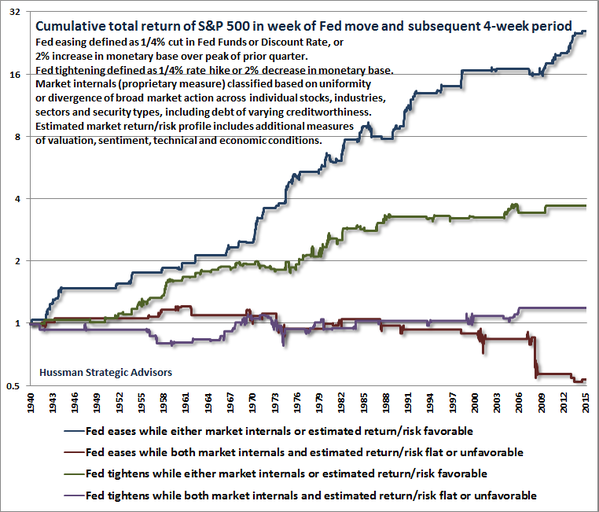

For the millions of investors in buy and never sell strategies today who look at the values on their statements today, trusting that the Federal Reserve will always cut rates and always flood the system with more cheap debt as though this were some sacred rite of passage for the American investor, I can only say two words. Wake up! Read more: BMI_TheBigNastyDWordIsHere_Sept22.15

You may not wish to become a short-seller due to the asymmetrical risk and reward, but you can certainly improve as an analyst to become more skeptical by taking on the viewpoint of a short-seller. Riders on the Storm or Short Selling An overview and primer. The best book yet that I have found: For those who wish to learn what a REAL BEAR MARKET is like then:

The only way to win a date is to become a hedge fund analyst. Your interview process requires you to analyze a real estate/mining company.

You look first at the balance sheet (Thanks Mr. Graham). You notice that this mining company bought claims under a ski resort (Park City, Utah) where it bought acres in 1907 at five dollars an acre.

Then you notice that the company issued 20-year corporate bonds when interest rates were 9% for AA corporates about fifteen years ago. Now similar companies can issue bonds at 5%.

How would you conduct your analysis? Good luck.

—

The End

So how will it all end? Dollars are created by computer key stroke when the Fed buys bonds, but the dollar is backed only by bonds (and a tiny bit of gold) and the bonds are payable in Federal Reserves Notes (the dollar) or just another form of debt. So debt is created to buy debt which, in turn, is payable in debt. Whoa?! No way this could ever be a problem. It’s magic. One thing bothers me, though, why do we need legal tender laws TO FORCE people to use dollars? I got a bad feelin’ on this.

But WHAT if more and more debt creates less and less “GDP” (let’s pretend it means something–govt spending creates economic growth, Ha Ha.) until each dollar of debt creates 0 or negative GDP growth. The Fed has to print to pay interest on the debt or the tail consumes the tiger.

Hemingway: We go broke slowly, then suddenly!

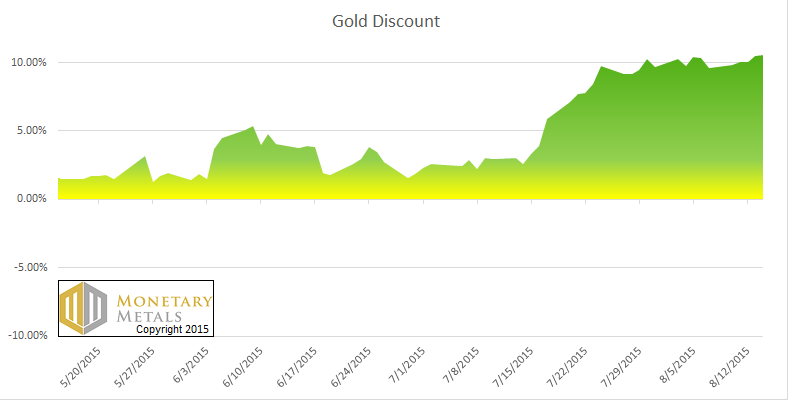

Anyone using CPI to gauge reality needs a reality check. You are a fool to buy gold as an “investment against “CPI inflation.” You own gold as a form of money to store wealth IF you lack confidence in central planning. So when it all comes down is when gold goes into permanent BACKWARDATION in gold. Holders of gold go NO BID on dollars. But don’t worry, the dollar derivatives like the Yen and the Euro will be earlier casualties. Meanwhile hope that the dollar rises against in order to buy more ounces. For others, Pray.

—

Now those who read the above my disagree, but know exactly fiat currencies do NOT go to 0 (or NO BID).

“I always thought I knew, from a distance, that business school was more or less a waste of time but then I actually taught at a business school so I’m pretty convinced it’s waste of time and money”

“Skepticism is something I try to teach my children”

“The largest creditor nations in the world are now in Asia … you have to have savings and investment to build an economy … even Karl Marx knew the importance of building capital “

The man himself famously started out by reading all the books in the Omaha Public Library with “finance” in the title. Over the years, Buffett took that knowledge and turned it into investing tips that have helped countless investors. The Motley Fool has even taken the best of Warren Buffett’s wisdom and packaged it in a new special report that you can get free just byclicking here now.

Today, we also have blogs that can make the learning process quicker. But with so many blogs out there on the subject of value investing, the quality of content varies widely. So here, in my opinion, are the 10 best value investing blogs for you to follow and what you can learn from them.

Contrarian Edge

Why you should follow it:Two reasons. One is that its author, Vitaliy Katsenelson, is a well-known value investor who’s been dubbed “the new Benjamin Graham” by Forbes. The other is the wonderfully eclectic nature of its content, ranging from insightful analysis of popular stocks like Apple and Amazon.com to musings on Tchaikovsky.

Philosophy: “I invest, I educate, I write, and I could not dream of doing anything else.”

ValueWalk

Why you should follow it:This site started in 2010 as a simple value-investing blog but has mushroomed into a popular site delivering breaking news, analysis, and syndicated content from other blogs. Expect multiple posts a day, as well as useful resources like a list of books recommended by Warren Buffett, Charlie Munger, and other gurus.

Philosophy: “Many academics claim investing is a random walk. We believe this to be partially true, but believe that value investing can outperform the market.”

Brooklyn Investor

Why you should follow it:Well, not for the design, which is old-school BlogSpot. The draw here is the supremely detailed posts analyzing individual securities, taking extracts from annual reports and investor presentations and explaining what they mean for investors. Even if you don’t plan to invest in the companies in question, the posts offer great insight into some good ways of researching a stock.

Philosophy: “Random Thoughts on Investing and Investment Ideas.”

The Aleph Blog

Why you should follow it:Asset manager David Merkel has been blogging since 2007, covering a range of different topics but accumulating almost 700 posts on value investing. He looks at both individual stocks and more general investing principles, and his posts are full of detail but easy to follow.

Philosophy: “To fight for what is right in money management, and encourage readers to pursue strategies that reduce risk and enhance returns.”

Wexboy

Why you should follow it:This blog spends a lot of time analyzing Irish stocks, which may not immediately seem useful to people from other parts of the world. But even if the companies are unfamiliar, the methods are classic value investing, picking through the numbers and trying to uncover value other investors have overlooked. And the breezy writing style makes it fun to read!

Philosophy: “I think the most valuable ‘skill’ any investor can wish for is a little dose of humility.”

Greenbackd

Why you should follow it: Author Tobias Carlisle runs a value investment firm and has some smart insights on value investing. His posts often introduce interesting research on subjects like negative-enterprise-value stocks and present them in a way that the rest of us can understand.

Philosophy: “Deep value, contrarian, and Grahamite investing.”

Value Investing World Why you should follow it:This blog takes a cerebral approach, bringing in a broad range of articles on investing and economicsthat are relevant to value investing, along with quotes from people like Seneca and Einstein.

Philosophy: “Promoting the multidisciplinary approach to investing.”

The Graham Investor

Why you should follow it: Posts here aren’t released very often — just once or twice a month — but they’re usually well thought-out. And the worth of this site lies not only in the blog posts, but also in the stock screens to help you find investments that meet the criteria proposed by famed value investor Benjamin Graham.

Philosophy: “I am generally a long-term value investor and try to use as many of Ben Graham’s principles as possible.”

Old School Value

Why you should follow it: This is a long-running blog with five years of value investing posts, some of them collected into series of tutorials that are a great way to learn the basics. Owner Jae Jun also writes very detailed posts analyzing particular stocks using a variety of valuation methods to show you how value investing works.

Philosophy: “Provide practical and actionable value investing tools, tutorials and educational material to help empower the individual investor.”

Long Term Value Blog

Why you should follow it: Some bloggers tend to trumpet their successes and gloss over their failures. This one is refreshingly honest, charting its owner’s real-life investing experiences and analyzing both what worked and what didn’t.

Philosophy: “Value Investing for the Long Term.”

Notice that www.csinvesting.org is off the radar. Good.

I started at page one [of these manuals-Moody’s and Value-Line] and went through every company that traded, from A to Z. When I was done I knew something about every company in the book.

I like businesses that I can understand. Let’s start with that. That narrows it down by 90%. There are all types of things I don’t understand, but fortunately, there is enough I do understand. You have this big wide world out there and almost every company is publicly owned. So you have all American business practically available to you. So it makes sense to go with things you can understand.

First, you need two piles. You have to segregate businesses you can understand and reasonably predict from those you don’t understand and can’t reasonably predict. An example is chewing gum versus software. You also have to recognize what you can and cannot know. Put everything you can’t understand or that is difficult to predict in one pile. That is the too-hard pile. Once you know the other pile, then it’s important to read a lot, learn about the industries, get background information, etc. on the companies in those piles. Read a lot of 10Ks and Qs, etc. Read about the competitors. I don’t want to know the price of the stock prior to my analysis. I want to do the work and estimate a value for the stock and then compare that to the current offering price. If I know the price in advance it may influence my analysis. We’re getting ready to make a $5 billion investment and this was the process I used.

You have to turn over a lot of rocks to find those little anomalies. You have to find the companies that are off the map – way off the map. You may find local companies that have nothing wrong with them at all

Most people get interested in stocks when everyone else is. The time to get interested is when no one else is. You can’t buy what is popular and do well.

I don’t look to jump over 7-foot bars: I look around for 1-foot bars that I can step over.

If we were to do it over again, we’d do it pretty much the same way. The world hasn’t changed that much. We’d read everything in sight about businesses and industries we think we’d understand. And, working with far less capital, our investment universe would be far broader than it is currently.

7 Gems from Buffet on Analyzing Stocks

You don’t need to be an expert in order to achieve satisfactory investment returns. But if you aren’t, you must recognize your limitations and follow a course certain to work reasonably well. Keep things simple and don’t swing for the fences. When promised quick profits, respond with a quick “no.”

There’s nothing different, in my view, about analyzing securities today vs. 50 years ago.

We favor businesses where we really think we know the answer. If we think the business’s competitive position is shaky, we won’t try to compensate with price. We want to buy a great business, defined as having a high return on capital for a long period of time, where we think management will treat us right. We like to buy at 40 cents on the dollar, but will pay a lot closer to $1 on the dollar for a great business.

Munger: Margin of safety means getting more value than you’re paying. There are many ways to get value. It’s high school algebra; if you can’t do this, then don’t invest.

If you’re going to buy a farm, you’d say, “I bought it to earn $X growing soybeans.” It wouldn’t be based on what you saw on TV or what a friend said. It’s the same with stocks. Take out a yellow pad and say, “If I’m going to buy GM at $30, it has 600 million shares, so I’m paying $18 billion,” and answer the question, why? If you can’t answer that, you’re not subjecting it to business tests.

Capital-intensive industries outside the utility sector scare me more. We get decent returns on equity. You won’t get rich, but you won’t go broke either. You are better off in businesses that are not capital intensive.

No formula in finance tells you that the moat is 28 feet wide and 16 feet deep. That’s what drives the academics crazy. They can compute standard deviations and betas, but they can’t understand moats. Maybe I’m being too hard on the academics.

7 Nuggets from Buffett on Valuing Stocks

When Charlie and I buy stocks which we think of as small portions of businesses our analysis is very similar to that which we use in buying entire businesses. We first have to decide whether we can sensibly estimate an earnings range for five years out, or more. If the answer is yes, we will buy the stock (or business) if it sells at a reasonable price in relation to the bottom boundary of our estimate. If, however, we lack the ability to estimate future earnings which is usually the case we simply move on to other prospects. In the 54 years we have worked together, we have never foregone an attractive purchase because of the macro or political environment, or the views of other people. In fact, these subjects never come up when we make decisions.

In 1986, I purchased a 400-acre farm, located 50 miles north of Omaha, from the FDIC. It cost me $280,000, considerably less than what a failed bank had lent against the farm a few years earlier. I knew nothing about operating a farm. But I have a son who loves farming, and I learned from him both how many bushels of corn and soybeans the farm would produce and what the operating expenses would be. From these estimates, I calculated the normalized return from the farm to then be about 10%. I also thought it was likely that productivity would improve over time and that crop prices would move higher as well. Both expectations proved out.

Intrinsic value is terribly important but very fuzzy. We try to work with businesses where we have fairly high probability of knowing what the future will hold. If you own a gas pipeline, not much is going to go wrong. Maybe a competitor enters forcing you to cut prices, but intrinsic value hasn’t gone down if you already factored this in. We looked at a pipeline recently that we think will come under pressure from other ways of delivering gas [to the area the pipeline serves]. We look at this differently from another pipeline that has the lowest costs [and does not face threats from alternative pipelines]. If you calculate intrinsic value properly, you factor in things like declining prices.

Investors making purchases in an overheated market need to recognize that it may often take an extended period for the value of even an outstanding company to catch up with the price they paid.

We use the same discount rate across all securities. We may be more conservative in estimating cash in some situations.

Just because interest rates are at 1.5% doesn’t mean we like an investment that yields 2-3%. We have minimum thresholds in our mind that are a whole lot higher than government rates. When we’re looking at a business, we’re looking at holding it forever, so we don’t assume rates will always be this low.

The appropriate multiple for a business compared to the S&P 500 depends on its return on equity and return on incremental invested capital. I wouldn’t look at a single valuation metric like relative P/E ratio. I don’t think price-to-earnings, price-to-book or price-to-sales ratios tell you very much. People want a formula, but it’s not that easy. To value something, you simply have to take its free cash flows from now until kingdom come and then discount them back to the present using an appropriate discount rate. All cash is equal. You just need to evaluate a business’s economic characteristics.

More Reading

Most of these quotes came from Buffett FAQ which contains the Q&A from shareholder meetings and goes beyond what you’ll find in the annual letters.

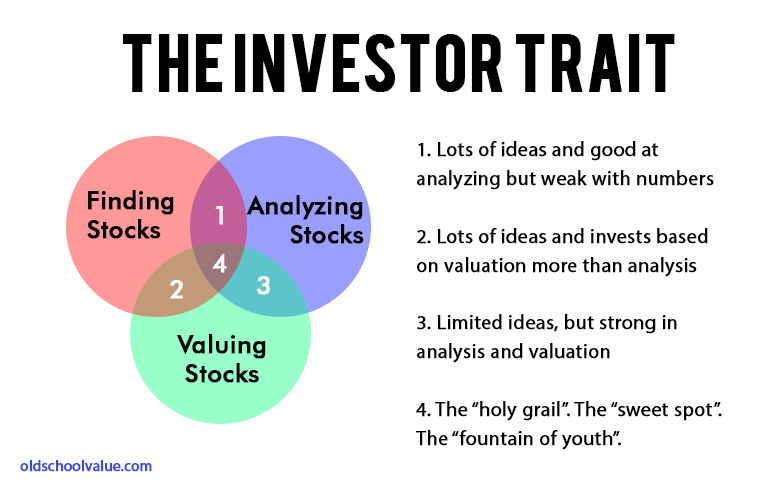

Just from these small selection of quotes, you can see how Buffett manages to dance in zone 4.

I’m writing this e-mail to ask for advice, as I value your opinion.

I’m 22 and graduated in Psychology. I moved to New York back in March as everyone said this was the place to be to get a job in finance. Since then I’ve been networking a lot, learning, and pretty much bugging every fund manager I’ve managed to get a hold on.

Attached you can find my current security analysis template; in Word and Excel (tables). I’d appreciate any feedback on anything to add.

I’m writing to you as I’m almost down to the penny (excluding my investing capital which is untouchable) and I need actionable advice. I’ve been crashing at a girl’s place in Brooklyn for the last 2 months and down to $400.

For write-up purposes, looking at equities, I still believe ESV and CLD are among the best plays.

ESV is currently the only driller making a profit and management has proven wise. It’s a good play for both safety and capital gains. The same could be said about CLD.

Looking at bonds, I haven’t analyzed them quite as much as equity opportunities since I can’t invest there yet. However, from a glance at the BTU bonds trading at around 34 cents and maturing on Nov. 15 18, they seem as potentially worth a closer look. BTU’s dominant size, presence and assets makes it unlikely to go through a disastrous formal chapter 11, so if it goes through an out of court restructuring or simply plows through, you’re seeing either full recovery or getting new equity in the restructured entity. It seems as a similar play to the equities I’ve looked at, albeit less secure. Can’t say the same on the BTU equity.

I would really appreciate any actionable advice you have for me. At this point I’m even willing to mow the lawn of whoever takes me in (funny, but true).

Thanks for reading such a long message, and thanks again for sharing your knowledge. Your advice and the Deep-Value group’s really helped me both intellectually and psychologically as I was feeling a bit bummed out.

John Chew:

Dear D (name withheld)

I am not quite sure what you are asking advice on:

Your investing templates, stocks, and/or job/career advice.

First, I did not post your templates here for others to see and comment on because of privacy, but I do think you put alot of effort and thought into constructing them. Just remember John Templeton’s advice to his analysts, “We want our analysts to adopt whatever approaches are appropriate to a particular situation.” Use your templates as a guide but don’t cut and paste.

There are many in the Deep-Value group with varied experiences who could give you their thoughts. I find it is hard to give advice not knowing the person well. The key is knowing yourself which can be difficult for a young person starting out. You seem to have a passion to learn and become an investor, so you are part way on your journey, but you have much to learn (as we all do). You have met other money managers and what has been the response? I can promise two things:

No one trains you on Wall Street and you have to show what you can do. In your case, that would be a well-written research report on a company or an industry to show an employer your through process and skills. You need time to develop your skills–about five years.

Do you need to be in an expensive city like New York or even work on “Wall Street?” I place Wall Street in quotes because I mean the investment business. Could you work as an assistant to a CFO at a small growing company? Would you think of working as a broker or back office clerk to get your foot in the door. You could work in a job to keep food on the table while you constantly build your skills and a track record no matter how small and keep networking. Francis Chou did this while he worked at a telephone lineman (Francis Chou) But again, easy to give advice while not knowing all your alternatives.

Perhaps think through EXACTLY what advice you want, but other people reading this can also provide their thoughts.

Cheer up, I remember being broke and staring up at the ceiling in an Indian brothel and wondering how the hell would I ever survive?

If you are seeking ways to becoming a master investor/analyst, the road is a long but rewarding one:

Can anyone understand the change in performance. Is it Einhorn’s process or the market? Hint: I don’t think Einhorn went from brilliance to idiocy or was it random luck? Comments welcome.