Posted in Buffett, Investing Gurus, Investor Psychology, Risk Management

Tagged Humor, Momentum, Retail traders

This makes an interesting psychological study. Who holds the stock and how they react. ($CMG last at $278, down 14.5%) Many conversations below show no interest in discussing the valuation of CMG, but just the price (and if the price is declining, the pitiful management).

Also, note the focus on P/E ratio for valuation. What about the flaws in using P/Es as a valuation metric? No discussion about the business, cash flows or discount rate.

CMG will probably trade north of 6 million shares today or about 20% of the 28.5 million outstanding shares. Where are the long-term shareholders? One in five investors will sell based on one quarterly report.

If you have done your homework on valuation, then unreflective sellers who are throwing in the towel may mean an attractive price over the next few weeks.

I don’t know much about Chipotle, but management should be able to right the ship OVER TIME–the next 24 months–not next quarter. I don’t own any CMG currently.

Time to pile on (rats falling from the ceiling!): https://www.bloomberg.com/news/articles/2017-10-25/ackman-s-lost-a-lot-of-queso-on-his-stake-in-chipotle

An interesting article on the struggle within the turnaround efforts.

“Every chain restaurant, he says, goes through this rite of passage. For every success like Starbucks, there are former high-flyers like Baja Fresh and Boston Market that no longer have cultural currency and are slowly fading.

Moran (Chipotle founder) remains confident that Chipotle will not end up an afterthought dotting the strip malls of America, but he preaches patience. “Will we climb out of it and get back to our former greatness? I absolutely believe we will,” he told me in June. “But will that take a year or two or three or four? I don’t know. The full recovery from this is going to take a long time.” https://www.fastcompany.com/3064068/chipotle-eats-itself

Why does a burrito company trades for 70 PE.

Lots of room all the way down to 15 PE.

![]()

![]()

13 hours ago

![]()

13 hours ago

![]()

14 hours ago

16 hours ago

![]()

10 hours ago

20 hours ago

![]()

14 hours ago

![]()

16 hours ago

![]()

1 hour ago

![]()

4 hours ago

The battle line is drawn at $295 ps. Buyers must buy at this previously held level – otherwise, it is abandoned and a new lower strength level is found. But holding this level will be difficult as it represents a triple bottom.

My bet is that the shares go lower. Once the dam at $295 is broken, the selling will accelerate and we may end up the day at -20%.

![]()

23 hours ago

23 hours ago

17 hours ago

![]()

20 hours ago

![]()

13 hours ago

15 hours ago

![]()

16 hours ago

8 hours ago

![]()

19 hours ago

![]()

12 hours ago

![]()

39 minutes ago

Does “Momentum” Investing work with “Value” Investing?

See the research paper by Nicholas Barberis below. Barberis concludes that value and momentum are driven by biases that mirror one another. Value is driven by an overreaction problem in which humans are too quick to draw conclusions from a small amount of recent data. In contrast, momentum is driven by an underreaction issue, which is the opposite of verreaction. With underreaction, humans are slow to update their views based on new evidence, which could be due to a systematic behavior bias and/or due to the fact human beings simply have limited cognitive power.

A lot to ponder. I recommend Quantitative Investing by Wesley Gray. Momentum investing is NOT growth investing (buying price at high multiples to underlying fundamentals), because momenum investing is strictly based on recent price movements not fundamentals.

a model of investor sentiment or under and over reaction

and http://blog.alphaarchitect.com/2017/06/06/the-value-momentum-trend-philosophy/#gs.7NtEcq4

Momentum Mauled: http://www.acting-man.com/?p=29724#more-29724

When momentum stocks crack, this is what it feels like: http://youtu.be/go9uekKOcKM

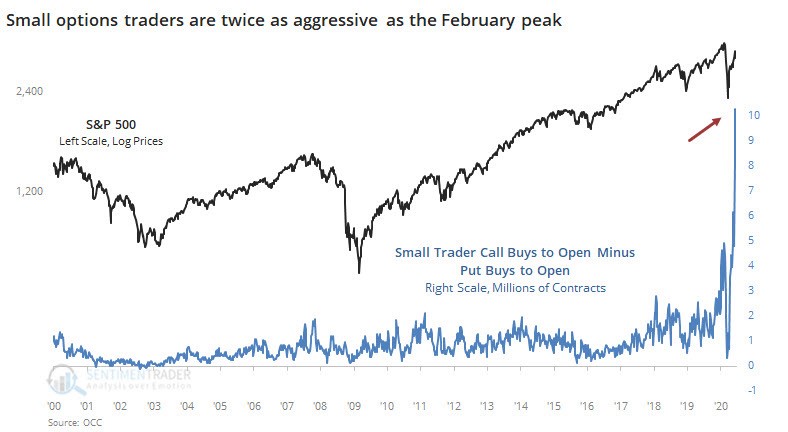

When retail investors blindly buy Yelp, Tesla, Concur Technologies, and IBB, I see:

A reader asked if ABCT was helpful in timing purchases or sales. I don’t believe so, but you see where the canaries are beginning to die in the coal mine. If artificially manipulated interest rates–through the Fed’s manipulating the value of the currency (The Fed monetizes the debt through “quantitative easing” which is just currency debasement/printing up fiat currency)–cause mal-investment, then you would expect to see the first cracks in the most over-valued areas of the market first. Note the collapse of sub-prime in 2007 before the general equity collapse in 2008/09.

Here Ludvig Von Mises(1881 – 1973) explains, “The boom can last only as long as the credit expansion progresses AT AN EVER-ACCELERATED pace. The boom comes to an end as soon as additional quantities of fiduciary media are no longer thrown upon the loan market.” Note that the Fed is “tapering” or buying fewer bonds with newly issued fiat currency. For the boom to continue, the Fed would need to VASTLY INCREASE the monetary madness.

This fractional reserve banking system allows banks to engage in credit creation by issuing notes and bank balances unsupported by any new wealth. Or the Fed simply creates the money out of thin air to purchase Treasury Debt from other individuals and institutions. Since money substitutes are created out of thin air, the whole process is a risky venture. On its face, such a practice would be fraudulent except that it has a legal basis whereby central banks give commercial banks the legal right to issue “counterfeit” money.

All the interference of free market prices by the Fed to lower interest rates just promotes business activity that would be uneconomic at normalized interest rates (read: a higher cost of capital). Can you be surprised when Tesla, Yelp or Pets.com (in 2000) are the first to plunge?

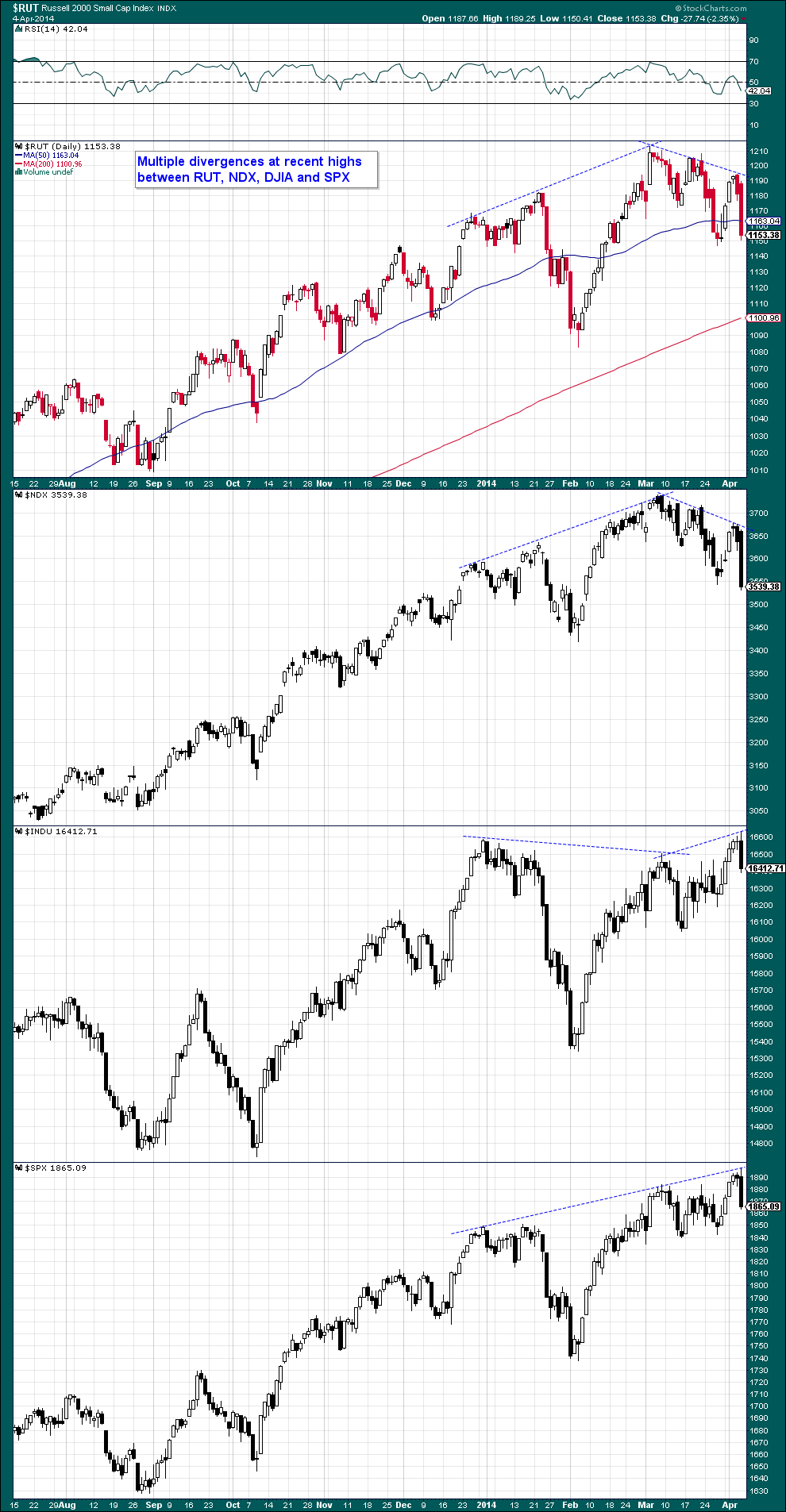

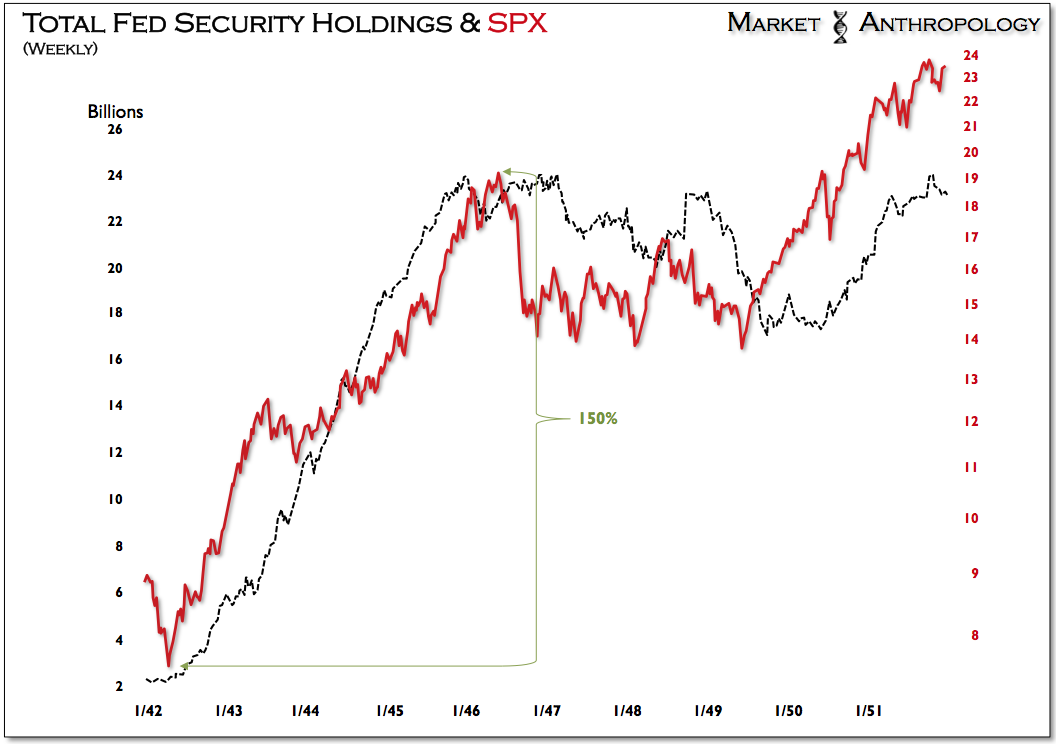

A great blog: http://www.marketanthropology.com/2014/04/a-staggered-start_7.html In the chart above, note the last time in the 1940s when the Fed was monetizing the government’s debt to pay for WWII.

Today:

from: www.tocqueville.com

“Whenever people agree with me, I always feel I must be wrong.”

I don’t know if Oscar Wilde was successful as an investor — or whether he was an investor at all, for that matter. But from my perspective, judging from the above quote, he certainly would have started with the right attitude.

Periodically, theories catch the imagination of the investing crowd about how the world works. At first, they intuitively make sense, then they seem to be confirmed by fancy academic literature and finally, they may be endorsed by prestigious experts. As they become widely accepted, these theories eventually turn into undisputed myths that, for a time, rule the investment world. But, just as often as not, many are eventually proven wrong. Distrusting such theories in principle thus seems a good idea.

The Efficient Market Hypothesis (EMH), which influenced professional investment thinking from roughly the mid-1960s to the mid-1990s, was one of those myths. Back in the 1930s and 1940s, research by Alfred Cowles had already indicated that most professional investors fail to outperform the market. Many subsequent, similar observations led to the broad acceptance of the Efficient Market Hypothesis in the mid-1960s, when it was proposed by University of Chicago Professor Eugene Fama and endorsed by economics Nobel Prize winner Paul Samuelson.

Without going into too much detail, EMH claims that prices on stocks, bonds and other traded assets reflect all the information publicly available at the time an investment is made. The corollary is that, over time, one cannot achieve returns in excess of average market returns— at least not without accepting more risk. And the implication is that you would be better off just buying an index fund designed to mimic “the market” or applying other supposedly sophisticated methods of diversification.

Although, as we will see, the Efficient Market Hypothesis has since been largely discredited, it left a legacy of practices (and the superstructures that thrive on them), which in my view generally hamper rather than improve the investment process. Among those are the Modern Portfolio Theory (MPT) developed by another economics Nobel Prize winner, Harry Markowitz, which aims to mathematically model what diversification between asset classes should be. The Modern Portfolio Theory itself gave birth to a whole industry of consultants, asset allocators, funds of funds and others which, as far as I can tell, more visibly added to management fees than to investment performance.

While picking on Nobel Prize winners’ contributions to investment science, we should not forget that Long-Term Capital Management, a fleetingly famous hedge fund that incurred 1998 losses so catastrophic as to require the intervention of the Federal Reserve, counted two Nobel laureates on its board. Of course, not all work by economics Nobel Prize winners is eventually doomed, but these examples vividly remind us that, in the realm of investments, there is a big and dangerous gap between theory and practice.

Warren Buffet was the first to convincingly challenge the idea that equity markets are efficient, in a May, 1984 speech at Columbia University. He documented that, over periods ranging from 12 to 18 years, nine successful investment funds, all of them managed by alumni of Benjamin Graham and using different tactics but following the same value investing philosophy, had all outperformed their market benchmarks by a significant margin.

Using a more recent period and a different list of ten funds suggested by Bob Goldfarb, of the Sequoia Fund, Louis Lowenstein, professor at Columbia University, made a similar point: “In the turbulent boom-crash-rebound years of 1999-2003 … every one of the ten funds outperformed the [S&P 500] index, and as a group they did so by an average of 11% per year…” (Searching for Rational Investors in a Perfect Storm – Columbia Law and Economics Working Paper No. 255).

Finally, in recent years, the rising influence of behavioral finance, which studies the often irrational behavior of investors, has again documented the likelihood that a rational investor can indeed outperform the market. As I mentioned earlier, this has helped discredit the Efficient Market Hypothesis and hopefully its sequels of falsely scientific disciplines.

Even though performance should be evaluated, there are two main caveats in using it:

It is important to judge managers on their stated investment philosophy, and on how disciplined they are in applying that philosophy. The alternative, i.e. relying solely on historical performance numbers without gaining a full understanding of how these numbers were achieved, may lead one to invest in or recommend Madoff-like schemes, as many professionals and consultants did. The Madoff episode is just a stark reminder that guaranteed returns, especially superior ones with the promise no risk, are a fool’s trap.

Volatility is a natural companion of superior long-term returns but it is very different from risk, which is the possibility of permanently losing one’s capital. Volatility, by contrast, is merely a series of shorter-term aberrations that, for serious investors, should be viewed as opportunities.

If volatility resulting from the cycles of crowd psychology is to be treated as a source of investment opportunities rather than as a “risk”, it is first necessary to acknowledge that the crowd’s consensus can be right: if everyone says it is raining outside, it is not wise to go out without an umbrella.

Second, it is important to distinguish between the momentum and contrarian approaches to investing. Briefly, the momentum approach sides with the crowd most of the time, in assuming that markets or even individual securities will continue to perform as they recently have. Rather, the contrarian approach assumes that the crowd is both poorly informed and overly emotional and therefore tends to be wrong on markets. The contrarian investor thus tends to take investment positions different from – if not opposite to — those of the crowd.

The irony is that momentum followers are right most of the time. However, while they are, they usually do not stand to make as much money as they hoped because the consensus expectations for the future that underlie the momentum approach (a continuation of the recent past) are already largely incorporated in the current prices for securities and the markets. In contrast, contrarian investors are right mostly at major turning points, after securities or markets have become grossly overvalued or undervalued. As a result, they are right less often but, when they are, they stand to make large profits or avoid large losses.

This is one of the most important rules of successful investing: It is not how often you are right that counts, it is how much you stand to earn if you are right or to lose if you are wrong.

This is why contrarian investing and value investing so often go hand in hand and why Tocqueville Asset Management elected to label its original discipline as “contrarian value investing”.

Author: François Sicart

—

Historical Newspapers Digitized.

Look what ONE individual did vs. a bureaucracy: http://reason.com/reasontv/2013/03/05/amateur-beats-gov-at-digitizing-newspape