The above post is an excellent tutorial and case study on riding a volatile, cyclical bull market in Uranium Company, Cameco (and others) from 2000 when CCJ traded about $7 to $8 until mid-2007 or about $40 to $45 (you never get the exact high). That is about a 27% compounded return over seven years. Buying near the low and selling near the high–isn’t that a fantasy. Not if you were following the fundamentals and the sentiment. The hardest part is holding on until it is clearly time to sell.

The article was written by https://www.uraniuminsider.com/ who did a great job on this article. I don’t know him or his newsletter, but I collated his articles in a case study below. I highly recommend you study the case below even if you avoid investing in cyclical, commodity companies.

The case also gives you a condensed application of the capital cycle.

Mr. Kaplan is the perfect investor to study to improve your investing in deeply cyclical resource investments and to understand gold. As Mr. Kaplan explains in an interview (2017): “Gold is not someone’s liability…. Economically, we are in unchartered waters.”

His philosophy is to start with a macro theme (A long-term bull market in gold) and then locate the best asset (Novagold) to leverage that theme. He considers gold the best risk reward of any asset class. Setting aside that gold is the best asset to own during financial crises, gold will be facing a severe supply crunch since no new large deposits over 5 million ounces are being discovered much less developed. Development from discovery to production requires over 20 years.

In addition, more and more foreign jurisdictions like the Philippines or Papua New Guinea are becoming too risky to mine. Mr. Kaplan estimates the equilibrium price to incentivize new discoveries is probably $3,000 to $5,000 per ounce. I think that is too low of a price.

The patience and conviction to be successful in this type of investing are extraordinarily high. Most professional investors cannot even pretend to be as patient. Mr. Kaplan became involved in Novagold during the crisis of 2009–imagine the fear and financial stress swirling amongst investors then.

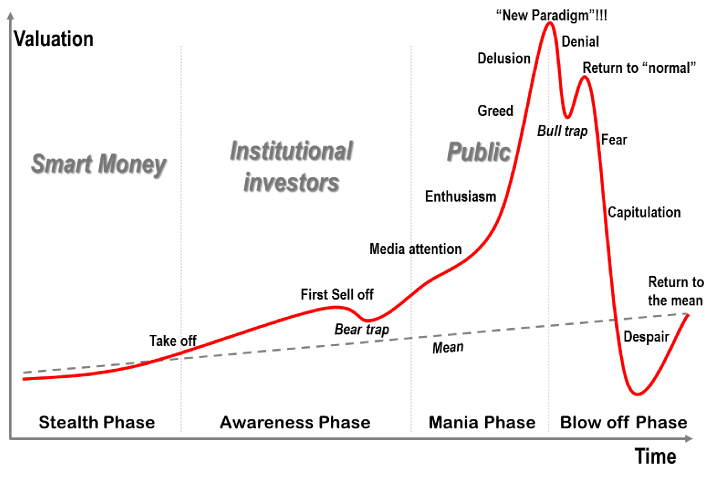

Recognizing the obvious: Intrinsic value rising well before price

From 2009 to 2019 the intrinsic value was rising as Novagold became de-risked. The decade ticked by as Novagold obtained all the required permits, it strengthened relationships with native communities, it spun off non-core assets like Galore (copper) to Trilogy, Novagold treasury increased its cash balance to $250 million with an annual cash burn of less than $10 million, and NG’s relationship with Barrick strengthened. Few cared or paid attention. Meanwhile, many jurisdictions have become even higher risk like the Philippines, Papua New Guinea, etc.

Price goes sideways while intrinsic value rises quietly. These are the best situations to hold onto. You just need VAST patience and to pay attention. Value accretion was occurring away from the financial statements. You would see expenses each quarter, but you would need to be aware of the permits won and the relationships strengthened. No algorithm or computer screening model will do that for you. But NG just traded as part of an index until decoupling in mid-2019. Everything related to Novagold was increasing except the share price until one day……. Meanwhile, Mr. Kaplan held fast because of his knowledge and conviction.

NG trades with the indexes, GDX and GDXJ, then decouples upward as price catches up with intrinsic value.

As a word of caution, this post is not a recommendation to buy Novagold even though I have been a shareholder since 2015. You should understand that Mr. Kaplan has been an investor for over 11 years through declines of 85% in NG’s share price. As an investor you might check on the statements and claims made in the annual reports listed below. If Novagold’s grade is considered outstanding, then look at the annual reports of five major miners and verify/check whether that fact checks out. Take nothing on faith so you can learn conviction.

How would you be willing to hold a investment without a huge payoff for over a decade while waiting for the market to turn to your analysis?

If you study those letters and annual reports, you will have a course in patient investing in a deeply cyclical industry and in understanding gold.

UPDATE 5/1/2020: 2008 Annual Report marks the entry of Electrum during the Great Financial Crisis.

2012 Annual Report began the time when management change had begun in earnest with CEO Greg Lang arriving from Barrick Gold as well as divesting of assets to focus on Donlin Gold. Those actions made the company into a perpetual option on the value of gold.

The Tortoise and The Hare Chairman’s Letter of 2015 explains why Thomas Kaplan was (and remains) bullish towards gold.

Please note how consistent Mr. Kaplan’s and Novagold’s message has been over the past twelve years. The Donlin project attributes remain consistent even while the resource base increases.

Remember that Novagold (NG) as a perpetual option is highly leveraged to the price of gold and to sentiment so expect prices swings of 25% to 50% or more. Such is the requirement to being a long-term investor. My secret is not to look at the share price but once a quarter.

Below is a case study of the capital cycle using Tidewater as an example. This page will be updated over time. This is not an investment recommendation but an ongoing case study.

Since Tidewater has been in business since 1955, its service is needed, but this is–at best–no more than an average business with no long-term competitive advantage. Currently, there is a trade-off between a decline in intrinsic value as time progresses without economic charter rates versus Tidewater’s competitive advantage over financially distressed competitors.

Update: 4/17/20

Tidewater filed to protect its $300 million in NOLs and $388 million in foreign tax credits. As an investor, you know that the NOLs can be worth more than $0 to worth a whole lot.

Meanwhile, Hornbeck (HOSS), a competitor filed for bankruptcy.

Update: 4/21/2020 US Crude oil near-term futures trade at a negative price for the first time in history. Natural gas is rising in price as shut-in oil wells reduce natural gas supply. What we are witnessing is a massive destruction of capital and productive capacity thanks to covid-19 and negative global interest rates. The future might require far higher oil prices. Near-term one would expect more pressure on TDW’s price because of the fear in hydrocarbon markets.

Update: 4/22/2020 TDW does not seem to be declining with oil prices–a divergence that may be signaling some change–perhaps investors are looking out at the supply destruction in oil.

4/25/20: Siem Management in their 2019 Shareholder letter move from hopeful to despair. (A good sign for Tidewater). These are dark days for the OSV industry and what you typically hear about in the depths of a downcycle.

The Siem Offshore is exposed to a number of risks. One of the most important risk factors is the demand for its services. The OSV market is now in its 7th year of depressed conditions and it has taken longer to recover than earlier expected. It is highly uncertain as to when charter rates will offer sufficient earnings for full debt servicing. The Company has been able to reduce its debt substantially over the last five years. Principal payment of debt instalments in 2019 was USD99 million (2018: 195 million). The significant debt reduction has been possible due to good cooperation between the Company and its financing banks, significant shareholder support, good ship operations and disposal of non-strategic and older assets. However, the significant excess capacity in the worldwide offshore service vessel fleet has increased the competition amongst owners for any vessel requirements, thereby depressing charter rates. The imbalance of supply and demand for offshore vessels is expected to remain for some years and will continue to put pressure on the charter rates and our cash flows. Five vessels were in lay-up at year-end 2019.

4/22/2020 OUTLOOK from Siem Offshore’s Annual Report. Despair!

The collapse in the oil price and the effect of the COVID-19 on the world’s economies have created a very different operating environment for our fleet. Field developments offshore are being cancelled or postponed by our clients and there will be much less work offshore during the coming several years. The demand for our services will therefore reduce rather than increase. At the end of last year, we looked forward to a gradual recovery in offshore activities and the nearing of balance in supply and demand in the OSV sector. That hope is now gone and we brace ourselves for a downturn probably worse than we have experienced during the past few years.

The actions required to achieve the best possible outcome when confronted with the market difficulties include consolidations between and among debt-burdened owners, such as practically all OSV owners in Norway. This is the time when owners should work together to embrace the opportunities to survive until the end of a long, dark tunnel of slow activity in the market for all of our vessels. Only by working together can the right scheduling and layup of vessels be achieved. The cost saving would be an added benefit. Most of our lending banks are lenders to several if not all of the competing OSV owners and are in the position to influence this required development. Disappointedly, the banks do not appear willing or prepared to assume this vital role.

The financial problems are currently solved independently within each company giving the owners more time to compete fiercely with each other, all to the benefit of the clients. Owners are seen to take higher risks as the clients take advantage of the desperate situations to shift operating risks from the clients to the OSV owners. The latter accepts the risks because they have nothing more to lose. Ironically, it is the banks who are exposed to the contractual downside in this new reality. This has created an artificial, unhealthy and unsustainable competitive situation in our industry.

May 17, 2020 Update. Tidewater currently trades at $4.13 or about 24% below its scrap liquidation value if we take Hornbeck’s bankruptcy filing as a guide.

Tidewater had 157 vessels operating at the end of the year. It took 4 of its active fleet to sell. So let’s take 150 vessels times $2 million per vessel (See last page on Hornbeck Bankruptcy filing below) for 300 million sales/scrap value then minus $85 million net debt for $215 liquidation value divided by 42 million shares or $5.11 per share. At $4.13, TDW trades 24% below this value.

I realize that the next twelve to eighteen months will be extremely difficult for TDW as it races to scrap excess vessels and conserve cash, but I don’t think it is a certainty that TDW will have to restructure it debt or declare bankruptcy again, but the market is pricing for extreme events ALREADY. The issue is whether to add on weakness.

The biggest risk is if financiers continue to throw good money after bad in this OSV industry. We shall see.

PRESENTS BEHIND-THE-SCENES DOCUMENTARY OF A DAY ON WALL STREET FROM OPENING GONG TO CLOSING OF THE DAY’S TRADING IN THE STOCK MARKET. FURIOUS PACE OF NEW YORK & AMERICAN STOCK EXCHANGES AND COMMODITY TRADING MARKETS AS LEADING BROKERS AND TRADERS EXPLAIN THEIR BUYING AND SELLING PHILOSOPHIES WITHOUT INTERRUPTING THEIR ACTIVITIES ON THE FLOOR. This covers the history of the stock market mostly from 1920 to 1960. Fascinating.

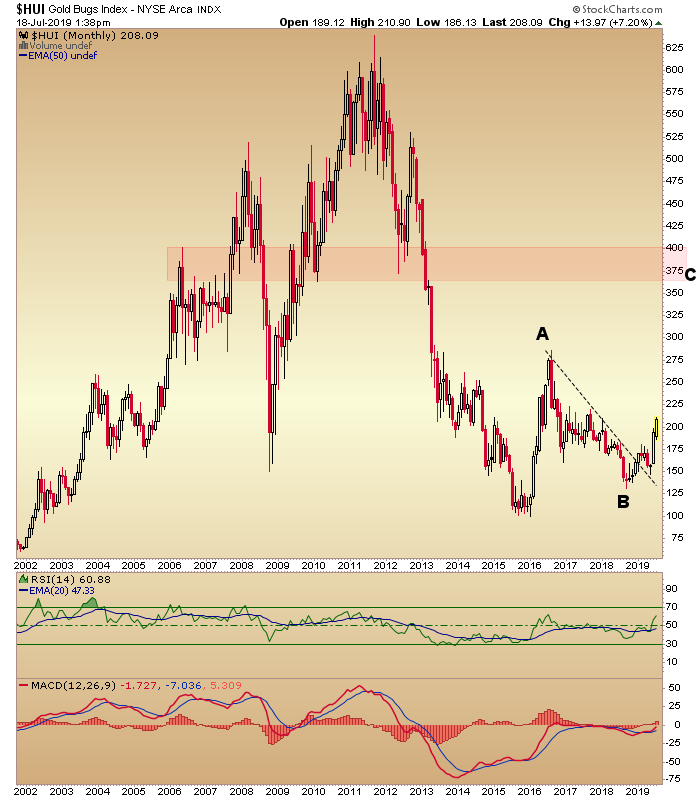

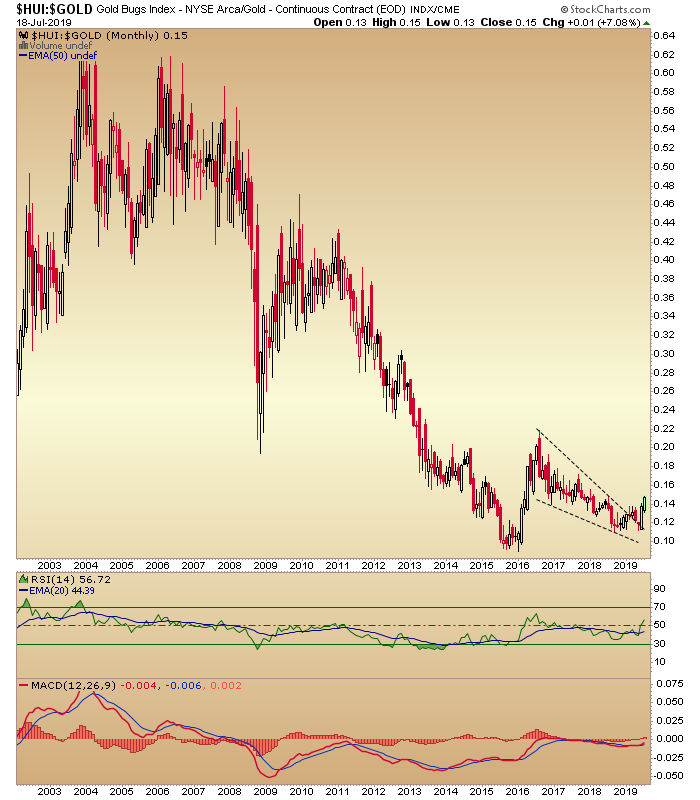

A forgotten sector comes to lifeMiners decline relative to gold as investors give up on poor capital allocation by managers who paid high prices at the top of the last cycle 2007/2011. But that has changed as the sector has been starved of capital for years. Go where they ain’t.A forgotten miner in an opaque market (Uranium). Eventually, the market MUST turn. An investor has to have a very (five years at least) timeframe for this market.

—

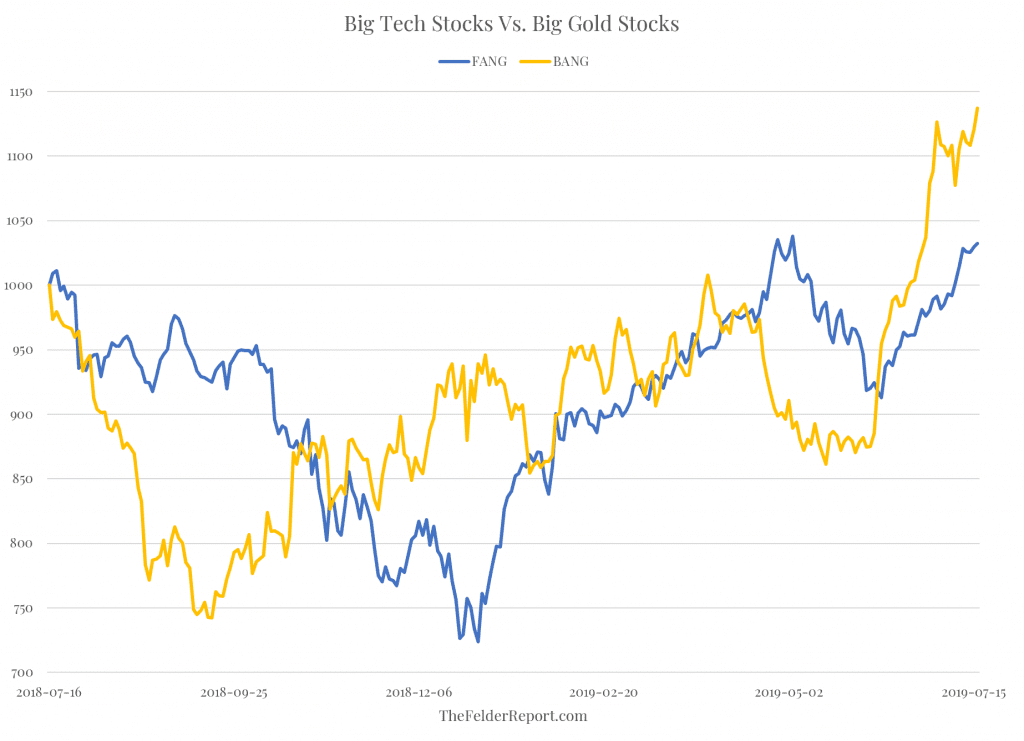

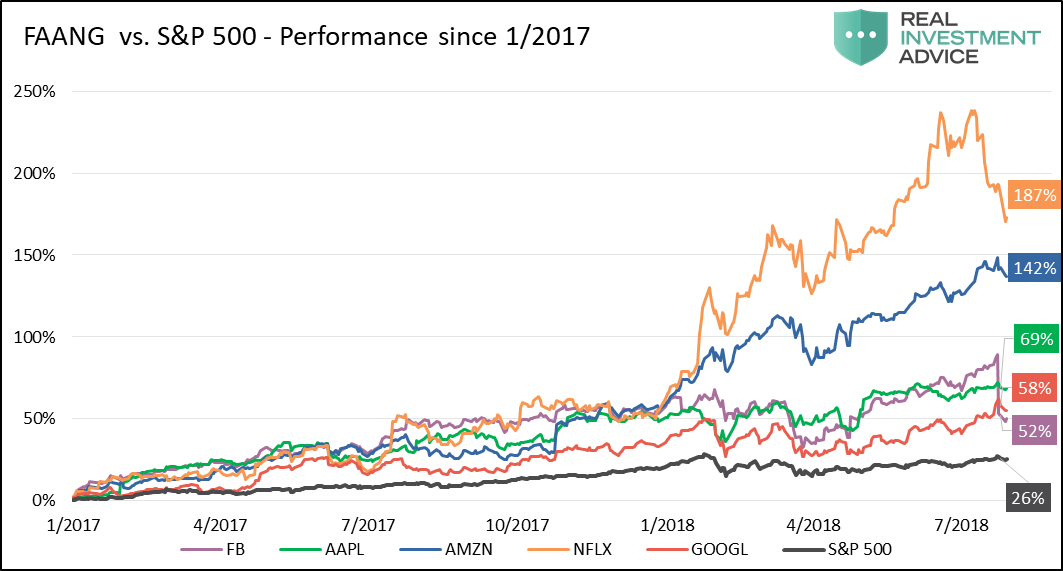

BANG stocks (Barrick, Agnico, Newmont and Goldcore vs. the FANG stocks–meaningless in the short-term but of interest to watch.

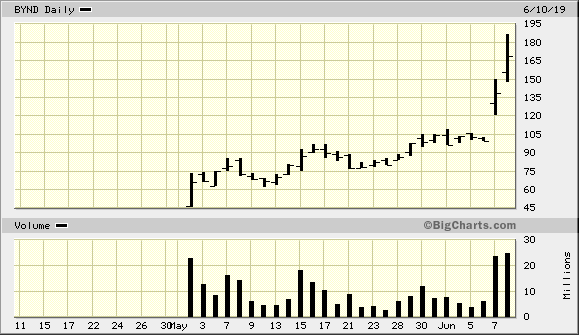

It’s the short squeeze of a vegan’s paradise. Shares of Beyond Meat (NASDAQ:BYND) jumped another 21% yesterday on an earnings beat, or really a loss beat, the company losing only $6.6 million on total net revenues of just over $40 million. The company now has a market cap of over $9 billion, and short borrowing costs keep rising. 51% of the company’s float is still being held short, which means the short squeeze can continue if the positions can’t be maintained, which would be especially relevant if the broader market starts to fall while Beyond keeps rising. There is about $800 million left in short positions on the stock. The short side is down about $400 million since January, while the stock is up about 650% since its IPO at $25.

—

Daniel Lacalle@dlacalle_IAQE is disinflationary because it perpetuates overcapacity and unproductive debt, yet it is massively inflationary on risky assets because the objective is to make rising government spending cheap. Hypernflation created in financial assets as sovereign bonds artificially inflated

My favorite book to recommend is The True Believer: Thoughts on the Nature of Mass Movements by Eric Hoffer. CSInvesting seconds this recommendation.

Review:

The book provides a concise and astute portrait of the personality type that is drawn to authoritarian institutions, whether political or religious. Hoffer makes an excellent case that the mass movements – the fascists, the communists, and the various brands of religious fundamentalists, that have caused so much death, suffering, and chaos throughout history in their attempts to impose their values and belief systems on others, have all depended on people of basically similar character to fill their ranks.

The true believer, as Hoffer portrays him/her, is someone who yearns for certainty and fears ambiguity; who sees the world in dualistic terms, black and white with no gray areas; who prefers to simply follow orders, letting others make the hard ethical decisions; who revels in belonging to an exclusive group and looking down on outsiders, particularly if they belong to a group the leaders have chosen as scapegoats.

Every voter should read this book and then look at the world today – the politics of fear and division, the growth of fundamentalist religion, the strident bigots on talk radio and TV – and then start working to reduce the danger they all pose to the freedoms in our Constitution, to the separation of church and state, and to our standing in the world.

— Back to Mr. Rosenberg…………

There is no discussion about investing in the book, but in my opinion, it is extremely helpful in understanding markets. It conveys the nature of human behavior in mass–how people act as a group. One of his great examples is explaining why people riot. There is no reason and no logic. People just get caught up in it. Riots don’t end all at once, they end person-by-person—that is markets. People panic in a group, but they come back to their sense one by one. That is why stock move incrementally the way the do.

CSIMA (Columbia Student Investment Management Association): How should they think about investment and time horizon?

JR: Young people today in business are much more macro-oriented than micro-oriented. They spend much more time on what is going on in Europe or Federal Reserve policies. They don’t focus much on company specifics. Even when they do they have a very low level of confidence in what they are doing. It’s very unfortunate. I hate that they don’t teach financial history in business schools. If it was up to me, I would make financial history and all history a number one requirement for business schools. Understanding how a spreadsheet works can be learned on the job easily but understanding the continuum of history requires certain intellect. I cannot for the life of me under-stand why business schools are not teaching financial history.

My advice to young people, if they really want to be successful in this business, is to learn financial history. Learn history in general and then dig deeper into financial history and you will not be in such awe of everything that’s going on. I see the same problem in my office. People just don’t know any financial history and they think that everything that is happening is unusual. Everything else can be learned on the job.

—

The Course on The Economics of the Great Depression

In this five-lecture course, Dr. Robert Murphy reviews the causes of the Great Depression, the response of the Hoover administration, and the New Deal. The focus is more on economic analysis rather than historical narratives, contrasting the Keynesian interpretation of various events versus the Austrian explanation in particular. Topics include the operation of the gold standard and the allegation that it inhibited policymakers from implementing the “stimulus,” Herbert Hoover’s supposed austerity program, the Friedman-Schwartz theory that the Fed’s unwillingness to inflate led to the severe downturn in the early 1930s, recent academic research showing the cartelization effects of the New Deal, and the myth of wartime prosperity. Dr. Murphy’s book, The Politically Incorrect Guide to the Great Depression and the New Deal, would be very helpful for students, but it is not required for the course. All necessary reading materials are provided.

Active Managers Horizon Kinetics Worth a careful read. Note the underperformance of several famous investors. Did they ALL become stupid at the SAME TIME?

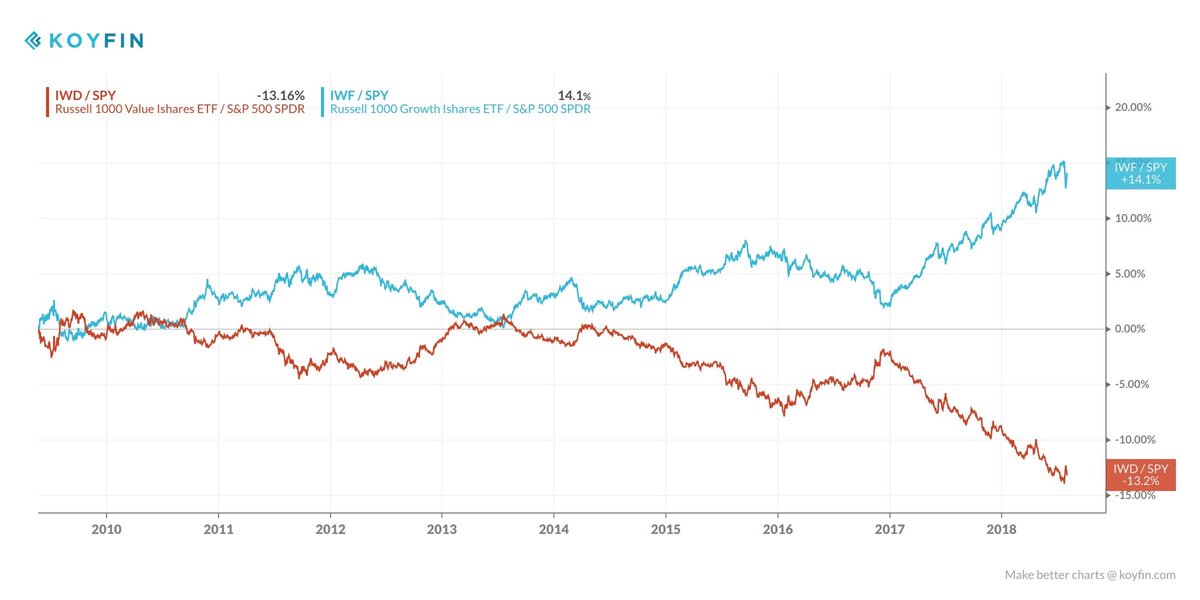

Perhaps a way to beat the ETF driven overvaluation is to search for companies that are in few indexes such as TPL or CVEO, for example. And search for owner-operated companies. Owner_Op_Paper With founder or owner-operated companies, there is less float so fewer of these companies end up in ETFs. When you see that Blackrock is a majority owner in a stock that you own but the stock represents only .003% of their five trillion dollar portfolio, you have a festering problem. Look for those founder led companies that treat shareholders fairly: