I am having difficulty finding value, so now I gotta go small. More on micro-cap investing…..Liquidity as an Investing Style and Microcap_Investing and then More_on_Microcap_Investing. If you can accurately value a business while the company’s stock price is volatile, then you have a gold mine. Smaller companies tend to be more OVER and UNDER-VALUED than larger, well-known names.

Secrets and Lies of the Bailout

The federal rescue of Wall Street didn’t fix the economy – it created a permanent bailout state based on a Ponzi-like confidence scheme. And the worst may be yet to come

So what exactly did the bailout accomplish? It built a banking system that discriminates against community banks, makes Too Big to Fail banks even Too Bigger to Failier, increases risk, discourages sound business lending and punishes savings by making it even easier and more profitable to chase high-yield investments than to compete for small depositors. The bailout has also made lying on behalf of our biggest and most corrupt banks the official policy of the United States government. And if any one of those banks fails, it will cause another financial crisis, meaning we’re essentially wedded to that policy for the rest of eternity – or at least until the markets call our bluff, which could happen any minute now.

An excellent article that shows what has happened to our centrally-controlled, socialist, Ponzi financial system. Of course, the author does not point out the causes or remedies, but he does show the results of the bailout.

My favorite line:

We thought we were just letting a friend crash at the house for a few days; we ended up with a family of hillbillies who moved in forever, sleeping nine to a bed and building a meth lab on the front lawn.

Economic theory demonstrates that only governmental inflation can generate a boom and bust cycle, and that the depression will be prolonged and aggravated by inflationist and other interventionary measures. In contrast to the myth of laissez-faire, we have shown how government intervention generate the unsound boom of the 1920s, and how Hoover’s new departure aggravated the Great Depression by massive measures of interference. The guilt for the Great Depression must, at long last, be lifted from the shoulders of the free market economy, and placed where it properly belongs: at the doors of politicians, bureaucrats, and the mass of “enlightened” economists. And in any other depression, past or future. the story will be the same. (Rothbard, America’s Great Depression p. 295)

Is Sears the Next Berkshire Hathaway?

A good article about not overpaying for assets.

It’s fair to blame Lampert for making what was, in effect, a major real estate investment near the peak of the biggest real estate bubble in American history. But investors frustrated by watching the share price fall by more than 80 percent from its 2007 highs have no one to blame but themselves. Anyone who bought Sears when it traded for nearly $200 per share clearly didn’t do their homework. They instead were hoping to ride Lampert’s coattails while somehow ignoring the value investor’s core principle of maintaining safety by not overpaying for assets.

I abhor guns of any kind and think it is outrageous that Americans should want the right to defend themselves. How dare this woman seek to carry a gun. Doesn’t everyone know that the government will protect us.

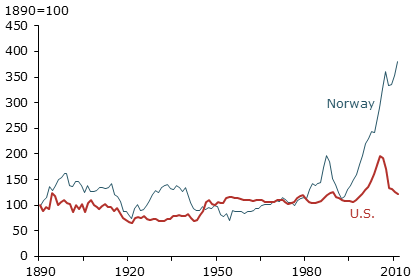

The Oslo Housing Bubble Syndrome

Mises Daily: Monday, January 07, 2013 by Mark Thornton (An important market to track in our study of booms and busts.)

The Stockholm syndrome is a psychological phenomenon whereby hostages develop irrational sympathy toward their captors even to the point of defending their captors in subsequent investigations and criminal trials. While this applies to individuals or small groups, the Oslo syndrome applies to whole national populations.

In The Oslo Syndrome: Delusions of a People under Siege (Smith and Kraus Global, 2005), Kenneth Levin describes a “psychological response common among chronically besieged populations, whether minorities subjected to defamation, discrimination and assault or small nations under persistent attack by their neighbors. People living under such stressful conditions often choose to accept at face value the indictments of their accusers in the hope of thereby escaping their predicament.”[1]

Actually, the Oslo syndrome applies to all people living in socialist states. The state tells people what to do, forces people into public schools to be indoctrinated, tells people what we can and cannot consume, uses police power, and punishes people who do not do what they are told, and throws people into prisons if they continue to live the way they choose. The state’s system leads most to just accept things as they are as if it were the only possible way of life. Given that the Oslo syndrome applies to an entire nation, and that Norway is living through what will hopefully be the final housing bubble of this cycle, I thought it appropriate to dub the psychological phenomenon associated with housing bubbles, the “Oslo housing bubble syndrome.” This psychological phenomenon is the “irrational” response of people living in a bubble economy. They ignore or dismiss signs of a bubble and instead attribute their good luck (i.e. higher home prices) to “fundamental factors” that appear to substantiate high prices in real estate or stocks.

Do not get me wrong. The business cycle is not a psychological phenomenon. However, it does impact mass psychology. If a central bank is intent on expanding the money supply with an easy money policy, then some bankers are going to make additional loans and seek out new clients to lend money to. The bankers will be rewarded and their clients will be happy. As the boom plays out, people make big gains and are euphoric and even manic. The boom eventually turns to bust. Many of the same people who were making big gains are now seeing their profits turn into losses, or even foreclosures or bankruptcies. As a result, they become depressed.

The reason that booms turn into busts is that the artificial expansion of credit leads entrepreneurs to embark on many new investment projects that expand the structure of production. The new investment projects eventually cause new constraints to develop. These new developments could not be anticipated by entrepreneurs as a whole.

First, all of these new investment projects place strains on the availability of resources and inputs. Therefore their costs are greater than they anticipated. For example, the price of oil and the wages of specialized labor increase as the bubble proceeds to the peak. Second, as the prices of things like food, energy, and other products with inelastic demand rises, customers have less income available to buy their products. Third, as more of these new investment projects come online and start supplying their products, they are faced with increased competition, again more than they could have anticipated. The result is that their investment projects are now faced with higher costs, fewer customers, and more competitors. This is a recipe for disaster that results in the realization of a cluster of entrepreneurial errors.

If your nation’s economy has not had a bubble in many years it is not surprising that people are shocked when the bubble bursts. However, Norwegians have surely noticed what has happened in the US and PIGS, or even closer to home, in Ireland, the UK, and Iceland. Despite what they have seen there are still those who claim that Norwegian housing prices are genuine. Norwegians have, in a sense, been “psychologically conditioned,” and, as with the Stockholm and Oslo syndromes, are doing precisely the opposite of what they should be doing. A similar phenomenon happened in the US, around 2005, when people were often heard to be saying that “housing prices never go down,” or that “you can’t lose money by investing in real estate.”

There appear to be housing bubbles across Europe with the exception of the PIIIGS (Portugal, Iceland, Ireland, Italy, Greece, and Spain), but the Norwegian bubble seems to be the strongest one. The chart below shows that housing prices in Norway have increased by nearly 300% in the last twenty years.

Sources: Shiller (2005) and Eitrheim and Erlandsen (2004, 2005).

The US has many fundamental flaws in its economy including a large government budget deficit, a large trade deficit, expanding national debt, and exploding, unfunded financial liabilities related to health care and retirees. In contrast, Norway has none of these problems and several factors that suggest that the Norwegian economy is fundamentally sound. It has a large trade surplus and government budget surplus (both have been averaging around 14% of GDP) due to substantial oil revenues that are also building a very large sovereign wealth fund. The fund is approaching $700 billion dollars (Norway’s population is approximately 5 million).

The unemployment rate in Norway has been averaging around 3% which would be considered well below the “natural unemployment rate” in the US (thought to be around 6%). Therefore, Norway has one of the best unemployment rates in its region, in Europe, and even globally. The C.P.I. measure of price inflation in Norway has been around 1%, again one of the best in the world. Real G.D.P. growth has been about 3% and is expected to continue on that path into the future. This growth rate would be consistent with full employment. It is almost too good to be true.

So the fundamental picture does support the impression that housing prices are real. Another factor that supports a “fundamental” view of housing prices is that Oslo, the capital city with almost 1/5th of the nation’s population, has land-use restrictions that keep much land unavailable for construction. This is the same fundamental case that was given for the severe housing bubble in Las Vegas: the government prevented land from being developed. Housing prices in Oslo, however, have not risen much more than the average increase. The largest increases have occurred in areas associated with the oil and oil exploration business.

We cannot know for certain that Norway is experiencing a bubble. However the reasons we suspect a bubble starts with their economy. Norway’s rosy economy is not the result of good policy, but of oil revenues that subsidize their socialist government. Norway ranks 40th on the Freedom Index, below Belgium (38) and Armenia (39), and only above countries like El Salvador (41) and Peru (42). A steep drop in oil prices would be a severe blow to their economy. However, as oil revenues are continuing to pour into the government budget and sovereign wealth fund, it makes the Norwegian economy look like a good bet.

That image is particularly compelling compared to other economies across the globe. All the world’s major economies (i.e., the US, EU, China, and Japan) appear to be tottering on the verge of disaster. Currencies seem to be particularly dangerous given the Bernanke regime of “coordinated” quantitative easing by central banks. The euro is considered most at risk because of a potential uncoordinated currency break up. This threat has resulted in a decreased demand for the euro and an increased demand for alternative currencies from safe countries, such as the Swiss franc and the Norwegian krone.

Instead of allowing the krone to increase in value with this increase in demand, the Norwegian central bank, the Norges Bank, has instead countered with an increase of supply. They have intentionally set interest rates artificial low. The overnight deposit rate has been set at 1.5 percent since last December. They are trying to prevent the krone from appreciating in value, but their efforts have not been completely successful. Preventing this appreciation of the krone is intended to protect exporters, including their national oil company. However, it also helps pump up the housing bubble.

Monetary inflation, as measured by Norway’s M2 measure of the money supply, has lately been running at 8%. During the economic crisis, circa 2007, it ran as high as 20%. From 2008 to the present monetary inflation has averaged about 7.5%.[2]

The result is that Norway is experiencing low price inflation, except in housing and there is still upward pressure on the value of the krone. With central banks around the globe setting interest rates outrageously low it makes it difficult for the Norges Bank to act to raise rates. Higher interest rates would help deflate the housing bubble, but they have failed to implement such a policy.[3] With central bankers embarking on an inflationary death march, the Norges Bank has found itself seemingly trapped into following their policy of ultra low interest rates and monetary inflation.

This is incongruous given that the Norway chose to keep its monetary independence and stay out of the euro zone. It is also unnecessary because the Norges Bank has a policy option.

If the central bank did act and raised interest rates and simply allowed their currency to float, the krone would appreciate and Norwegian savers would get a windfall as the value of their savings increased. This would encourage them to work more, save more, and become wealthy. Every krone would buy more goods from around the world and would buy even more goods tomorrow than today. This appreciation would indeed hurt exporters, such as oil and cheese exporters, but most importantly it would stop and reverse the housing bubble before things get even worse and more distorted.

As usual, with policy decisions it is a matter of making a people wealthier or making a people poorer. In the case of the Oslo housing bubble syndrome, it looks like poorer will win out again.

…..So Ackman vs. Herbalife has no heroes. Both parties, in their own way, take advantage of the goodwill and trust that underlie capitalism. Herbalife recruits sales people with the knowledge–based on mathematical certainty but undisclosed to its recruits–that the vast majority will lose money. Mr. Ackman, for his part, has gotten rich betting against bad companies. One party is possibly immoral, the other party at best amoral. Who do you cheer for? –Mr. Karlgaard, publisher of Forbes (A Short Seller Takes on a Vitamin Vendor, WSJ Jan 4, 2013)

Yes this battle will be gruesome, bloody and long (perhaps) but our purpose is to understand whether Herbalife which–as of the last filing–sported franchise-like financials of high ROA, ROE and ROIC with growing sales. Copious cash flow. On the surface, the company seems to have a franchise. Why can’t other companies do the same thing. What barriers to entry are there? Product patents, customer captivity, economies of scale and scope, network effects, etc. This battle will allow us to understand what drove Herbalife’s success. Will it be fleeting or lasting. My bet is that Herbalife does NOT have a lasting competitive advantage.

The quote above by Mr. Karlgaard is disappointing because as a publisher of a business magazine, he should understand Mr. Ackman’s purpose. A good investor should invest in companies that will use owner’s capital wisely and should not invest or even warn against investing in companies that mis-allocate capital for the long-term. Short sellers are just as important as having a Warren Buffett in the market. An Ackman does more for future growth than any government program because–like him or not–Mr. Ackman is trying to take capital away from poorly managed, potential frauds, unsustainable businesses while allocating capital to companies that will use his investors’ capital beneficially. He may be proven wrong but that is for the market to decide.

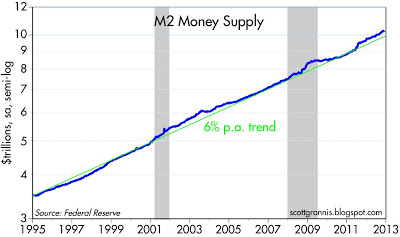

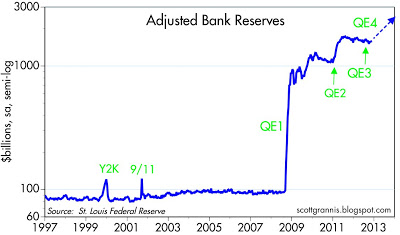

UPDATE: MONEY SUPPLY EXPLOSION--We are now officially in double digit territory for non-seasonally adjusted 13 week annualized money supply (M2) growth. Here is the amazing ascent in growth over recent weeks: 5.1%, 5.6%, 6.6%, 7.1%, 7.5%, 7.8%, 8.2%, 8.4%, 8.7%, 9.0%, 9.3%, 9.6%, 9.9%, 10.7%. It is this growth that is going to fuel the U.S. economy, the U.S. stock market and commodities. www.economicpolicyjournal.com

Investing in Banks

I find investing in global banks like Bank of America or Citibank impossible because I have no way to value or understand their businesses. How much “shadow” banking do these entities engage in? I don’t want to find out the hard way. See the article below

Some four years after the 2008 financial crisis, public trust in banks is as low as ever. Sophisticated investors describe big banks as “black boxes” that may still be concealing enormous risks—the sort that could again take down the economy. A close investigation of a supposedly conservative bank’s financial records uncovers the reason for these fears—and points the way toward urgent reforms.

The financial crisis had many causes—too much borrowing, foolish investments, misguided regulation—but at its core, the panic resulted from a lack of transparency. The reason no one wanted to lend to or trade with the banks during the fall of 2008, when Lehman Brothers collapsed, was that no one could understand the banks’ risks. It was impossible to tell, from looking at a particular bank’s disclosures, whether it might suddenly implode. Red the whole article:

The authors of the above article don’t grasp the true cause of the banking panic. Yes, transparency is a problem, but that would ALWAYS be true under our current fractional reserve banking system–it’s inherently a Ponzi scheme that functions on public gullibility and government edict–banks get to violate private property rights.

PS: can anyone fill in the blanks? All panics arise from excess _______ over and above ___________. Correct answer wins this prize:

This was published on January 2, 2013, in Ron Paul’s Monetary Policy Anthology: Materials From the Chairmanship of the Subcommittee on Domestic Monetary Policy and Technology, US House of Representatives, 112th Congress. All the books mentioned in this article are free on the web, go to www.mises.org and do a book search by title.

The scholarly contributions of Murray N. Rothbard span numerous disciplines, and may be found in dozens of books and thousands of articles. But even if we confine ourselves to the topic of money, the subject of this volume, we still find his contributions copious and significant.

As an American monetary historian Rothbard traced the party politics, the pressure groups, and the academic apologists behind the various national banking schemes throughout American history. As a popularizer of monetary theory and history he showed the public what government was really up to as it took greater and greater control over money. As a business cycle expert he wrote scholarly books on the Panic of 1819 and the Great Depression, finding the roots of both in artificial credit expansion. And while the locus classicus of monetary theory in the tradition of the Austrian School is Ludwig von Mises’ 1912 work The Theory of Money and Credit, the most thorough shorter overview of Austrian monetary theory is surely chapter 10 of Rothbard’s treatise Man, Economy and State.

Rothbard placed great emphasis on the central monetary insight of classical economics, namely that the quantity of money is unimportant to economic progress. There is no need for the money supply to be artificially expanded in order to keep pace with population, economic growth, or any other factor. As long as prices are free to fluctuate, changes in the purchasing power of money can accommodate increases in production, increases in money demand, changes in population, or whatever. If production increases, for example, prices simply fall, and the same amount of money can now facilitate an increased number of transactions commensurate with the greater abundance of goods. Any attempt by “monetary policy” to keep prices from falling, to accommodate an increase in the demand for money, or to establish “price stability,” will yield only instability, entrepreneurial confusion, and the boom-bust cycle. There is no way for central bank policy or any form of artificial credit expansion to improve upon the micro-level adjustments that take place at every moment in the market.

With the exception of the Austrian School of economics, to which Rothbard made so many important contributions throughout his career, professional economists have treated money as a good that must be produced by a monopoly – either the government itself or its authorized central bank. Rothbard, on the other hand, teaches that money is a commodity (albeit one with unique attributes) that can be produced without government involvement. Rothbard’s history of money, in fact, is a history of small steps, the importance of which are often appreciated only in hindsight, by which government insinuated its way into the business of money production.

It was Carl Menger who demonstrated how money could emerge on the free market, and Ludwig von Mises who demonstrated that it had to emerge that way. In this as in so many other areas, Mises broke with the reigning orthodoxy, which in this case held that money was a creation of the state and held its value because of the state’s seal of approval. A corollary of the Austrian view was that fiat paper money could not simply be created ex nihilo by the state and imposed on the public. The fiat paper we use today would have to come about in some other way.

It was one of Rothbard’s great contributions to show, in his classic What Has Government Done to Our Money? and elsewhere, the precise steps by which the fiat money in use throughout the world came into existence. First, a commodity money (for convenience, let’s suppose gold) comes into existence on the market, without central direction, simply because people recognize that the use of a highly valued good as a medium of exchange, as opposed to persisting in barter, will make it easier for them to facilitate their transactions. Second, money substitutes began to be issued, and circulate instead of the gold itself. This satisfies the desires of many people for convenience. They would rather carry paper, redeemable into gold, than the gold itself. Finally, government calls in the gold that backs the paper, keeps the gold, and leaves the people with paper money redeemable into nothing. These steps, in turn, were preceded by the seemingly minor – but in retrospect portentous indeed – government interventions of monopolizing the mint, establishing national names for the money in a particular country (dollars, francs, etc.), and imposing legal tender laws.

Rothbard also brought the Austrian theory of the business cycle to a popular audience. Joseph Salerno, who has been called the best monetary economist working in the Austrian tradition today, was first drawn to the Austrian School by Rothbard’s essay “Economic Depressions: Their Cause and Cure.” There Rothbard laid out the problems that business cycle theory needed to solve. In particular, any theory of the cycle needed to account, first, for why entrepreneurs should make similar errors in a cluster, when these entrepreneurs have been chosen by the market for their skill at forecasting consumer demand. If these are the entrepreneurs who have done the best job of anticipating consumer demand in the past, why should they suddenly do such a poor job, and all at once? And why should these errors be especially clustered in the capital-goods sectors of the economy?

According to Rothbard, competing theories could not answer either of these questions satisfactorily. Certainly any theory that tried to blame the bust on a sudden fall in consumer spending could not explain why consumer-goods industries, as an empirical fact, tended to perform relatively better than capital-goods industries.

Only the Austrian theory of the business cycle adequately accounted for the phenomena we observe during the boom and bust. The cause of the entrepreneurial confusion, according to the Austrians, is the white noise the Federal Reserve introduces into the system by its manipulation of interest rates, which it accomplishes by injecting newly created money into the banking system. The artificially low rates mislead entrepreneurs into a different pattern of production than would have occurred otherwise. This structure of production is not what the free market and its price system would have led entrepreneurs to erect, and it would be sustainable only if the public were willing to defer consumption and provide investment capital to a greater degree than they actually are. With the passage of time this mismatch between consumer wants and the existing structure of production becomes evident, massive losses are suffered, and the process of reallocating resources into a sustainable pattern in the service of consumer demand commences. This latter process is the bust, which is actually the beginning of the economy’s restoration to health.

The concentration of losses in the capital-goods sector can be explained by the same factor: the artificially low-interest rates brought about by the Fed’s intervention into the economy. What Austrians call the higher-order stages of production, the stages farthest removed from finished consumer goods, are more interest-rate sensitive, and will therefore be given disproportionate stimulus by the Fed’s policy of lowering interest rates.

Equipped with this theory, Rothbard wrote America’s Great Depression(1963). There Rothbard did two things. First, he showed that the Great Depression had not been the fault of “unregulated capitalism.” After explaining the Austrian theory of the business cycle and showing why it was superior to rival accounts, Rothbard went on to apply it to the most devastating event in U.S. economic history. In the first part of his exposition, Rothbard focused on showing the extent of the inflation during the 1920s, pointing out that the relatively flat consumer price level was misleading: given the explosion in productivity during the roaring ’20s, prices should have been falling. He also pointed out how bloated the capital-goods sector became vis-a-vis consumer goods production. In other words, the ingredients and characteristics of the Austrian business cycle theory were very much present in the years leading up to the Depression.

Second, Rothbard showed that the persistence of the Depression was attributable to government policy. Herbert Hoover, far from a supporter of laissez-faire, had sought to prop up wages during a business depression, spent huge sums on public works, bailed out banks and railroads, increased the government’s role in agriculture, impaired the international division of labor via the Smoot-Hawley Tariff, attacked short sellers, and raised taxes, to mention just a portion of the Hoover program.

Rothbard had been interested in business cycles since his days as a graduate student. He had intended to work on a history of American business cycles for his Ph.D. dissertation under Joseph Dorfman at Columbia University, but he found out that the first major cycle in American history, the Panic of 1819, provided ample material for study in itself. That dissertation eventually appeared as a book, via Columbia University Press, called The Panic of 1819: Reactions and Policies (1962). In that book, which the scholarly journals have declared to be the definitive study, Rothbard found that a great many contemporaries identified the Bank of the United States – which was supposed to be a source of stability – as the primary culprit in that period of boom and bust. American statesmen who had once favored such banks, and who thought paper money inflation could be a source of economic progress, converted to hard money on the spot, and proposals for 100-percent specie banking proliferated.

In A History of Money and Banking: The Colonial Era to World War II, a collection of Rothbard’s historical writings published after the author’s death, Rothbard traced the history of money in the United States and came up with some unconventional findings. The most stable period of the nineteenth century from a monetary standpoint turns out to be the period of the Independent Treasury, the time when the banking system was burdened with the least government involvement. What’s more, the various economic cycles of the nineteenth century were consistently tied to artificial credit expansion, either participated in or connived at by government and its privileged banks. Rothbard further showed that the traditional tale of the 1870s, when the United States was supposed to have been in the middle of the “Long Depression,” was all wrong. This was actually a period of great prosperity, Rothbard said. Years later, economic historians have since concluded that Rothbard’s position had been the correct one.

Rothbard’s treatment of the Federal Reserve System itself, which he dealt with in numerous other works, involved the same kind of analysis that historians like Gabriel Kolko and Robert Wiebe applied to other fruits of the Progressive Era. The conventional wisdom, as conveyed in the textbooks, is that the Progressives were enlightened intellectuals who sought to employ the federal regulatory apparatus in the service of the public good. The wicked, grasping private sector was to be brought to heel at last by these advocates of social justice.

New Left revisionists demonstrated that this version of the Progressive Era was nothing but a caricature. The dominant theme in Progressive thought was expert control over various aspects of society and the economy. The Progressives were not populists. They placed their confidence in a technocratic elite administering federal agencies removed from regular public oversight. What’s more, the resulting regulatory apparatus tended to favor the dominant firms in the market, which is why the forces of big business were in sympathy with, rather than irreconcilably opposed to, the Progressive program. “With such powerful interests as the Morgans, the Rockefellers, and Kuhn, Loeb in basic agreement on a new central bank,” Rothbard wrote, “who could prevail against it?”

It is with these insights in mind that Rothbard scrutinized the Federal Reserve. He would have none of the idea that the Fed was the creation of far-seeing public officials who sought to subject the banking system to wise regulation for the sake of the people’s well-being. The Fed was created not to punish the banking system, but to make its fractional-reserve lending operate more smoothly. In The Case Against the Fed, What Has Government Done to Our Money?, and The Mystery of Banking, Rothbard took the reader through the step-by-step process by which the banks engaged in credit expansion, earning a return by lending money created out of thin air. Without a central bank to coordinate this process, Rothbard showed, the banks’ position was precarious. If one bank inflated more than others, those others would seek to redeem those notes for specie and the issuing bank would be unable to honor all the redemption claims coming in.

The primary purpose of the central bank, therefore, in addition to propping up the banks through its various liquidity injections and its position as the lender of last resort, is to coordinate the inflationary process. When faced with the creation of new money by the Fed, the banks will inflate on top of this new money at the same rate (as determined by the Fed’s reserve requirement for banks). Therefore, the various redemptions will tend, on net, to cancel each other out. This is what Rothbard meant when he said the central bank made it possible to “inflate the currency in a smooth, controlled, and uniform manner throughout the nation.”

Although Rothbard distinguished himself as a monetary theorist and as a monetary historian, he did not confine himself to theory or history. He devoted plenty of attention to the here and now – to critiques of Federal Reserve policy, for example, or to criticisms of government responses to the various fiascoes, the Savings and Loan bailout among them, to which our financial system is especially prone. He likewise looked beyond the present system to a regime of sound money, and in The Case for a 100 Percent Gold Dollar and The Mystery of Banking laid out a practical, step-by-step plan to get there from here.

In his work on monetary theory and history, as in his work in so many other areas, Rothbard showed from both an economic and a moral point of view why a system of liberty was preferable to a system of government control. At a time when the political class and the banking establishment are being subjected to more scrutiny than ever, the message of Rothbard takes on a special urgency.

For that reason we should all be grateful that his monetary work, and that of the other great Austrian economists, is being carried on by Murray Rothbard’s friend and colleague Ron Paul. By my reckoning, no one in history has brought true monetary theory and history to a larger audience.

Only a sudden, improbable drop in society’s rate of time preference (read: real interest rate) would allow stock-market indexes, in the absence of credit expansion, to jump to a new, consolidated level, from which point, at most, slow gradual stock-market growth could take place. Thus continuously prolonged stock-market booms and euphoria are invariably artificial and fed by credit expansion. Moreover such episodes of euphoria encourage the public to postpone consumption for the short-term and invest cash balances in the stock market. Therefore while expectations of stock-market booms fed by credit expansion last, the crisis and recession can be temporarily postponed. This is what happened at the end of the 1990s, before the severe stock-market adjustment of 2000-2001…..Therefore–and this is the most important conclusion–uninterrupted stock market growth NEVER indicates favorable economic conditions. Quite the contrary: all such growth provides the most unmistakable sign of credit expansion, un-backed by real savings, expansion which feeds an artificial boom that will invariably culminate in a severe stock market crisis. Source: The Stock Market, Credit and Capital Formation by Machlup

Reader’s Question on Adjusted PEs

I would like your opinion on an original (?) issue I have with the Shiller PE10 index. I wrote a blog post on that subject (and I merely did it to get feedback):

I had seen too many Shiller PE10 indices, and investment decisions which depend on it (last one being the GMO Capital “13th Labour of Hercules” White Paper). Found here: JM_13thLabourofHercules_11122 (1)

In a nutshell: P/E10 is used where the denominator is inflated by official CPI-U, which has changed definition over time, with a wide convergence compared to the inflation indicated by a historic (1980, 1990) CPI-U index definition.

If you recalculate the Shiller PE10 with earnings inflated with “real inflation” (which I did in my post), you get 17 instead of 22 for today (roughly).

John Chew’s reply: I applaud your efforts to correct a distortion but any government aggregate is flawed. See article on the CPI below. Your adjustment may be less flawed but still you may not have a worthwhile tool/indicator. I mostly focus on individual companies and disregard discussions on market P/E. First the P is distorted by the FED and the Earnings are distorted by GAAP accounting. I would rather spend time on understanding the quotation (under the cartoon) on the stock market.

One thing that has achieved Holy Writ with economists and politicians is the Consumer Price Index, or the CPI. Each month, people from Alan Greenspan to traders at the New York Stock Exchange to the economist in the Economics 101 prison await the latest announcement from the US Department of Labor that tells us the change in “consumer prices” from the previous month.

Many folks make very important decisions after hearing this number, since it supposedly measures the “rate of inflation.” If the change in the price index is “too high,” then the Federal Reserve Board of Governors might vote to increase the Fed’s discount rate. Likewise, high numbers will also trigger a giant sale of stocks on Wall Street, as traders anticipate higher interest rates, which both eat into profits and provide safer avenues of investment through interest-bearing securities.

Economists depend upon the CPI when taking time-series measurements of financial instruments, since such measurements can only sense if they are expressed in “constant” money terms. For example, the 11,000-point Dow Jones Industrial Average of today is not 11 times the value of the 1,000-point Dow of 1969 because the relative value of the US dollar has declined by about fourfold in the past three decades, according to the CPI.

Given that the US government has made war on money for most of the past century, one cannot blame those who make a living from financial instruments to want a consistent measure of value over time. Like most products coming from the bowels of government offices, however, the CPI should be tagged with warning labels. Furthermore, one should remember that economists and politicians often use the CPI dishonestly.

The first thing to keep in mind is that the CPI is not an economic variable. It is a statistic that at best gives an inaccurate picture of an economic phenomenon: inflation. To calculate the monthly CPI, the USDepartment of Labor takes a weighted average of prices of various things that consumers purchase, and then its statisticians try to figure out the various proportions of different items in a “mythical” household budget. For example, the statisticians may hold that housing costs are 30 percent of household expenditures, food costs 20 percent, gasoline another 15 percent, and so on.

Armed with the proportional spending of the “average” household, the statisticians then assign that percentage to price changes of each item. Obviously, the higher the percentage of a household budget for a certain item, the more “influential” that item may be. For example, if gasoline prices rise sharply, then those particular price increases are seen as “fueling inflation” (no pun intended).

It is easy for the observer to see that the CPI can perpetuate the myth of “cost-push” inflation, in which the cause of rising prices is, well, rising prices. Indeed, many evening news broadcasts on the new CPI figures will begin with something like, “Increases in gasoline prices have helped ignite a new round of inflation, the Labor Department reported today.”

Furthermore, the portrayal of the “official” version of inflation as an average causes other mischief as well, the most noticeable being the classification of the prices of some goods and services as “rising faster than the rate of inflation.” The implication of such a statement is that if the price of something increases at a faster rate than the increase in the CPI, then something illegitimate must be occurring. Soon afterward, politicians begin to call for price controls, and then the real damage to the economy begins.

As economists and others of the Austrian School understand, inflation occurs when the value of money declines relative to the goods and services it can purchase. In other words, inflation is a monetary phenomenon, not a price phenomenon. Prices go up because inflation is happening, not the other way around.

During a period of inflation, prices of some things increase more rapidly than prices of others. For example, during the last decade, money prices of gasoline and food have increased, while personal computer prices have fallen. That does not mean computers are impervious to inflation, but rather that inflation affects different items in different ways. Furthermore, without inflation, computer prices would have fallen even further.

What, then, is the real rate of inflation if the CPI is inaccurate? The truth is that there is no good way to gain a true measure of inflation, especially in this era when the Federal Reserve System is flooding the economy with new dollars. All we can say for certain is that inflation, with all its evils and distortions, has become what seems to be a permanent part of our economy.

___________________________

William L. Anderson, adjunct scholar of the Mises Institute, teaches economics at Frostburg State University (anderwl@ prodigy.net).

The author of this blog when he lived with cannibals in Irian Jaya (Western Papua New Guinea). How this picture came to be is a long, long story told over several beers. I urge readers to think of these skulls as representing investors who did NOT read the proxies and financial footnotes of the companies they bought. Be careful and always think for yourself. Please! A moment of silence for the many who did not survive. More on cannibals here: http://www.smithsonianmag.com/travel/cannibals.html.

Bernanke’s money printing is certainly having his intended effect in the stock market today. The joys and inevitable sorrows of manipulation. Eventually, the Fed will have to stop having its foot on the monetary gas pedal. This blog has been updating you on the 8% to 9% money growth and you are all aware of the current negative real interest rates ( a war on savers).

Irrational Behavior

Don’t forget to improve by signing up for A Beginner’s Guide to Irrational Behavior (Dan Ariely). “In this course we will learn about some of the many ways in which people behave in less than rational ways, and how we might overcome these problems.” https://www.coursera.org/course/behavioralecon

A Special Situation

A Leveraged Stub Stock Remember to do your own work and if you invest, size your position accordingly in a company that could either pay down debt and turnaround or be crushed by debt. The author of the blog below addresses many of the issues that need to be thought about. One key is to look carefully at maintenance capital expenditures (“MCX”) because if management skimps on MCX to pay down debt, then the company really is in liquidation and the asset values may not be there to support the turnaround. You can learn as much about investing/companies that you analyze and pass on as the ones you invest in. You just need to keep track of your omissions and see if your thought process was correct. I bet you 10 to 1 that not 1 in 100 professional money managers do that on a systematic basis. What a chance to learn, but you have to be diligent.

Debate about the efficacy of the Austrian Business Cycle

This debate is somewhat similar to the debate of efficient market theory. How can entrepreneurs be fooled time and time again by the Fed’s market manipulations that consistently lead to booms and busts. What about rationality?

Solution to Earnings Quality Case Study (Manufactured Housing)

The case was introduced here:http://wp.me/p2OaYY-1y8. Try it now if you haven’t. What jumps out at you? Red flags should be flying when you read the chilling lines (at the bottom of this post so as to not give you the answer now.)

Don’t ever let school interfere with your education.~ Mark Twain

Education is an ongoing confrontation between those who want to help children learn how tothink, and those who want to teach them what to think. While there are numerous variations on these themes, the contrast can most clearly be found in the distinctions between child-centered Montessori systems, and teacher- and test-centered schools. Government schools usually fall into the latter category. Homeschooling, religious schools, un-schooling, and other forms tend to emphasize either the “how” or the “what” in their efforts with children.

Those who focus on learning how to think have in mind helping children develop their own methods of questioning and analyzing the world around them; to control their own inquiries and opinions; to the end of helping children become independent, self-directed persons. The role of the teacher in such a setting is to provide new learning situations (e.g., open up new subjects of inquiry when the student is ready to do so) and to facilitate the processes of questioning so as to help the students get to deeper levels of understanding.

People who have developed the capacity for epistemological independence are not easy to control for purposes that do not serve their interests. Institutions – which have purposes of their own that transcend those of individuals – require a mass-minded population that has been conditioned to accept outer-imposed definitions of “reality.” Any deviation from this systemic purpose – as would derive from students questioning how the arrangement would benefit them – would be fatal to all forms of institutionalism.

The established order has, from one culture and time period to another, insisted on educational systems that train young minds into what to think. “Truth” becomes a set of beliefs that conform to an institutional imperative, and it becomes the purpose of schools to inculcate such a mindset. Whereas “how to think” learning that finds its purpose and focus within theminds of self-directed, independent students, “what to think” education derives from outside the students’ experiences and analytical skills. As Ivan Illich so perceptively expressed it, “[s]chool is the advertising agency which makes you believe that you need the society as it is.”

To this end, the established order has helped generate – with eager assistance from academia – a belief that all understanding is a quality requiring phalanxes of self-styled “experts” who, by virtue of their prescribed status, enjoy monopolies to offer opinions about their respective fields of study. Plato’s designation of “philosopher kings” has been sub-franchised into categories of “experts” to be found in “history,” “physics,” “psychology,” “economics,” “law,” and seemingly endless sub-groupings that negate the role once respected for those who had received a “liberal arts” education.

Entry into the sanctum sanctorum of the upper floors of this pyramidal high-rise is determined by a process of certification usually reflected in a graduate school degree provided by those already recognized. Of course, given the logic of any vertically-structured system, there is a hierarchy of certifying agencies, wherein Ivy League universities are presumed more capable of identifying and recognizing expert genius, than would Boll Weevil State University. Nor is tolerance exhibited toward any interloper who might dare to offer an opinion outside his or her area of certification. (When my book, In Restraint of Trade was first published some fifteen years ago, one reviewer – from a history department at a highly-respected university – spent the bulk of his time criticizing not the substance of my book, but the fact that I taught in a law school!)

The assumption is often expressed that, in a complicated world we must rely on “experts” to navigate through the turbulence and uncertainties that abound. But the study of “chaos” and “complexity” challenge this thinking, reminding us that complex systems produce unpredictable outcomes; that the most effective action occurs when decision-making is decentralized closest to the source of such turbulence. In a world currently being destroyed by centralized state systems of “economic planning,” “military planning,” misnomered “intelligence agencies,” “health-care planning,” among others, it is increasingly evident to people that the certified “experts” tend to supply answers to problems that their epistemological arrogance has helped to generate.

Systems premised upon outer- rather than inner-directed learning – training students what to think rather than how to think – turn children’s minds into so much “mush” as to deplete their inherent creative energies. People become neutralized by a system that trains them to accept the inadequacy of their own minds to make empirical and analytical judgments about the world. The outer-directed approach, in which “truth” is presumed to be found within the opinions of the certified intelligentsia, is self-sustaining as long as students’ minds remain in the default mode. Expertism is a circular process that makes it difficult for people to break the circle unless they have a sufficiently independent mind.

The method of learning I have found essential for encouraging the inner-directed (i.e., how to think) approach is found in the use of the Socratic method, which used to be used in most law schools. My all-time favorite professor was Malcolm Sharp, a law professor at the University of Chicago, one of the loveliest persons I have ever known; but who frustrated most of his students with his insistence on getting us to keep refining the quality of our questions. This was done through an ever-deepening level of inquiry encouraged by the creative us of the word “why?”

To the proposition “government is necessary in order to protect the lives, property, and liberty of people” the following questions could be asked: “how is property being protected if the state must forcibly take property from people (taxation) in order to support its activities?” “Can liberty be protected if the state can compel people to act – or refrain from acting – in ways contrary to how they would otherwise choose to behave?” “How can lives be protected if the state is able to engage in deadly wars?” “If the war system generates restrictions on human action, including the forced conscription of people as soldiers, how is individual liberty being defended?” “If it is our purpose to protect the lives, liberty, and property of people, can such ends be served by a system that regularly contradicts such ends? Are there alternative ways to accomplish such purposes?” As each question is asked, the response might generate additional sub-questions to be explored (e.g., is it possible to support a system through voluntary payments? Is the marketplace an example of accomplishing these ends without violating them in the process?)

Most of my students experience frustration over my methods of providing them with cases and materials, and then playing around with hypotheticals – and the factual modification of hypotheticals – to explore the ramification of case holdings and rules of law. “I came to law school to get answers, one student raged, and all you’re giving me is more questions!” “How do you propose to deal with legal questions once you are in practice?” I asked him. “And if you think I am such a fount of understanding, how do you think I got that way; and do you think you might be able to develop such a skill?” It is encouraging to find some students who grasp, at the outset, that their success in the classroom and as lawyers depends upon this process of learning how to think. I often receive favorable responses from students years later. I had one student tell me “when I was a student of yours, I hated your guts. Now that I’ve been out in practice for ten years, I think I learned more from you than from anyone else.” Just a few months ago, a former student wrote me – thirteen years after graduation – to thank me for what she learned from my classes.

Perhaps the most pleasant experience I had with a first-year law student came on the first day of class a few years ago. We had discussed a particular case, and I began playing around with the facts to see how the students might follow the process of discovering the boundaries of legal concepts. At this stage, most students are able to give a one-line answer, but can go no further. This young woman, however, took the inquiry to greater depths: “how does this square with what the court said in the earlier case?,” and similar inquiries. I knew, at once, that she was a real “keeper;” that classes were going to be far more interesting with her ability to use the Socratic process to discover the kind of understanding one never gets from answers; that it is the endless pursuit and improvement of one’s questions that makes for real learning.

I asked this young woman about her educational background: “I was homeschooled up to high school,” she responded. “The best teachers I ever had were my parents.” I suspect that she was the beneficiary of parents who knew that how to think was of greater importance to a creative and successful life, than being conditioned into what to think! The former approach allows men and women to develop, within their own minds, the skills not only for understanding the nature of the world, but to act competently. The latter method reduces people to the task of seeking the opinions of others – particularly the “experts” – to be informed of what they are expected to know.

After working through a series of hypotheticals, I still get a few students who ask “but what is the answer?” “Who cares?,” I respond. “It is going through the process of constant questioning that is the purpose of what we are doing here? I don’t know how the courts would rule in this situation, but I do know what noises to make were I representing one of the parties.” The Socratic method helps students grasp the meaning of Milton Mayer’s observation that “the questions that can be answered aren’t worth asking.”

Our world is being torn apart by men and women who naively try to integrate into some manageable whole their confusions, contradictions, conflicts, lies, evasions, corrupt and violent dispositions, and other destructive behavior. We live at a time when people become righteously indignant over the heinous murder of another, but wave flags and cheer for those who conduct wars against the millions; when Nobel Peace Prize grantors cannot distinguish Mother Theresa from Henry Kissinger as worthy recipients of such an award. Perhaps when our well-organized, expertly-run world finally runs out of answers to the destructive conditions it has created, we may – as Malcolm Sharp urged – undertake the search for improved questions.

RED FLAG on Earnings Quality Case Study (Thanks to a reader)

Note 3 on receivables says revenues are recognized when units are manufactured and assigned [at the company’s discretion] to specific contracts.(What the F%^&!) Then it says contracts provide for payment upon completion. (Expect a massive difference between GAAP accruals and CASH FLOW–lots of room for funny stuff!)

[not manufacture/assignment] and receipt of all approvals necessary

[which is not in Homex’s control]… Ergo revenues are booked when the customer doesn’t even have to pay. BINGO!

That note to the financials (Revenue Recognition) should have you reaching for the barf bag.

Corporate treasurers have been driving the bull market in stocks, not retail and institutional investors. The Fed’s Flow of Funds data show that net issuance of corporate equities over the past year through Q3 was minus $274 billion. In other words, buybacks well exceeded gross issues. Nonfinancial corporations registered net buybacks of $419 billion, while the financial sector had net issuance of $119 billion and foreign corporations issued $25 billion, according to the Fed’s data.

The financial sector data include stock issuance by all ETFs, which rose to $174 billion over the latest four-quarter period. Excluding these ETFs, net issuance by financial corporations was minus $55 billion.

The Fed also compiles monthly data for total gross equity issuance. Over the past 12 months through October, corporations raised $152 billion. However, that was overshadowed by buybacks. Data available for the S&P 500 show that they totaled $406 billion over the past four quarters through Q2.

Secrets and Lies of the Bailout

Secrets and Lies of the Bailout