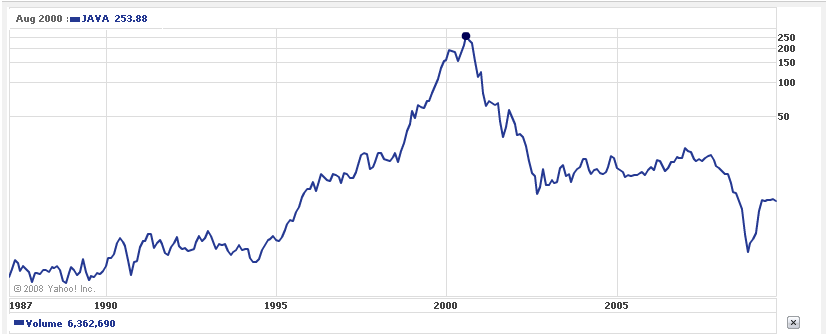

While at all times Wall Street analysts try to justify the valuations, here is a fun quote (via Bloomberg) from 2002 looking back from Scott McNeely, the CEO of Sun Microsystems, one of the darlings of the 2000 tech bubble:

“At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes.

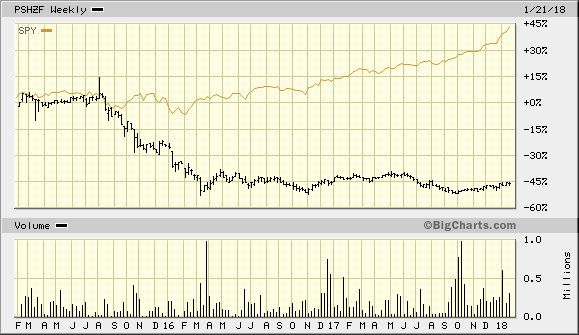

Ackman’s embattled Pershing Square hedge fund laid off 18 percent of its staff on Friday — a total of 10 pink slips that brought head count down to 46.

Investors have suffered in Pershing Square (PSHZF) vs. S&P 500:

He wants to hire an analyst who can THINK INDEPENDENTLY. You walk into his office and he asks you, “Can you think independently as an analyst?”

How do you reply. Be careful…………think for awhile before you reply. What proof can you give?

Technical analysis, in all of its forms, uses the past price movements to predict the future price movements. In some cases (e.g. momentum analysis) it calculates an intermediate signal from the price signal (momentum is the first derivative of price). But no matter the style, one analyzes price history to guess the next price move.

This is necessarily probabilistic. There is no way to know that a particular price move will follow the chart pattern you see on the screen. There is no certainty. And when it does work, it is often because of self-fulfilling expectations. Since all traders have access to the same charts, and the same chart-reading theories, they can buy or sell en masse when the chart signals them to do so.

Fundamentals or Arbitrage:

Arbitrage works just like a spring. If the price in the futures market is greater than the price in the spot market, then there is a profit to carry gold—to buy metal in the spot market and sell a futures contract. If the price of spot is higher, then the profit is to be made by decarrying—to sell metal and buy a future.

There are two keys to understanding this. One, when leveraged speculators push up the price of gold futures contracts, then that increases the basis spread. A greater basis is a greater incentive to the arbitrageur to take the trade. Two, when the arbitrageur buys spot and sells a future, the very act of putting on this trade compresses the spread.

If someone were to come along and sell enough futures contracts to push down the price of gold by $50 or $150 or whatever amount is alleged, then this selling would be on futures only. It would push the price of futures below the price of spot, a condition called backwardation.

Backwardation just has not happened at the times when the stories of the big “smash downs” have claimed. Monetary Metals has published intraday basis charts during these events many times.

The above does not describe technical analysis. It describes physics—how the market functions at a mechanical level.

There are other ways to check this. If there was a large naked short position in a contract that was headed into expiry, how would the basis behave? The arbitrage theory predicts the opposite basis move. We will leave the answer out as an exercise for the interested reader, as thinking this through is really good work to understand the dynamics of the gold and silver markets (and you can Google our past articles, where we discuss it).

This check can be observed every month, as either gold or silver has a contract expiring (right now it’s gold, as the April contract is close to First Notice Day).

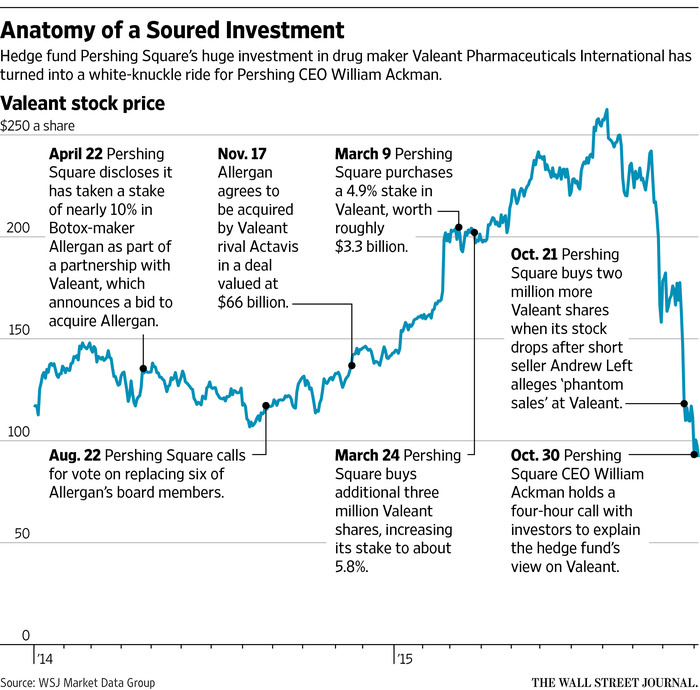

Ironically, one of the best research on Valeant was done by Allergan: Allergan analysis of Valeant 2014. Did Ackman’s analysts even read it? At least you have an example of solid research.

Compare to Ira-Sohn-2015-Presentation on Valeant and Other Platform Companies Studying the two different presentations provides a FREE course on valuation and presenting a research idea. But not 1 person in 10,000 would be willing to sweat the details like studying the two documents linked above.

Mr. Ackman calls you into his office and tells you that he shorted gold three days ago, because he wants to make money to support his positions in VRX, etc. Goldman Sachs promised sub-$1,000 gold in 2015. He ignored whatever you said because you are a “junior” analyst. But today gold is up $50 +. Pershing Square recently installed two hotlines: 1. for investor suicide prevention and 2. for death threats. Phones are ringin’ off the hook.

Also, this morning Janet Yellen had a nervous breakdown during her testimony to Congress. She told Congress that, “We have no clue what is going on.” Then she asked Congressional leaders to join her in prayer, “God, Help us!”

Part II on Valeant Let’s pretend you are asked to evaluate the situation for Mr. Ackman. He is in deep #$%^& and has brought in fresh eyes to advise him. Pershing Square has had to install two hotlines–Hotline 1: for investor suicide calls and Hotline 2: for investors who wish to phone-in death threats.

All bad joking aside, you have a huge pile of information to present the critical issues. Do you advise Mr. Ackman to buy more, sell immediately, sell down to a “more reasonable amount,” or hold? Use reason not opinion or emotion to guide you.

Step back and ask what are the important issues? What is Valeant worth? Can you know that? Pretend you are an investigative journalist trying to uncover the story.

What does Valeant do? Does Valeant have assets or a business method that gives the company a higher sustainable return on capital? What roll-ups/acquisition firms have been very successful in the past and how was success achieved?

Then you can read all the rumours and commentary swirling around Valeant, but be quick to focus on what you determine to be important. There are several links in the documents for you to follow further.

You can follow the reactions of investors and analysts at Seeking Alpha.

Hedge Fund Herding The psychological aspects of following others and the pressures of the short-term performance derby. Lesson: Never cease to do YOUR own thinking and analysis.

Readers should share if they believe there are actionable lessons here for investors in terms of psychology, portfolio management and analysis. Time is precious so we need to learn the important lessons.

And that ladies and gentlemen is called a permanent loss of capital IF investors paid too much for growth in a company doing roll-ups of commodity-like products (generic drugs) at unsustainable retail prices (competition and insurer push-back will cap price gains).

—

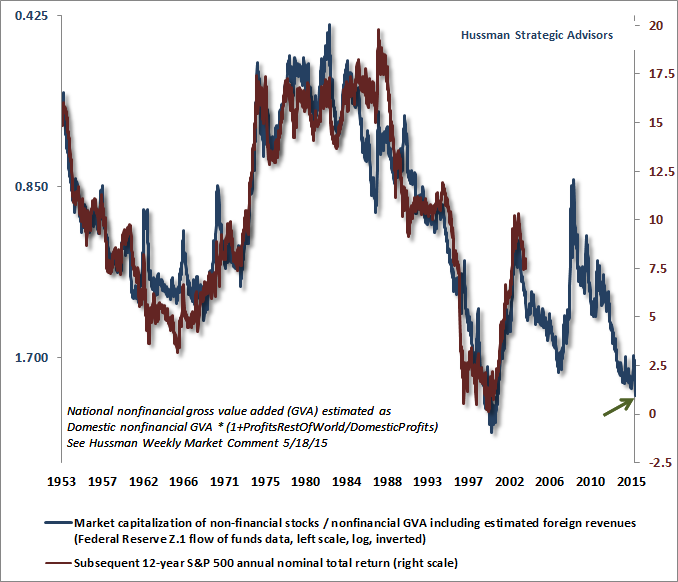

Meanwhile, investors face the second most overvalued equity market in history (Source: Hussman Funds).

You must know yourself if you want to accomplish anything in life–Jim Rogers, A Gift to My Children

We need to do our best to break the dangerous cycle of investment returns impacting our mood. The best way to do this is by not focusing on outcomes, but on the process you used to make decisions. Most of us also have a tendency to anchor off our peak net worth or the high point of the portfolio in the current year. Ravee Mehta, The Emotionally Intelligent Investor

KILL BILL

CSInvestor: As I learned during “my best day ever” http://wp.me/p2OaYY-1Ez arrogance and overconfidence bring forth tragedy as in any Greek drama.

Have a Good Weekend!

Editor’s Note: There is as much ego as money behind Dan Loeb and Bill Ackman’s battle over the nutritional company Herbalife. The story of their cycling trip from Bridgehampton to Montauk, which has practically achieved urban-legend status in the hedge-fund eco-system, provides a vivid example of what is at stake for the two former friends. Vanity Fair contributing editor William D. Cohan gets Ackman’s response on the ride in a story on the rivals that will appear in the April issue. Read an excerpt here—the full story will be released next week.

The supremely confident billionaire hedge-fund manager Bill Ackman has never been afraid to bet the farm that he’s right.

In 1984, when he was a junior at Horace Greeley High School, in affluent Chappaqua, New York, he wagered his father $2,000 that he would score a perfect 800 on the verbal section of the S.A.T. The gamble was everything Ackman had saved up from his Bar Mitzvah gift money and his allowance for doing household chores. “I was a little bit of a cocky kid,” he admits, with uncharacteristic understatement.

Tall, athletic, handsome with cerulean eyes, he was the kind of hyper-ambitious kid other kids loved to hate and just the type to make a big wager with no margin for error. But on the night before the S.A.T., his father took pity on him and canceled the bet. “I would’ve lost it,” Ackman concedes. He got a 780 on the verbal and a 750 on the math. “One wrong on the verbal, three wrong on the math,” he muses. “I’m still convinced some of the questions were wrong.”

Not much has changed in the nearly 28 years since Ackman graduated from high school, except that his hair has gone prematurely silver. He still has an uncanny knack for making bold, brash pronouncements and for pissing people off. Nowhere is that more apparent than in the current, hugely public fight he and his $12 billion hedge fund, Pershing Square Capital, are waging over the Los Angeles–based company Herbalife Ltd., which sells weight-loss products and nutritional supplements using a network of independent distributors. Like Amway, Tupperware, and Avon, Herbalife is known as “a multi-level marketer,” or MLM, with no retail stores. Instead, it ships its products to outlets in 88 countries, and the centers recruit salespeople, who buy the product and then try to resell it for a profit to friends and acquaintances.

Ackman has called Herbalife a “fraud,” “a pyramid scheme,” and a “modern-day version of a Ponzi scheme” that should be put out of business by federal regulators. He says he is certain Herbalife’s stock, which in mid-February traded around $40 per share, will go to zero, and he has bet more than a billion dollars of his own and his investors’ money on just that outcome. (Ackman declines to discuss the specifics of his trade.) “This is the highest conviction I’ve ever had about any investment I’ve ever made,” he announced on Bloomberg TV. An interviewer on CNN reminded him that Herbalife had been around since 1980 and had withstood many previous challenges to its business plan. How long was he willing to “sit on this bet”? Ackman replied, “We’re not sitting. We’re shouting from the rooftops. They’ve never had someone like me prepared to say the truth about the company. I’m going to the end of the earth. If the government comes out and determines this is a completely legal business, then I will lobby Congress for them to change the law. I had a moral obligation. If you knew that Bernie Madoff was running a Ponzi scheme, and you didn’t tell anyone about it, and it went on for 33 years … ”

Ackman says he suspected, when he “shorted” (i.e., bet against) Herbalife, that other hedge-fund investors would likely see the move as an opportunity to make money by taking the other side of his bet. What he hadn’t counted on, though, was that there would be a personal tinge to it. It was as if his colleagues had finally found a way to express publicly how irritating they have found Ackman all these years. Here finally was a chance to get back at him and make some money at the same time. The perfect trade. These days the Schadenfreude in the rarefied hedge-fund world in Midtown Manhattan is so thick it’s intoxicating.

“Ackman seems to have this ‘Superman complex,’ ” says Chapman Capital’s Robert Chapman, who was one of the investors on the other side of Ackman’s bet. “If he jumped off a building in pursuit of super-human powered flight but then slammed to the ground, I’m pretty sure he’d blame the unanticipated and unfair force of gravity.”

Lined up against the 46-year-old Ackman on the long side of the Herbalife trade were at least two billionaires: Daniel Loeb, 51, of Third Point Partners, who used to be Ackman’s friend, and Carl Icahn, 77, of Icahn Enterprises. Along for the ride are some smaller, well-regarded hedge-fund investors—who would like to be billionaires—John Hempton, of Bronte Capital, and Sahm Adrangi, of Kerrisdale Capital.

It’s Ackman’s perceived arrogance that gets to his critics. “The story I hear from everybody is that one can’t help but be intrigued by the guy, just because he’s somewhat larger than life, but then one realizes he’s just pompous and arrogant and seems to have been born without the gene that perceives and measures risk,” says Chapman. “He seems to look at other members of society, even legends such as Carl Icahn, as some kind of sub-species. The disgusted, annoyed look on his face when confronted by the masses beneath him is like one you’d expect to see [from someone] confronted by a homeless person who hadn’t showered in weeks. You can almost see him puckering his nostrils so he doesn’t have to smell these inferior creatures. It’s truly bizarre, given that his failures—Target, Borders, JCPenney, Gotham Golf, First Union Real Estate, and others—prove he’s as fallible as the next guy. Yet, from what I hear, he behaves that way with just about everybody.”

Another hedge-funder describes the problem he has with Ackman in more measured tones. “There is a saying in this business: ‘Often wrong, never in doubt.’ Ackman personifies it He is very smart—but he lets you know it. And he combines that with this sort of noblesse oblige that lots of people find offensive—me, generally not. On top of that he is pointlessly, needlessly competitive every time he opens his mouth. Do you know about the Ackman cycling trip with Dan Loeb?”

It’s Not About the Bike

The story of the Ackman-Loeb cycling trip is so widely known in the hedge-fund eco-system that it has practically achieved urban-legend status, and Loeb himself was eager to remind me of it.

It happened last summer when Ackman decided to join a group of a half-dozen dedicated cyclists, including Loeb, who take long bike rides together in the Hamptons. The plan was for Loeb, who is extremely serious about fitness and has done sprint triathlons, a half-Ironman, and a New York City Marathon, to pick up Ackman at Ackman’s $22 million mansion, in Bridgehampton. (Ackman also owns an estate in upstate New York and lives in the Beresford, a historic co-op on Manhattan’s Central Park West.) The two would cycle the 20 or so miles to Montauk, where they would meet up with the rest of the group and ride out the additional 6 miles to the lighthouse, at the tip of the island. “I had done no biking all summer,” Ackman now admits. Still, he went out at a very fast clip, his hypercompetitive instincts kicking in. As he and Loeb approached Montauk, Loeb texted his friends, who rode out to meet them from the opposite direction. The etiquette would have been for Ackman and Loeb to slow down and greet the other riders, but Ackman just blew by at top speed. The others fell in behind, at first struggling to keep up with the alpha leader. But soon enough Ackman faltered—at Mile 32, Ackman recalls—and fell way behind the others. He was clearly “bonking,” as they say in the cycling world, which is what happens when a rider is dehydrated and his energy stores are depleted.

While everyone else rode back to Loeb’s East Hampton mansion, one of Loeb’s friends, David “Tiger” Williams, a respected cyclist and trader, painstakingly guided Ackman, who by then could barely pedal and was letting out primal screams of pain from the cramps in his legs, back to Bridgehampton. “I was in unbelievable pain,” Ackman recalls. As the other riders noted, it was really rather ridiculous for him to have gone out so fast, trying to lead the pack, considering his lack of training. Why not acknowledge your limits and set a pace you could maintain? As one rider notes, “I’ve never had an experience where someone has gone from being so aggressive on a bike to being so hopelessly unable to even turn the pedals…. His mind wrote a check that his body couldn’t cash.”

Nor was Ackman particularly gracious about the incident afterward, not bothering to answer e-mails of concern and support from others in the group until months later.

In a recent interview on CNBC, the blunt-talking and cagey Icahn hinted there would be a concerted effort to take Ackman down a peg or two in the Herbalife battle, which “could be the mother of all the short squeezes,” he said, referring to a technique that can be used by a group of traders who band together to try to clobber a short-seller.

Chapman agrees. “This is like Wall Street’s version of the movie Kill Bill,” he says. “Bill Ackman has been so arrogant and disrespectful to so many people, presumably on the theory that he would never be in a position where these subjects of his disrespect could actually act on their deserved hatred for him But now, with JCPenney [which is down 20 percent from Ackman’s 2010 investment] and Herbalife going against Ackman, his ‘stock’ has moved down, allowing once again, a decade later, for those holding their Kill Billputs [i.e., options they have been waiting to cash in] to exercise them against him.”

We continue our study of Herbalife’s saga with a recent post from www.brontecapital.com. There are lessons here on conducting research and on hubris.

What this story is really about

Herbalife is a company which combines a lot of good (think the life-saved diabetic above) with some pretty ugly features.

But this is not really a story about Herbalife – Herbalife will survive globally. Like all multi-level marketing schemes it will have its ups and downs. There will be all sorts of problems (such as tax compliance throughout the scheme, cash handling, perhaps even using Herbalife accounts to launder money).

What this has (deservedly) become is the story about how Bill Ackman can be so wrong. He spent (by his own admission) a year and a half analysing this company and his thesis can be falsified by visiting a few clubs in his home city. Bill Ackman’s thesis is the most easily falsified bear-thesis I have seen from a major hedge fund ever.

You have to wonder how this happened. So I am going to tell you:

Bill Ackman a Harvard educated (magna cum laude) billionaire New York hedge fund manager bet over a billion dollars on a short position (imperilling his fund and his reputation) without checking the facts.

And he did not check the facts because he was so rigid with a misplaced silver spoon that he could not stoop to sit on a subway for thirty minutes and talk with poor people for ninety minutes.

Market Review LMCM See Future Value (See page 5). Perhaps the market is discounting real growth vs. nominal growth? Don’t take that chart at face value.

Where is the Inflation (CPI) ? Another lesson in why price aggregates are so misleading.

Critics of the Austrian School of economics have been throwing barbs at Austrians like Robert Murphy because there is very little inflation in the economy. Of course, these critics are speaking about the mainstream concept of the price level as measured by the Consumer Price Index (i.e., CPI).

….

High prices seem to be the norm. The US stock and bond markets are at, or near, all-time highs. Agricultural land in the US is at all time highs. The Contemporary Art market in New York is booming with record sales and high prices. The real estate markets in Manhattan and Washington, DC, are both at all-time highs as the Austrians would predict. That is, after all, where the money is being created, and the place where much of it is injected into the economy.

This doesn’t even consider what prices would be like if the Fed and world central banks had not acted as they did. Housing prices would be lower, commodity prices would be lower, CPI and PPI would be running negative. Low-income families would have seen a surge in their standard of living. Savers would get a decent return on their savings.

Of course, the stock market and the bond market would also see significantly lower prices. Bank stocks would collapse and the bad banks would close. Finance, hedge funds, and investment banks would have collapsed. Manhattan real estate would be in the tank. The market for fund managers, hedge fund operators, and bankers would evaporate.

In other words, what the Fed chose to do ended up making the rich, richer and the poor, poorer. If they had not embarked on the most extreme and unorthodox monetary policy in memory, the poor would have experienced a relative rise in their standard of living and the rich would have experienced a collective decrease in their standard of living.

Based on its strong financial performance, Herbalife is a classic “compounder” – a well-managed company that sustains consistent top-line growth, has a leading market position, and steadily increases margins, earnings per share and free cash flow while demonstrating shareholder-friendly behavior. …Led by CEO Michael Johnson, management has also used the company’s ample free cash flow to de-lever its balance sheet and shrink the share count by nearly 25%. This type of steady non-cyclical growth is hard to find and puts Herbalife at the head of the compounders’ class.

With results like these, the case against Herbalife rests on a bold claim that the company is a fraud. The short seller’s lengthy argument against the Company can be boiled down to three principal smoking guns: the first, a claim that Herbalife has been operating an “illegal pyramid scheme” under the nose of the Federal Trade Commission for the past 32 years; the second, that Herbalife’s loyal customer and distributor base has been exploited and harmed despite the low number of consumer complaints and generous company return policies; and the third, a claim that Herbalife’s products are commodities sold at inflated prices not supported by sufficient levels of advertising or R&D.

Taken in reverse order, the third claim misses an essential truth that invalidates the indictment. No one believes Starbucks is a scam because you can buy a cheaper cup of coffee at your local bodega. A key contributor to Herbalife’s growth has been its distributor-led “Nutrition Clubs”, where consumers can purchase single servings of the Company’s signature beverages. The short seller’s assertion ignores the significant value customers place on every consumer brand and its community “experience” – whether at a Herbalife Nutrition Club, a Starbucks, or a corner bar. The markup is merited by community and brand identity, not by the commodity itself.

(Editor: in disclosure, I am long HLF but not as aggressively as Mr. Loeb. Is HLF a franchise because of its brand? But a brand has no meaning unless there is customer captivity. Does HLF have customer captivity?)

The second claim seems similarly dubious. The FTC, by all accounts, receives a very low volume of complaints annually about Herbalife – fewer than forty per year. ….The Company repurchases an average of only 1% of sales volume pursuant to this policy. It is difficult for us to understand why the buyback volume would be so low if there are in fact so many unsatisfied consumers and distributors who presumably would not hesitate to be reunited with their cash.

The pyramid scheme is a serious accusation that we have studied closely with our advisors. We do not believe it has merit. The short thesis rests on the notion that the FTC has been asleep at the switch, missed a massive fraud for over three decades, and will shortly awaken (at the behest of hedge fund short seller) to shut down the Company.

Applying a modest 10-12x earnings multiple suggests Herbalife’s shares are worth $55-$68, offering 40-70% upside from here and making the company a compelling long investment for Third Point.

Herbalife Battle: Great Theater, Terrible Trade By Jeff Macke

In the last 30 days shares of Herbalife (HLF) have gone from the mid-40’s to the 20’s and then back again. It’s a dizzying ride driven by bickering hedge fund managers taking turns in the spotlight to make their cases on the long and short sides. It’s a striking turn for an 11-year-old company with a market cap under $5 billion and, until very recently, almost no mindshare in the investment community.

For those considering getting involved with the stock on either side of the trade, the question is whether or not Herbalife is a “Ponzi Scheme,” as Bill Ackman alleges, or if it’s just another relatively boring company most investors should ignore. Value investor Vitaliy Katsenelson, chief investment officer at Investment Management Associates, says the company is probably best avoided.

“I think you just want to stay away from this fight,” Katsenelson says. He has been to Herbalife’s clubs and came away unimpressed. For one thing, most of the people were there, in his words, “just to sell the product to each other.” For another, the product itself seemed overpriced for what you’re getting. “Most people get into Herbalife not because they want to consume the product but because they want to sell it to their favorite mother-in-law.”

That makes HLF a lousy long, but is it a short? Not really. Katsenelson has done his homework. He’s been to HLF stores and he watched all three hours of Bill Ackman’s argument for shorting the company. After all that legwork Katsenelson just doesn’t see the appeal for either bullish or bearish investors.

Companies don’t just tumble to zero, they need to be pushed. Katsenelson thinks Ackman’s best chance in that regard is to create a self-fulfilling fundamental slide. If Ackman generates enough negative publicity it’s going to be harder for HLF to set up distribution centers. Failing that, the stock could muddle along with the company itself for years before hitting the wall.

“I would just basically stay away,” Katsenelson concludes. That’s probably good advice for the vast majority of individual investors.

Interview with a serial killer

To understand what drives hedge fund managers, I studied this video. Chilling but informative.

Hempton: Short-seller Went Long Herbalife Fri 04 Jan 13. The following transcript has not been checked for accuracy.

CNBC: Activist Robert Chatman battling Bill Ackman on Herbalife (see next article in this post). Herbalife’s Chairman says Ackman will lose his fight against Herbalife. But he have not the only one who thinks they will lose. Watching this battle, in his own words, says it is like watching hedge fund porn. Herb, thanks for joining us today.

Herb Greenberg: What makes him so interesting in this case is that he is mostly known as a short seller and he is buying the stock even though he agrees with Ackman. He joins us now live in our studios. John Hempton of www.bronte.com, “How are you.”

Hempton: I’m pretty well.

Greenberg: I got to ask a quick question here. yeah. You’re a short seller and you are — you are long this stock. How does that work? Why would you do that? I’m pretty familiar with scum bags. Multilevel marketing schemes are scum bags. There are a million people in their chain and Bill Ackman says Herbalife is ripping them off. Tobacco companies kill twice as many people a year as Herbalife has in its network. Those companies kill 400,000 people in America. Hugely profitable. They are scum bags but return cash to shareholders for decades. If you have shorted them, you’ve been run over.

Herbalife, five years ago, had about 140 million shares, it now has 108 million shares. It buys back stock regularly; pays a fairly hefty dividend. They are a scum bags, but they are a stock market scum bag.

Greenberg: You have to be careful with what you say here. The question is, will the Federal Trade Commission (“FTC”) go after the company? One reason you don’t believe that Ackman will be right is because you don’t believe the FTC will do that.

Hempton: You say something obviously is wrong and you think the government will rescue you. all Herbalife needs to do is find somebody who was fat and is less fat because of Herbalife and somewhere in the 2.5 million distributors there will be a few of those. Wheel them out in front of them (FTC regulators), and you are know, what Bill Ackman’s case now is that the government’s going to go and help the billionaire hedge fund manager.

Greenberg: I know another hedge fund manager here john, and he is very politically connected, very short the stock, and he believes that the heat will get turned up on this industry very quickly here. And he believes that one of the things they will be looking at is the industry itself targeting lower-income people. So what is to say that even though the FTC didn’t do this before, they don’t come back and do it now?

Hempton: I believe the same thing about the tobacco companies 20 years ago. the FTC has known about multilevel marketing schemes for decades. If this (Herbalife’s scam/cash flows) lasts three years, Ackman is wrong. If it lasts a decade, Ackman is so wrong, it’s just silly. Now this thing really has cash flow. A thesis that says, I got to wait for government is a bad thesis. I don’t know how many really dodgy companies I’ve reported to the FTC and what do they do? Sometimes they fine them. The vast bulk of the time they don’t.

CNBC: “Herb (Greenberg), I’m wondering where we go from here. I know we are looking forward to Herbalife’s rebuttal and Ackman is preparing his rebuttal to that rebuttal. What is the next chapter in the story?

Greenberg: Does this does become the equivalent of the for profit education industry where they go after it and where the industry, people said, they will never go after that industry. The government went after that and in this case you end up with a very hard reset of the business models of these companies.

Hempton: And for profit education industry case the victim is at least in part the government. the government giving stupid loans. a relatively easy way of the government reducing their fiscal drain.

Greenberg: John (Hempton), if in it case the victim is lower-income population, a lot of lower-income population and the Obama Administration could be very interested in that, wouldn’t that potentially have an impact?

Hempton: When did the government care about lower-income people in that way? Lower-income people are largely the victims of tobacco companies too. You look at tobacco, it is completely inversely correlated to wealth and income. Rich people don’t smoke. Poor people smoke. People in most jurisdictions just raise taxes from that.

Greenberg: Okay, we will see who is correct on this one. John, thank you very much for coming along.

Herbalife: Why I Made It a 35% Position after the Bill Ackman Bear Raid

This is a guest post prepared by Robert Chapman. Chapman is the founder of Chapman Capital LLC, which is a Los Angeles based investment company specializing in takeovers and turnarounds. In 2000, Chapman Capital was an activist versus Herbalife following the death of Herbalife’s founder Mark Hughes. This is an amazing article. It’s well-researched and easy to understand. If you’re remotely curious about the future of Herbalife after Ackman’s attack, the mechanics of short selling and the potential value of Herbalife’s stock, this is a MUST read. If you find this article informative, hit the +1 or Like buttons above. Sincerely, +Kevin Thompson

…REGUATORY SUMMARY: FTC has been there, done that.

The Ackman Tell. Many poker games are won and lost upon that infamous turning point when a player properly reads his opponent’s “tell.” To wit, I am confident that during an interview with CNBC’s Andrew Ross Sorkin on “D-Day” (12/20/2012), Bill Ackman slipped his “tell”, confirming my suspicion that he already realized the FTC wasn’t going to make his day by shutting down HLF. I strongly recommend all HLF traders/investors read the transcript of this interview, as Sorkin does a masterful job of fighting the media urge to genuflect before Ackman’s drawn down zipper, otherwise known as “The Whitney Tilson”.

Interview with Michael Mauboussin: Untangling Skill and Luck in Business, Sports, and Investing (From www.simoleonsense.com)

Today we’re going to talk about the role of skill and luck in generating success.

Michael Mauboussin’s Background

Michael Mauboussin, is the Chief Investment Strategist at Legg Mason Capital Management. Michael is also an adjunct at Columbia Business School and Chairman of the Board of Trustees at The Santa Fe Institute.

Book Synopsis

What role, exactly, do skill and luck play in our successes and failures? Some games, like roulette and the lottery, are pure luck. Others, like chess, exist at the other end of the spectrum, relying almost wholly on players’ skill. In his provocative new book, Michael Mauboussin untangles the intricate strands of skill and luck, defines them, and provides useful frameworks for analyzing their relative contributions. He offers concrete suggestions for how to put these insights to work to your advantage in business and other dimensions of life.

CSinvesting Editor: Just remember that those that know, don’t tell; and those that don’t know, have the floor to themselves. Some might call Mr. Mauboussin, “an entertainer.”

…..So Ackman vs. Herbalife has no heroes. Both parties, in their own way, take advantage of the goodwill and trust that underlie capitalism. Herbalife recruits sales people with the knowledge–based on mathematical certainty but undisclosed to its recruits–that the vast majority will lose money. Mr. Ackman, for his part, has gotten rich betting against bad companies. One party is possibly immoral, the other party at best amoral. Who do you cheer for? –Mr. Karlgaard, publisher of Forbes (A Short Seller Takes on a Vitamin Vendor, WSJ Jan 4, 2013)

Yes this battle will be gruesome, bloody and long (perhaps) but our purpose is to understand whether Herbalife which–as of the last filing–sported franchise-like financials of high ROA, ROE and ROIC with growing sales. Copious cash flow. On the surface, the company seems to have a franchise. Why can’t other companies do the same thing. What barriers to entry are there? Product patents, customer captivity, economies of scale and scope, network effects, etc. This battle will allow us to understand what drove Herbalife’s success. Will it be fleeting or lasting. My bet is that Herbalife does NOT have a lasting competitive advantage.

The quote above by Mr. Karlgaard is disappointing because as a publisher of a business magazine, he should understand Mr. Ackman’s purpose. A good investor should invest in companies that will use owner’s capital wisely and should not invest or even warn against investing in companies that mis-allocate capital for the long-term. Short sellers are just as important as having a Warren Buffett in the market. An Ackman does more for future growth than any government program because–like him or not–Mr. Ackman is trying to take capital away from poorly managed, potential frauds, unsustainable businesses while allocating capital to companies that will use his investors’ capital beneficially. He may be proven wrong but that is for the market to decide.

UPDATE: MONEY SUPPLY EXPLOSION--We are now officially in double digit territory for non-seasonally adjusted 13 week annualized money supply (M2) growth. Here is the amazing ascent in growth over recent weeks: 5.1%, 5.6%, 6.6%, 7.1%, 7.5%, 7.8%, 8.2%, 8.4%, 8.7%, 9.0%, 9.3%, 9.6%, 9.9%, 10.7%. It is this growth that is going to fuel the U.S. economy, the U.S. stock market and commodities. www.economicpolicyjournal.com

Investing in Banks

I find investing in global banks like Bank of America or Citibank impossible because I have no way to value or understand their businesses. How much “shadow” banking do these entities engage in? I don’t want to find out the hard way. See the article below

Some four years after the 2008 financial crisis, public trust in banks is as low as ever. Sophisticated investors describe big banks as “black boxes” that may still be concealing enormous risks—the sort that could again take down the economy. A close investigation of a supposedly conservative bank’s financial records uncovers the reason for these fears—and points the way toward urgent reforms.

The financial crisis had many causes—too much borrowing, foolish investments, misguided regulation—but at its core, the panic resulted from a lack of transparency. The reason no one wanted to lend to or trade with the banks during the fall of 2008, when Lehman Brothers collapsed, was that no one could understand the banks’ risks. It was impossible to tell, from looking at a particular bank’s disclosures, whether it might suddenly implode. Red the whole article:

The authors of the above article don’t grasp the true cause of the banking panic. Yes, transparency is a problem, but that would ALWAYS be true under our current fractional reserve banking system–it’s inherently a Ponzi scheme that functions on public gullibility and government edict–banks get to violate private property rights.

PS: can anyone fill in the blanks? All panics arise from excess _______ over and above ___________. Correct answer wins this prize:

This was published on January 2, 2013, in Ron Paul’s Monetary Policy Anthology: Materials From the Chairmanship of the Subcommittee on Domestic Monetary Policy and Technology, US House of Representatives, 112th Congress. All the books mentioned in this article are free on the web, go to www.mises.org and do a book search by title.

The scholarly contributions of Murray N. Rothbard span numerous disciplines, and may be found in dozens of books and thousands of articles. But even if we confine ourselves to the topic of money, the subject of this volume, we still find his contributions copious and significant.

As an American monetary historian Rothbard traced the party politics, the pressure groups, and the academic apologists behind the various national banking schemes throughout American history. As a popularizer of monetary theory and history he showed the public what government was really up to as it took greater and greater control over money. As a business cycle expert he wrote scholarly books on the Panic of 1819 and the Great Depression, finding the roots of both in artificial credit expansion. And while the locus classicus of monetary theory in the tradition of the Austrian School is Ludwig von Mises’ 1912 work The Theory of Money and Credit, the most thorough shorter overview of Austrian monetary theory is surely chapter 10 of Rothbard’s treatise Man, Economy and State.

Rothbard placed great emphasis on the central monetary insight of classical economics, namely that the quantity of money is unimportant to economic progress. There is no need for the money supply to be artificially expanded in order to keep pace with population, economic growth, or any other factor. As long as prices are free to fluctuate, changes in the purchasing power of money can accommodate increases in production, increases in money demand, changes in population, or whatever. If production increases, for example, prices simply fall, and the same amount of money can now facilitate an increased number of transactions commensurate with the greater abundance of goods. Any attempt by “monetary policy” to keep prices from falling, to accommodate an increase in the demand for money, or to establish “price stability,” will yield only instability, entrepreneurial confusion, and the boom-bust cycle. There is no way for central bank policy or any form of artificial credit expansion to improve upon the micro-level adjustments that take place at every moment in the market.

With the exception of the Austrian School of economics, to which Rothbard made so many important contributions throughout his career, professional economists have treated money as a good that must be produced by a monopoly – either the government itself or its authorized central bank. Rothbard, on the other hand, teaches that money is a commodity (albeit one with unique attributes) that can be produced without government involvement. Rothbard’s history of money, in fact, is a history of small steps, the importance of which are often appreciated only in hindsight, by which government insinuated its way into the business of money production.

It was Carl Menger who demonstrated how money could emerge on the free market, and Ludwig von Mises who demonstrated that it had to emerge that way. In this as in so many other areas, Mises broke with the reigning orthodoxy, which in this case held that money was a creation of the state and held its value because of the state’s seal of approval. A corollary of the Austrian view was that fiat paper money could not simply be created ex nihilo by the state and imposed on the public. The fiat paper we use today would have to come about in some other way.

It was one of Rothbard’s great contributions to show, in his classic What Has Government Done to Our Money? and elsewhere, the precise steps by which the fiat money in use throughout the world came into existence. First, a commodity money (for convenience, let’s suppose gold) comes into existence on the market, without central direction, simply because people recognize that the use of a highly valued good as a medium of exchange, as opposed to persisting in barter, will make it easier for them to facilitate their transactions. Second, money substitutes began to be issued, and circulate instead of the gold itself. This satisfies the desires of many people for convenience. They would rather carry paper, redeemable into gold, than the gold itself. Finally, government calls in the gold that backs the paper, keeps the gold, and leaves the people with paper money redeemable into nothing. These steps, in turn, were preceded by the seemingly minor – but in retrospect portentous indeed – government interventions of monopolizing the mint, establishing national names for the money in a particular country (dollars, francs, etc.), and imposing legal tender laws.

Rothbard also brought the Austrian theory of the business cycle to a popular audience. Joseph Salerno, who has been called the best monetary economist working in the Austrian tradition today, was first drawn to the Austrian School by Rothbard’s essay “Economic Depressions: Their Cause and Cure.” There Rothbard laid out the problems that business cycle theory needed to solve. In particular, any theory of the cycle needed to account, first, for why entrepreneurs should make similar errors in a cluster, when these entrepreneurs have been chosen by the market for their skill at forecasting consumer demand. If these are the entrepreneurs who have done the best job of anticipating consumer demand in the past, why should they suddenly do such a poor job, and all at once? And why should these errors be especially clustered in the capital-goods sectors of the economy?

According to Rothbard, competing theories could not answer either of these questions satisfactorily. Certainly any theory that tried to blame the bust on a sudden fall in consumer spending could not explain why consumer-goods industries, as an empirical fact, tended to perform relatively better than capital-goods industries.

Only the Austrian theory of the business cycle adequately accounted for the phenomena we observe during the boom and bust. The cause of the entrepreneurial confusion, according to the Austrians, is the white noise the Federal Reserve introduces into the system by its manipulation of interest rates, which it accomplishes by injecting newly created money into the banking system. The artificially low rates mislead entrepreneurs into a different pattern of production than would have occurred otherwise. This structure of production is not what the free market and its price system would have led entrepreneurs to erect, and it would be sustainable only if the public were willing to defer consumption and provide investment capital to a greater degree than they actually are. With the passage of time this mismatch between consumer wants and the existing structure of production becomes evident, massive losses are suffered, and the process of reallocating resources into a sustainable pattern in the service of consumer demand commences. This latter process is the bust, which is actually the beginning of the economy’s restoration to health.

The concentration of losses in the capital-goods sector can be explained by the same factor: the artificially low-interest rates brought about by the Fed’s intervention into the economy. What Austrians call the higher-order stages of production, the stages farthest removed from finished consumer goods, are more interest-rate sensitive, and will therefore be given disproportionate stimulus by the Fed’s policy of lowering interest rates.

Equipped with this theory, Rothbard wrote America’s Great Depression(1963). There Rothbard did two things. First, he showed that the Great Depression had not been the fault of “unregulated capitalism.” After explaining the Austrian theory of the business cycle and showing why it was superior to rival accounts, Rothbard went on to apply it to the most devastating event in U.S. economic history. In the first part of his exposition, Rothbard focused on showing the extent of the inflation during the 1920s, pointing out that the relatively flat consumer price level was misleading: given the explosion in productivity during the roaring ’20s, prices should have been falling. He also pointed out how bloated the capital-goods sector became vis-a-vis consumer goods production. In other words, the ingredients and characteristics of the Austrian business cycle theory were very much present in the years leading up to the Depression.

Second, Rothbard showed that the persistence of the Depression was attributable to government policy. Herbert Hoover, far from a supporter of laissez-faire, had sought to prop up wages during a business depression, spent huge sums on public works, bailed out banks and railroads, increased the government’s role in agriculture, impaired the international division of labor via the Smoot-Hawley Tariff, attacked short sellers, and raised taxes, to mention just a portion of the Hoover program.

Rothbard had been interested in business cycles since his days as a graduate student. He had intended to work on a history of American business cycles for his Ph.D. dissertation under Joseph Dorfman at Columbia University, but he found out that the first major cycle in American history, the Panic of 1819, provided ample material for study in itself. That dissertation eventually appeared as a book, via Columbia University Press, called The Panic of 1819: Reactions and Policies (1962). In that book, which the scholarly journals have declared to be the definitive study, Rothbard found that a great many contemporaries identified the Bank of the United States – which was supposed to be a source of stability – as the primary culprit in that period of boom and bust. American statesmen who had once favored such banks, and who thought paper money inflation could be a source of economic progress, converted to hard money on the spot, and proposals for 100-percent specie banking proliferated.

In A History of Money and Banking: The Colonial Era to World War II, a collection of Rothbard’s historical writings published after the author’s death, Rothbard traced the history of money in the United States and came up with some unconventional findings. The most stable period of the nineteenth century from a monetary standpoint turns out to be the period of the Independent Treasury, the time when the banking system was burdened with the least government involvement. What’s more, the various economic cycles of the nineteenth century were consistently tied to artificial credit expansion, either participated in or connived at by government and its privileged banks. Rothbard further showed that the traditional tale of the 1870s, when the United States was supposed to have been in the middle of the “Long Depression,” was all wrong. This was actually a period of great prosperity, Rothbard said. Years later, economic historians have since concluded that Rothbard’s position had been the correct one.

Rothbard’s treatment of the Federal Reserve System itself, which he dealt with in numerous other works, involved the same kind of analysis that historians like Gabriel Kolko and Robert Wiebe applied to other fruits of the Progressive Era. The conventional wisdom, as conveyed in the textbooks, is that the Progressives were enlightened intellectuals who sought to employ the federal regulatory apparatus in the service of the public good. The wicked, grasping private sector was to be brought to heel at last by these advocates of social justice.

New Left revisionists demonstrated that this version of the Progressive Era was nothing but a caricature. The dominant theme in Progressive thought was expert control over various aspects of society and the economy. The Progressives were not populists. They placed their confidence in a technocratic elite administering federal agencies removed from regular public oversight. What’s more, the resulting regulatory apparatus tended to favor the dominant firms in the market, which is why the forces of big business were in sympathy with, rather than irreconcilably opposed to, the Progressive program. “With such powerful interests as the Morgans, the Rockefellers, and Kuhn, Loeb in basic agreement on a new central bank,” Rothbard wrote, “who could prevail against it?”

It is with these insights in mind that Rothbard scrutinized the Federal Reserve. He would have none of the idea that the Fed was the creation of far-seeing public officials who sought to subject the banking system to wise regulation for the sake of the people’s well-being. The Fed was created not to punish the banking system, but to make its fractional-reserve lending operate more smoothly. In The Case Against the Fed, What Has Government Done to Our Money?, and The Mystery of Banking, Rothbard took the reader through the step-by-step process by which the banks engaged in credit expansion, earning a return by lending money created out of thin air. Without a central bank to coordinate this process, Rothbard showed, the banks’ position was precarious. If one bank inflated more than others, those others would seek to redeem those notes for specie and the issuing bank would be unable to honor all the redemption claims coming in.

The primary purpose of the central bank, therefore, in addition to propping up the banks through its various liquidity injections and its position as the lender of last resort, is to coordinate the inflationary process. When faced with the creation of new money by the Fed, the banks will inflate on top of this new money at the same rate (as determined by the Fed’s reserve requirement for banks). Therefore, the various redemptions will tend, on net, to cancel each other out. This is what Rothbard meant when he said the central bank made it possible to “inflate the currency in a smooth, controlled, and uniform manner throughout the nation.”

Although Rothbard distinguished himself as a monetary theorist and as a monetary historian, he did not confine himself to theory or history. He devoted plenty of attention to the here and now – to critiques of Federal Reserve policy, for example, or to criticisms of government responses to the various fiascoes, the Savings and Loan bailout among them, to which our financial system is especially prone. He likewise looked beyond the present system to a regime of sound money, and in The Case for a 100 Percent Gold Dollar and The Mystery of Banking laid out a practical, step-by-step plan to get there from here.

In his work on monetary theory and history, as in his work in so many other areas, Rothbard showed from both an economic and a moral point of view why a system of liberty was preferable to a system of government control. At a time when the political class and the banking establishment are being subjected to more scrutiny than ever, the message of Rothbard takes on a special urgency.

For that reason we should all be grateful that his monetary work, and that of the other great Austrian economists, is being carried on by Murray Rothbard’s friend and colleague Ron Paul. By my reckoning, no one in history has brought true monetary theory and history to a larger audience.