The above letters can teach you how a business owner should communicate

with his or her fellow owners. A lesson in understanding a business.

The above letters can teach you how a business owner should communicate

with his or her fellow owners. A lesson in understanding a business.

Introducing HOLT Economic Profit

Valuation of Classic Companies

I haven’t had a chance to read the above, but a reader shared them. Let me know if useful.

Perhaps you should differentiate yourself by focusing on management’s character and skill. However, you will need to focus and work hard to make a difference in understanding who is unique.

Find founder-led companies who are mission driven–one place to start your search.

Imagine putting the numbers of Berkshire Hathaway during the early days of Buffett’s takeover into a spreadsheet–would ANYONE have bought Berkshire. Who would have focused on Buffett’s integrity and skills?

Also: https://microcapclub.com/2018/05/invest-in-owner-management/

Interviewer: Are you unbiased?

John Chew: What a dumb question! Next.

Interviewer: No matter how you answered that question, how could you have an edge in researching companies?

John Chew: Well, I ……………..

and

Any suggestions? Is it possible to be unbiased? And based on your answer, how can you have an edge researching companies? Prize.

Posted in Investing Gurus, Search Strategies, Valuation Techniques, YOU

Tagged biased. Unbiased, Choosing Management, Managment, Robert Vinall, RV Capital

Alternatives to College

Posted in Free Courses, Valuation Techniques

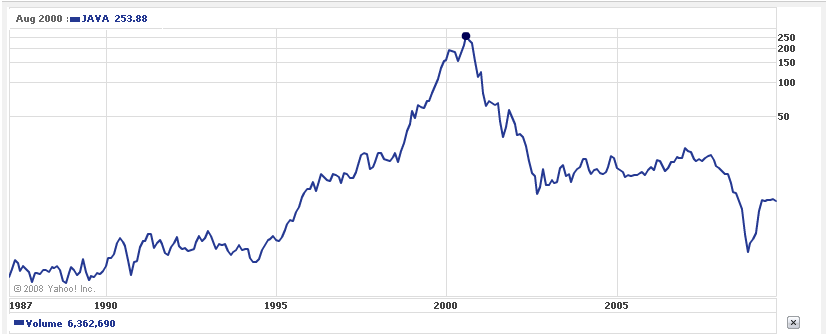

While at all times Wall Street analysts try to justify the valuations, here is a fun quote (via Bloomberg) from 2002 looking back from Scott McNeely, the CEO of Sun Microsystems, one of the darlings of the 2000 tech bubble:

“At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes.

What were you thinking?”

An educational, savagely satirical view of our current market conditions and lessons on valuation. I read about 40 investment letters a quarter and this is about the best I have read in five years. Hilarious! Mark McKinney – Its Like Deja Vu All Over Again – Final and his prior letter: I Dont Get It – Mark McKinney – Final 8292017 New

—

An excellent interview by Tobias Carlisle. CHEAPNESS not quality wins! Yes, I was somewhat shocked. Why?

http://www.valuewalk.com/2018/01/tobias-carlisle-talks-acquirers-multiple-valuetalks/

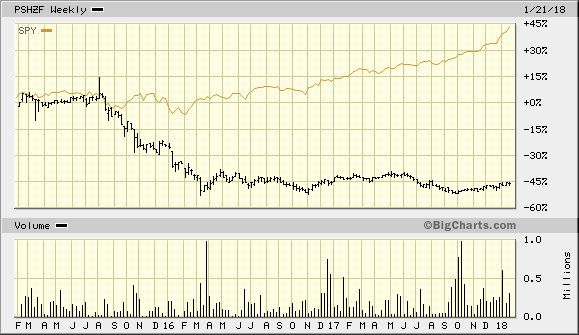

Ackman’s embattled Pershing Square hedge fund laid off 18 percent of its staff on Friday — a total of 10 pink slips that brought head count down to 46.

Investors have suffered in Pershing Square (PSHZF) vs. S&P 500:

He wants to hire an analyst who can THINK INDEPENDENTLY. You walk into his office and he asks you, “Can you think independently as an analyst?”

How do you reply. Be careful…………think for awhile before you reply. What proof can you give?

If you are struggling to answer, then https://www.newyorker.com/magazine/2015/11/23/conversion-via-twitter-westboro-baptist-church-megan-phelps-roper

will provide clues.

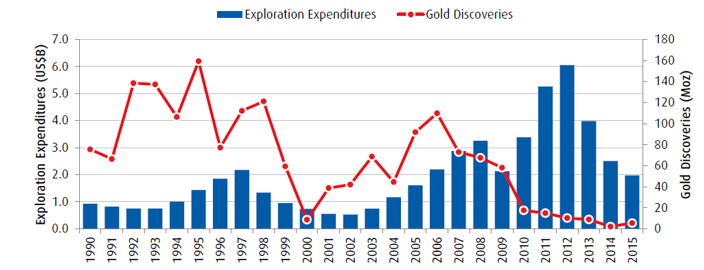

We last discussed Sandstorm (SAND) here: http://csinvesting.org/2017/11/01/sanstorm-gold-analysis-other-readings/

I did a back of the envelope valuation here: Sand Report

The analysis is in response to http://csinvesting.org/2017/10/27/sandstorm-gold-so-whats-it-worth/

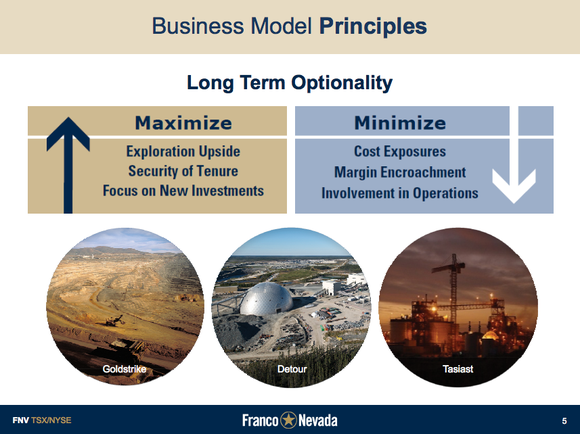

Business Model

Sandstorm provides financing for other junior, mid-tiers and major gold producers. In exchange for a principal amount provided by Sandstorm, gold producers exchange a royalty stream on their gold production. This royalty stream can take different forms, the most common being a percentage of Net Smelter Revenue (“NSR”) or by offering an off-take agreement at discounted prices. In addition, Sandstorm may receive warrants or other traded securities.

Sandstorm offers their shareholders a diversified portfolio of royalty streams, which offers some benefits over investing in a gold exploration/producing company: 1) predictable cash flows, 2) very low cost structure, 3) replacement capex (investment in new projects) typically much lower than for a gold producer.

In my view, this kind of investment should benefit from a lower cost of capital because of its lower risk, so therefore investors would be willing to pay more for this cash flow stream vs. a cash flow stream coming out directly from a mine.

Valuation

I’m looking at 3 main buckets of value here.

1) Producing assets – currently generate ~US$50mm of cash flows each year. My rough assumption here is that these cash flows should be relatively stable over the next 10 years. I assume no terminal value as these mines are winded-down over time. Discounting this at a cost of equity of ~8% yields ~US$335mm

2) Advanced exploration / explo / investment portfolio – I’m assuming no value to the exploration projects and assuming a 10% discount to the FMV of the investment portfolio. This yields ~US$70mm.

3) Development projects – this one is certainly tougher to ascribe value. If we look at the SSL presentation, we see that the majority of future cash flows will come out from Hot Maden which was paid US$175mm. Assuming there was a market check done on the sale of the stream, we can assume this is market value. Other projects from the development portfolio will also yield future cash flows, but it can be assume to be somewhat captured in the above DCF.

So overall, I compute US$335mm + US$70mm + US$175mm = US$580 which is far from the current market cap of the company.

One needs to believe that the development portfolio will materialize into sustainable cash flows (which would essentially translate into the addition of a terminal value in my DCF) before investing in this business.

Let me know your thoughts and feel free to share my response on your website!

CSInvesting: I will be posting my thoughts soon.

https://thefelderreport.com/2017/10/31/tobias-carlisle-on-beating-the-little-book-that-beats-the-market/ Worth a listen!

Posted in Valuation Techniques

Tagged Financial History, Sandstorm gold, Valuations, Wiserdaily

If am able to provide an investing course, then once the fundamentals are covered, we could study cases. Let me know your thoughts.

—

Your boss slaps these documents on your desk. “Let me know what you think. I want a back-of-the-envelope valuation and a sixty-second summary of this business by this afternoon.”

What’s the essence of this business? Hannibal Lecter will guide you: https://youtu.be/UhDZPYu8piQ?t=58s

Your analysis should be clear and simple:

How can the portfolio manager expect YOU to answer quickly with this deluge of info? That’s what we will learn here today.

I will post my “answer” by Tuesday of next week. Email me at aldridge56@aol.com if you wish to share your thoughts or do so at the deep-value group at Google Groups (sign up here: http://csinvesting.org/2015/01/14/deep-value-group-at-google/) rather than post in the comments section, because readers shouldn’t be influenced by others. No help! This case illustrates the reality at investment firms. Your boss dumps a 500-page prospectus and says get back to me in two hours–“What’s it worth?”

Have fun!

CSInvesting: We can’t increase our IQ but we can try to improve our critical thinking skills by seeking out opposing views to the now current din of pundits screaming that this “over-valued market is set to crash.” 1987 here we come. What do you think of his arguments? I certainly agree about how GAAP accounting punishes growth investments.

At Oakmark, we are long-term investors. We attempt to identify growing businesses that are managed to benefit their shareholders. We will purchase stock in those businesses only when priced substantially below our estimate of intrinsic value. After purchase, we patiently wait for the gap between stock price and intrinsic value to close.

“All the company would have to do is raise prices 50% and the P/E ratio would fall to the low-teens.” -Analyst recommending a new stock purchase

We are nine years into an economic and stock market recovery and P/E ratios are elevated somewhat beyond historic averages. So when an experienced portfolio manager hears a young analyst make the above comment, he hears alarm bells. But instead of seeing this as a sign that the market has peaked, we purchased the stock for the Oakmark Fund. But, more on that later.

For several years, the financial media has been dominated by pronouncements that the bull market is over. Throughout my career, I can’t remember a more hated bull market. Many state that a recession is “overdue” since past economic booms have almost never lasted as long as this one. But do nine years of sub-normal economic growth even constitute a recovery, much less a boom? If recessions occur to correct excesses in the economy, has this recovery even been strong enough to create any? Maybe recessions are less about duration of the recoveries they follow and more about the magnitude. If so, earnings might not even be above trend levels.

Bears will also point to the very high CAPE ratio—or the cyclically adjusted P/E. That metric averages corporate earnings over the past decade in an attempt to smooth out peaks and valleys. But remember that the past decade includes 2008 and 2009, frequently referred to as the “Great Recession” because of how unusually bad corporate earnings were. I’ll be the first to say that if you think an economic decline of that magnitude is a once-in-a-decade event, you should not own stocks today. But if it is more like a once-in-a-generation event, then that event is weighted much too heavily in the CAPE ratio. If the stock market and corporate profits maintained their current levels for the next two years—an outcome we would find disappointing—simply rolling off the Great Recession would result in a large decline in the CAPE ratio.

Higher P/E ratios are also caused by near-zero short-term interest rates because corporate cash now barely adds to the “E” in the P/E ratio. When I started in this business in the early 1980s, cash earned 8-9% after tax. Consider a simple example of a company whose only asset is $100 of cash and the market price is also $100. In the early 1980s, the $8 or $9 of interest income would generate a P/E ratio of about 12 times. Today, $100 would produce less than $1 of after-tax income, driving the P/E ratio north of 100 times. There is, of course, uncertainty as to whether that cash will eventually be returned to shareholders or invested in plants or acquisitions, but it seems that making a reasoned guess about the value of cash is more appropriate than valuing it at almost nothing.

A less obvious factor that is producing higher P/E ratios today is how accounting practices penalize certain growth investments. When a company builds a new plant, GAAP accounting spreads that cost over its useful life—often 40 years—so the cost gets expensed through 40 years of depreciation as opposed to just flowing through the current income statement.

But when Amazon hires engineers and programmers to help it prepare for sales that could double over the next four years, those costs get immediately charged to the income statement. When Facebook decides to limit the ad load on WhatsApp to allow it to quickly gain market share, the forgone revenue immediately penalizes the income statement. And when Alphabet invests venture capital in autonomous vehicles for rewards that are years and years away, the costs are expensed now and current earnings are reduced.

The media is obsessed with supposedly bubble-like valuations of the FANG stocks—Facebook, Amazon, Netflix and Google (Alphabet). The FANG companies account for over 7% of the S&P 500 and sell at a weighted average P/E of 39 times consensus 2017 earnings. In our opinion, the P/E ratio is a very poor indicator of the value of these companies. Alphabet is one of our largest holdings, and our valuation estimate is certainly not based on its search division being worth 40 times earnings. If one removed the FANG stocks from the S&P multiple calculation—not because their multiples are high, but because they misrepresent value—the market P/E would fall by nearly a full point. And, clearly, more companies than these four are affected by income statement growth spending.

In addition, no discussion of stock valuations would be complete without some consideration of opportunities available in fixed income. Many experts argue that investors should sell their stocks because the current S&P 500 P/E of 19 times is higher than the 17 times average of the past 30 years. By comparison, if we think of a long U.S. Treasury bond—say, 30 years—in P/E terms, the current yield of 2.9% results in a P/E of 34 times. The average yield on long Treasuries over the past 30 years has been 5.5%, which translates to a P/E of 18 times. Relative to the past 30 years, the long bond P/E is now 90% higher than average. We don’t think the bond market at current yields is any less risky than equities.

We think our investors would also fare best by limiting their in-and-out trading. We suggest establishing a personal asset allocation target based on your financial position and risk tolerance. Then limit your trading to occasionally rebalancing your portfolio to your target. If the strong market has pushed your current equity weighting above your target, by all means take advantage of this strength to reduce your exposure to stocks.

Now, back to the P/E ratio distortions caused by investing for growth. This highlights a costly decision we made six years ago. In 2011, when Netflix traded at less than $10 per share, one of our analysts recommended purchase because the price-per-subscriber for Netflix was a fraction of the price-per-subscriber for HBO. Given the similarity of the product offerings and Netflix’s rapid growth, it seemed wrong to value the company’s subscribers at less than HBO’s. But, at the time, streaming was a relatively new technology, HBO subscribers had access to a much higher programming spend than Netflix subscribers and Netflix was primarily an online Blockbuster store, providing access to a library of very old movies. Netflix had only one original show that subscribers cared about, House of Cards, and churn was huge as they would cancel the service after a month of binging on the show. Despite the attractive price-per-sub, we concluded that the future of Netflix was too uncertain to make an investment.

Today, Netflix trades at $180 per share and has more global subscribers than the entire U.S. pay-TV industry. Netflix provides its subscribers access to more than two times the content spending that HBO offers, making it very hard for HBO to ever match the Netflix value proposition. Finally, Netflix is no longer just a reseller of old movies. The company has doubled its Emmy awards for original programming in each of the past two years and now ranks as the second most awarded “network.” On valuation, Netflix is still priced similarly to the price-per-subscriber implied by AT&T’s acquisition of HBO’s parent company Time Warner, despite Netflix subscribers more than quadrupling over the past four years while HBO subscribers have grown by less than one third.

Last quarter, when our analyst began his presentation recommending Netflix, selling at more than 100 times estimated 2017 earnings, I was more skeptical than usual. His opening comment was that Netflix charges about $10 per month while HBO Now, Spotify and Sirius XM each charge about $15. “All the company would have to do is raise prices 50% and the P/E ratio would fall to the low teens,” he argued. Anecdotally, those who subscribe to several of these services tend to value their Netflix subscription much higher despite its lower cost. Quantitatively, revenue-per-hour-watched suggests Netflix is about half the cost (subscription fees plus ad revenue) of other forms of video. Netflix probably could raise its price to at least $15 without losing many of its subscribers. For those reasons, Netflix is now in the Oakmark portfolio.

So, is Netflix hurting its shareholders by underpricing its product? We don’t think so. Like many network-effect businesses, scale is a large competitive advantage for content providers. Scale creates a nearly impenetrable moat for new entrants to cross. With more subscribers than any other video service, Netflix can pay more for programming and still achieve the lowest cost-per-subscriber. As shareholders of the company, we are perfectly amenable to Netflix’s decision to forfeit current income to rapidly increase scale.

Because we are value investors, when companies like Alphabet or Netflix show up in our portfolio, it raises eyebrows. Investors and advisors alike are full of questions when investors like us buy rapidly growing companies, or when growth investors buy companies with low P/Es. Portfolio managers generally don’t like to be questioned about their investment style purity, so they often avoid owning those stocks. We believe our portfolios benefit from owning stocks in the overlapping area between growth and value. Therefore, we welcome your questions about our purchases and are happy to discuss the shortcomings of using P/E ratio alone to define value.

Posted in Investing Gurus, Valuation Techniques

Tagged accounting, Nygren, Oakmark, valuation

Pitch the Perfect Investment, by two money managers who have also taught for many years at Columbia University’s Graduate Business School, can stop small caliber bullets or deflect a vicious sword blow with its heavy-gloss 496 color pages. Bad jokes aside, is the book worth the $30+ for its intended audience, young professionals seeking an investment career or can other readers gain investing insights?

FYI: I previously mentioned here Sept. 6th 2016, Pitch the Perfect Investment and Sept. 21, 2017 Pitch the Perfect Investment

Slide presentation:170926_Fordham_LC_final

The authors synthesized many academic publications for the reader to understand the subtleties behind concepts like the Wisdom of Crowds, market efficiency, behavioral finance, and risk into clearer language. This book with its colorful diagrams can help you grasp the theory of a discounted cash flow model or “DCF”; DCFs are used throughout the book because as the authors say, “all valuation is at the core a DCF, either explicitly or implicitly, whether they (analysts and portfolio managers) admit it or not.” Of course, it is a given that the young analyst can gain his or her own company and industry expertise so as to insert reasonable assumptions into the DCF model.

Investing is simple but not easy some say. This book provides the simple concepts in a colorful, insightful way, but you have to do the hard part—scratch out a variant perception while competing with many other professionals. Sobering.

The reader is taken through the basics of valuing an asset, a business, how to evaluate competitive advantage and value growth with simple examples (The Lemonade Stand). The authors drive home the importance of differentiating between nominal growth and profitable growth. Growth without competitive advantage earning a return above its cost of capital is useless or worse. Certainly, all investors must grasp those concepts. Every page is festooned with color cartoons, diagrams, tables and graphs. This is a visual text.

The most interesting part of the book for me was the Chapter 6, The Wisdom of Crowds. As Buffett says, “You must know two things as an investor: how to value a business, and how to think about prices.” If I can paraphrase correctly, the Wisdom of Crowds with an adequate amount of domain-specific knowledge and diverse views acting independently from each other on disseminated information will be a force to push price towards efficiency or intrinsic value. My respect for market efficiency and the person on the other side of the trade from me was reinforced. If you gain anything from this book, understand that earning an investment edge or variant perception is EXTREMELY difficult and rare. The authors may have intentionally driven home their point with their example of Cloverland Timber Company.

In their example, the analyst had the domain expertise to notice a line in the financial statement that the Cloverland was undercutting its forests, then satellite imagery was used to assess the quality of the asset and arrive at a more accurate valuation than the market’s current estimate. The information is available but not publicly disseminated. I wonder how many analysts/portfolio managers have the time, energy, money, or inclination to go this extra mile? If you are this able, then you deserve alpha. What are the implications?

If diverse individuals with independent thoughts are required to have the “Wisdom of Crowds” operate effectively, how will investment firms with their hordes of MBAs and CFAs all taught the same concepts, reading the same newspapers, magazine, research reports, and attending the same investment conferences arrive at non-consensus conclusions often–or ever?

The Wisdom of Crowds gives you an understanding of how prices are set under normal conditions when the forces of darkness and “Mr. Mayhem” (cartoon figure in the book using a magnet to pull prices away from market efficiency; he is the guy you need to spot quickly) are not strong enough to pull prices sufficiently away from intrinsic values. In other words, behavioral finance is complementary to efficient markets. One can then recognize when the Wisdom of Crowds becomes the Madness of Crowds. For an understanding of how prices are set by individuals in a free market, go to pages 79-185 in Man, Economy, and State by Murray Rothbard (Google: Man, Economy, and State.pdf) which has an analysis of how individuals set prices through direct exchange.

Another valuable chapter in the book is Chapter 9, How to Assess Risk. When investors confuse uncertainty (unknowns) with risk (losing money), then opportunity may appear.

Paul Sonkin, one of the authors, gives sobering advice to students who dream of becoming money managers. Page 151: “I’m not trying to discourage you from pursuing your dreams, but you should do it with your eyes open. Do it because you love analyzing companies, not to make a quick buck. And, if your goal is to outperform the market, keep in mind how difficult it has been in the past and the fact that it will only be more challenging in the future.” Those are true words. The investing profession may end up like acting. Only the crazy brave will pursue.

Once you have finished Section 1, The Perfect Investment, you then learn how to “Pitch” the Perfect Investment. Assuming you are diligent enough to acquire the information, assess risk, identify an actual mispricing, and know the catalyst, then convincing another of the merits of your investment should be the easy part. Unfortunately, too many do not provide a convincing case for the merits of their investment. An example, of a devastatingly compelling case: The truth shall set you free (liar, liar)

The authors lay out a framework below in this example:

Value or What Can I Make: Market price is $90 but the stock is worth $140—time horizon is less than 18 months.

Catalyst: Or Who else will figure this out: Activist with a good track record is pushing for a sale.

Mispricing: The activist did an independent appraisal which the market is unaware of showing a substantially higher value than the company appraisal. Also, the presence of the activist does not appear to be priced into the stock. The market is unaware of the activist or does not think he will be successful.

Downside: Limited. Timberland is a hard asset.

For another example of a forceful investment case with an implied catalyst: Other People’s Money Does Danny Devito provide a strong case? Does he show how much one can make, lose, what is the market missing, and the catalyst?

If you truly have a variant perception, then this is usually your reception: Michael Burry’s Variant Perception

And, only if you are right, and you make the decisions can you present this way: Michael Burry’s Investors If you read the book, The Big Short, ironically you know that Michael Burry was not making a macro bet, but on the impossibility of individual mortgage holders to make their mortgage payment when asset prices decline and/or interest rates reset higher.

An investment edge: There are only three ways to gain an edge

In summary, while I do not agree with the book-jacket blurb:

Mr. Nicholas Gallucio, CEO of Teton Advisors, who said, “In this era of hyper-competition on Wall Street ……even the smallest edge can make the difference between success and failure. Pitch the Perfect Investment will give the professional investor that edge.” I do believe the book is worth $30 for a beginning and intermediate investor who wants to refine their understanding of key investment concepts and to review how to make clear and convincing investment pitches. Even if an investor does not have a boss to pitch to, the investor should always write down a succinct investment case for each investment.

Remember, I’m biased. I’m a cheapie who went Dutch on his honeymoon, charged an entrance fee, and had a cash bar. Sure, I made a profit, but the divorce cost a fortune. Perhaps, I confused price with value.