The above post is an excellent tutorial and case study on riding a volatile, cyclical bull market in Uranium Company, Cameco (and others) from 2000 when CCJ traded about $7 to $8 until mid-2007 or about $40 to $45 (you never get the exact high). That is about a 27% compounded return over seven years. Buying near the low and selling near the high–isn’t that a fantasy. Not if you were following the fundamentals and the sentiment. The hardest part is holding on until it is clearly time to sell.

The article was written by https://www.uraniuminsider.com/ who did a great job on this article. I don’t know him or his newsletter, but I collated his articles in a case study below. I highly recommend you study the case below even if you avoid investing in cyclical, commodity companies.

The case also gives you a condensed application of the capital cycle.

Mr. Kaplan is the perfect investor to study to improve your investing in deeply cyclical resource investments and to understand gold. As Mr. Kaplan explains in an interview (2017): “Gold is not someone’s liability…. Economically, we are in unchartered waters.”

His philosophy is to start with a macro theme (A long-term bull market in gold) and then locate the best asset (Novagold) to leverage that theme. He considers gold the best risk reward of any asset class. Setting aside that gold is the best asset to own during financial crises, gold will be facing a severe supply crunch since no new large deposits over 5 million ounces are being discovered much less developed. Development from discovery to production requires over 20 years.

In addition, more and more foreign jurisdictions like the Philippines or Papua New Guinea are becoming too risky to mine. Mr. Kaplan estimates the equilibrium price to incentivize new discoveries is probably $3,000 to $5,000 per ounce. I think that is too low of a price.

The patience and conviction to be successful in this type of investing are extraordinarily high. Most professional investors cannot even pretend to be as patient. Mr. Kaplan became involved in Novagold during the crisis of 2009–imagine the fear and financial stress swirling amongst investors then.

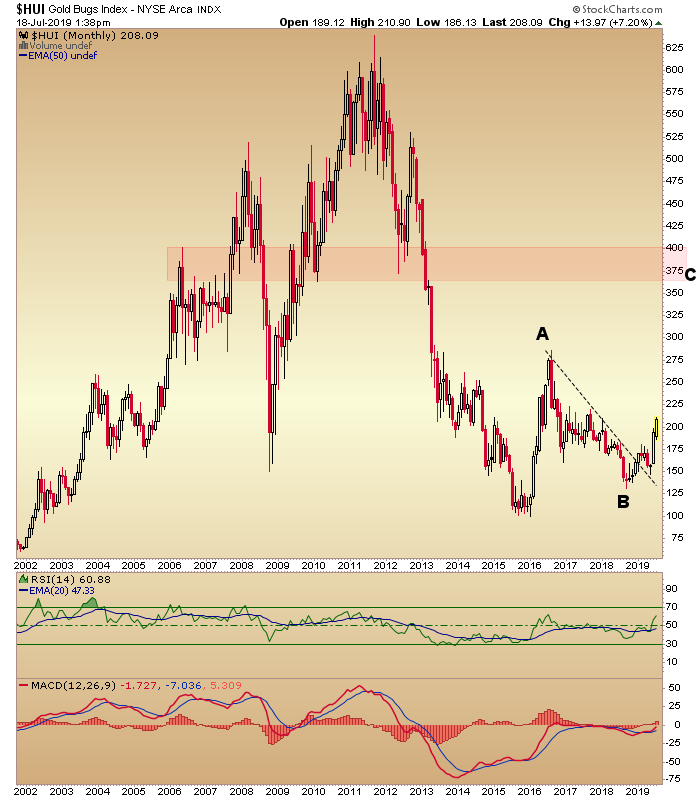

Recognizing the obvious: Intrinsic value rising well before price

From 2009 to 2019 the intrinsic value was rising as Novagold became de-risked. The decade ticked by as Novagold obtained all the required permits, it strengthened relationships with native communities, it spun off non-core assets like Galore (copper) to Trilogy, Novagold treasury increased its cash balance to $250 million with an annual cash burn of less than $10 million, and NG’s relationship with Barrick strengthened. Few cared or paid attention. Meanwhile, many jurisdictions have become even higher risk like the Philippines, Papua New Guinea, etc.

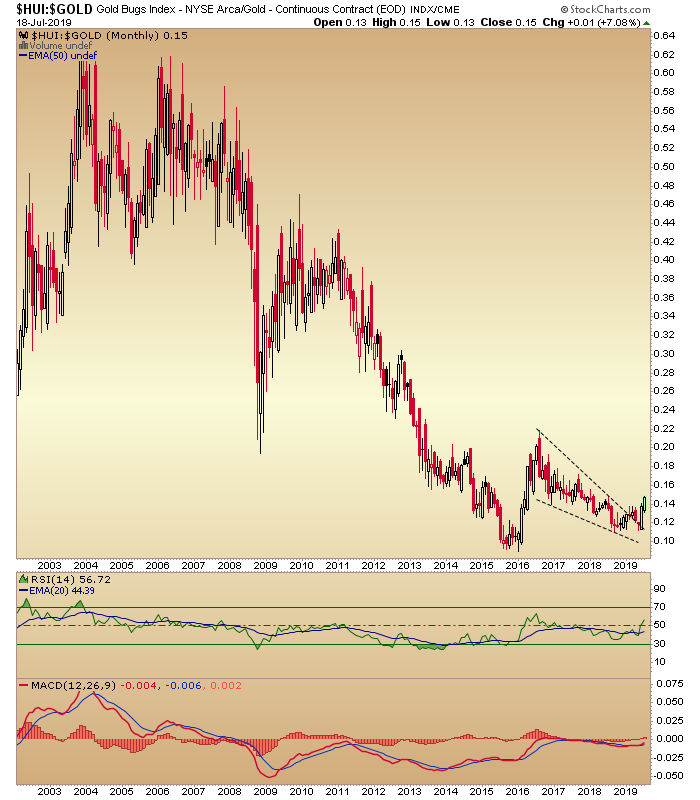

Price goes sideways while intrinsic value rises quietly. These are the best situations to hold onto. You just need VAST patience and to pay attention. Value accretion was occurring away from the financial statements. You would see expenses each quarter, but you would need to be aware of the permits won and the relationships strengthened. No algorithm or computer screening model will do that for you. But NG just traded as part of an index until decoupling in mid-2019. Everything related to Novagold was increasing except the share price until one day……. Meanwhile, Mr. Kaplan held fast because of his knowledge and conviction.

NG trades with the indexes, GDX and GDXJ, then decouples upward as price catches up with intrinsic value.

As a word of caution, this post is not a recommendation to buy Novagold even though I have been a shareholder since 2015. You should understand that Mr. Kaplan has been an investor for over 11 years through declines of 85% in NG’s share price. As an investor you might check on the statements and claims made in the annual reports listed below. If Novagold’s grade is considered outstanding, then look at the annual reports of five major miners and verify/check whether that fact checks out. Take nothing on faith so you can learn conviction.

How would you be willing to hold a investment without a huge payoff for over a decade while waiting for the market to turn to your analysis?

If you study those letters and annual reports, you will have a course in patient investing in a deeply cyclical industry and in understanding gold.

UPDATE 5/1/2020: 2008 Annual Report marks the entry of Electrum during the Great Financial Crisis.

2012 Annual Report began the time when management change had begun in earnest with CEO Greg Lang arriving from Barrick Gold as well as divesting of assets to focus on Donlin Gold. Those actions made the company into a perpetual option on the value of gold.

The Tortoise and The Hare Chairman’s Letter of 2015 explains why Thomas Kaplan was (and remains) bullish towards gold.

Please note how consistent Mr. Kaplan’s and Novagold’s message has been over the past twelve years. The Donlin project attributes remain consistent even while the resource base increases.

Remember that Novagold (NG) as a perpetual option is highly leveraged to the price of gold and to sentiment so expect prices swings of 25% to 50% or more. Such is the requirement to being a long-term investor. My secret is not to look at the share price but once a quarter.

A forgotten sector comes to lifeMiners decline relative to gold as investors give up on poor capital allocation by managers who paid high prices at the top of the last cycle 2007/2011. But that has changed as the sector has been starved of capital for years. Go where they ain’t.A forgotten miner in an opaque market (Uranium). Eventually, the market MUST turn. An investor has to have a very (five years at least) timeframe for this market.

—

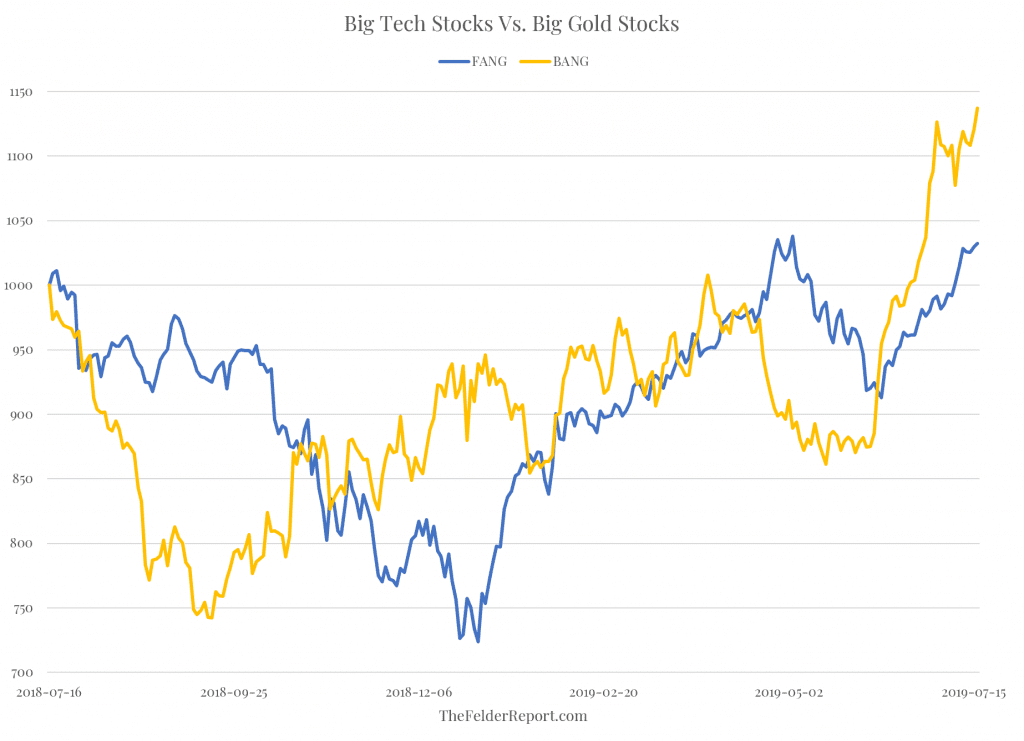

BANG stocks (Barrick, Agnico, Newmont and Goldcore vs. the FANG stocks–meaningless in the short-term but of interest to watch.

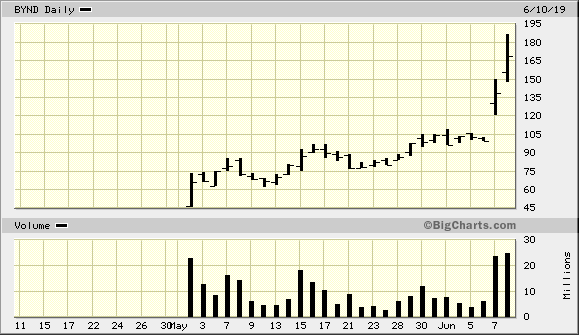

It’s the short squeeze of a vegan’s paradise. Shares of Beyond Meat (NASDAQ:BYND) jumped another 21% yesterday on an earnings beat, or really a loss beat, the company losing only $6.6 million on total net revenues of just over $40 million. The company now has a market cap of over $9 billion, and short borrowing costs keep rising. 51% of the company’s float is still being held short, which means the short squeeze can continue if the positions can’t be maintained, which would be especially relevant if the broader market starts to fall while Beyond keeps rising. There is about $800 million left in short positions on the stock. The short side is down about $400 million since January, while the stock is up about 650% since its IPO at $25.

—

Daniel Lacalle@dlacalle_IAQE is disinflationary because it perpetuates overcapacity and unproductive debt, yet it is massively inflationary on risky assets because the objective is to make rising government spending cheap. Hypernflation created in financial assets as sovereign bonds artificially inflated

Because intelligence is absolutely no barrier to cult recruitment. This is because a person’s intelligence is totally bypassed during the process of cult recruitment. When reality testing is suspended then one’s intelligence is not applied at all in order to ascertain the reasonableness of the cult’s teachings.

Do you want to transcend your consciousness and be blissfully happy forever? https://www.tm.org/

Or

Don’t Fall Down The Rabbit Hole

An ex-TM teacher peels back the union and reveals the dark side of the TM and the TM organization. The Maharishi was a sociopath in his eyes. A very thorough discussion of cult mind techniques from an insider of Transcendental Meditation:Skeptical TM

What does questioning the benefits of TM have to do with investing? Be skeptical. Attack your favorite ideas. Never stop questioning and learning. Note that several TM instructors quit when they saw paid scientists doctoring studies to benefit the TM.org.

There are benefits to meditation and, yes, transcendental meditation–if done in a limited fashion for relaxation–can induce a state of deep relaxation. The problem is the hype and supposed need to learn from a teacher or “guru.” ONLY an expert knows your proper mantra. PLEASE…….

The simple Relaxation Response helps me be better focused. I avoid having a “monkey-mind.” My suggestion is to learn for free (Don’t pay $1000’s for TM training) by viewing the video below and give yourself a few weeks. Keep a journal of your progress. If you see no benefit then stop. I take fifteen minutes in the morning and 15 minutes in the afternoon. No, your problems won’t evaporate nor will you transcend humanity and see God, but you may be more relaxed, less irritable, calmer, more focused, and, strangely, more compassionate.

Here is an early interview of Eliz. Holmes: Could this finger prick blood test be the next “Game-Changer? Imagine if this company can change the cost and inconvenience of diagnostic care? Wow!

Why study this case of Theranos?

Whenever you study an investment, you should make notes on your thoughts at the time to go back and check your thinking and biases. How else can you improve as an analyst?

Now, unless you have been living in a cave, you know what happened. However, pretend that you didn’t know the outcome and you were reading the articles above for the first time and seeing the video. What RED FLAGS jump out at you. Or what would you need to prove in order to invest? And if you could not find the answer easily to the main question of the investment, what else would you scrutinize carefully? Think hard before reading on………..

I highly recommend the above book as a great read. You will also learn about investor manipulation, the will to believe and how it shuts off our critical thinking abilities, incompetent governance, employee abuse, EXTREMELY bad management, criminal actions, and a female sociopath. I could not put the book down–read it in a day.

—

Next, a few years later, when Theranos, a private company with an estimated $9 billion value (!), faced a barrage of critics over the lack of transparency and no verification of the technology (“The Edison”), Cramer gives her a chance to rebut her critics.

Cramer asks Holmes about her Technology. What do you think of the answers? If you were an investor, what would be the first area to investigate?) Did Cramer ever follow-up specifically? No.

By the way, did you notice her deep (affected?) voice and her black uniform. Creepy.

As a former employee said Theranos product was like building a bus while driving down the highway with passengers. The problem is that people could get killed. This fraud hit home since I have amyloidosis. Not only did she and her accomplices hurt employees, investors, and–most importantly–PATIENTS! She and her CEO deserve a minimum 25-year sentence.

Note how SOCIAL PROOF euthanized investors critical thinking. Look at the prestigious board: George Schultz, General , etc. But note the lack of specific product/industry expertise to vet Holmes’ claims. She brilliantly piggybacked on the prestige of others. Any investor could have visited the Walgreen stores to check on the accuracy and completeness of the tests. Red flags would fly.

The employee turnover and secretiveness would have been other flags. What relevant experience to this field did she have? I am not knocking outsiders, but she and her CEO lacked any background in biochemistry. That isn’t enough to suspect problems, but it would place more urgency on verifying the efficacy of the technology.

A very interesting presentation of how Barrick is planning its future.

—

CORRECTION

I have often mention gold as a “Store of Value.” I never defined my terms.

I apologize. A better explanation by Keith Weiner of www.monetary-metals.com

Store of Value Fallacy

And this leads us to make one final, if tangential point. We often hear people talk about gold as a “store of value”. If you have a tank, that is a store of water. A grain silo is a store of wheat. In both cases, what is being stored is a quantity of a commodity. In this sense, a vault is a store of gold.

However, economic value—as we see above—is whatever the bidder is willing to pay. Gold’s moneyness does not come from it commanding the same amount of wheat today as it did last year or 2000 years ago. In fact, its purchasing power of wheat is not fixed. Over the last ten years, pricedingold.com shows that wheat has ranged from about 0.9 grams gold per bushel to 3.6g. The highest price during this time is 4X the lowest.

One reason for gold’s moneyness is that we value the next ounce of gold—the marginal ounce—the same as the last one. Proof of this extraordinary claim is observed in the extraordinary fact that virtually all gold ever mined in 5,000 years of human history is still in human hands. Gold is not produced to be consumed, but to be held. And we keep on producing, regardless of how much has already been produced.

In other words, we measure the value of gold like we measure the value of all other things in the economy—in gold. Gold does not have constant purchasing power (perhaps we should use scare quotes “purchasing power”). It has a constant price. The price of gold is always 1. This is not expressing a tautology. It is expressing that gold has constant marginal utility.

Gold is the steel meter stick of measuring economic values. Even if we climb in elevation (quantity) the meter (ounce) does not shrink.

On April 11, 2018, the price of gold in US Dollars was $1,370. This morning on July 19th, the price was $1,2110.90 for a decline of $159 in 99 days. If current trends continue, then in 712 days or less than two years, the Gold price in USD terms will be about $0.00. The trend is your friend!

The single greatest mistake investors make is to extrapolate recent history out into the future. They take the financial returns of the past 5 days or 5 years or even 50 years and assume the next few days or years will look just the same without any consideration for the historical context or conditions that provided for those returns.

They forget that, while ‘history may rhyme, it doesn’t repeat itself’ (Twain). Or that, “the only thing that is constant is change” (Heraclitus). These two famous quotes apply to the financial markets as much as anything.

Ignoring these truths and instead simply extrapolating is why investors are suckered into pouring money into the stock market only after a run of great performance. They believe that the recent gains are about to repeat to their great benefit when they should be thinking about what conditions allowed for those gains to take place and analyzing whether they are still relevant or not.

This is also why they are suckered into selling only after a painful decline as they did at the lows made during the financial crisis. They believe that they are about to suffer another 50% decline on top of the one they just endured when they should really be reminding themselves that change is the only guarantee in life.

I believe this is one of the biggest problems with so-called “passive” investing. It is built upon the faulty premise that it is ‘impossible to forecast’ the future returns of any asset class over any period of time so we should just own all of them all the time. My response to this is that while ‘ignorance may be bliss’ it’s not a valid investment strategy.

In his 1992 letter to Berkshire Hathaway shareholders, Warren Buffett wrote:

We’ve long felt that the only value of stock forecasters is to make fortune tellers look good. Even now, Charlie and I continue to believe that short-term market forecasts are poison and should be kept locked up in a safe place, away from children and also from grown-ups who behave in the market like children. However, it is clear that stocks cannot forever overperform their underlying businesses, as they have so dramatically done for some time, and that fact makes us quite confident of our forecast that the rewards from investing in stocks over the next decade will be significantly smaller than they were in the last.

Much can be learned from this short passage. First, short-term stock market forecasts are, indeed, nearly worthless – essentially a guessing game. Second, long-term forecasts, on the other hand, can be made with ‘confidence.’ “How?” you ask.

It’s actually very simple. Rather than fixate on recent history and extrapolate it into the future you must abandon this natural tendency. And as I said earlier you also need to analyze the conditions that allowed for those returns to see whether they are still relevant to today’s market.

In Buffett’s example he’s referring to the wonderful returns equity investors experienced from 1982-1992. During that span investors roughly quadrupled their money. Over the coming decade they merely doubled their money so Buffett was right that the decade beginning in 1993 would fall far short of the return of the prior decade even if they were still very good.

sc-22

But Buffett made another prescient forecast in November 1999 when he wrote:

Today, staring fixedly back at the road they just traveled, most investors have rosy expectations. A Paine Webber and Gallup Organization survey released in July shows that the least experienced investors–those who have invested for less than five years–expect annual returns over the next ten years of 22.6%. Even those who have invested for more than 20 years are expecting 12.9%. Now, I’d like to argue that we can’t come even remotely close to that 12.9%… you need to remember that future returns are always affected by current valuations and give some thought to what you’re getting for your money in the stock market right now.

You probably already know that stock market returns from 1999 to 2009 were not very kind to investors.

And Buffett tells us how he was so confident that this would be the case. He examined the conditions that allowed for returns to be so wonderful from 1982-1999 but were no longer present in 1999: wonderful valuations. Stocks were so cheap in 1982 that the coming decade was virtually guaranteed to be better than the decade that preceded it. (1972-1982 was another decade that was not fun for investors.) Then in 1999 valuations were so expensive that there was almost no possibility of decent returns going forward.

So let’s take a look at Buffett’s favorite valuation yardstick which he refers to on both of those prior writings. It tracks the total value of the stock market in relation to Gross National Product.

From the chart, it’s plain to see that valuations were extremely attractive back in the early 1980’s. This is why stocks performed so well over the next 20 years. However, I find it absolutely fascinating that stock market valuations today are essentially equivalent to valuations in November 1999 when he wrote that latter passage. Yeah, go back and read that last line again. It’s a doozy and it’s absolutely fact.

This is also why the past 5 years or even the past 50 years are totally irrelevant to equity investors in today’s market. There is almost zero possibility today of achieving a return anywhere close to what those historical returns represent. So shun forecasts if you want. Plead ignorance if it makes you feel blissful. But at today’s valuations you should at least be aware of the fact that it’s exceedingly dangerous to fall into the trap of extrapolating without analyzing.

What The Buy-And-Hold Cult Doesn’t Want You To Know

Buy-and-hold, and all of its related strategies like BTFD, garnered a cult following a long time ago and it’s only gotten even more popular in recent years. (There may be no better evidence of this than the StockTwits merch store – which I love, btw). And after one of the longest and strongest equity bull markets in history this should not come as any surprise. Investors are always influenced by recency bias and prone to extrapolation.

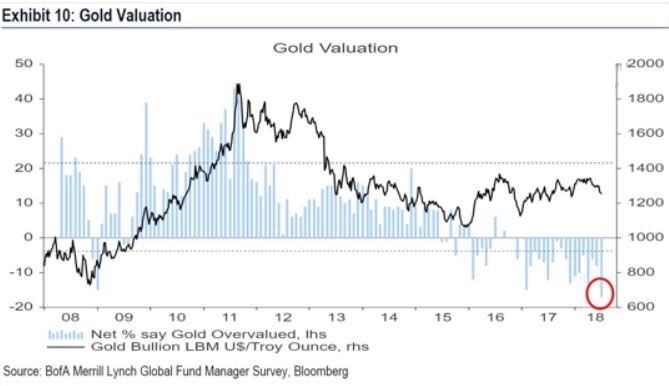

What is surprising, however, is that, despite that fact that it’s long-term (20-year) performance still crushes that of the broad stock market, gold has become so maligned among investors of all stripes, including gold bugs themselves. Yes, the past few years have favored equities over precious metals and I guess that’s where the recency bias kicks in again. But the truth is it has paid far better to be gold bug over the past two decades than to be an equity bull.

The point being to understand your time preference and time reference!

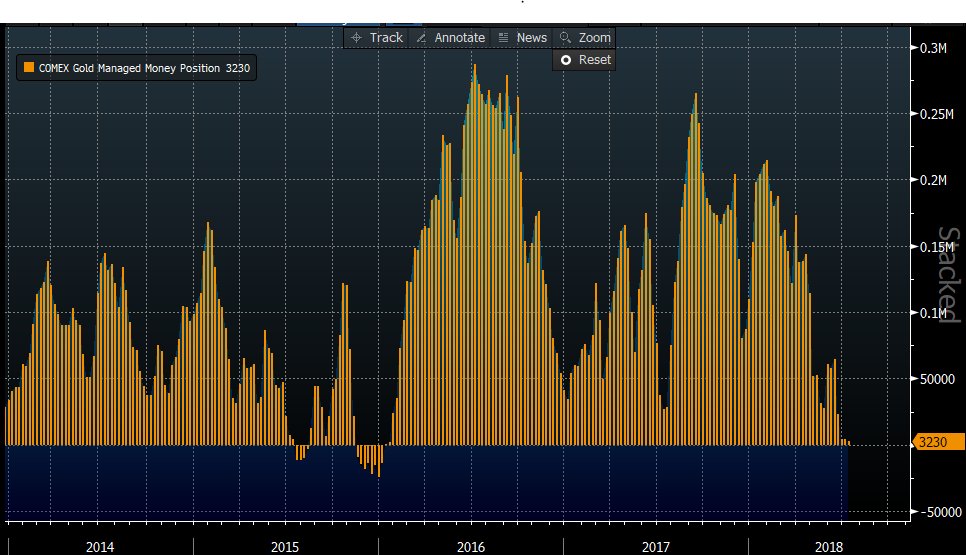

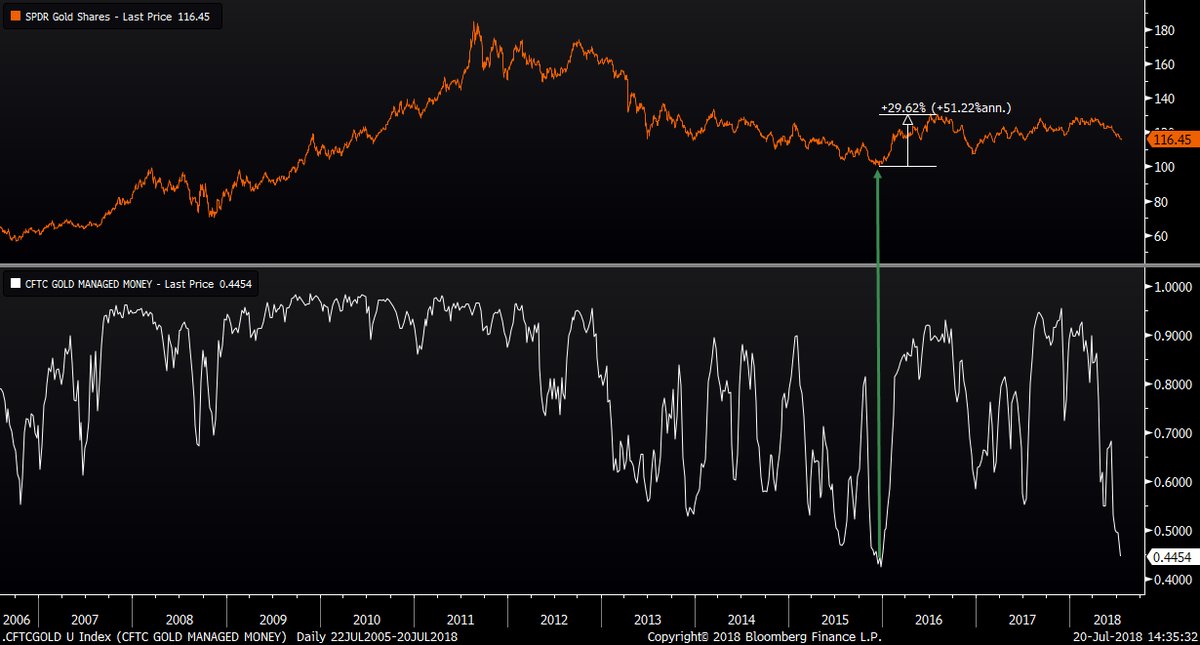

Update:

fred hickey @htsfhickey 20/July 2018 5 PM

Here’s Managed Money(mostly hedge funds) COT details: 134.2K short, 11% higher than highest level (gold’s bottom) seen in 2015, so likely a record.. Net short -26.5k contracts-essentially equal to Dec. 2015 gold bottom. For comparison, at gold’s mid-2016 top they were net 270K long ago

The setup: Gold bugs totally demoralized. Gold sentiment(DSI)down to just 7% with extreme dollar bullishness(92% DSI). Trump beginning to talk $ down (will continue). FY ’19 $1T+ budget deficit. Gold seasonal demand (starts now). Managed Money (hedge funds) net short& have to cover.

It’s likely these are record level shorts. That means there are more shorts than at the bottom in late-2015 – before gold exploded 30% & miners +160% in 6 months and more shorts than at late-2008 bottom before gold soared over 75% in 1 year. Perfect setup-assuming gold’s bottomed.

Whoa Nelly! Just as I suspected it was short traders driving gold down. Thru Tuesday (likely even worse now), a slight increase in longs& another massive 27.7K jump in large spec. futures shorts. In past 5 weeks +121% jump in short contracts to 161K -highest level in at least 11yrs.

BUT, ALWAYS STUDY THE OTHER SIDE–GOLD TO KEEP FALLING.