A reader worked diligently to create the Value Forum where it may be easier to discuss topics of interest.

http://forum.frenzel-herzing.com/

A reader worked diligently to create the Value Forum where it may be easier to discuss topics of interest.

http://forum.frenzel-herzing.com/

Course Review

Our goals in this course are to learn about investing, especially deep value investing through the book, DEEP VALUE by Toby Carlisle and supplemented by Quantitative Value by Toby Carlisle. Also, many original source readings will be provided to clarify and deepen our understanding of the primary readings. Also, we wish to be skeptical, independent thinkers who prove to ourselves what works and makes sense. We will be open to disconfirming evidence. We will question and help each other learn.

Below are the links in chronological order. The REQUIRED readings are in BOLD. Everything else is supplementary, but I hope you dig even deeper into the concepts and ideas.

OK, so after the chaos of postings and all the videos, you SHOULD have read:

The Preface and Chapter 2 in Deep Value by Tobias Carlisle (primarily supplemented by Chapters 1 & 2 in Quantitative Value). That’s it! All the other material is simply if you wish to go further or want greater understanding and reinforcement. For example, a student asked me what cost of capital would I use to discount the royalty earnings in the Munsingwear case study. If you dug into Margin of Safety by Seth Klarman, he would say to use your required rate of return. Try to find the answers from the investing greats and then determine if it makes sense to you. You should answer for yourself whether the returns to net/nets are due to higher risk or behavioral biases of other investors. Pose questions in the comment section of the blog if you have thoughts or other ideas.

You should after those readings have an understanding of why net/net investing generates superior performance. The returns are generated by the behavioral flaws of other investors. We should understand the concepts of Mr. Market and Margin of Safety. Investing is simple but not easy. Often temperament trumps IQ.

Next to read will be Chapter 3 in Deep Value.

There will be a review of the readings in another post. Our goal is to move DEEPLY and slowly through the readings. If you will notice all the other supplementary readings like Seth Klarman’s Margin of Safety, the Intelligent Investor, the SSRN research are from the footnotes of DEEP VALUE or Quantitative Value.

At the end of the week I will send out a zipped folder containing the books and materials collected for this course. Relax and don’t panic if you don’t have a book. I will email the folder to everyone in the Deep-Value group at Google.

I am sorry for the confusion, and I will strive to clarify.

Posted in Housekeeping, Uncategorized

The Buffett Partnership Letters were mailed out as a supplement for the reading we will do in Chapter 3 in Deep Value. Also, several keys were mailed out that should give you access to King Icahn, the book. One special project to find a better way to determine the cost of capital was sent as well.

UPDATE: I put those books in the DEEP VALUE folder and then mailed keys to EVERYONE in the DEEP-VALUE GROUP (at Google).

Later this week, we will review the readings so far and catch up. We should progress slowly, but I wanted to send out as many readings as I could since there are many people with different schedules so they can have time to go at their own pace.

First Quarter Earnings are on tap. Expect this

How to negotiate

Posted in Housekeeping

Where are the Customer’s Yachts? (1940)

For one thing thing, customers have an unfortunate habit of asking about the financial future. Now if you do someone the signal honor of asking him a difficult question, you may be assured that you will get a detailed answer. Rarely will it be the most difficult of all answers–“I don’t know.”

—

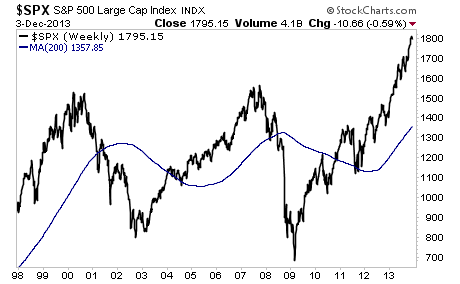

Today (Dec. 01, 2013) “As measured by the weekly Investors Intelligence survey of newsletter writers, the bullish boat is standing room only while the bear boat has the least amount of passengers dating back to the 1980’s. In today’s numbers, Bulls rose to 55.7 from 53.6 while the Bears fell to 14.4 from 15.5, an historic low in the history of this survey according to II. Combined with another record high in margin debt in October that puts its ratio to GDP at about 2.4%, near the high of 2.6% in July ’07 and 2.8% in March ’00 and it’s worth noting the historical limits in these two figures that we are pushing up against. That said, this says nothing about where markets go in the short term from here. This Fed hosted party can still have life left but I feel it’s always important to have perspective and these two data points should provide reason for an investing gut check in early 2014 in terms of how to be positioned.” www.hussmanfunds.com

“Being wrong on your own, as Keynes described so eloquently in Chapter 12 of the General Theory, is the cardinal crime of an investment manager. The management of career risk results in very destructive herding. Investors should be aware that the U.S. market is already badly overpriced – indeed, we believe it is priced to deliver negative real returns over seven years [GMO estimates fair value for the S&P 500 at 1100]. Be prudent and you’ll probably forego gains. Be risky and you’ll probably make some more money, but you may be bushwhacked and if you are, your excuses will look thin. My personal view is that the path of least resistance for the market will be up.”

– Value investor Jeremy Grantham, GMO, November 18, 2013

“I cannot look at myself in the mirror; everything I have believed in I have had to reject. This environment only makes sense through the prism of trends. You have got to be in things that are trending. Crashing is the least of my concerns. I can deal with that, but I cannot risk my reputation because we are in this virtuous loop where the market is trending. I may be providing a public utility here, as the last bear to capitulate.”

– Hedge fund manager Hugh Hendry, Eclectica, November 22, 2013

“I am out of justification to fight the uptrend. Up until now, I have had what I thought was compelling evidence to believe in the bearish case, but it has now been revealed to have been insufficient for the task. I am without ammunition to bet on the bears. I don’t like it, because I see the market as overly dependent upon the Fed’s largesse for its upward continuation. I see this as a bubble, but a bubble that is continuing higher even though it should not. I plan to ride the bubble for a while, and will hope to be able to succeed in reading the right [exit] signs.”

– Market technician Tom McClellan, November 26, 2013

In a classic case of not only locking the barn door after the horse is loose, but removing its best opportunity to return home, we’re seeing a capitulation by investment managers across every discipline, from technical, to value-conscious, to global macro. Historically extreme overvalued, overbought, overbullish conditions were in place even ten months ago, and my impression is that every further extension worsens the payback will inexorably follow.

Lesson: Don’t listen to gurus or “experts”. They are more apt to be wrong. Follow your own common-sense thinking. Right now RISKS ARE HIGH. BE CAREFUL.

Lessons in Entrepreneurship (Gary Hoover) http://www.today.mccombs.utexas.edu/gary-hoover-video-library/

My break

I have been so busy buying gold and miners that I haven’t had much chance to post, but I do plan to resume once things settle down (I hope).

I like this: buying bullion (gold/silver) at a 10% discount. Last time was 2001.

While being wary of this (in general). Go here: www.hussmanfunds.com

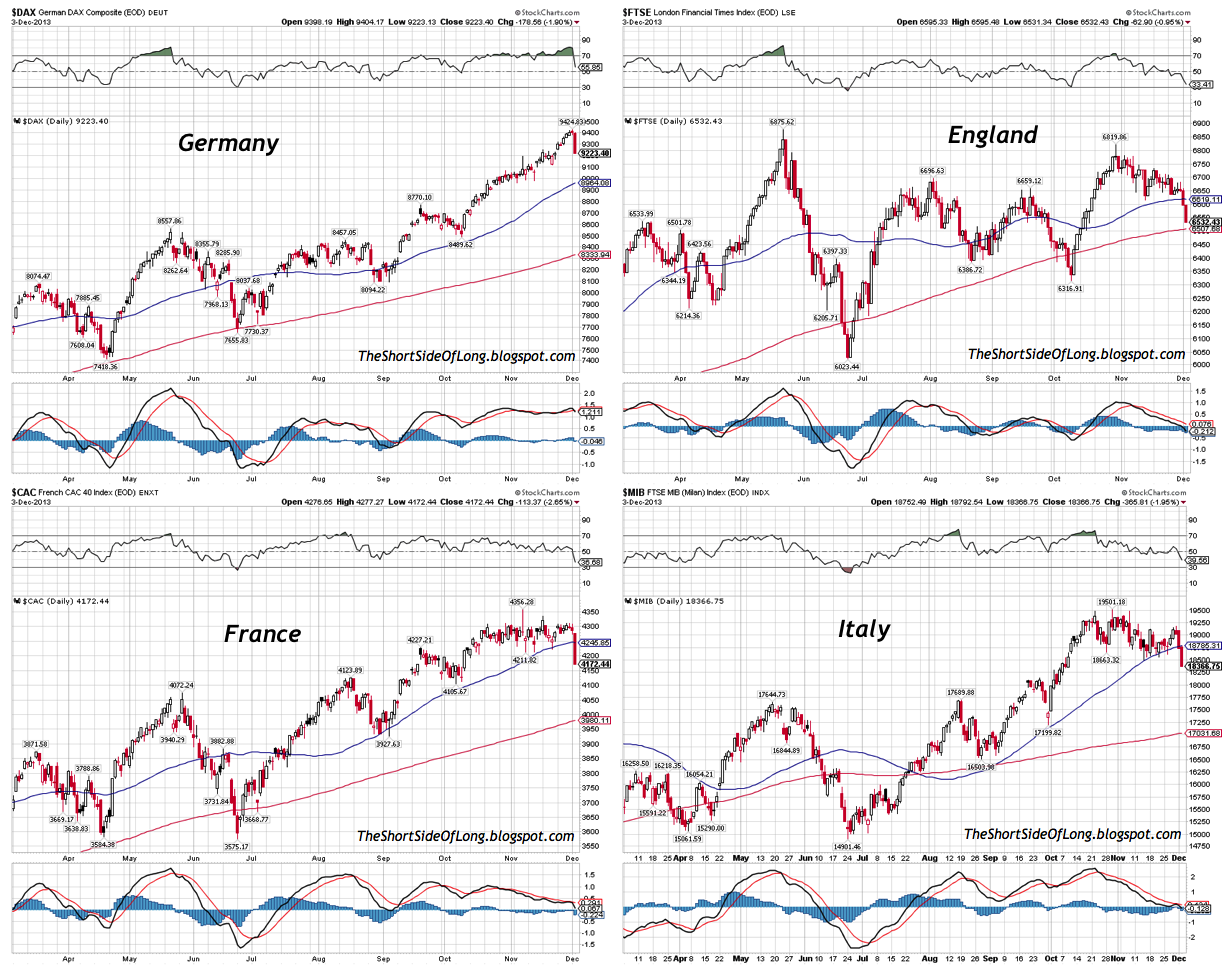

Note the early warnings signs—not all is well in Europe.

Jean-Marie Eveillard: “I just returned from Europe, where I was mostly in France, and the mood was not good there because the economy is not doing well. And since the economy is not doing well, there are political developments on the far-right and on the far-left….

“Some people, and I cannot blame them, believe that the establishment has failed them in the sense that the economy continues to do poorly.”

Eric King: “Jean-Marie, it sounds like there is a polarization happening in Europe where people are jumping on both sides and the middle-ground is being lost.”

Eveillard: “Yes, and usually it’s the middle-ground that governs. That has been the case in France where both the socialist party, which is currently in power, and the center-right party, both of them have historically been close to the center. That’s not the case any more.

They both have their own extreme wings, but it has been the center that has always governed. Now people believe that the ‘center’ has governed poorly enough that you have more people who are being seduced by the far-right, and the far-left.”

Eric King: “Does that worry you?”

Eveillard: “Yes, but, again, it’s a result of the establishment and it’s happening in the US as well. You have the center disappearing in the US, which means that both extremes on the left and the right will keep gaining additional audiences.”

Eric King: “This trend obviously has you worried.”

Eveillard: “It worries me particularly because in the US, France, and elsewhere, it’s Neo-Keynesian policies that are being followed because it’s the fashion of the day. Even though the Neo-Keynesians didn’t see the financial crisis coming, nevertheless they are still in power in academia, the political world, and in the world of corporate economists.

I ask myself, ‘If Keynes were alive today, would he be a Neo-Keynesian?’ I don’t think so. But the Neo-Keynesians believe, as Keynes did, that every now and then private sector demand is weak and has to be supplemented by public sector demand.

What we’ve had in the US over the past 5 years , both from a monetary and from a fiscal point of view, is the most stimulative economic policies ever — completely unprecedented. The printing of money, QE, etc, the budget deficit, the tremendous increase in government debt, and yet the economic recovery continues to be weak.

Now, the stock market is up sharply because some of the excess liquidity being created by the Fed is going into stocks. Some of it has also gone into things such as the real estate and fine art markets. But the money goes particularly into the stock market.

And the stock market is strong not just because of the excess liquidity, but because the vast majority of investors seem to believe, they are wrong, but they believe that, ‘Yes, we had a financial crisis 5 years ago, but that’s all over. We are going back to normal, and within a few months the economy in the US will grow at more than an annual rate of 2%.’

It hasn’t happened yet. How come it hasn’t happened yet? Nobody seems to be asking the question. It hasn’t happened yet because the medicine being prescribed by the Neo-Keynesians is not working. Incidentally, I don’t think anything will work because there no steps which can be taken by the politicians that would, almost overnight, result in a non-inflationary economy growing at 3% or 4% a year.

The reality is the steps which have been taken over the past 5 years will cause tremendous chaos and problems in the future, but we haven’t seen that yet.”

Eveillard also spoke about gold: “I believe that if I’m right, and the Neo-Keynesian medicine continues not to work, although they can continue with their QE, even at the Fed they know that quantitative easing cannot go on forever. So at some point something will have to give. That’s the point where investors will change their attitudes and move to gold. But it isn’t happening right now in the West because investors continue to believe the Neo-Keynesian medicine will succeed any day now.”

Eric King: “If there is this move you just described back to gold in the West, Jean-Marie, do you see new all-time highs in gold?”

Eveillard: “Yes, because gold will become the substitute currency. People will say, ‘I don’t want the yen, dollar, or the euro because they are all engaged in a race to the bottom.’ Yes, then gold will become the substitute currency. Gold will be money again. In a sense it never stopped, but 40 years ago the politicians decided that we were going to operate on the basis of a pure paper money system. But I can assure you that the history of pure paper money systems is not inspiring.” (www.kingworldnews.com)

CSInvesting: I don’t agree with everything said. Will gold become a substitute “currency?” Perhaps, more people will understand that Gold is the best money in the world (despite the raving over bitcoin or “token” money).

Posted in Economics & Politics, Housekeeping, Investing Gurus

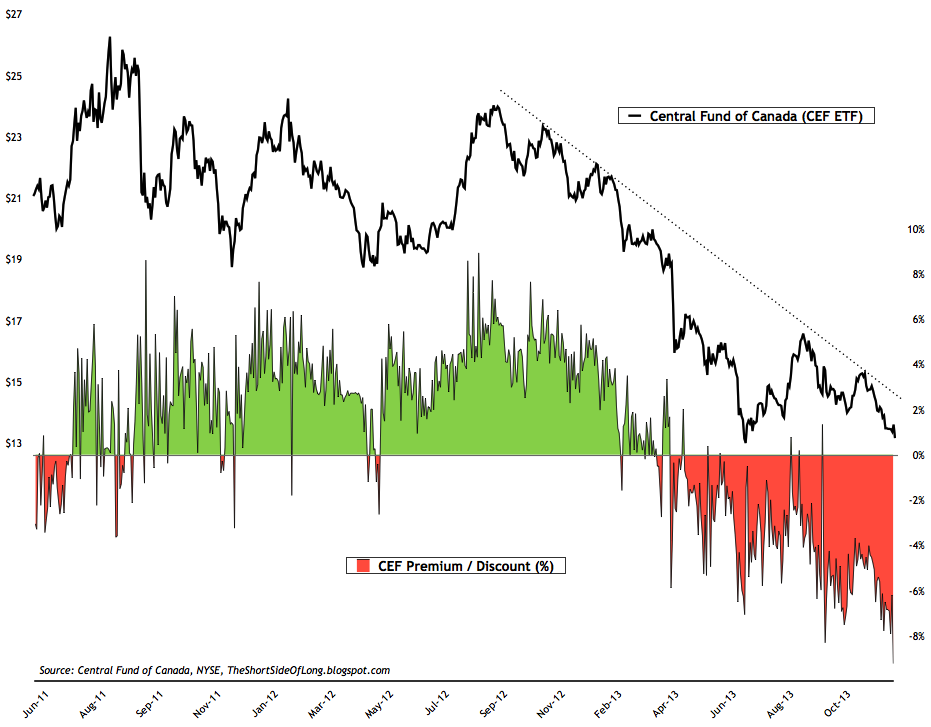

Tagged 1999, CEF, Contrarian, Entrepreneurship, Experts, Hoover, Market Bubbles, SPY

Yesterday’s $40 drop in gold. A gift.

Today, gold jumps back up $30. I have often wondered by gold bulls complain about “manipulators” slamming the gold price. Ah men! If someone wishes to make an uneconomic decision or force weak speculators to sell then they subsidize more rational buyers. Ultimately, for higher or lower prices, the fundamentals will prevail.

If gold is sound money with supply only changing about 1.5% a year then what causes such volatility? The amount of speculative hot dollars jumping from one pocket to the other.

Housekeeping

As I grind my way through writing the CSInvesting Handbook, I will not be posting much unless someone wants to share material. I hope to have another chapter in a few days. Thanks.

Posted in Housekeeping

Housekeeping

This weekend I will answer many questions such as: when to sell, suggested readings, and any other questions missed or buried within my email.

Free Courses

“We human beings always seek happiness,” says Mr. Zhang. “Now there are two ways. You make yourself happy by making other people unhappy–I call that the logic of robbery. The other way, you make yourself happy by making other people happy-that’s the logic of the market. Which do you prefer?” (http://bastiat.mises.org/2012/10/austrian-influence-china-and-the-wsj/)

The Blog is now www.csinvesting.org, a self-hosted site.

This blog has been moved to a self-hosting site so I can have more control over content and presentation. Slowly I am regaining my energy from surgery, so the blog will be back to normal shortly.

I will focus more on investing case studies and different investing problems than before. No one has complained, but political commentary detracts from the mission here which is to become a better investor through thinking critically and independently. I believe an effective way to learn is through understanding the principles and theory of investing then applying those principles to case studies. Finally, the investor must use his/her principles and investing methods to the opportunities available. As investors, we need a coherent investment philosophy and process that fits with our personality and skills. Only YOU can know yourself, but you can learn about investing here. Investing is simple but not easy.

VALUE VAULT for BOOKS

Below is a link for the Value Vault for BOOKS that contains or will contain hundreds of books. Think of this as a way to visit an investing library. There will other Value Vaults (posted links) for cases studies, videos, and articles. Each value vault is limited to 2 Gigs. Firefox’s browser can view the content but other browsers (I am told) show empty folders. Periodically new material will be added to each folder, so check back.

| Books (You can only download contents from this folder) |

|

||||

| Do you have anything to share? | |||||

More to follow……. |

|||||

Thanks to www.greenbackd.com/

[youtube http://www.youtube.com/watch?v=_VBGAeJ3eJM&w=560&h=315]

Read his transcript: Amit Wadhwaney TAVF Interview on International Value Investing

Ray Dalio on International Economics http://www.cfr.org/business-and-foreign-policy/conversation-ray-dalio-video/p28984

Thanks to a reader–Ray Dalio, founder and co-chief investment officer of Bridgewater Associates, L.P., discusses global economics.

This meeting is part of the Corporate Program’s CEO Speaker Series, which provides a forum for leading global CEOs to share their priorities and insights before a high-level audience of CFR members. The series aims to educate the CFR membership on the private sector’s important role in the policy debate by engaging the global business community’s top leadership.

Don’t panic if you are wondering what happened to the Value Vault. I moved the files. I will place the video files into separate folders and books into other folders. This should make for easier access and better organization. Though I go under the knife within two weeks, this will get done. Thanks for your patience. An email will go out to all Value Vault key holders with updates.

Many have been having troubles opening the Value Vault. The main problem is the size of the folder; there is a 2 Gig limit. Splitting folders means multiple emailing of keys. I get 10 requests a day so time constraints make this a hassle. Yes, there is Google, Dropbox and many other choices than Yousendit.com.

To make this blog more assessable for learning, I will post the videos up on this blog and the important books. All case studies, documents and more obscure books, I will place in a folder (less than 2 Gigs) or two and then email out all the keys.

This blog will no longer have advertising on it. The videos will have the corresponding case studies and financials for ease of study. Once that is up, you have about 10 valuation case studies with videos to develop your skills along with all the prior posts.

I have all your emails, so you won’t be forgotten when I email out the new keys. You will see the videos going up by tomorrow.

—

![]() I have been finally approved as a kidney donor so I wait for the date of my surgery. More blood samples, CAT scans and X-rays have been taken of me than any lab rat. Ready to go so the recipient doesn’t have to suffer dialysis or death.

I have been finally approved as a kidney donor so I wait for the date of my surgery. More blood samples, CAT scans and X-rays have been taken of me than any lab rat. Ready to go so the recipient doesn’t have to suffer dialysis or death.

http://www.mayoclinic.org/kidney-transplant/what-is-a-kidney-transplant.html

—

Your company has been given a concession to open a resort on the North coast of Cuba. What recommendation would you make to your investment committee? What should your required rate of return be?

Posted in Competitive Analysis, Economics & Politics, Housekeeping

Tagged Blog, blogging, business, Cuba, kidney donor, Transplant

I am back from my travels. Thanks for all the advice on storage and downloading services. I will read through and post your suggestions. The first order of the day will be building indexes for the various folders, so people can see what information they can request and download. Essentially these folders are like sections of a library that you should borrow from to learn more about investing.

The first index is of the Distress Folder:Distress

The folder has 7 books in PDF format on Distress Debt Investing, LBOs, Breakups, MBOs and 2 HBR case studies on bankruptcies. Many of these books were generously donated by readers. Thank you.

As always, if you would like access to this folder, please email me at aldridge56@aol.com with DISTRESS in the subject heading and within 24 hours I will email you a key.

I will be posting various indexes of folders each day until all the material is indexed. Perhaps, I will have the indexes on Google.docs so people can automatically become aware of any updates.

I’ll be back: http://www.youtube.com/watch?v=soYDuaurNKY