The above post is an excellent tutorial and case study on riding a volatile, cyclical bull market in Uranium Company, Cameco (and others) from 2000 when CCJ traded about $7 to $8 until mid-2007 or about $40 to $45 (you never get the exact high). That is about a 27% compounded return over seven years. Buying near the low and selling near the high–isn’t that a fantasy. Not if you were following the fundamentals and the sentiment. The hardest part is holding on until it is clearly time to sell.

The article was written by https://www.uraniuminsider.com/ who did a great job on this article. I don’t know him or his newsletter, but I collated his articles in a case study below. I highly recommend you study the case below even if you avoid investing in cyclical, commodity companies.

The case also gives you a condensed application of the capital cycle.

Mr. Kaplan is the perfect investor to study to improve your investing in deeply cyclical resource investments and to understand gold. As Mr. Kaplan explains in an interview (2017): “Gold is not someone’s liability…. Economically, we are in unchartered waters.”

His philosophy is to start with a macro theme (A long-term bull market in gold) and then locate the best asset (Novagold) to leverage that theme. He considers gold the best risk reward of any asset class. Setting aside that gold is the best asset to own during financial crises, gold will be facing a severe supply crunch since no new large deposits over 5 million ounces are being discovered much less developed. Development from discovery to production requires over 20 years.

In addition, more and more foreign jurisdictions like the Philippines or Papua New Guinea are becoming too risky to mine. Mr. Kaplan estimates the equilibrium price to incentivize new discoveries is probably $3,000 to $5,000 per ounce. I think that is too low of a price.

The patience and conviction to be successful in this type of investing are extraordinarily high. Most professional investors cannot even pretend to be as patient. Mr. Kaplan became involved in Novagold during the crisis of 2009–imagine the fear and financial stress swirling amongst investors then.

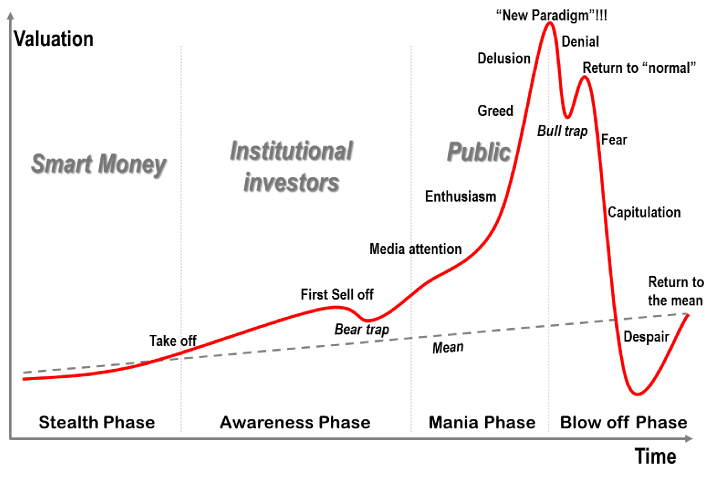

Recognizing the obvious: Intrinsic value rising well before price

From 2009 to 2019 the intrinsic value was rising as Novagold became de-risked. The decade ticked by as Novagold obtained all the required permits, it strengthened relationships with native communities, it spun off non-core assets like Galore (copper) to Trilogy, Novagold treasury increased its cash balance to $250 million with an annual cash burn of less than $10 million, and NG’s relationship with Barrick strengthened. Few cared or paid attention. Meanwhile, many jurisdictions have become even higher risk like the Philippines, Papua New Guinea, etc.

Price goes sideways while intrinsic value rises quietly. These are the best situations to hold onto. You just need VAST patience and to pay attention. Value accretion was occurring away from the financial statements. You would see expenses each quarter, but you would need to be aware of the permits won and the relationships strengthened. No algorithm or computer screening model will do that for you. But NG just traded as part of an index until decoupling in mid-2019. Everything related to Novagold was increasing except the share price until one day……. Meanwhile, Mr. Kaplan held fast because of his knowledge and conviction.

NG trades with the indexes, GDX and GDXJ, then decouples upward as price catches up with intrinsic value.

As a word of caution, this post is not a recommendation to buy Novagold even though I have been a shareholder since 2015. You should understand that Mr. Kaplan has been an investor for over 11 years through declines of 85% in NG’s share price. As an investor you might check on the statements and claims made in the annual reports listed below. If Novagold’s grade is considered outstanding, then look at the annual reports of five major miners and verify/check whether that fact checks out. Take nothing on faith so you can learn conviction.

How would you be willing to hold a investment without a huge payoff for over a decade while waiting for the market to turn to your analysis?

If you study those letters and annual reports, you will have a course in patient investing in a deeply cyclical industry and in understanding gold.

UPDATE 5/1/2020: 2008 Annual Report marks the entry of Electrum during the Great Financial Crisis.

2012 Annual Report began the time when management change had begun in earnest with CEO Greg Lang arriving from Barrick Gold as well as divesting of assets to focus on Donlin Gold. Those actions made the company into a perpetual option on the value of gold.

The Tortoise and The Hare Chairman’s Letter of 2015 explains why Thomas Kaplan was (and remains) bullish towards gold.

Please note how consistent Mr. Kaplan’s and Novagold’s message has been over the past twelve years. The Donlin project attributes remain consistent even while the resource base increases.

Remember that Novagold (NG) as a perpetual option is highly leveraged to the price of gold and to sentiment so expect prices swings of 25% to 50% or more. Such is the requirement to being a long-term investor. My secret is not to look at the share price but once a quarter.

A Stoic would agree with this quote from the above book:

The most important thing successful investors have in common is worrying about what they can control. They don’t waste time worrying about which way the market will go or what the Federal Reserve will do or what inflation or interest rates will be next year. They stay within their circle of competence, however narrow that might be.

Other useful quotes:

In my nearly fifty years of experience in Wall Street I have found that I know less and less about what the stock market is going to do but I know more and more about what investors ought to do; and that is a pretty vital change in attitude — Ben Graham

Investment success accrues not so much to the brilliant as to the disciplined.– William Bernstein

Investors who confine themselves to what they know, as difficult as that may be, have a considerable advantage over everyone else — Seth Klarman

Genius is a rising market — John Galbraith

In a winner’s game the outcome is determined by the correct actions of the winner. In a loser’s game, the outcome is determined by mistakes made by the loser. — Charlie Ellis

How could economics not be behavioral? If it isn’t behavioral, what the hell is it? — Charlie Munger

You need patience, discipline, and an ability to take losses without going crazy — Charlie Munger, 2005

You will do a great disservice to yourselves, to your clients, and to your businesses, if you view behavioral finance mainly as a window onto the world. In truth, it is also a mirror that you must hold up to yourselves. — Jason Zweig

If I could sum up the lesson of the above 175-page book at $35, it would be that IF you invest long-term in compounders or franchise companies that redeploy their capital at high rates of return, then expect to suffer through multiple 50% to 60% declines in stock price as you hold on for the long-term. And remember that a price decline of 50% does not necessarily indicate a bargain.

You can see the 50% sell-off in Bershire’s stock in 1999/2000 while you can barely make out the multiple 50% or more declines in AMZN over the past twenty years. Investing is HARD!

To understand the prospects for bitcoin and the other cryptocurrencies and tokens, it is necessary to grasp the centrality of gold.

Gold resolved both the horizontal and vertical enigmas of money. As a universal index of value, it muted the volatile shifts and shuffles of exchange rates. As an unchanging standard, it made interest rates a reliable guide for entrepreneurs making commitments in the darkness of time.

The gold standard thus provided maps and metrics that enabled entrepreneurs to act confidently across time and space. they were assured that in an ever-changing and insecure world the monetary measuring sticks would not change when they brought their products in for a landing in the marketplace.

As King Midas discovered, gold (and all candidates to be real money) is not wealth itself but a metric of wealth. While some gold advocates–including George Gilder in years past–have insisted that its slow but steady 2 percent rate of growth assures an expanding supply of money. But under a gold standard, the money supply has virtually nothing to do with the gold supply. In 1775, the total mount of currency in circulation (primarily gold and silver coins) was an estimated $12 million. In 1900, it was $1,954 million –an increase of 163X. During this time, the amount of gold in the world increased by about 3.4 times, due to mining production.

Since gold does not deteriorate, all the 189,000 tones of gold mined over the centuries remains available for use as money. Maintaining neutrality in time and space, gold is neither inflationary nor deflationary (KEY POINT!) It penalized neither creditors nor debtors. It is a measuring stick and unit of account for the world’s goods and services.

Bitcoin

Satoshi, the “founder” of Bitcoin believed that his mining algorithm was mimicking gold. Bitcoin did laboriously cancel out the advance of technology through its ten-minute mining cycles and lottery process.

However, Mike Kendall, who was drilling down into the economic model of bitcoin as a possible successor to the gold standard noted that “Contrary to the most egregiously erroneous and central tenet of the state theory of money, it was not government that decreed gold as money, rather it is only by holding gold that governments could EVEN ISSUE ANY FORM OF MONEY AT ALL.” http://manonthemargin.com/notes-on-the-bitcoin-standard/

Nakamoto invented digital scarcity….a digital good that is scarce and cannot be reproduced infinitely….a digital good whose transfer stops it from being owned by the sender..

“The limit on the quantity we can produce of any good is never its prevalence on the planet, but the effort and time dedicated to producing it. With its absolute scarcity, writes Ammous, “bitcoin is highly salable across time.”

THE FATAL FLAW

The fatal flaw is the belief that the money supply can and should be determined by the supply of bitcoin or gold. Gold (or bitcoin mimicking gold) should serve not only as a measuring stick or unit of account but as the actual medium for all exchanges.

Such monolithic money was also the ERROR of Murray Rothbard, an idiosyncratic exponent of Austrian theory who believed that any authentic gold standard must have 100 percent gold backing. He did not even believe in fractional reserve banking, intrinsic to the role of banks, which necessarily mediates between savers seeking safety and liquidity and entrepreneurs destroying it through long-term investments. The value of liquid savings is necessarily dependent on the achievements of illiquid and long-term enterprise. There is no way to avoid the maturity mismatch between savings and investments except by abolishing capitalism.

In the same way, bitcoin and other cryptocurrencies cannot become significant money without systems to intermediate between savers and investors. Money cannot be simply a smart contract. It entails continual acts of intelligent discretion in the provision of loans and investments responding to changes in markets and technologies.

Cameron Harwick of George Mason University makes the point that BITCOIN CANNOT SUCCEED AS A SMART CONTRACT; IT MUST BE COMPLEMENTED BY AN ENTREPRENURIAL BANKING FUNCTION:

If the main source of Bitcoin’s volatility is volatile demand, we can expect the issue and circulation of bitcoin-redeemable liabilities to stabilize the demand for and therefore the value of Bitcoin by allowi9ng fluctuations to be borne by changes in the supply of liabilities rather than by the price level or the volume of transactions.

A currency needs oracles to channel it to the most promising entrepreneurial uses.

As Kendall explains, “While Satoshi was brilliant in creating the blockchain as the basis for bitcoin, Satoshi had no understanding of currency as a unit of account. By limiting bitcoin’s supply to 21 million units over a 131-year period, Satoshi designed bitcoin as a deflationary currency….Because of its deflationary design, bitcoin is used more as a volatile investment bet: than as a MEASURING STICK or UNIT OF ACCOUNT. In other words, bitcoin’s fixed limit is deflationary and unworkable.

Bitcoin is the transactions medium ITSELF rather than a stable metric for the valuation of fiat moneys. For gold, transactions are incidental; for bitcoin, transactions are the key point. Bitcoin, unlike gold, must therefore increase in either volume or value if the system is to succeed.

Bitcoin, as now constituted, CANNOT BE A CURRENCY. Currencies create value by measuring it. The price of bitcoin changes with demand. You could respond that the price of the dollar also changes with demand. That has been mostly true since 1971, and such fluctuations are the Achilles heel of the dollar as a long-term currency.

“No other basic unit of measure,” says Kendall–whether it is the second, the meter, the ampere, or the kilogram-“changes in value with demand. They are standards” based on physical constants. IF MONEY IS A MEASURING STICK, IT CANNOT RESPOND TO DEMAND.

Since bitcoin cannot fulfill its basic role as a currency. its historical fate is to provide a haven from governments and central banks and a harbor for a great innovation, the blockchain.

Source: Life After Google by George Gilder.

—

The EXPERTS

Lorimer Wilson January 24, 2011

$5,000 Gold Bandwagon Now Includes 85 Analysts!

More and more economists, analysts and financial writers, 125 in fact, have taken the bold step of projecting the price at which gold will achieve its parabolic peak with 5 individuals claiming that the peak price will be realized sometime in 2011. Some have adjusted their previous prognostications higher given gold’s strong advance again in 2010 while others have jumped aboard what has become a bandwagon of optimism. The majority (85) maintain that $5,000 or more for gold is possible.

These 5 Analysts Believe Gold Will Reach Parabolic Peak Sometime in 2011

1. Bob Kirtley: $10,000;

2. Patrick Kerr: $5,000 – $10,000;

3. James Dines: $3,000 – $5,000;

4. Taran Marwah: $3,000;

5. Jim Sinclair: $3,000 – $5,000 (by June 2011);

These 6 Analysts See Gold Price Going Parabolic to +$10,000

1. Mike Maloney: $15,000;

2. Ben Davies: $10,000 – $15,000;

3. Howard Katz: $14,000;

4. Dr. Jeffrey Lewis: $7,000 – $14,000;

5. Jim Rickards: $4,000 – $11,000;

6. Roland Watson: $10,800

These 46 Analysts See Gold Price Peaking Between $5,001 and $10,000

1. Bob Kirtley: $10,000 (by 2011);

2. Arnold Bock: $10,000 (by 2012);

3. Porter Stansberry: $10,000 (by 2012);

4. Peter George: $10,000 (by Dec. 2015);

5. Tom Fischer: $10,000;

6. Shayne McGuire: $10,000;

7. Eric Hommelberg: $10,000;

8. David Petch: $6,000 – $10,000;

9. Gerald Celente: $6,000 – $10,000;

10. Egon von Greyerz: $6,000 – $10,000;

11. Peter Schiff: $5,000 – $10,000 (in 5 to 10 years);

12. Patrick Kerr: $5,000 – $10,000 (by 2011);

13. Peter Millar: $5,000 – $10,000;

14. Roger Wiegand: $5,000 – $10,000;

15. Alf Field: $4,250 – $10,000;

16. Jeff Nielson: $3,000 – $10,000;

17. Dennis van Ek: $9,000 (by 2015);

18. Dominic Frisby: $8,500;

19. Paul Brodsky: $8,000;

20. James Turk: $8,000 (by 2015);

21. Joseph Russo: $7,000 – $8,000;

22. Bob Chapman: $7,000+;

23. Michael Rozeff: $2,865 – $7,151;

24. Jim Willie: $7,000;

25. Dylan Grice: $6,300;

26. Chris Mack: $6,241.64 (by 2015);

27. Chuck DiFalco: $6,214 (by 2018);

28. Jeff Clark: $6,214;

29. Aubie Baltin: $6,200 (by 2017);

30. Murray Sabrin: $6,153;

31. Samuel “Bud” Kress: $6,000 (by 2014);

32. Adam Hamilton: $6,000;

33. Robert Kientz: $6,000;

34. Harry Schultz: $6,000;

35. John Bougearel: $6,000;

36. David Tice: $5,000 – $6,000;

37. Laurence Hunt: $5,000 – $6,000 (by 2019);

38. Taran Marwah: $3,000 – $6,000+ (by Dec. 2011 and Dec. 2012, respectively);

39. Martin Hutchinson: $3,100 – $5,700;

40. Stephen Leeb: $5,500 (by 2015);

41. Louise Yamada: $5,200;

42. Jeremy Charlesworth: $5,000+;

43. Przemyslaw Radomski: $5,000+;

44. Jason Hamlin: $5,000+;

45. Greg McCoach: $5,000+ (by 2012)

46. David McAlvany: $5,000+

Cumulative sub-total: 52

These 34 Analysts Believe Gold Price Could Go As High As $5,000

1. David Rosenberg: $5,000;

2. Doug Casey: $5,000;

3. Peter Cooper: $5,000;

4. Robert McEwen: $5,000 (by 2012 -2014);

5. Martin Armstrong: $5,000 (by 2016);

6. Peter Krauth: $5,000;

7. Tim Iacono: $5,000 (by 2017);

8. Christopher Wyke: $5,000;

9. Frank Barbera: $5,000;

10. John Lee: $5,000;

11. Barry Dawes: $5,000;

12. Bob Lenzer: $5,000 (by 2015);

13. Steve Betts: $5,000;

14. Stewart Thomson: $5,000;

15. Charles Morris: $5,000 (by 2015);

16. Marvin Clark: $5,000 (by 2015?);

17. Eric Sprott: $5,000;

18. Nathan Narusis: $5,000;

19. Bud Conrad: $4,000 – $5,000;

20. Paul Mylchreest: $4,000 -$5,000;

21. Pierre Lassonde: $4,000 – $5,000;

22. Willem Middelkoop: $4,000 – $5,000;

23. Mary Anne and Pamela Aden: $3,000 – $5,000 (by February 2012);

24. James Dines: $3,000 – $5,000 (by June 2011);

25. Goldrunner: $3,000 – $5,000 (by 2012);

26. Bill Murphy: $3,000 – $5,000;

27. Bill Bonner: $3,000 – $5,000;

28. Peter Degraaf; $2,500 – $5,000;

29. Eric Janszen: $2,500 – $5,000;

30. Larry Jeddeloh: $2,300 – $5,000 (by 2013);

31. Larry Edelson: $2,300 – $5,000 (by 2015);

32. Luke Burgess: $2,000 – $5,000;

33. Jim Sinclair: $3,000-$5,000 (by June 2011);

34. Marc Faber: $1,500 – $5,000

Cumulative sub-total: 86

These 27 Analysts Believe Gold Will Achieve a Parabolic Peak Price Between $3,000 and $4,999

1. David Moenning: $4,525;

2. Larry Reaugh: $4,000+;

3. Mike Knowles: $4,000;

4. Ian Gordon/Christopher Funston: $4,000;

5. Barry Elias: $4,000; (by 2020);

6. Jay Taylor: $3,000 – $4,000;

7. Christian Barnard: $2,500 -$4,000;

8. John Paulson: $2,400 – $4,000 (by 2012);

9. Myles Zyblock : $3,800;

10. Eric Roseman: $3,500+;

11. Christopher Wood: $3,360;

12. Franklin Sanders: $3,130;

13. John Henderson: $3,000+ (by 2015-17);

14. Michael Berry: $3,000+; (by 2015)

15. Hans Goetti: $3,000;

16. Michael Yorba: $3,000;

17. David Urban: $3,000;

18. Mitchell Langbert: $3,000;

19. Brett Arends: $3,000;

20. Ambrose Evans-Pritchard: $3,000;

21. John Williams: $3,000;

22. Byron King: $3,000;

23. Ron Paul: $3,000 (by 2020);

24. Chris Weber: $3,000 (by 2020);

25. Mark Leibovit: $3,000;

26. Mark O’Byrne: $3,000;

27. Kevin Kerr: $3,000

Cumulative sub-total: 113

Source:- http://www.munknee.com

There seems to be one name missing from the list. All those SWAGS have missed one important element. When you are talking about the price of gold, you are talking about two commodities, gold and whatever currency you are quoting the price in.

If you can’t predict the value of the dollar in the future with accuracy, you cannot predict the price of gold either.

You should buy gold when it is cheap and unloved. You should then sell it when it is expensive and everyone loves it.

Because intelligence is absolutely no barrier to cult recruitment. This is because a person’s intelligence is totally bypassed during the process of cult recruitment. When reality testing is suspended then one’s intelligence is not applied at all in order to ascertain the reasonableness of the cult’s teachings.

Do you want to transcend your consciousness and be blissfully happy forever? https://www.tm.org/

Or

Don’t Fall Down The Rabbit Hole

An ex-TM teacher peels back the union and reveals the dark side of the TM and the TM organization. The Maharishi was a sociopath in his eyes. A very thorough discussion of cult mind techniques from an insider of Transcendental Meditation:Skeptical TM

What does questioning the benefits of TM have to do with investing? Be skeptical. Attack your favorite ideas. Never stop questioning and learning. Note that several TM instructors quit when they saw paid scientists doctoring studies to benefit the TM.org.

There are benefits to meditation and, yes, transcendental meditation–if done in a limited fashion for relaxation–can induce a state of deep relaxation. The problem is the hype and supposed need to learn from a teacher or “guru.” ONLY an expert knows your proper mantra. PLEASE…….

The simple Relaxation Response helps me be better focused. I avoid having a “monkey-mind.” My suggestion is to learn for free (Don’t pay $1000’s for TM training) by viewing the video below and give yourself a few weeks. Keep a journal of your progress. If you see no benefit then stop. I take fifteen minutes in the morning and 15 minutes in the afternoon. No, your problems won’t evaporate nor will you transcend humanity and see God, but you may be more relaxed, less irritable, calmer, more focused, and, strangely, more compassionate.

Please put a check mark by the letter you choose or write it down next to the number of the question.

You will be compared to a Chimp who—on each question—will be thrown bananas labeled A, B, or C.

The Chimp will answer correctly about 33% of the questions.

GOOD LUCK!

In all low-income countries across the world today, how many girls finish primary school?

A. 20 percent

B. 40 percent

C. 60 percent

Where does the majority of the world population live?

A. low-income countries

B. middle-income countries

C. high-income countries

In the last 20 years, the proportion of the world population living in extreme poverty has….

A. Almost doubled

B. Remained more or less the same

C. Almost halved

What is the life expectancy of the world today?

A. 50 years

B. 60 years

C. 70 years

There are 2 billion children in the world today, aged 0 to 15 years old. How many children will there be in the year 2100, according to the United Nations?

A. 4 billion

B. 3 billion

C. 2 billion

The UN predicts that by 2100 the world population will have increased by another 4 billion. What is the main reason?

A. There will be more children age below 15

B. There will be more adults age 15 to 74

C. There will be more very old people aged 75 and older.

How did the number of deaths per year from natural disasters change over the last hundred years?

A. More than doubled

B. Remained about the same

C. Decreased to less than half

How many of the world’s 1-year-old children today have been vaccinated against some disease?

A. 20 percent

B. 50 percent

C. 80 percent

9 World-wide, 30-year-old men have spent 10 years in school, on average, how many years have women of the same age spent in school?

A. 9 years

B. 6 years

C. 3 years

10 In 1996, tigers, giant pandas, and black rhinos were all listed as endangered. How many of these three species are more critically endangered today?

A. Two of them

B. One of them

C. None of them

11. How many people in the world have some access to electricity?

A. 20 percent

B. 50 percent

C. 80 percent

Global climate experts believe that, over the next 100 years, the average temperature will……

A. Get warmer

B. Remain the same

C. Get colder

Email: Aldridge56@aol.com with the subject heading: CHIMPSand I will email you the answers. Did you beat the chimps?

A reader shares his investment conference in Cyprus

I wonder if this crowd could beat the chimps? Bets?

If you only read one post on this blog, then let it be this one. John Chew

Let me tell you the story of two investors, neither of whom knew each other, but

whose paths crossed in an interesting way.

Grace Groner was orphaned at age 12. She never married. She never had kids. She never drove a car. She lived most of her life alone in a one-bedroom house and worked her whole career as a secretary. She was, by all accounts, a lovely lady. But she lived a humble life. That made the $7 million she left to charity after her death in 2010 at age 100 all the more confusing. People who knew her asked: Where did Grace get all that money?

But there was no secret. There was no inheritance. Grace took humble savings

from a meager salary and enjoyed eighty years of hands-off compounding in the stock market. That was it.

Weeks after Grace died, an unrelated investing story hit the news. Richard Fuscone, former vice chairman of Merrill Lynch’s Latin America division,

declared personal bankruptcy, fighting off foreclosure on two homes, one of which was nearly 20,000 square feet and had a $66,000 a month mortgage.

Fuscone was the opposite of Grace Groner; educated at Harvard and

University of Chicago, he became so successful in the investment industry

that he retired in his 40s to “pursue personal and charitable interests.” But

heavy borrowing and illiquid investments did him in. The same year Grace

Goner left a veritable fortune to charity, Richard stood before a bankruptcy

judge and declared: “I have been devastated by the financial crisis … The

only source of liquidity is whatever my wife is able to sell in terms of personal

furnishings.”

The purpose of these stories is not to say you should be like Grace and avoid

being like Richard. It’s to point out that there is no other field where these

stories are even possible.

In what other field does someone with no education, no relevant experience,

no resources, and no connections vastly outperform someone with the best

education, the most relevant experiences, the best resources and the best

connections? There will never be a story of a Grace Groner performing heart

surgery better than a Harvard-trained cardiologist. Or building a faster chip

than Apple’s engineers. Unthinkable.

But these stories happen in investing.

That’s because investing is not the study of finance. It’s the study of how people behave with money. And behavior is hard to teach, even to really smart people. You can’t sum up behavior with formulas to memorize or spreadsheet models to follow. Behavior is inborn, varies by person, is hard to measure, changes over time, and people are prone to deny its existence, especially when describing themselves.

Grace and Richard show that managing money isn’t necessarily about what

you know; it’s how you behave. But that’s not how finance is typically taught

or discussed. The finance industry talks too much about what to do, and not

enough about what happens in your head when you try to do it.

This report describes 20 flaws, biases, and causes of bad behavior I’ve seen

pop up often when people deal with money.

The above article confirms my bias that all the MBAs, CFAs, CPAs, and study won’t help you unless you understand yourself. Tough. For example, I can see the speck in your eye but not the mud in mine.

Two Investors

Two Investors