The popularity of inflation and credit expansion, the ultimate source of the repeated attempts to render people prosperous by credit expansion, and thus the cause of the cyclical fluctuations of business, manifests itself clearly in the customary terminology. The boom is called good business, prosperity, and upswing. Its unavoidable aftermath, the readjustment of conditions to the real data of the market, is called crisis, slump, bad business, depression. People rebel against the insight that the disturbing element is to be seen in the malinvestment and the overconsumption of the boom period and that such an artificially induced boom is doomed. (Ludwig von Mises, Human Action: A Treatise on Economics, 1966)

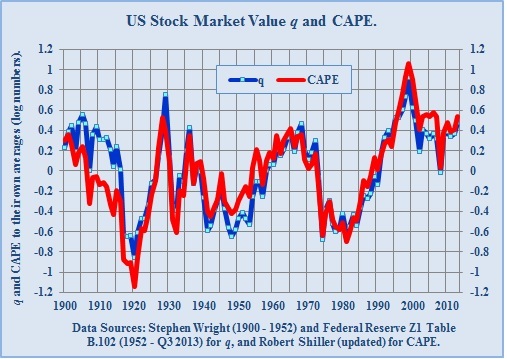

What is q?

q is the ratio between the value of companies according to the stock market and their net worth measured at replacement cost.

It can be defined to include or exclude corporate debt. When debt is included, we refer to the ratio as Tobin’s q, as it was in this form that Nobel Laureate James Tobin introduced the concept. For stock market purposes, however, it is easier to exclude debt and we refer to it in this form as “equity q”.

The data from which q is calculated are published in the “Flow of Funds Accounts of the United States Z1”, which is published quarterly by the Federal Reserve. This data source is available from 1952 onwards. Earlier data are available from a variety of sources from 1900. (For an academic article on the data and sources see Stephen Wright’s “Measures of Stock Market Value and returns to the US Non-financial Corporate Sector 1900-2002.”)

How Does q Differ from Price to Book?

q is the ratio of price to net worth at replacement cost rather than the historic or book cost of companies. It therefore allows for the impact of inflation. In addition, balance sheet figures use reported earnings figures to derive book value, whereas the Fed’s net worth figures are consistent with the (more rigorous) national income measures of profits.

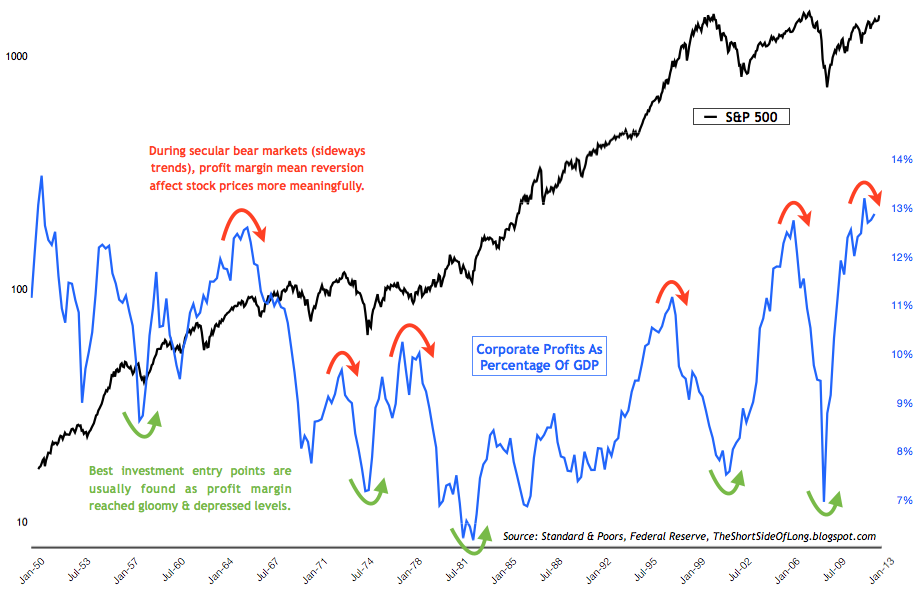

Mr. Smithers says that currently (December 2013) the market is overvalued by approximately 60%. Though profit margins are not GUARANTEED to revert, margins have always done so in the past. So why are so many American companies buying their stock near all-time highs or after five years of rising stock prices? First, they are not investing as much for the future so secondly, they are buying back stock to “return” cash to shareholders. The key is incentives. Management’s are incentivized with stock so the lower the number of shares in the denominator, the faster their earnings per share growth–the better for their compensation. So if businesses are not investing as much while buying in shares what do YOU think will be FUTURE profit margins. Because if profit margins dip then for certain operationally leveraged businesses the cash flow drop will be huge–equity prices will follow. Who knows when this process reverses–because if people could time the inflection point, the distortion would not be as large.

You might listen to the above interview with Andrew Smithers to learn more. Also, explore his homepage: http://www.smithers.co.uk/index.php

Finally, corporations have been borrowing at low interest rates to buy back stocks. The market and this game can continue as long as interest rates do not rise significantly. Buffett mentioned that equity secular bull market require declines in (real) interest rates–see:Buffett_on_1999_Stock_Market_-_Fortune_Article & 2008 Market Call

See the chart of the three hundred year chart of long-term interest rates: TTMYGH_06_Jan_2014

5 responses to “Tobin’s Q: The Market is 60% Overvalued”