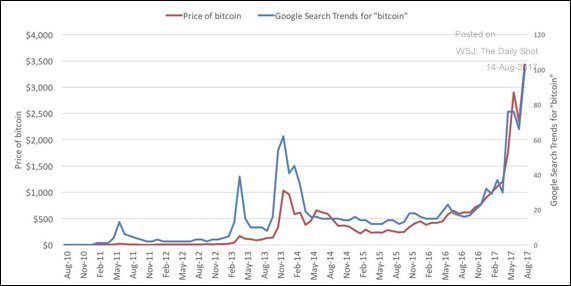

Bitcoin is not only irredeemable, but also unbacked. That is a big difference—in favor of the dollar. (Keith Weiner of Monetary-Metals)

Read an analysis of Bitcoin as money (Bitcoin has no backing. I think of Bitcoin as “Token” money. What are your thoughts?

Also, the developer of Bitcoin provides his understanding of the theory of money. As a review read: On the Origins of Money_5 Menger

![]()

For those who are interested and are in NYC:

Blockchain Technology Versus Fiat Currency

The next CMRE event will be held on October 3 at the University Club in New York City: Blockchain Technology Versus Fiat Currency. Speakers will include noted author George Gilder, co-founder of Etherium Joe Lupin, thought-leader Saifedean Ammous, and more.

Topics will range from an introduction of blockchain technology, economic implications, the politics surrounding private currencies, and the role of gold. Full program to come.

Check back on www.cmre.org for more information and to purchase tickets.

TIMING THE CRASH: Performance_Update_2017_07

QUIZ: What has caused or one of the MAIN reasons that companies like Amazon keep gaining strength? Hint: What Bezos does is meaningless.

4 responses to “Bitcoin and the Theory of Money; Hedge Fund Quiz”