Karl Pillemer of Cornell University interviewed 1200 people age 70 to 100+ for his book, 30 Lessons for Living,

asking them:

“If you look back over the course of your life, what are the most important lessons you learned that you would like to share with younger people?”

What was the #1 answer?

“Life is short.”

Seneca, in a beautifully worded passage, strongly disagrees:

“It is not that we have a short time to live, but that we waste a lot of it. Life is long enough, and a sufficiently generous amount has been given to us for the highest achievements if it were all well invested. But when it is wasted in heedless luxury and spent on no good activity, we are forced at last by death’s final constraint to realize that it has passed away before we knew it was passing. So it is: we are not given a short life but we make it short, and we are not ill-supplied but wasteful of it… Life is long if you know how to use it.”

No offense to Karl. He did a survey. So he didn’t necessarily get the right answer, he got the most common answer.

I’m with Seneca.

Life doesn’t have to be short.

We all have 24hrs in a day. Every single one of us.

You can use them to create something amazing, to visit that someone special who misses you desperately, to provide for your family, or to savor a great moment.

But don’t waste your hours.

Don’t end up wondering, “What have I been doing with my time?”

Leave a trail of accomplishments or smiles behind you.

– Andrew

—

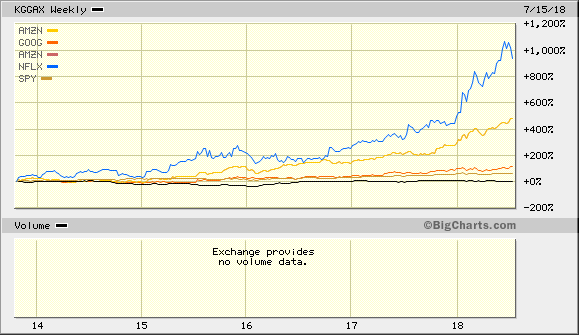

A Deep Value Investor’s Perspective: Kopernik vs, SPY and then FANGs