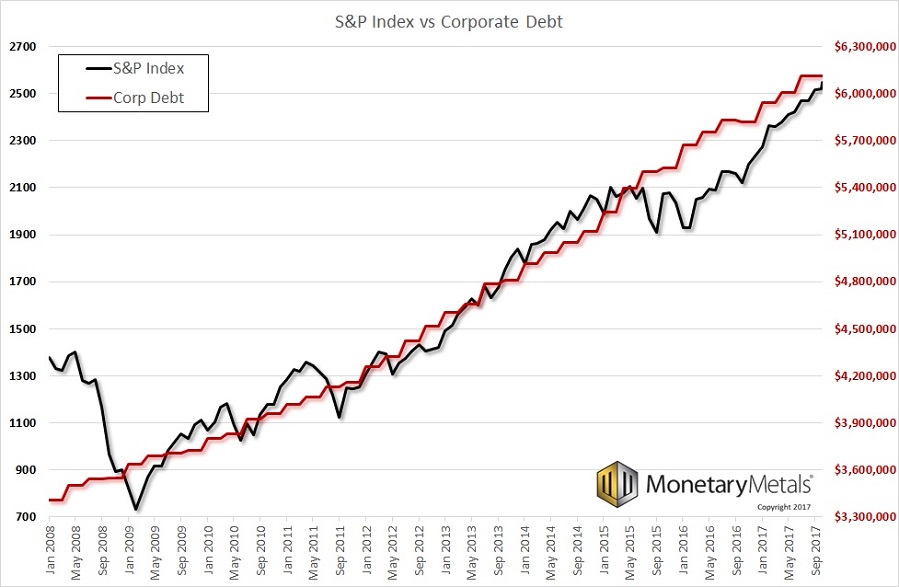

Increasing debt for equity swap

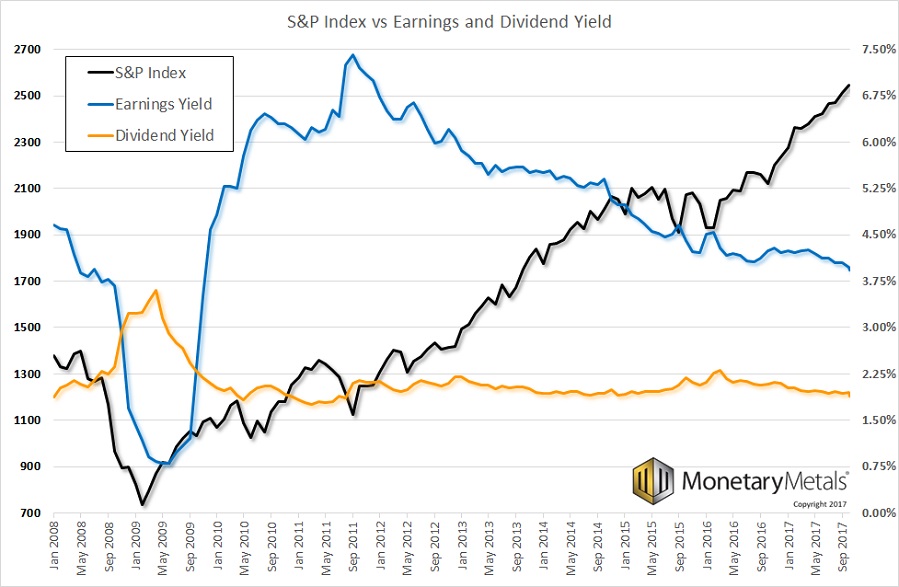

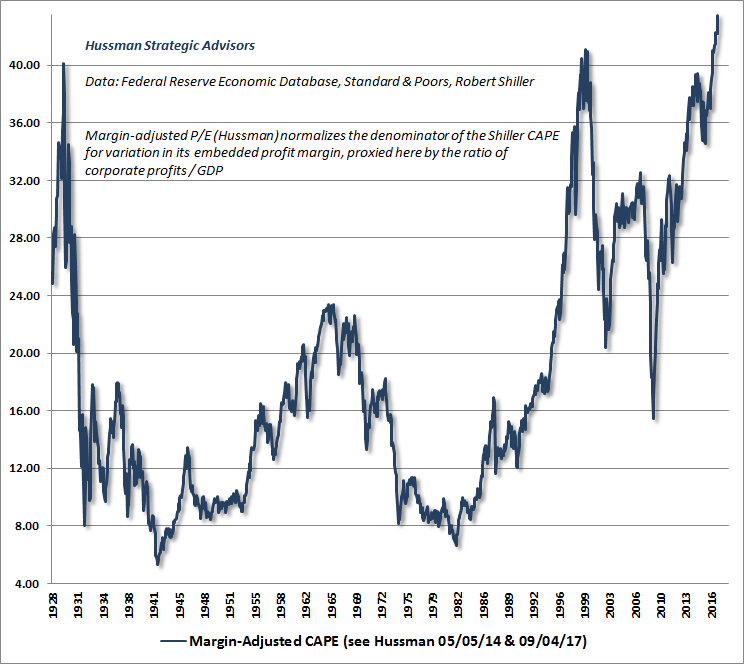

Sentiment bullish and prices high relative to the past.

Pingback: This Week's Best Investing Reads | Stock Screener - The Acquirer's Multiple®

Your email address will not be published. Required fields are marked *

Comment

Name *

Email *

Website

This site uses Akismet to reduce spam. Learn how your comment data is processed.

Pingback: This Week's Best Investing Reads | Stock Screener - The Acquirer's Multiple®