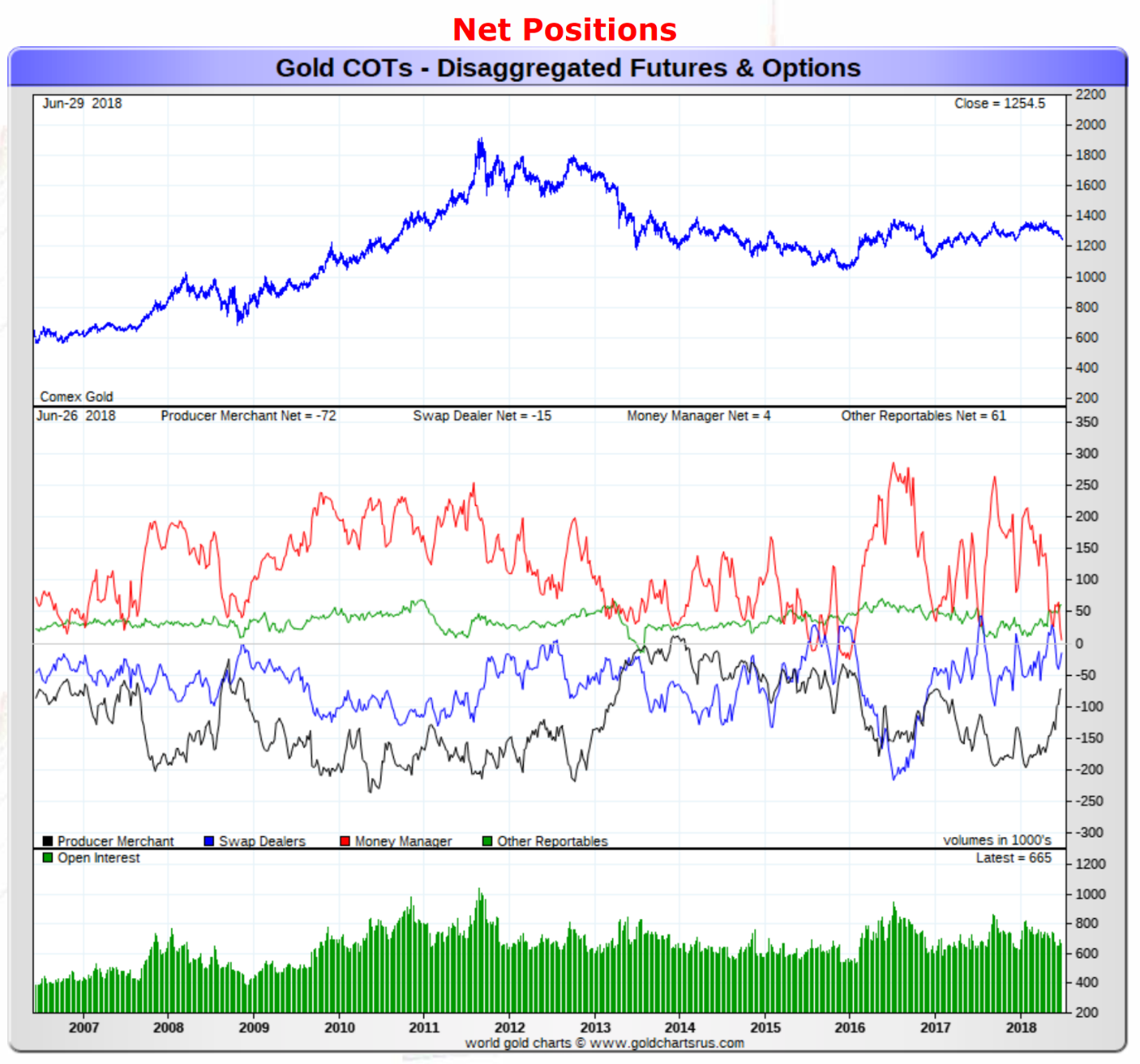

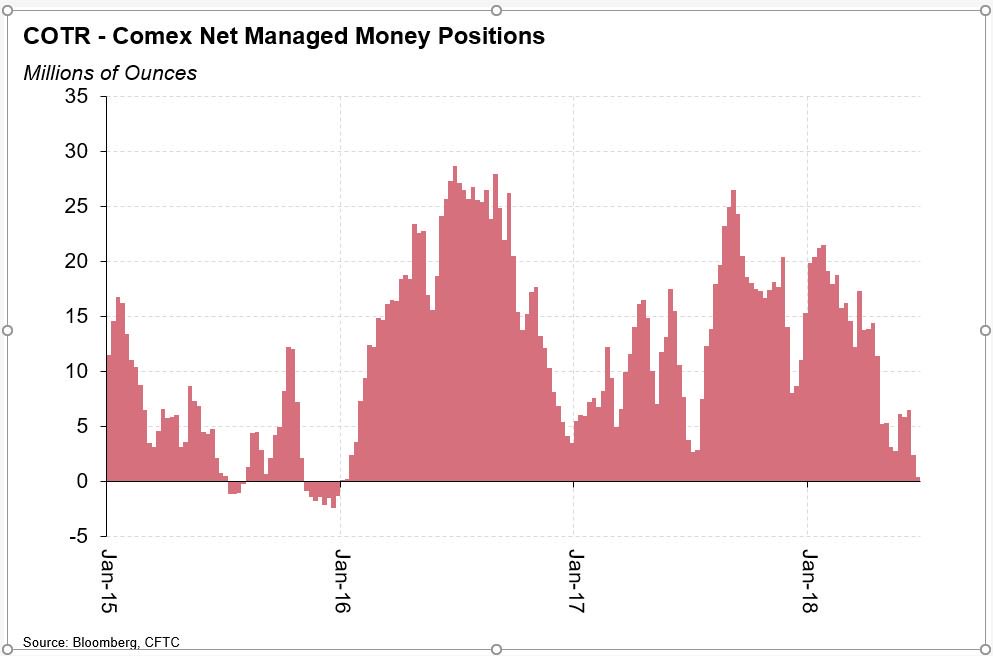

I am on my knees buying gold/silver/uranium miners with both hand this prior week (ouch!). Since the chart of the futures positions (COTS) is now more extreme–money managers are probably short now like back at end 2015/beginning 2016. I use the blog as a diary/bulletin board on occasion. I hate miners as a business but love the values. Note the vast underperformance of hard (read: miners) vs. financial assets (SPY). Not a recommendation, just a “diary” post.

Buying resource stocks has nearly nothing to do with the commodity. And near zero to do with management or country risk or interest rates or the dollar or what the DOW is doing. Those who are always wrong about markets spend a lot of time mumbling about all those things and they are just wasting ink.

Unbeknownst to GATA or the other PermaBulls who believe some munchkin at the Federal Reserve pulls the levers all of the time, markets go up and markets go down. They all do and they do it constantly. So if someone is telling you silver is the rarest mineral known to mankind and it should go up everyday of the week, forever, he’s lying to you in order to get you to pay for a subscription to his service. In short he’s like a bible thumping preacher or politician, he wants your support, and he specializes in telling you the lies you want to hear.

During the bull phase of the metals markets even the biggest piece of crap stocks go up. During the eventual bear phase of the metals markets even the best run with the most desired commodity in the safest jurisdiction goes down.

So investors in junior resource stocks need to keep two things in mind. You have to trade markets and take a profit when you can or the only alternative is to take a loss. I have had hundreds of investors tell me their biggest mistake was not taking a profit when they could. And given that something like 95% of investors in junior lottery tickets lose money, sell when you can, not when you have to.

You need to align yourself with the phase of the market you are in and let the wind be on your back. We had major lows in 2001 in gold and silver, again in 2008 and late in 2015. Don’t try to second-guess the market. If you were a buyer of anything from 2001 until 2008 you had a wonderful opportunity to profit. If you bought in 2009 or 2016, it was like shooting fish in a barrel. If you didn’t sell in March of 2008 or September of 2011, you got creamed regardless of the merits of the project or company. The phase of the market will either put money in your pocket or extract it regardless of what anyone says about a company.

A Discussion about Whether Austrian Economists and Value Investors Agree on How Intrinsic Value is Determined.

CSInvesting: Understand that Intrinsic Value is SUBJECTIVELY determined while prices are set by the marginal buyer and seller. All an investor does is compare price to value.

Essentially, value investing focuses on the comparison of a good’s intrinsic value and its market price and recommends investing in it as long as the asset’s value exceeds its price given a margin of safety.

The first article says in summary: value investing and Austrian economics are nevertheless incompatible, particularly given that value investing’s definition of value contradicts the Austrian value concept.

An Austrian economist who is also a value investor, Chris Leithner rebuts the above statement: “Value investors’ conception and assessment of value are congruent with the Austrian School’s.”

“A value investor” measures value by one of two methods:

First, he/she values a company according to the external prices of its assets. He/she observes, for example, that X Ltd owns quantity Y of land, and that such land has a market price of $Z per hectacre.

Second, the value investor makes plausible (based, perhaps, upon past experience and/or domain specific expertise) assumptions about a company’s future cash flows and, using some rate, discounts them to the present. He might do these calculations in his head or on a spreadsheet.

The Hinge between the theory of Value and the Practice of Value Investing.

John Burr Williams in his The Theory of Investment Value, 1938 wrote, “With bonds, as with stocks, prices are determined by marginal opinion…..Concerning the right and proper interest rate (discount rate), however, opinions can easily differ, and differ widely….Hence those who believe in a low rate will consent to pay high prices for bonds…while those who believe in a high rate will insist on low prices…Thus investors will be bullish or bearish on bonds according to whether they believe low or high interest rates to be suitable under prevailing economic conditions. As a result, the actual price of bonds….will thus be only an expression of opinion, not a statement of fact. Today’s opinion will make today’s rate; tomorrow’ opinion, tomorrow’s rate; tomorrow’s opinion, tomorrow’s rate; and seldom if ever will any rate be exactly right as proved by the event.

How then does Warren Buffett define and measure value? In his 1994 Letter to Shareholders he writes:

We (Charlie Munger and I) define intrinsic value as the discounted value of the cash that can be taken out of a business during its remaining life. Anyone’s calculation intrinsic value necessarily comes up with a highly subjective figure that will change both as estimates of future cash flows are revised and as interest rates move. Despite its fuzziness, however, intrinsic value is all-important and is the only logical way to evaluate the relative attractiveness of investments and businesses.

Graham, by the way, would agree with the definition of intrinsic value but he would doubt whether investors could usefully apply it. (Ben Graham, 1939) “The rub,” writes James Grant in the 6th Edition of Security Analysis (2009), page 18, “was that, in order to apply Williams’s method, one needed to make some very large assumptions about the future course of interest rates, the growth of profit, and the terminal value of the shares when growth stops.”

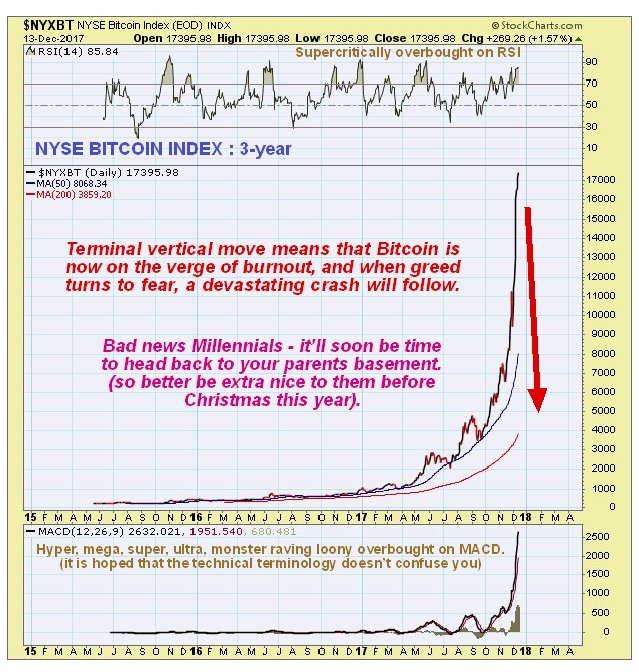

The video below–though choppy in the first few minutes–is worth hearing about the psychology of market bubbles. The interviewer of Bob Moriarty is ignorant of basic economics (Can prices EVER go below the cost pf producing a useful/needed product? Yes or No), but you can follow the discussion. Note the pushback of the interviewer who is also an owner of bitcoins to Moriarty’s questions. The psychology is fascinating–the will to believe and suspend judgment.

Other Comments

Bitcoin is up more than 2,000 percent in the last year and now trades above $17,000. Bitcoin futures trading launched this week on the Cboe exchange, gaining more than 19 percent Monday in the first full day of trading.

There are now 1,358 cryptocurrencies in existence, according to CoinMarketCap. Other digital currencies such as ethereum are better designed for programmable “smart contracts” and have quicker transaction times versus bitcoin.

Bitcoin’s scalability is another issue. There is technical limitation on how many transactions that can be processed at the same time. Partly as a result, widespread use of the cryptotcurrency for payments has not occurred yet.

So cryptocurrency investors must honestly ask themselves, is bitcoin really changing the word through blockchain technology innovation or is it mainly speculative asset? It’s the latter.

Kynikos Associates short-seller Jim Chanos, lauded for his prescient negative calls on Enron and Tyco, compared bitcoin to previous fads.

Bitcoin “is a speculative mania. It’s Beanie Babies,” he said at a Schechter event in Detroit, Michigan Wednesday, referring to the toy fad craze during the 1990s.

DoubleLine Capital CEO Jeffrey Gundlach criticized the lack of analytical rigor in the recent “nice round number” $1,000,000 price targets for the bitcoin, which is reminiscent of previous speculative blow-offs.

“I have no interest in this type of maniacal type of trading market,” he said on CNBC Wednesday.

Hedge fund manager Seth Klarman, the value investing giant who often draws comparisons to Warren Buffett, wrote in his classic “Margin of Safety” book an illuminating parable warning against speculation:

“There is the old story about the market craze in sardine trading when the sardines disappeared from their traditional waters in Monterey, California. The commodity traders bid them up and the price of a can of sardines soared. One day a buyer decided to treat himself to an expensive meal and actually opened a can and started eating. He immediately became ill and told the seller the sardines were no good. The seller said, ‘You don’t understand. These are not eating sardines, they are trading sardines.’

Like sardine traders, many financial-market participants are attracted to speculation, never bothering to taste the sardines they are trading. … trading in and of itself can be exciting and, as long as the market is rising, lucrative. But essentially it is speculating, not investing. You may find a buyer at a higher price—a greater fool—or you may not, in which case you yourself are the greater fool.”

Given the surprising US election outcome and the tumultuous market environment we wanted to connect with 321gold founder & editor Bob Moriarty for his latest thoughts on geopolitics and of course, markets. Bob obliged and this is an interview that you definitely don’t want to miss!

CEO Technician: Does the election result have any impact on gold and markets?

Bob Moriarty: I’m not sure it has any impact. Everyone wants to connect news with price movement and it just doesn’t work that way. We’ve been taught since we were two years old “the stock market went up today for reason xyz,” the financial news media needs news but the market goes up and down for many reasons and there is not a direct correlation between news and price movement.

I think Donald Trump is a fool but he’s not nearly as big of a criminal as Hillary Clinton. For whatever reason Trump’s surprise win sent precious metals tumbling and I see this as the real opportunity to load up and get aboard the train before it leaves the station. I will be buying silver on Monday.

CEO Technician: Russia is getting even more serious in Syria by moving their sole aircraft carrier to the region in order to assist in bombing “terrorist” groups. With Turkey moving land forces inside Syria and the usual cast of characters remaining very much involved in the power struggle inside the country and in Iraq next door, the situation doesn’t look like it could be much more dangerous. What’s next in Syria?

Bob Moriarty: Hillary Clinton got us involved in Syria. Syria is a completely different situation from Iraq although the two are often confused. Israel came out with a proposal in 1996 called “The Clean Break From The Peace Process,” it’s on Google. In this proposal Israel says it needs to destroy Syria and that’s exactly what they’re doing. It’s a plan that’s been in place for 20 years. The US is in Syria because of Israel but if you step back for a minute and ask yourself “what interest does the US have in Syria and why do we care who runs Syria?” the answer would be “we have no interest in Syria.” We are destroying the Middle East and the 65 million or so refugees from the Middle East are going to destroy Europe and the EU.

CEO Technician: The refugee situation in Europe is out of hand and Europe faces a terror threat from within its own borders of an unprecedented scale.

Bob Moriarty: If you’re in a village in Syria and someone comes in and bombs the shit out of you, then you do 1 of 3 things: You die, you leave, or you fight back. If there’s another option please let me know. When you leave you’re angry. Syria is a 7-dimensional chess match and there’s no good guys. The refugees are angry, by creating refugees we are creating terrorists. The key to solving the terrorist threat is to stop creating refugees.

A lot of people act like this refugee crisis isn’t going to come to the United States, of course it’s going to come to the United States. We need to stop bombing countries and creating refugees.

CEO Technician: I was at the New Orleans Investment Conference a couple of weeks ago and there were a couple of themes that stood out to me and I’m interested to hear your thoughts. Big discoveries are becoming extremely rare and the biggest investment profits come from big discoveries. Another theme of the conference is the idea that yields have bottomed and we are now in a rising rate environment.

Bob Moriarty: That’s correct. The last big discovery I can think of is Fruta Del Norte down in Ecuador and that was about 10 million ounce (20-30 million ounces over the long term). There are some big deposits of lower grade but those require several billion dollars to move into production.

Here’s what used to happen, the majors had big exploration teams and did a lot work themselves while partnering with high quality juniors. Suddenly 200-300 juniors skyrocketed to 1,500-2,000 juniors due to the evolution of the internet and the rapid access to information. It is more important than ever to distinguish high quality well run juniors from the rest of the crowd. I believe this is the best time ever to be a junior mining investor but you must do your research and pick the companies with top tier management teams. There is more opportunity today than there has ever been in history.

Yields have bottomed but you must remember that the Fed follows the market, not the other way around. Interest rates are increasing but with the entire world awash in debt and an extremely unstable financial system it will be an increase in interest rates that blows the whole thing up.

CEO Technician: What do you think about gold in a rising interest rate environment? I posted a chart last week on CEO.CA showing that over the last 40+ years gold has more often than not been positively correlated to interest rates. It’s only been in the very recent history (since the Global Financial Crisis) that we have witnessed a negative correlation between rates and gold.

Bob Moriarty: I’ll tell you something that few have the guts to say. Gold is expensive relative to other commodities (such as oil, pigs, platinum, etc.) because gold is the #1 real asset. The real interest rate environment is what matters to gold, if inflation is 4% and interest rates are 3% that’s a very positive environment for gold. Gold can do well in a rising rate environment but it’s the real rate of interest that matters.

CEO Technician: Any thoughts on lithium, cobalt, and renewable energy revolution?

Bob Moriarty: The key to lithium is how soon they can get it into production. Lithium is actually a very common element but we are having a revolution in energy storage. By 2025 solar power will be comparable in cost to coal and that’s going to create an absolute revolution, fortunes will be made between now and then. Cobalt is much less covered than lithium, if you can find real cobalt companies with legitimate projects I think you will do very well. There are way too many lithium companies and many of them will go away.

CEO Technician: We’ve seen the sharpest move lower in precious metals and mining shares in more than 3 years since Trump won last Tuesday night. Where are we at and is it time to buy?

Bob Moriarty: Trump didn’t win the election, Clinton lost it. There is a difference. If Clinton had read Nobody Knows Anything, she would have known to not trust the “Experts” and “Gurus” and the other fools. Trump has never worn a uniform or held a public office. He will either be the best president in US history or the worst. Flip a quarter and find out. This is the bottom and the buying opportunity in gold and gold shares, right now. I am buying silver this morning (Monday 11/14).

—

There is a time to buy, a time to sell and a time to do nothing. Now buying miners. Note the extreme swings in sentiment