http://www.nyssa.org/authorseries/ctl/viewdetail/mid/4196/itemid/2691/d/20160822.aspx

YSSA’s Value Investing Thought Leadership Group presents

NYSSA Author Series™:

|

Monday August 22, 2016 6:00 PM through 8:00 PM

NYSSA Conference Center

Available as: Live Session

Categories: Market Integrity, NYSSA Author Series™, Programs for Members, Seminar, Value Investing

| Program Details |

| Date Monday, August 22, 2016 Time Format: Location Fees Chair CFA Institute CEs |

From 1975-2001: ROI for T-Bills was 6.6%, S&P 500 14.1% with a 15% std. dev., Bulk Shipping 7.2 with a 40% std. dev., and Tanker Shipping 4.9% with a 70.4% std. dev! (Source: Maritime Economics, 3rd Edition)

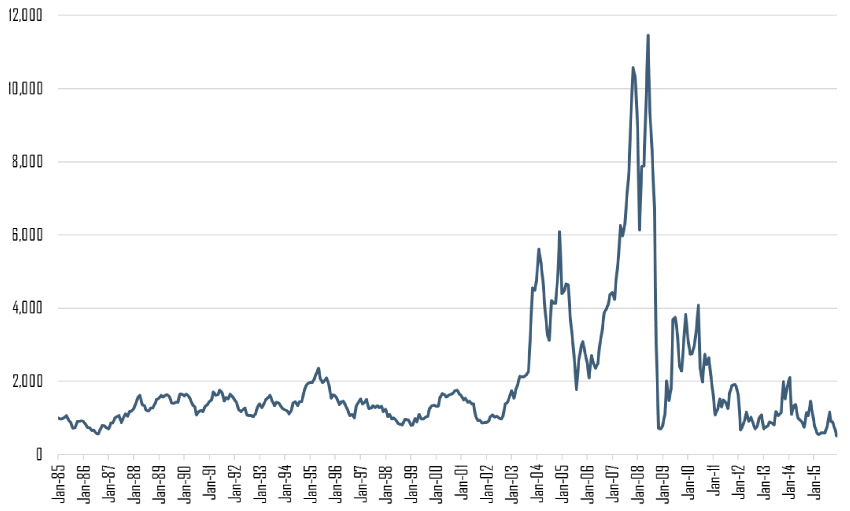

Who in their right mind would invest in the shipping business? Well, if you can buy low, then fortunes can be made. Recently, the Baltic Dry Index (BDI) hit a thirty-year low of 291, BDI Index and note the long-term chart below. Always look at MANY years of past data. The boom of 2007/08 will probably not be seen again for many years.

See a deep contrarian investor discuss the dry bulk shippers (March 2016):Deep Value Inv./Operator Discusses Dry Bulk Mkt.

“Dry bulk is a screaming buy; one of the best entry points in the cycle in the last thirty years. But be prepared to sustain a prolonged period of poor freight market conditions and have plenty of cash reserves and low leverage. In other words, you have to have a longer-term perspective than most investors–three to five years at least.

Isaac sowed seeds into the land during a drought. –Leon Patitasas

“That’s the funny thing about ships. They are actually more attractive to buy at 20xs EBITDA, or even negative cash flow, than they are at 4xs EBITDA,” Coco said.

“So you are telling me that investors should seek out money losing shipping deals?” she asked incredulously.

“Correct. And sell the ones that are making lots of money. Itis like that little Napoleon said….”Buy on the sound of cannons and sell on the soundsof trumpets.” (Source: The Shipping Man by Matthew McCleery).

—

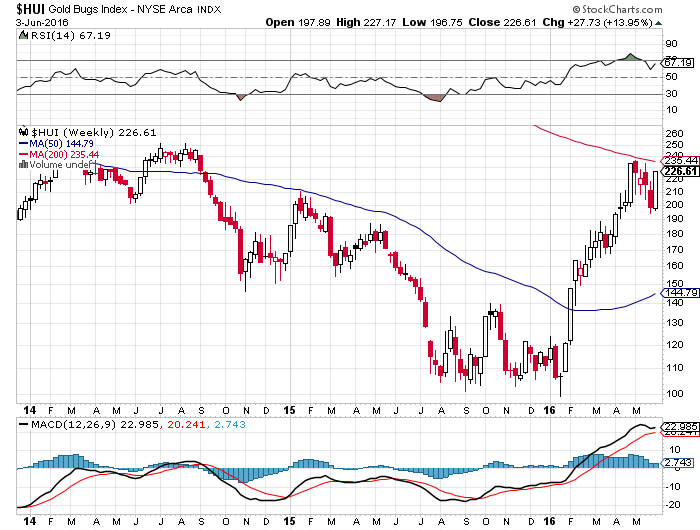

John Chew: Here is where I wonder if this post helps readers’ understanding of investing because is this investing or speculating? Note as much as what Warren Buffett does NOT do. He doesn’t invest in mining or shipping stocks. He has already had poor results with the airline industry. So why even mention an industry in massive distress with historically sub par returns and huge volatility? I would prefer businesses with great reinvestment opportunities or great capital allocators at the helm like Markel (MKL), but a horrific business going from a distress price to a bad price may give much better returns depending upon the price paid. Also, the worst bear market in freight rates in the past 30 years for dry bulkers means unusual opportunity just as the worst bear market in gold miners in the past 100 years offered bargains galore.

Readers know that I ventured into the miners in mid-to-late 2013, subsequently suffering back-to-back declines of about 25% before seeing the portfolio rally about 100%. So I still do not have a great return (12% after three years), but I bought miners with a five-year-to-seven year outlook and I am only three years into the investment. With Junior miners you can expect to see a 50% decline before they rally five to 10 times (assuming you chose the ones that survive! –Rick Rule). In a land of negative-to-low interest rates, I have to look further for bargains.

Readers can pipe in what they would like to learn in future posts–let me know.

Five years of declines in gold mining stocks and then…..

Are you investing or speculating by dry-bulk shipping stocks? These are stub stocks where the equity is a small fraction of the enterprise values due to the shrunken market cap and the large debt taken on to finance ship purchases. But if you buy a few well-managed and relatively well-financed shipping companies that can survive the trough of the cycle–two to four more years?– you can tolerate a few going to zero if the ones remaining multiply many-fold. Not for the weak-kneed. Scorpio Bulkers (SALT) has ALREADY diluted shareholders and has taken drastic action to survive. Note management buying shares at $3.00 Scorpio Bulkers Inc. Announces Financial Results for the First Quarter of 2016. An ugly past, but we invest for the future in terms of mean reversion. I have not yet invested in any shipping stocks!

Here is what I love about the shipping business. 10 ships and 11 cargoes, then a BOOM. 11 ships and 10 cargoes, then a BUST. You are also on the SAME footing as the most experienced ship owners in the world. NO ONE knows when the cycle will turn. This is like a poker game where the investor that has the ships when others have thrown in the towel takes a lot of the marbles. The worse the freight rates and the outlook, the better IF you can carry the costs until the cycle turns, and it WILL turn due to the laws of supply and demand.

I view this as intelligent speculation. I allocate five tranches of investment into five shipping companies. Say $5 units each. One unit goes to zero (ouch!), the next to $2 (Boo!), the next to $1 (Damn!), the next to $3 and the next to $50 (Homerun!) and it takes three years. There is a 31% compouned return. Though I have no idea if this is realistic because I must study the shipping industry thoroughly. I am just formulating a possible strategy IF I find the right companies at the right prices. But I am drawn to the shipping companies because some companies are trading below depressed net asset values. As Mr. Templeton suggests, look where the outlook is most dire.

The best source to learn about shipping is Maritime Economics. And a must read:

Meanwhile keep reading………………..

RISK Management Video – Be prepared for the unexpected.

Posted in Humor & Entertainment, Investor Psychology, Search Strategies, YOU

Tagged croc, Deep Value, search, shipping, the Shipping Man

“Value investors are born not made.” Richard Oldfield

I am an investor similar to Walter Schloss and Peter Cundhill.

Your main job as a net/net buyer is to elminate the possibility of bankruptcy.–Peter Cundill

During that time he was also a partner in the company called the Vanan Financial Management Ltd. which in 1975 took over the All-Canadian Venture Fund. In 1977, Cundill established his very own Vancouver-based firm named Peter Cundill & Associates Ltd. and renamed the All-Canadian Venture Fund to Cundill Value, when the fund became the flagship of his newly established firm. Peter Cundill & Associates, now named Mackenzie Cundill Value Series A after a strategic partnership of PCA with Mackenzie Financial Corporation, best epitomizes the bottom-up value investment outlook of Peter Cundill.

The Cundill Value Fund was launched in December 1974 and immediately lost money during 1975. However, after this dismal start, the star fund manager recovered quickly and reported few losing years after 1975.

From 1974 through to 1988 the fund returned 22% per annum. Over its 35 year history to 2010, the Cundill Value Fund achieved a CAGR of 13.7%, which is especially impressive when you consider the fact that the market was still recovering from the financial crisis when this figure was calculated.

Peter Cundill was awarded the Analysts’ Choice Career Achievement Award for the best mutual fund manager of all time in 2001. At the award ceremony which recognized his 35 plus years of contribution and expertise as a fund manager and value investor, he was referred to as the ‘Indiana Jones of the Canadian Money Managers’, a title which was acknowledged by Cundill with great pleasure. Cundill’s expertise even gained recognition from Warren Buffet, who claimed Peter Cundill had the traits of a good successor and possessed the kind of credentials required that would be suitable for Berkshire Hathaway’s next chief investment officer.

Observing the multi-dimensional personality of Peter Cundill, it is evident that he enjoyed life to the fullest. By no means did he limit himself from challenges or new experiences. He had an innate child-like curiosity and explored various aspects of his interests. His love for travelling turned him to one of the best global investors, and his rapacious reading habit lead him to the writings of the great Benjamin Graham. Cundill also enjoyed and challenged himself with various sports such as handball, rugby, skiing and hiking; being a dedicated marathon runner, at the age of over 40 he was capable of completing 22 marathon races including ‘Sub 3 hour’ (running the marathon under three hours).

His contribution was not limited to the financial world, but to the world of academia and literacy. Being a philanthropist, in 2008, he founded the Cundill Prize at McGill University to recognize the non-fiction publication for authors who have a great impact on literary, social and academic fields.

Despite of his recent death on 23rd January 2011 due to a rare neurological disease, the legacy and investment philosophy of Peter Cundill is kept alive by the firm he founded in 1975 and the numerous contributions made by him in the world of finance and academia.

Like many value investors, Cundill’s style of investing can trace its roots back to Benjamin Graham; Cundill liked to buy $1 for $0.40. What’s more, Cundill liked to buy stocks that were generally ignored and rejected by the general public, giving his approach a contrarian style.

Unlike Graham, who brought as many companies as he could, as long as each company met his strict criteria, Peter Cundill only considered companies with strong balance sheets and an upcoming catalyst that could unlock value for investors. It’s often the case that deep-value investments languish for years before acatalyst unlocks value. By investing only when a catalyst was upcoming, Cundill increased his risk of success. Peter usually scrutinized each company’s balance sheet to discover off balance sheet financing and assess the company’s true debt load.

A Hermit has no peer pressure–Robin Wright

A Hermit has no peer pressure–Robin Wright

Thanks

Thanks for all the comments. A student from Germany kindly offered to host a discussion board for anybody who wants to analyze investment ideas, cases and/or investment subjects in more detail. The infamous Dr. K has also offered to moderate the board. If he upsets too many people, I will referee. As long as differing views are respected then we will be fine.

My overall goals for this course are to study deep value investing while encouraging independent and skeptical thinking. We will try to read original sources and apply principles to our own situations.

I don’t “like” deep value investing or mechanical investing but I was curious why investing in business disasters is so profitable (Preface in Deep Value). I also find it odd at first glance that Ben Graham the father of detailed security analysis gravitated to rule-based (my substitute for “mechanical”) investing. Joel Greenblatt who was the master of special situation, heavily concentrated investing also moved towards the “magic formula” style of investing. Another great investor I know used to visit companies and be highly concentrated into 8 or so businesses. Now he buys a diversified group of STABLE franchises when they go on sale. He also has a rules-based valuation method. What is going on?

Also, as more time passes, you realize that our human flaws are tough to overcome. Toby in Deep Value mentions that experts often DEGRADE mechanical systems. In other words, human tendencies hurt investment performance. Perhaps “mechanical” investing is worth exploring further without preconceived notions.

I often feel investing is like this situation:

Killing a child is wrong. Those soldiers acted, but then the unexpected happened. What now? Morally you know what is right but can you face the consequences?

It isn’t hard to find cheap companies in this pile (but many worth $0), but there is every reason not to act. Can you endure the ridicule?

Gold mining is a tough business–when wasn’t it a bad business? Managements are bad (true, but note how US tech firms are buying back stocks near their all-time highs—their managements are no better than the miners yet their stock prices are stratospheric), and on and on.

Altucher writes of Buffett’s early career. Even in the 1990’s Buffett was buying net/nets and companies in Korea trading at 2 to 3xs earnings.

So I chose Deep Value as a guide/textbook to pursue these topics with this group.

The direction of the course will be easy to follow:

We will go chapter-by-chapter in DEEP VALUE by Toby Carlisle while reading the footnotes and original sources as best we can. Let’s understand terms in the book like enterprise value and EBITDA, for example, before moving on to the next chapter.

We just finished Chapter 3, Warren Buffett: Liquidator to Operator where we had the case study of See’s Candies. Buffett moved from investing in deeply discounted tangible assets like Dempster Mills to a franchise like See’s Candies. Buffett was willing to pay a premium over book value because the assets of the business generated returns far in excess of its cost of capital. See’s takes commodities like sugar, milk and chocolate and turns them into boxed chocolates that customers are happy to pay a premium for. Why? The company has a brand built through the customer’s experiences with the product. As a deep value guy, I gave a second-hand box of chocolates to my EX. I said, “Here, ignore the half-eaten chocolates, the rest look OK. I got this on a 95% off sale!” Tense!

So what can WE learn from the case that we can apply in our investments? So rather than try to be like Buffett let’s take his principles and find applications which we can apply going forward. Why is See’s a great business? Taking commodities and turning them into a product that consumers pay a premium for seems like a business to buy. Note that Bicardi was the best business in Cuba and still is going strong. Bicardi takes sugar and water and turns it into premium Rum. I see similarities—brand name built upon quality and good distribution within its geographical boundaries. See’s is strong in southern California, for example. Perhaps, Sherwin-Williams is a bit like See’s Candies. People are willing to pay a premium for paint because 98% of the cost of a painting job is the labor while you want the job to last and look good. Good distribution coupled with service (color tinting/application advice) is also critical. I could go on but the point is to take the general concepts and apply them in your own way. Don’t be Buffett, but be yourself in applying Buffett’s lessons.

Chapter 4: The Acquirer’s Multiple: Fair Companies at Wonderful Prices in Deep Value

is the next assignment. As a supplement: Placing EBITDA into Perspective

Time-out: How to Think and How to read a book Worth reviewing.

As a supplement to Chapter 2, Contrarians at the Gate in DEEP VALUE, please read the highlighted paragraphs on liquidation value in Seth Klarman’s chapter on Valuation (Chapter 8 in Margin of Safety and emailed to the Deep Value Group at Google).

You will understand

Therefore, a value investor passes on what he or she can’t understand or uses CONSERVATIVE assumptions to build-in a margin of safety.

Take your time and read the above chapter carefully, especially his case study on Esco Electronics. He makes a compelling case. The difference between price and intrinsic value (determined several ways) is ASTOUNDING. A great investment should slap you in the face–it should be obvious, but then you might say what am I missing? You can’t believe the opportunity.

To reveal one of the secrets of this course (shh..) by the time we have journeyed through the readings, examples, videos, and cases, you will realize that if you are buying assets like net/nets, then you must buy them VERY cheaply to allow REVERSION to the MEAN to work.

Or if you go the Munger/Buffett (in his later years) route and buy franchises with moats around them (the companies have high returns on invested capital and they either grow profitability or return excess cash to shareholders) those companies are RARELY on sale. The franchise moat (barrier to entry) slows the reversion to the mean process while high profitability allows for compounding of capital–an investor’s nirvana.

Great investments are FEW and FAR BETWEEN unless markets are in a huge dislocation. Keep waiting and waiting until the money is just lying there for you to safely pick it up. In other words wait for:

Can any pretty women taking this course teach the others:

Certainly we need to do better than this:

I will be posting a lesson index shortly. We will tackle Chapter 1, The Paradox of Dumb Money, of Quantitative Value next before we move back to Chapter 3 in Deep Value and read Buffett’s Partnership letters (to be posted).

Below are supplementary readings and original sources for Chapter 2, Contrarians at the Gate, in Deep Value. This is an important chapter because we are introduced to the father of security analysis. He was the first person to systematize his analysis and separate the price of a security from its intrinsic value.

I realize that some may find Graham fusty and his prose turgid/boring, but Graham was a Renaissance man who had a razor-sharp intellect and integrity. You can’t lose by reading his works. Note his attitude, skepticism, and logic.

So far in the course I am surprised by the ironies and subtleties of Deep Value investing–picked up in the preface of the book, Deep Value. Our Deep Value Group has close to 400 members, yet, currently (Jan. 17, 2015), the number of net/nets in the US market is negligible. Financial assets (with a few exceptions) are sky-high in valuation due to Central Bank intervention, negative interest rates, and a six-year upward trend in US bonds and stocks. I am surprised at the interest.

We invest today for the future, but the future is unknowable. Look at the predictive record of experts! Investors tend to extrapolate the past into the future just in time for a reversal of fortune–reversion to the mean reverses the trend.

Deep value investing takes advantages of the cognitive biases of others to gain profits, but if we are human too then how do we avoid the same? Cheapness or the discount from intrinsic value is the main determinant of margin of safety. The cheaper you buy the less risk and MORE reward. This smashes academic finance theory in the face.

Here I am quite surprised that the highest returns to the net/net strategy go to the MONEY-LOSING companies. The worst of the ugly gain the most. Perhaps because price drops the most due to fear and earnings trend extrapolation. Like assuming the driver of the car will continue to motor off the cliff instead of turning or stopping the car.

A TEST: Let’s say a company earned $5 per share and it is growing at 5% per year, the cost of capital is 10%, and it is trading at $85 per share. Then the next year earnings drop to $1 per share and the following year earnings drop to $0.05 or five cents, the next year earnings go up to $3 and in the fifth year back to $5.25 and 5% growth. After ten years the company will continue to grow but only at 3%. Guess the price drop quickly and write it down. Now do the DCF and see where the intrinsic value is compared to your guess.

Last year $5.00

Year 1 $5.25

Year 2: $1.00

Year 3: $0.05

Year 4: $3.00

Year 5: $5.25

Year 6: $5.51 (5% growth)

…. next year, next year, etc.

After year 10, then terminal value 10% cost of capital with 3% perpetual growth. Can a financial wizard post in the comments section? Was anyone surprised by your initial reaction the Intrinsic value result vs. their initial thoughts on how price would react?

—

Back to the post….

The higher probability (Montier, 5%) for each INDIVIDUAL company to go down 90% or more vs. 2% of non net/nets may cause other investors to shy away from investing. HOWEVER, the GROUP of net/nets STILL outperforms. You have certain companies go to zero and some rebound multiple times but you don’t know which ones. You have to deal with much uncertainty but believe you are playing the odds like an insurance company.

When net/nets are abundant like in 1932, the world appears to be ending. Investor fear is off the charts. The question is whether you will have the capital to buy and the courage to act. Again we come round and round to temperament or character or whatever you want to call acting in the face massive fear.

But knowing that a company is too cheap when it trades at less than 2/3rds to net asset value (Asset value is tenuous, liabilities are 100 cents on the dollar) does not seem difficult, but probably the surrounding circumstances for the company and/or market are ugly! “Don’t you read the papers!” an outsider might say if he or she learned of your purchase.

Remember 2009? Jim Cramer in a panic. http://youtu.be/rOVXh4xM-Ww?t=1m35s (just paste into your browser)

Those are my thoughts and questions so far as I keep reading.

Graham’s Writings and Testimony

Graham Testimony to Congress (note his remarks on the MYSTERY of price eventually closing the gap with intrinsic value)

Important writings on Liquidation Values during the 1930s

1932_American Corporations Worth More Dead than Alive 3 Parts by B Grahams (Please read). You can’t understand the depths of despair in the financial markets (and thus the net/nets and prices below liquidation values) without understanding the preceding boom.

Historical perspective

A Study of Market History through Graham Babson Buffett and Others The 1920s BOOM.

A Great Depression_Rothbard Obviously, you don’t have time to read this, but IF you do want to understand the causes of the biggest bear market in US history then this is the definitive work. The book destroys the common wisdom that the depression was caused by the Fed’s tight monetary policy.

The Outperformance of Net/Nets

97001708-Case-for-Quantitative-Value-Eyquem-Global-Strategy-20120613

Benjamin-Graham-s-Net-Nets-Seventy-Five-Years-Old-and-Outperforming I imagine that some net/nets are micro/nano-cap stocks under 50 million in market cap and with wide (5% to 10% bid/offer spreads) perhaps the studies do not deduct the spread?

There is a lot here so I will refrain from posting until the middle of the week. Take your time with Chapter 2. I will be posting next on Klarman’s thoughts on liquidation and valuation.

Traditional finance savaged: The Dumbest Ideas in Finance_Montier

How NOT to take this course

You don’t have to read EVERYTHING, but you do have a choice. Better to understand what you read.

How is it possible that an issue with the splendid records of Tonopah Mining should sell at less than the company’s cash assets alone? Three explanations of this strange situation may be given. The company’s rich mines at Tonopah are known to be virtually exhausted. At the same time the strenuous efforts of the Exploration Department to develop new properties have met with but indifferent success. Finally, the drop in the price of silver last year has provided another bearish argument. It is this combination of unfavorable factors which has carried the price down from $7 1/8 in 1917 to its present low of $1 3/8 in 1923.

Granting that the operating outlook is uncertain, one must still marvel at the triumph of pessimism which refused to value the issue at even the amount of its cash and marketable investments; particularly since there is every reason to believe that the company’s holdings in the Tonopah and Goldfield railroad, are themselves intrinsically worth the present selling price. (Ben Graham on Investing)

VIDEOS

Marty Whitman criticizes Graham and Net Nets (3 minutes Must see!)

Marty Whitman: They Just Don’t Get it. (23 minutes) Marty says many analysts on Wall Street do not understand credit analysis. We will explore later in this course whether the quality of credit provides a better assessment of the true cost of capital for a firm rather than “beta.”

One investor’s experience investing in Net/Nets (3 minutes)

Net/nets as value traps (5 minutes)

Good advice on behavioral investing (3.5 minutes)

Prof. Greenwald on UGLY and Cheap or Graham’s Search Strategy (8 minutes)

Greenwald on the Balance Sheet (risk of financials) (10 minutes)

Posted in Free Courses, History, Investing Careers, Investor Psychology, Risk Management, Search Strategies

Tagged Deep Value, Graham, Greenwald, NEt Nets, Search Strategy

My Idea:

This is an experiment to see if a group of serious students of value investing can learn from each other and an in-depth reading of the course materials to become better investors. If you send me your email to aldridge56@aol.com (DEEP VALUE COURSE) in the title, I will send you the course materials (Thanks to a reader for contributing!). There is a catch however. You are expected to do the readings and comment/participate in the discussion in the comments section. So don’t seek unless committed to being an active participant. Since there will be supplementary readings for each chapter of the book (see chapter titles below), we will take one to two weeks per chapter. You may have homework or be asked to research investment questions further. I won’t think any less of you if you decide to pass–this course is only for fanatics. Course will start a week or two into the New Year.

Description of the book below (also type in DEEP VALUE) in the search box of this box and view some of the videos on deep value and the author, Toby Carlisle. Also, go to www.greenbackd.com and look at the past ten posts.

Book blurb from Wiley:

Deep Value: Why Activist Investors and Other Contrarians Battle for Control of Losing Corporations is a must-read exploration of deep value investment strategy, describing the evolution of the theories of valuation and shareholder activism from Graham to Icahn and beyond. The book combines engaging anecdotes with industry research to illustrate the principles and methods of this complex strategy, and explains the reasoning behind seemingly incomprehensible activist maneuvers. Written by an active value investor, Deep Value provides an insider’s perspective on shareholder activist strategies in a format accessible to both professional investors and laypeople.

The Deep Value investment philosophy as described by Graham initially identified targets by their discount to liquidation value. This approach was extremely effective, but those opportunities are few and far between in the modern market, forcing activists to adapt. Current activists assess value from a much broader palate, and exploit a much wider range of tools to achieve their goals. Deep Value enumerates and expands upon the resources and strategies available to value investors today, and describes how the economic climate is allowing value investing to re-emerge. Topics include:

Table of Contents

Chapter 1 The Icahn Manifesto 1

Chapter 2 Contrarians at the Gate 19

Chapter 3 Warren Buffett: Liquidator to Operator 35

Chapter 4 The Acquirer’s Multiple 53

Chapter 5 A Clockwork Market 77

Chapter 6 Trading in Glamour: The Conglomerate Era 99

Chapter 7 Catch a Falling Knife 119

Chapter 8 The Art of the Corporate Raid 151

Chapter 9 How Hannibal Profits From His Victories 169

Chapter 10 Applied Deep Value 187

Posted in Free Courses, Search Strategies, Special Situations, Valuation Techniques

Tagged Course, Deep Value, value investing