Bill Miller used to run Legg Mason’s Value Trust but then people learned he wasn’t a value investor and not to trust him –Port Stansberry

Value Investing in India

India’s market seems cheaper than the good ole USA’s S&P 500. The average stock in the US is trading at 25-times earnings. Americans have to look beyond the decks of the Titanic and view foreign shores. I traveled for a half year in India but I am ignorant about investing there, but we can always learn.

Stansberry Radio

This week, Steve Sjuggerud and his good friend Rahul Saraogi, a managing director at Atyant Capital, join Stansberry Radio to share the unique situation in India right now.

Rahul is a hedge-fund manager based in Chennai, India. He has been investing in India as his career for 14 years. And he told us on the radio show that India is “looking better than I’ve seen it in my career.”

Rahul wasn’t so concerned about the specific way you invest… as long as you simply get some money in. “India itself is going to do really well,” he said. “You need to have a piece of India in your portfolio.”

Guest: RAHUL SARAOGI

Rahul is a managing director at Atyant Capital and manages the Atyant Capital India Fund. In the last 13 years he’s managed money exclusively in the Indian markets. His mission is to consistently identify the best 10-15 investment ideas from among the thousands of publicly-traded Indian corporations. Rahul’s value-based investment philosophy stands apart due to his belief in the paramount importance of corporate governance, specifically how management operates with its minority shareholders in mind.

Prior to Atyant, Rahul spent four years leading Meridian Investments, generating a 430% absolute return for the firm’s high net worth clients.

Rahul graduated from the Wharton School of the University of Pennsylvania with a degree in Economics. Outside of Atyant, he practices Vipassana, a 2,500 year-old meditation technique that helps people see things as they really are. Rahul lives and works in Chennai, India.

CSInvesting:Color me skeptical, but I will take a look.

If I had to invest with a manager in India (vs. an ETF. See above) I might seek out: Prof. Sanjay Bakshi to the left of Prof. Greenwald of Columbia University.

Improving as an investor is hard. You can make money while doing the wrong thing and vice-versa. I always write down the reasons for my investment thesis and then record the result when the position is exited. I will place a tickler in my calendar say eighteen months later to again review my past investment to see if there is more I can learn dispassionately. My last post on JCP, http://wp.me/p2OaYY-1JG. I bought near $20 on the assumption of buying below real estate value with little value for the retail operations, then sold near $15 after Johnson was fired. I was wrong.

Here is an update on the story behind the company’s struggles, How to Fail in Business While Really, Really Trying.Read: http://omnichannelretailing.com/how-to-fail-in-business-while-really-really-trying/A good read! Investing teaches humility. My take-away turnarounds in a difficult business often don’t turn. The reputation of the business overcomes the management.

A reader asked me via email about what books to read to understand history.Please post your questions in the comments section because I most likely will lose your email–let others see your thoughts.

Then read Wall Street, A History by Charles R. Geisst.

That will get you started. Don’t forget to read more general history as well such as The Rise and Fall of the Third Reich-the mother of all bear markets for the human race. Couple that with Winston Churchill’s books on European history and WWII for another perspective.

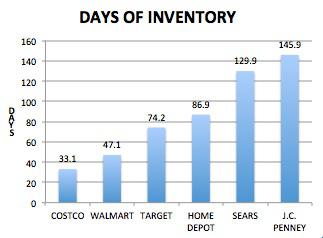

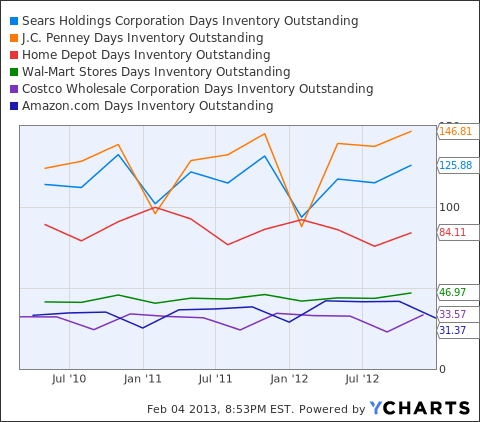

Here is a good article that captures the problem at JCP. Essentially a retailer owns or leases space to sell goods to customers. The wider the mark-up and/or the faster the turnover of goods, the greater the profits, return on capital, etc. JCP HAS to get customers in the door AND then get them to buy–obviously. I don’t agree on all the comparison (Costco vs. a Dept. Store) in the graphs, but you get the picture.

(Days of Inventory = Inventory/Cost of goods x 365 days. Data courtesy of Morningstar.com in TTM time frame.)

Any slower inventory management and Penney and Sears might as well advertise in Frommer’s Guide to museums.

Make no mistake: Sears (SHLD) and J.C. Penney (JCP) act more like museums than retailers. They’ve become simply corridors to get to the rest of the mall. The tip off: The two can’t unload their inventory. Goods move at a trickling pace and it’s killing the bottom line.

Check the length of time it takes these brick-and-mortar retailers to move their goods: Costco (COST), Wal-Mart (WMT), Target (TGT), Home Depot (HD), Sears and J.C. Penney. The chart shows how long it takes to turnover inventory. The longer the days of inventory, the longer dollars are tied up.

JCP dropped below $17 for about a 20% decline. More than 15% of its float has traded in less than 24 hours. 30% of the float is short.

Where to find maximum pessimism and hatred:

Here are the headlines.

“Simply stunning results” from J.C. Penney (JCP), says Tiburon Research’s Rob Wilson, quickly…

Wednesday, February 27, 4:58 PM ET

Sales Sink, Stock Gets Hammered in After-hours Trading (Reuters)

Feb. 27, 2013, 4:44 PM More on J.C. Penney’s (JCP) Q4: No sigh of relief for investors just yet as the firm reports comparable store sales fell 31.7%, below the consensus call of -26.9%. Customer are fleeing, but no give up from CEO Ron Johnson: “…we are energized by our shop roll out plans.” Gross margin was crushed, falling to 23.8% of sales vs. 30.2% last year. Internet sales slumped again, losing 34.4% Y/Y just marginally better than last quarter’s 37% nosedive. Cash position $930M at end of Q4. No guidance is issued, but the retailer says it will open 20 shops geared toward home products in 505 stores with brand partners. JCP -4.4% AH. (PR) Read comments

· Shareholders need to revolt aggressively (Yahoo poster 6 PM 2/27/13)

The Board needs to fire Ron Johnson tonight. They need to then hirte a trustee to rebuild it and then resign en masse for hiring this imbecile. First rule of retail: Don’t f it up! Kill the BOD and Johnson NOW.

Ron Johnson couldn’t sell pus*y to a troop train. How many times will we sell retailers fail due to hiring rock star leadership who is so arrogant to turn away from the existing customers without attracting any replacements? Just desserts Ron. Eat #$%$. Ron is a $%^&*! piece of $%^&!

Where is the class action shareholder lawsuit ? Will RJ fly home tomorrow on the corporate jet ? Will he still be racking up insane bills at the Ritz ?

—

Can you feel the love? Yes, investors are upset, but do you read any deep analysis as to the value of the company?

What happened in this situation–Dillards (DDS)? Perhaps a case study is in order. Ron Johnson is a genius at $40 and now at $17 he receives death threats. I have never seen a turn-around take less than 36 months. Let’s check back in 2014.

Dillards monetized some of its real estate assets through a REIT.

I am not implying that JCP should do the same, but I recon there is a reason JCP has not dropped below $14 per share even in the dark days of 2009. Can the massive hate and fear take us to new lows? Not, if it doesn’t happen in the next month.

My take: Turn off the price news and just look at the business as if you owned it. It is a tale of two cities (Dickens). The old JCP (which is the majority of sales/profits) is sliding faster than expected as the typical/traditional customer is confused, while the new JCP is doing well. In the long run this is good news but in the short run the news is worse.

Ron Johnson had this to say about the future of Penney’s on the conference call: “It’s really becoming a tale of two companies… one is J.C. Penney, a promotional department store; the other is jcp, which is a start-up, which is a specialty department store. And it turns out what’s good for one isn’t necessarily good for the other – and that’s why we’ve seen this year, J.C. Penney has performed tougher than we’ve expected… but the good news is jcp is much better than we imagined. As we wind down J.C. Penney over the next 36 months, my job is to deliver as best it can and generate as much cash as possible to fund the new jcp.”

Will management just do the same thing if sales keep dropping at the same rate? Probably they will look to sell some of their real estate while being more aggressive on a simple discount plan.

Yes, I agree with a reader that JCP is a “special situation” or transformation. You have a good vs. bad business here. But you also have hard assets of decent real estate and a balance sheet that isn’t too indebted so there may be replacement value for the real estate. However, retail is a very difficult business. More “value” investors hit the rocks in this industry than in any other except financial. Be very careful to get a rediculous price or stay away. It is hard to buy a lot of JCP when you have CSCO, INTC and other franchises at decent prices.

However, institutions who have owned this stock probably want out so expect continuous pressure and volatility with the stock price which is good for patient buyers. There might be an opportunity to see JCP trade at its real estate value with little or no value imputed to the new JCP. But if you are confused or uncertain of the value or the risk/reward, then walk away. Learn from the outcome.

The main lesson to be gleaned is to focus on the numbers and what the company is trying to do not the pundits. Let’s revisit in 2014.

Few stocks detracted from returns. Dell fell 21% over the last three months, and the stock’s 33% decline in 2012 made it the primary detractor to the Fund’s performance for both periods.

The primary challenge over the last two quarters was a larger than-expected decline in End User Computing (EUC) revenue due to several pressures. Tablets and other mobility devices displaced notebooks more rapidly than anticipated; demand in India and China shrunk, where Lenovo aggressively priced to take share in these geographies; and commercial purchases slowed because of general economic weakness and the anticipated release of Windows 8. In spite of the decline in notebooks and PCs, margins held up in EUC, a testament to the company’s successful cost cutting and variable cost structure.

Far more importantly, the growing, higher margin Enterprise Solutions and Services (ESS) business had strong networking and server growth with servers gaining market share. While ESS represents about one-third of revenues, it constitutes over half of profits and a far higher share of our appraisal. The company’s transformation to a solutions-based company is well underway and leverages Dell’s direct distribution advantage of over 20,000 employees responsible for customer relationships with small and mid-size businesses. Interestingly, IBM successfully refocused its business over a ten year period starting in the early 1990’s from mainframe hardware to multifaceted technology solutions for large-scale customers. The head of IBM’s mergers and acquisitions was Dave Johnson, who joined Dell in 2009 to lead its strategy to enhance solutions offerings and has purchased a number of companies and products that have grown through Dell’s expansive distribution.

VALUATION: If we assume that EUC continues its rapid decline and has no value, we appraise the remaining ESS business at over twice the current stock price. With adjusted cash earnings of $2.00/share and an enterprise value of less than $3.50/share (share price minus net cash and DFS), the stock trades at less than a 2X adjusted P/E for a growing business (ESS) with good margins and an owner/operator as CEO who is focused on growing value per share.

Wow, I am skeptical Dell is that cheap. The question to ask is: “Does ESS have a competitive advantage? Because only then will growth matter.

In The Intelligent Investor, Benjamin Graham sums up his investment philosophy by saying that an intelligent investor must be “businesslike” in approach. Investing in shares in a company is just like owning a share in a business enterprise and the investment must be approached as if one were buying a business, or a partnership in one.

There are four guiding principles for Graham:

1. Know the business

The investor needs to become knowledgeable about the business or businesses carried on by the company in which they propose to invest – what it sells, how it operates, what is the competitive environment, what are the threats and opportunities, the strengths and weaknesses.

An investor who bought a fruit shop, or a shoe factory, without investigating these things, and knowing them, would be foolish. The same applies to share investment. An investor who does not understand the business should not be investing in it.

2. Know who runs the business

An investor who cannot operate the business for himself or herself, needs a manager. This is the position of the average share investor, who owns a share of an enterprise that is run by others.

The owner of a business in this position would want a manager who will manage the business competently, efficiently and honestly. The share investor should not be satisfied with less. Unless the investor believes, through sound research, that the company is managed efficiently, competently and honestly, in the best interests of the shareholders, the investment should not be made.

3. Invest for profits

An investor would not normally buy a business that did not, on proper research, appear to have reasonable expectations of producing good profits over time. Share investors should take the same approach and buy, as Graham says, “not on optimism, but on arithmetic”.

4. Have confidence

Graham encourages investors to properly research their investments and, if they believe their investment judgment to be sound, to act on it. He cautions investors in this position against listening to others.

“You are neither right nor wrong because the crowd disagrees with you. You are right [or wrong] because your data and reasoning are right [or wrong].”

You can feel the fear, anger, and despair (visit the Yahoo Finance Board for JCP to get a feel for what small investors think), because you own the company. Whom do you blame, what can you do? The only way to stop the price from going down is to turn off your screen. 🙂

To gain a more realistic view of J.C. Penney’s prospects, however, here is the Deutsche Bank analyst Charles Grom: “Trends at J.C. Penney are obviously getting worse, not better, and we are becoming more and more convinced that sales in 2013 will also decline, which could lead to a going-concern problem next year.” (CS Editor: OK, if that were the case would the management and Board of Directors take a different course? Slow spending, sell off assets, etc. OR is the analyst just linearly extrapolating to come up with his thesis?)

The company’s stock has fallen nearly 50 percent since the beginning of the year. Even its online sales, through jcp.com, fell 37.3 percent last quarter from a year ago. Yet Mr. Johnson, a well-regarded and charismatic retailer who worked at Target before his meteoric rise at Apple, appears to be trying to mimic Steve Jobs and create what Mr. Jobs’s biographer, Walter Isaacson, called a “reality distortion field.” An opinion not a fact.

Andrew Burton/ReutersRon Johnson, chief executive of J.C. Penney, says the store renovation plan is a success. Mr. Johnson has spent the last several months trying to persuade investors that his transformation of J.C. Penney was the equivalent of Mr. Jobs’s efforts to turn around Apple a decade ago.

“You know, I watched this movie before. When I joined Apple in 2000, Apple was a company dwindling. Everyone said to me, ‘What are you doing there?’ ” Mr. Johnson told investors in September. “Apple wept through 2002 and I think sales were down 38 percent as we dreamed about becoming a digital device company. But Apple invested during that downturn. That’s when Apple built, started to build its chain of stores. That’s when Apple transitioned to Intel. That’s when Apple started its app division. That’s when Apple imagined and built the first iPod.”

O.K., Mr. Johnson, but that was Apple. And J.C. Penney is not Apple — and let’s be honest, it can never be Apple. The company doesn’t make its own magical, revolutionary products that bring tears of joy to its customers. It is a low-end department store that Mr. Johnson is hoping to turn into a slightly higher-end department store that sells clothing made mostly by other manufacturers.

Still, Mr. Johnson has sought to remake the company quickly, perhaps too quickly, by eliminating promotions and discounts, moving the stores more upscale, rebranding the company as JCP and putting in place a “fair and square” pricing model. (J.C. Penney is, however, putting on a special sale for the holidays.) Granted, JCP is no Apple, but what did Ron Johnson accomplish at Target–probably a better comparison.

Yet the renovations are hardly finished — or in some cases even started. Only 11 percent of its stores’ floor space has been remodeled with his successful specialty-store-within-a-store concept, in which he has opened up outposts for brands like Levi’s, Izod, Liz Claiborne and the Original Arizona Jean Company.

J.C. Penney may have been dying a slow death before Mr. Johnson’s arrival — some rivals used call it “death by coupon,” given the retailer’s penchant for discounts — but the company’s decline has only accelerated.

But the lessons, and successes, of the rollout of Apple stores are proving that they do not apply to Penney. While the customer experience at Apple is in a class by itself, and Mr. Johnson should rightly receive credit for that, the success of the stores was in large part a function of stunning products with a fan base that would stand outside stores for days in the rain to get their hands on them without any chance of a discount. Do you think there are customers who will ever stand outside J.C. Penney overnight for the next Liz Claiborne sweater? (J.C. Penney bought the Liz Claiborne brand last year.)

“Ron Johnson’s remake of JCP has assumed the consumer — the only one who matters — is the one who shops at Target or Macy’s or Nordstrom’s. Instead of pivoting on and strengthening the historic JCP brand (What brand?), Johnson’s decided to recreate the Target and Apple wheel, a move akin to Toyota suddenly deciding it’s Porsche. In short, a ridiculous and condescending move,” Margaret Bogenrief, a partner at ACM Partners, a boutique crisis management and distressed investing firm, recently wrote.

There is something romantic about watching Mr. Johnson try to remake a dying classic icon (So why did Sorkin call JCP a brand in the prior paragraph). At some gut level, you have to root for him. He’s making a bold bet. Transitions are inherently painful. And everyone loves a great comeback story.

Here’s the good news: In the stores that have been transformed, J.C. Penney is making $269 in sales a square foot, versus $134 in sales a square foot in the older stores. So the model itself is working. And Mr. Johnson has the support of the company’s largest shareholder, Pershing Square’s Bill Ackman, who personally recruited Mr. Johnson. If Mr. Johnson were starting with a blank slate, it might be a great business.

Mr. Ackman declined to comment. J.C. Penney did not make Mr. Johnson available.

Now here’s the bad news. Mr. Johnson still has to convert nearly 90 percent of his square feet of shopping space. That will very likely take $1 billion and as long as three years. If the sales decline that occurred last quarter accelerates, the company could run out of money. It now has about a half-billion in cash and access to a credit line for as much as $1.5 billion.

Of course, it remains possible that Mr. Johnson, who people close to him say is a realist, could always decide that the transformation is not working and change course to return to the old model of J.C. Penney and save all that money remodeling. But that would be a huge setback.

The question Mr. Johnson may be asking himself now is: What would Steve do?

A version of this article appeared in print on 11/13/2012, on page B1 of the NewYork edition with the headline: A Dose Of Realism For the Chief Of J.C. Penney.

So What is JCP worth? Forget the price today, what is the value of JCP? Since this is NOT a franchise, then this would be an asset type of investment. What is the real estate worth for JCP? I would start there and review with a critical mind my valuation of the company. Oh, and forget blaming anyone for the price being below your purchase price, perhaps or perhaps not, today is your luckiest day.

JC Penny’s (JCP) Announces Terrible Earnings but The stock rallies

Is the market a discounting mechanism? Jim Cramer of CNBC would say, “JCP is a CROWDED short.” The beginnings of a case study here: JCP_Barrons

Scams

My inbox is being flooded (as a subscriber–to find shorts–to Penny Stock Newsletters my email is raw meat for scammers) with more sophisticated scams: IMF_–_International_Monetary_Fund_SCAM

My email automatically responds to the scammer to call about 50 different (phony) phone numbers in the US to reach me so I can wire funds to help them.

Note: Charlie Munger once said that no one ever got rich being an asset allocator.

Updated: Aug. 13, 2012: from www.economicpolicyjournal.com

The economist and financial author Harry Browne once designed what he

called a “Permanent Portfolio”. The idea behind PP was to create a

portfolio in away that investments were made so that the portfolio

would maintain its value and grow conservatively over time, with

certain parts of the portfolio outperforming other parts of the

portfolio at different times, depending upon the economic

environment—without having to time the economy.

Browne’s idea was to equally divide up a certain amount of money

between various sectors. Because he felt the economy was cyclical, he

felt that when a sector was cheap (and might be poised for a climb)

you would end up buying more unit wise in that sector, if you

allocated your money equally among the sectors, and less, unit wise,

when prices were higher, BUT that this still resulted in your

participating in all sectors, without having to attempt to time the

exact ups and downs of the business cycle.

There’s a lot to be said for Browne’s PP.

His four sectors were:

The US stock market via warrants

The 30-year T-bond.

Gold coins.

Cash, i.e.,Treasury bills

This is a good base to work with. However, given that the yield on the

30-year Treasury bonds is so low (2.65%), in my view it makes no sense

to put money in them. Thus, I would put money into only three sectors:

gold coins, Treasury bills and the US stock market.

As far as gold coins are concerned, I would divide up purchases

between both gold coins and silver coins. And also, if your back is

strong enough, nickels.

Put 33% in nickels of your “gold sector” purchases. They can be

acquired at any bank. Put 33% in gold coins and 33% in silver coins.

Buy only what is known as “junk silver” (These silver coins come in

bags of $1,000 face value). as for gold buy only “bullion coins” such

as the American Eagle and Canadian Mapleleaf.

If you do not live near a major gold coin dear that has been in

business for at least a decade, consider buying from Kitco.I have

successfully purchased coins via mail with Kitco for many years. If

you chose to use a different dealer, you can use the Kitco prices

online as a guide. One note when buying online, split up your order,

so you don’t risk having an order lost. It’s very unlikely an order

will get lost but take the precaution and split you order up.,Kitco

sends by registered mail and they video tape every step of your coin

order as it is put in a box.

As for Treasury bills, depending upon the size of your purchase, you

can buy them directly from the Fed or through a bank or broker.When

possible, I recommend dealing directly with the Fed.

For those dealing in smaller numbers, I recommend simply using a bank

account at a “Too Big To Fail” bank.

Browne recommended using warrants for the stock market portion of the

portfolio, there is nothing wrong with this. However, carefully chosen

stocks picks will provide just as much upside potential as warrants,

with less of the downside risk.

Thus to re-cap:

A PP, under current market conditions should look like this:

33% in Treasury bills (or funds at a Too Big To Fail bank)

33% In gold coins (actually split up between 1/3 gold coins, 1/3,

silver coins and 1/3 nickels)

33% in the stock market (with stocks that will benefit from inflation

and also from individual growth trends)

How much should be put into your PP?

It depends upon your age and your wealth. The older you are and the

more wealth you have, the more that should be put into PP. perhaps

100%.

If you are very young and are willing to take on more risk, then

perhaps only 50% of your funds should be in a PP. The rest can be for

more aggressive trading.

The EPJ Daily Alert is about identifying opportunities for the stock

part of the PP and also identifying opportunities for more aggressive

traders.

Below are stocks and other investments that I have previously

identified in the EPJ Daily Alert and are still “active’ investments.

They are designated as PP (permanent portfolio) or AP (aggressive

portfolio) investments.

First, here is my view on nickels a gold coin sector PP investment:

NICKELS

At some point,nickles, which are mostly made of copper, will start to

disappear from

circulation, as the copper price climbs

There is right now approximately 5.0 cents worth of metal in a nickel.

It was much higher before the financial crisis: Close to 7 cents worth

of metal. When I run into someone that does not have a strong

background in investing, I now tell them to buy nickels. You need storage space and a strong back to move them around, but a $100 box of nickels (roughly the size of a very large brick) can be lifted without problem. You can stack

plenty of “bricks” on a hand truck.

What’s great about this investment is that there is no downside. In

the unlikely event that there is no inflation, you can just spend your

nickles. But you will have to “order” your nickles from your bank. I

tend to try and keep any one order (per bank) to around $2,000 for

both handling (lifting) purposes and so that Ben Bernanke doesn’t

personally visit to see what is going on.

You can also buy brand shiny new nickels from numismatic dealers for a

small charge, and obviously they don’t ask any questions. But, again, nickels are a great conservative investment [If you have the space and the back] with zero downside.

One hedge fund manager has reportedly ordered from his bank a million

dollars worth of nickels. I fully expect the coins will eventually

climb in value to at least double their 5 cent face value price. The

government has made it illegal to melt them down, but you will never have to do anything close to that. When you need to liquidate, just sell them to a

numismatic dealer. Via the magic of black markets, the value (with a

good spread) will track the metal value. You can monitor the value of

the metal in the nickels at the website Coinflation.com.

As part of the PP stock portfolio, I include:

COMMERICA WARRANTS

Comerica (CMA-WT) warrants have much less exposure to foreclosuregate

than other major banks (They are heavy into commercial loans which

will benefit from Fed printing, and the warrants offer an opportunity

to play CMA on a leveraged basis, while limiting risk. These warrants

were issued by Comerica to the Treasury as part of the TARP program.

Warrants give you great upside leverage with limited downside risk. A

hedge fund manager I know, who has studied these warrants, tells me

they are mis-priced. He tells me traders use the Black_Scholes option

model to determine value of the warrants, but the manger argues, the

option model undervalues warrants.

For example Comerica warrants expire in late 2018 and the change in

intrinsic value of the warrants will depend on the value of Comerica

in 2017. Which means long-term trends are much more important in these

warrants, and this is not properly taken into consideration in the

short-term thinking of the Black-Scholes model.

We have long been devoted to the practice of maintaining written research on each of our Fund’s investment ideas as a way to document our thoughts and expectations for each idea. Generally, our research should explain why a given investment should work, the risks that might keep it from working, and define a range of plausible scenarios that we use to formulate our valuation assumptions.

As ideas play out, we document the interim events and any decisions we make along the way. If an investment doesn’t work out, we try to determine whether there is a lesson to be learned that will benefit us in our future decisions.

While this research process is time-consuming, over the years we have come to believe in the approach even though there can be periods where the process doesn’t seem like it is helping our performance. Even worse, we occasionally succumb to mistakes that we should have recognized from prior experience, usually after sufficient time has passed to take the sting out of the prior event. Recently, however, we encountered a situation where we did benefit from having documented our experience with a similar investment many years ago.

Betting on the Jockey Rather than the Horse

As part of our search for promising investments, we look for management teams with great long term track records and that are strongly aligned with common shareholders. Over time, however, we have learned that so-called “jockey” investments can be a form of a value trap in certain conditions. Often, the reputation and track record of a manager or team can overshadow the quality and value of the underlying business. An investment based on faith that a given management will create value without careful analysis of the assets in place can be dangerous, and such stocks are prone to a “halo effect” that lasts until something goes wrong. It is easy as investors to become infatuated with a great management team to the extent that one might be willing to buy a stock without being entirely sure of getting great value for the underlying business. It is therefore quite common for businesses with well-known and well-regarded management to trade for a significant premium to comparable peers.

What we’ve learned is that while we very much prefer to have great “jockeys” directing our investment horses, it is usually a mistake to pay a premium for the privilege. It is usually far better to patiently wait until the stock gets cheap enough to eliminate any management premium. By not paying extra for management, we protect ourselves from the same types of errors in judgment that can occur when assessing business quality or business valuation. When the management team either turns out not to be as good as hoped or alternatively where good management simply makes what turns out to be a mistake that impairs investment value, capital is protected to some degree by ensuring that we do not overpay for the underlying assets or business.

Back in 2006, we decided to make an exception to the above rule of buying the assets at a discount and getting the management for free. The stock was Sears Holdings, and the “jockey” was Edward Lampert.

At the time, we wrote an internal research document arguing that Lampert’s track record was so good that we should purchase Sears Holdings even though we couldn’t make a strong and convincing case that the stock was undervalued. Rather, we made the case that the risk of missing out on the potential benefits of such an obviously great manager in his prime would be the greater sin. In essence, we were willing to pay up for value that hadn’t yet been created because we were so sure it would be. We realized our mistake a year or so later and sold the stock. We never had any real idea what Sears Holdings was worth, and we still don’t.

(CSInvesting: an honest, brave assessment of a permanent loss of capital)

Recently we were struggling with the temptation to invest in a new idea featuring many of the same ingredients: a management team with impressive credentials that is highly incentivized to create value for shareholders taking over a business that has been performing poorly relative to peers, making it ripe for a management turnaround. The stock was JC Penney, which was trading for about $35 at the time of our initial analysis.

After working through several iterations of the potential valuation case, we still couldn’t come up with a clear picture of what the business is worth with any high level of conviction. Still, the idea seemed to pull at us, until we asked ourselves a simple question: if this idea doesn’t work out, is there an obvious mistake that we will be able to point to and kick ourselves for having made? The answer was yes – that we would be making the Sears Holdings “jockey” mistake. We decided against the investment.

In any event, JCP now trades at a much lower price than when we first looked at it, and the market no longer views the management through the same rose-colored lenses it did even three months ago. While we still have a very high regard for the management team at JCP, we haven’t been able to get any more comfortable with our ability to value the business. So even at the much lower price, JC Penney is not an easy call for us.

While we won’t be surprised to see JC Penney work out as an investment – particularly from the recent $20 price – we simply have been unable to get to the point where we have great conviction in the idea. Until we do, we will leave it to others who may understand it better — and we won’t kick ourselves if it turns out to be a money maker for someone else. We are grateful, however, for the benefit of having documented a mistake we made back in 2006 so that we did not repeat it in 2012.

CSInvesting: This is an example of how you can learn from your investing experience. The author recorded his investment, then honestly assessed how it developed and used what he learned to avoid a future loss.