Selling today in the pits-gold and silver

Selling today in the pits-gold and silver

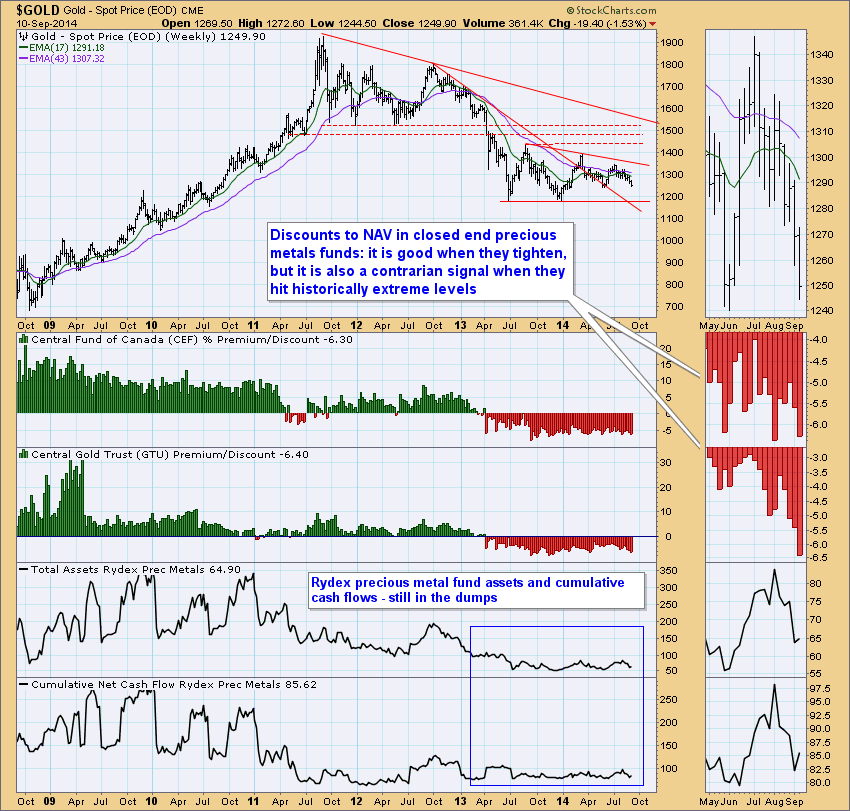

Above is a chart of CEF, Canadien Gold (60%) and Silver (40%) bullion closed-end fund trading at a 6.5% discount today. ON SALE! I have no clue if tomorrow the price will be higher or lower.

http://www.cefconnect.com/Details/Summary.aspx?Ticker=CEF

Note the premiums as high as 10% and currently 6.5% discount.

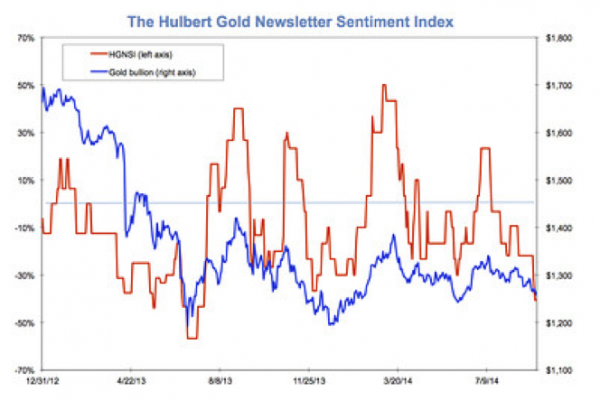

Learn more about interpretating sentiment indicators: www.acting-man.com

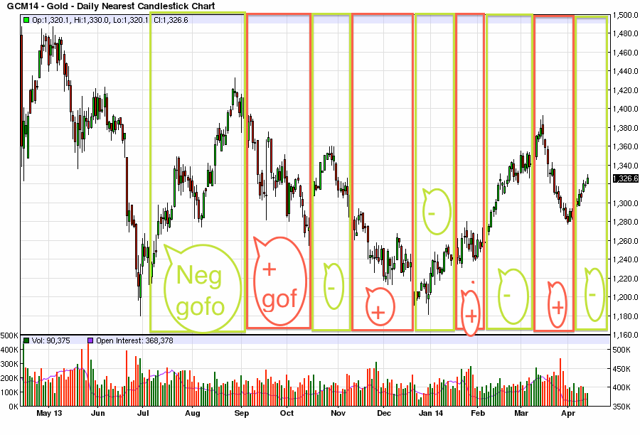

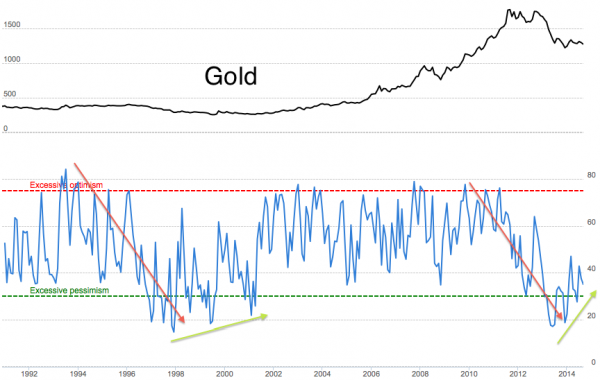

Long term sentiment

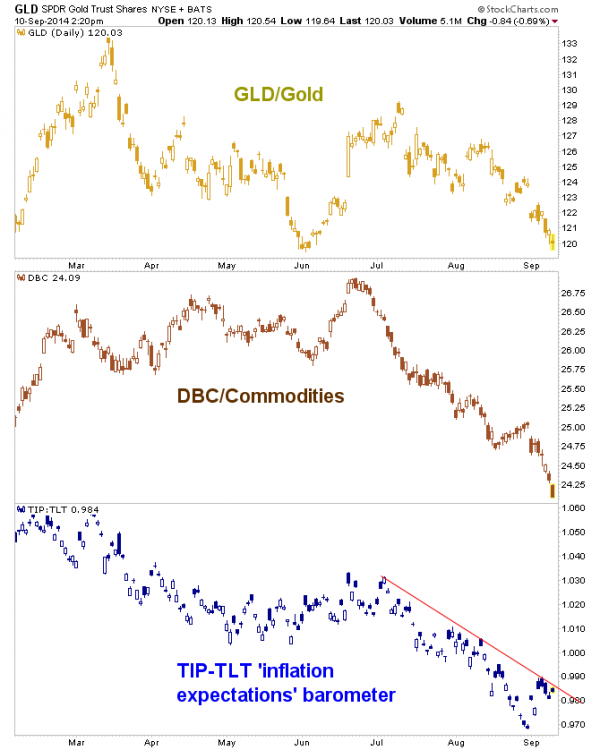

A Great blog, Down the Rabbit Hole: http://biiwii.com/wordpress/2014/09/10/sentiment-shifting-gold-bugs/

Though, I like miners more, but now is a good time to pick up tangible money at a discount. Pay 94 cents and get a dollar of gold and silver today–I will take it. SOLD! Miners make money on the arbitrage between their input costs and output prices. You don’t need a rising nominal gold price; you need a rising REAL gold price.

Now is the time for me to post on Yamana (by this weekend, I pray) because it is at a price $7.33 that I have purchased in the past and it may be a reasonable choice for a BASKET of miners.

Also, you want to see analysts pile-on negatively AFTER price has fully dicounted the news. I am not being contrarian or cynical, it is just how markets work–they DISCOUNT.

Yamana Gold suffers rash of stock price target cuts • 12:58 PM

- Yamana Gold (AUY -1.2%) is lower after Morgan Stanley, Credit Suisse and Raymond James cut their price targets on the stock to $10.70, $10.50, and $10, respectively.

- In the case of Morgan Stanley, the lower target still implies upside of more than 40%; AUY has said the Pilar mine in Brazil has shown improvements with output increasing M/M, but the ramp up is tracking modestly below expectations, thus the firm’s tempered outlook.

- An update on Canadian Malartic and meeting quarterly expectations are potential catalysts expected over the next 6-8 weeks.

Read the link below and the link within it to gain more understanding on gold and miners.