the weakening of the process of real savings formation through the diversion of real savings from wealth generators to non-wealth-generating activities.

The US economy has been subjected to massive monetary pumping since early 1980 via the introduction of financial deregulations. The ratio of our monetary measure AMS to its trend jumped from 1.17 in January 1980 to 3.5 in July 2009. (The trend values were calculated by a regression model, which was estimated for the period 1959 to 1979, the period prior the onset of financial deregulations).

Likewise, the US economy was subjected to massive government spending. For the fiscal year 2009, US federal government outlays are expected to stand at $3.5 trillion.

The outlays-to-trend ratio (the trend was estimated for the period 1955 to 1979) jumped to 4.1 in 2009, up from 3.5 in 2008 and 1.45 in 1980.

The ever-expanding government outlays are also depicted by the federal debt, which stands at $11.6 trillion thus far into 2009. Against the background of massive monetary pumping and ever-expanding government, we suggest that this raises the likelihood that the pool of real savings could be in serious trouble.

That this could be the case is also suggested by the private sector debt-to-its-trend ratio. This ratio stood at 5.8 in first quarter, against a similar figure from the previous quarter. The ever-rising ratio raises the likelihood that the increase in the private sector debt is on account of nonproductive debt. Real savings, instead of funding wealth generating activities, have been supporting non-wealth-generating activities. This weakens the ability of wealth-generating activities to grow the economy.

We can conclude that, given prolonged reckless fiscal and monetary policies, there is a growing likelihood that the pool of real savings is in trouble. If our assessment is valid, this means that US real economy is likely to struggle in the quarters ahead.

In addition, if the pool of real savings is under pressure, none of the government and central-bank policies to lift the economy is going to work. Note that as long as the pool of real savings is holding its ground, such policies appear to be effective. In reality, though, it is the expanding pool of real savings that drives the economy — and not various stimulus policies.

Conclusions

According to latest US government data, the personal saving rate jumped to 4.6% in June this year after settling at 0.4% in June last year. We suggest that on account of an erroneous methodology, the so-called “saving rate” that the government presents has nothing to do with true savings.

Since early 1980s, the ever-rising money supply and government outlays have severely undermined the process of real savings formation. As a result, it will not surprise us if the US pool of real savings is in serious trouble. If what we are saying is valid then it will be very hard for the US economy to grow, for it is a growing pool of real savings that makes economic growth possible.

Furthermore, the growing pool of real savings is the reason that loose monetary and fiscal policies appear to be working. In reality, however, all that these loose policies achieve is a further depletion of the pool of real savings — thus reducing prospects for a genuine economic recovery.