A Masters in Munger Take the university level course.

110302239-Munger-Talk-at-Harvard-Westlake

Berkshire Hathaway Annual Meeting Notes 2004

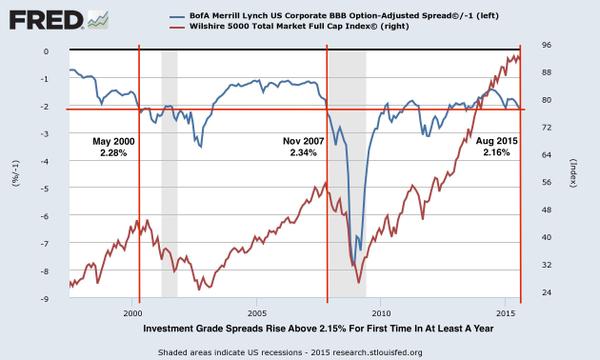

What is Mr. Druckenmiller worried about?

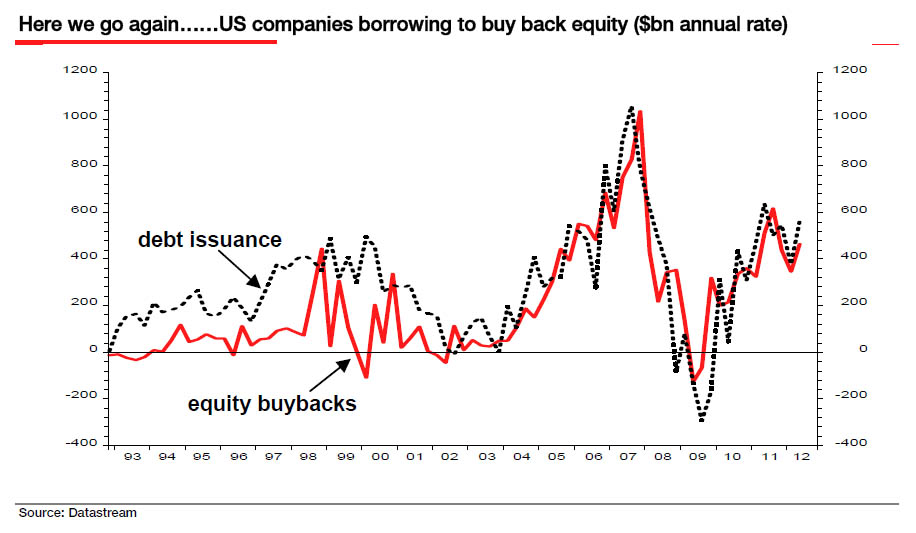

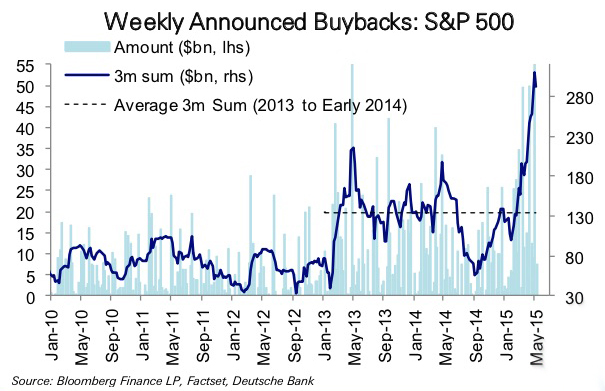

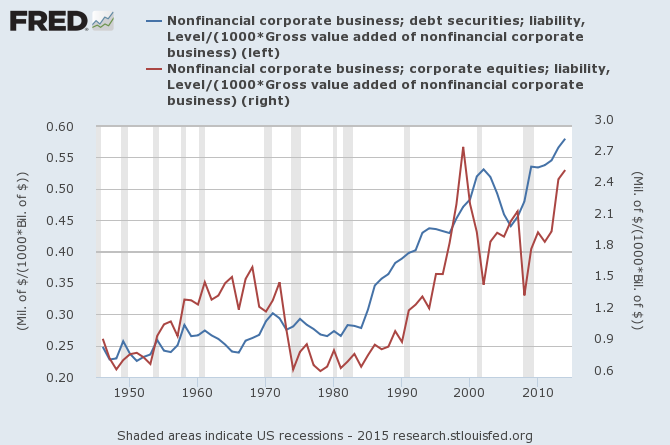

Buy-Backs Create Stealth Leverage

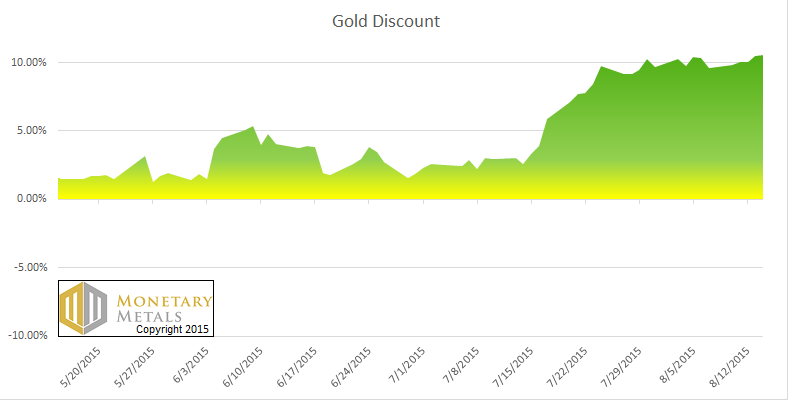

Gold “UNDERVALUED?”

A Masters in Munger Take the university level course.

110302239-Munger-Talk-at-Harvard-Westlake

Berkshire Hathaway Annual Meeting Notes 2004

What is Mr. Druckenmiller worried about?

Buy-Backs Create Stealth Leverage

Gold “UNDERVALUED?”

Bill Miller used to run Legg Mason’s Value Trust but then people learned he wasn’t a value investor and not to trust him –Port Stansberry

Value Investing in India

India’s market seems cheaper than the good ole USA’s S&P 500. The average stock in the US is trading at 25-times earnings. Americans have to look beyond the decks of the Titanic and view foreign shores. I traveled for a half year in India but I am ignorant about investing there, but we can always learn.

Stansberry Radio

This week, Steve Sjuggerud and his good friend Rahul Saraogi, a managing director at Atyant Capital, join Stansberry Radio to share the unique situation in India right now.

AUDIO (A tad obnoxious, but bear with them) http://www.stansberryradio.com/Porter-Stansberry/Latest-Episodes/Episode/541/0/Ep-151-Rahul-Saraogi-Investing-in-India

Rahul is a hedge-fund manager based in Chennai, India. He has been investing in India as his career for 14 years. And he told us on the radio show that India is “looking better than I’ve seen it in my career.”

Rahul wasn’t so concerned about the specific way you invest… as long as you simply get some money in. “India itself is going to do really well,” he said. “You need to have a piece of India in your portfolio.”

Guest: RAHUL SARAOGI

Rahul is a managing director at Atyant Capital and manages the Atyant Capital India Fund. In the last 13 years he’s managed money exclusively in the Indian markets. His mission is to consistently identify the best 10-15 investment ideas from among the thousands of publicly-traded Indian corporations. Rahul’s value-based investment philosophy stands apart due to his belief in the paramount importance of corporate governance, specifically how management operates with its minority shareholders in mind.

Prior to Atyant, Rahul spent four years leading Meridian Investments, generating a 430% absolute return for the firm’s high net worth clients.

Rahul graduated from the Wharton School of the University of Pennsylvania with a degree in Economics. Outside of Atyant, he practices Vipassana, a 2,500 year-old meditation technique that helps people see things as they really are. Rahul lives and works in Chennai, India.

CSInvesting: Color me skeptical, but I will take a look.

If I had to invest with a manager in India (vs. an ETF. See above) I might seek out: Prof. Sanjay Bakshi to the left of Prof. Greenwald of Columbia University.

http://www.sanjay_bakshi.net/articles-talks/

Prof. Sanjay Bakshi of http://www.value_quest_capital.com/

Revisiting Failure (JCP)

Improving as an investor is hard. You can make money while doing the wrong thing and vice-versa. I always write down the reasons for my investment thesis and then record the result when the position is exited. I will place a tickler in my calendar say eighteen months later to again review my past investment to see if there is more I can learn dispassionately. My last post on JCP, http://wp.me/p2OaYY-1JG. I bought near $20 on the assumption of buying below real estate value with little value for the retail operations, then sold near $15 after Johnson was fired. I was wrong.

Here is an update on the story behind the company’s struggles, How to Fail in Business While Really, Really Trying. Read: http://omnichannelretailing.com/how-to-fail-in-business-while-really-really-trying/ A good read! Investing teaches humility. My take-away turnarounds in a difficult business often don’t turn. The reputation of the business overcomes the management.

Posted in Search Strategies, Special Situations

Borrowers want capital, but they get money–newly created credit money. More credit money has been issued by the banking system than savers have deposited (“fiduciary media”). Those participants in the economy who suffer losses due to price changes were not parties to the original credit transactions. They are participants in the economy who receive the new money late in the process, after prices have been bid up by the credit money. –Mises (so much for the harmless actions of the Fed)

What Happens When You Buy Quality: October_Quest_2013

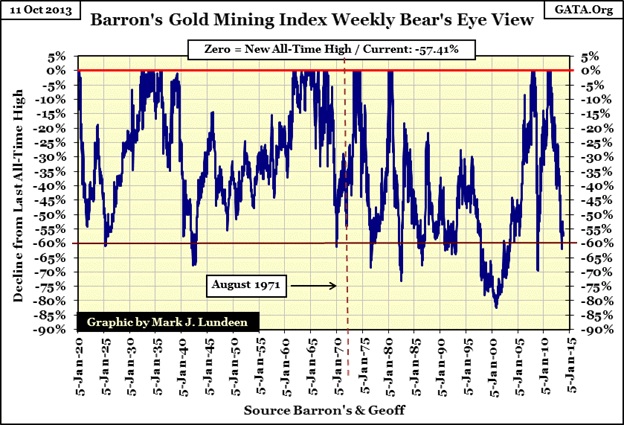

CAPITULATION IN THE MINERS

When I use the word capitulation it implies an ending to the bear market in precious metal equities, however NOTHING is certain in markets. I know not all public gold stocks will go to zero. Eventually, the laws of supply and demand assert themselves and you can only buy assets super cheap if sentiment is SUPER bearish. I think in late June when gold hit $1,180, gold stocks made a FEAR bottom while today they are going through despair/throw in the towel selling.

People see no hope so why own. Volume is relatively low and the selling persistent–day after day.

The above chart shows the sell-off from new highs over the past 90 years in the BGMI, the Barron’s Gold Mining Index). Currently, 2013 shows about a 63% loss or in the range of the past 10 bear markets.

Read more: http://www.gold-eagle.com/article/dow-jones-and-barron%E2%80%99s-gold-mining-index-1885-2013

The low relative volume, the historical depth of the sell-off and the demarcation of price movement between high quality (RGLD, FNV, SLW) and low quality gold stocks (NEM, GLDX) as the chart above shows, leads me to believe that we are closer to the end of the decline.

From: http://www.acting-man.com/?p=26553

We continue to get one ‘do or die’ moment after another in the charts of gold and gold-related instruments. So far, the outcomes have obviously been bearish every time since the 2011 peak, but at some point that is bound to change, as the fundamental backdrop continues to be gold-friendly (note that not every aspect of the fundamental backdrop is – for instance, the declining federal deficit is probably viewed as a negative by market participants). Often it is precisely at those times when nothing seems capable of turning a market around that surprise changes in trend can and do occur.

Note that gold sentiment remains absolutely dismal. Recently Mark Hulbert’s HGNSI (gold newsletter writer sentiment index) stood at minus 20 (meaning gold timers recommended a 20% net short position on average), while the daily sentiment index among gold futures traders (DSI) stood at 9 (all time low: 5). Bearish sentiment in the sector rarely becomes as extreme as it is at the moment. Of course it has been quite negative for some time now, but the current readings are rather extreme even so.

A major reason why we continue to maintain that the fundamental backdrop remains gold-friendly even though the price action suggests a bear market is still in progress, is that we believe that mainstream analysts are quite mistaken when they assert that it is back to ‘business as usual’ in the economy. It clearly isn’t.

History is being made today!

Of course, if you believe QE will lead to sustainable growth without monetary mayhem then stay away from anything to do with gold.

SHORTING SOCIALISM

The company exists as a social transfer mechanism between Western investors and Brazilian government officials and Petrobras workers. No hope.

Posted in Investor Psychology, Search Strategies

Tagged Acting Man, Bakshi, BGMI, Gold Stocks, Quality Companies

On the day when I left home to make my way in the world, my daddy took me to one side, “Son,” my daddy says to me, “I am sorry I am not able to bankroll you to a large start, but not having the necessary lettuce to get you rolling, instead I’m going to stake you to some very valuable advice. One of these days in your travels, a guy is going to show you a brand-new deck of cards on which the seal is not yet broken. Then this guy is going to offer to bet you that he can make the jack of spades jump out of this brand-new deck of cards and squirt cider in your ear. But, son, do not accept this bet, because as sure as you stand there, you are going to wind up with an ear full of cider.” –Sky Masterson

From David Ricardo making a fortune buying British government bonds on the eve of the Battle of Waterloo to Warren Buffett selling insurance to the California earthquake authority, the wisest investors have earned extraordinary returns by investing in the unknown and the unknowable (UU). But they have done so on a reasoned, sensible basis. The acronym UU refers to situation where both the identity of possible future states of the world as well as their probabilities are unknown and unknowable.

This article may take several readings but you will find that your investing can vastly improve if you understand how to distinguish risk from uncertainty. Click on link here: Investing_in_Unknown_and_Unknowable_Zeckhauser

An EXCELLENT article for advanced investors.

Zeckhauser’s Approach

(from Sanjay Bakshi) Let’s keep this idea – of seeking exposure to positive black swans in mind, and move on to Richard Zeckhauser whose famous essay “Investing in the Unknown and Unknowable”

(http://hvrd.me/b87ESq) is a must-read for all investors.

In this essay, Zeckhauser discusses a few critical things. Let me just list them out.

First, most investors can’t tell the difference between risk and uncertainty.

Risk, as you know from Buffett, is the probability of permanent loss of capital, while uncertainty is the sheer unpredictability of situations when the ranges of outcome are very wide. Take the example of oil prices. Oil has seen US$ 140 a barrel and US$ 40 a barrel in less than a decade. The value of an oil exploration company when oil is at US$ 140 is vastly higher than when it is at US$ 40. This is what we call as wide ranges of outcome.

In such situations, it’s foolish to use “scenario analysis” and come up with estimates like base case US$ 90, probability 60%, optimistic case US$ 140, probability 10%, and pessimistic case US$ 40, probability 30% and come up with weighted average price of US$ 80 and then estimate the value of the stock. That’s the functional equivalent of a man who drowns in a river that is, on an average, only 4 feet deep even though he’s 5 feet tall. He forgot that the range of depth is between 2 and 10 feet.

Let’s come back to what Zeckhauser says on this subject.

Most investors, according to Zeckhauser, whose training fits a world where states and probabilities are assumed to be known, have little idea how to deal with unknowable and treat as if risk is the same as uncertainty. When they encounter uncertainty, they equate it with risk, and tend to steer clear. This often produces buying opportunities for thoughtful investors who shun risk but seek uncertainty on favourable terms.

Second, Zeckhauser states that historically, some types of unknowable situations – those that Taleb calls positive black swans – have been associated with very powerful investment returns and that there are systematic ways to think about such situations. And if these ways are followed, they can lead you to a path of extraordinary profitability.

One way to think of unknowable situations is to recognise the asymmetric payoffs they offer. The opportunity to multiply your money 10 or 100 times as often as you virtually lose all of it is a very attractive opportunity. So if you have a chance to multiply your money 10 or a 100 times, and that chance is offset by the chance that you can lose all of it in that particular commitment, is a good bet, provided you practice diversification, isn’t it? That’s the power of asymmetric payoffs. So, Zeckhauser’s idea of profiting from unknowable situations is akin to Taleb’s idea of getting exposure to positive black swans.

Third, there are individuals who have complementary skills – they bring something to the table you can’t bring. They get deals you can’t get. An example that comes to mind is the deal Warren Buffett got from Goldman Sachs when he bought the investment bank’s preferred stock on very favourable terms during the financial crisis of September 2008 – a US$ 5 billion investment in Goldman’s preferred stock and common stock warrants, with a 10% dividend yield on the preferred and an attractive conversion privilege on the warrants.

Essentially what Zeckhauser says is that there are people who can get amazing deals – that they have this ability to source these transactions. They have certain skills that allow them to attract such transactions to them – maybe they’ve got capital, contacts, or something in them which a typical investor does not have. Zeckhauser advises that when the opportunity arises to make a “sidecar investment” alongside such people, you shouldn’t miss it.

For many Indians, sidecar investing can best by understood by remembering that famous scene in the movie “Sholay” in which one sees Veeru driving the mobike and Jai enjoying the free ride in a sidecar attached to the bike. That’s essentially the idea here. The investor is riding along in a sidecar pulled by a powerful motorcycle driven by a man who has complimentary skills. The more the investor is distinctively positioned to have confidence in the driver’s integrity and his motorcycle’s capabilities, says Zeckhauser, the more attractive is the investment. So how do you bring all this together?

Let me summarise.

We talked about Buffett’s idea on risk. We talked about Taleb’s ideas on uncertainty and the need to avoid negative black swans and the need to get exposure to positive black swans. We talked about Zeckhauser’s advice on uncertain and unknowable situations and how to profit from them. Sure, as value investors, we want exposure to positive black swans. But we are not like private equity investors or venture capitalists. We are far more stingy and risk averse than those people. We want exposure to positive black swans on extremely favourable terms.

But what do we mean by “extremely favourable terms?” Well, that’s where Graham – our fourth role model comes in. Margin of Safety.