—

—

Posted in History, Investor Psychology, Search Strategies

Tagged CCJ, cyclical markets, Gold, gold miners, Psychology, Uranium

Two Investors

Two InvestorsIf you only read one post on this blog, then let it be this one. John Chew

Let me tell you the story of two investors, neither of whom knew each other, but

whose paths crossed in an interesting way.

Grace Groner was orphaned at age 12. She never married. She never had kids. She never drove a car. She lived most of her life alone in a one-bedroom house and worked her whole career as a secretary. She was, by all accounts, a lovely lady. But she lived a humble life. That made the $7 million she left to charity after her death in 2010 at age 100 all the more confusing. People who knew her asked: Where did Grace get all that money?

But there was no secret. There was no inheritance. Grace took humble savings

from a meager salary and enjoyed eighty years of hands-off compounding

in the stock market. That was it.

Weeks after Grace died, an unrelated investing story hit the news. Richard Fuscone, former vice chairman of Merrill Lynch’s Latin America division,

declared personal bankruptcy, fighting off foreclosure on two homes, one of which was nearly 20,000 square feet and had a $66,000 a month mortgage.

Fuscone was the opposite of Grace Groner; educated at Harvard and

University of Chicago, he became so successful in the investment industry

that he retired in his 40s to “pursue personal and charitable interests.” But

heavy borrowing and illiquid investments did him in. The same year Grace

Goner left a veritable fortune to charity, Richard stood before a bankruptcy

judge and declared: “I have been devastated by the financial crisis … The

only source of liquidity is whatever my wife is able to sell in terms of personal

furnishings.”

The purpose of these stories is not to say you should be like Grace and avoid

being like Richard. It’s to point out that there is no other field where these

stories are even possible.

In what other field does someone with no education, no relevant experience,

no resources, and no connections vastly outperform someone with the best

education, the most relevant experiences, the best resources and the best

connections? There will never be a story of a Grace Groner performing heart

surgery better than a Harvard-trained cardiologist. Or building a faster chip

than Apple’s engineers. Unthinkable.

But these stories happen in investing.

That’s because investing is not the study of finance. It’s the study of how people behave with money. And behavior is hard to teach, even to really smart people. You can’t sum up behavior with formulas to memorize or spreadsheet models to follow. Behavior is inborn, varies by person, is hard to measure, changes over time, and people are prone to deny its existence, especially when describing themselves.

Grace and Richard show that managing money isn’t necessarily about what

you know; it’s how you behave. But that’s not how finance is typically taught

or discussed. The finance industry talks too much about what to do, and not

enough about what happens in your head when you try to do it.

This report describes 20 flaws, biases, and causes of bad behavior I’ve seen

pop up often when people deal with money.

The Psychology of Money-9dbc86

The above article confirms my bias that all the MBAs, CFAs, CPAs, and study won’t help you unless you understand yourself. Tough. For example, I can see the speck in your eye but not the mud in mine.

Have a good weekend!

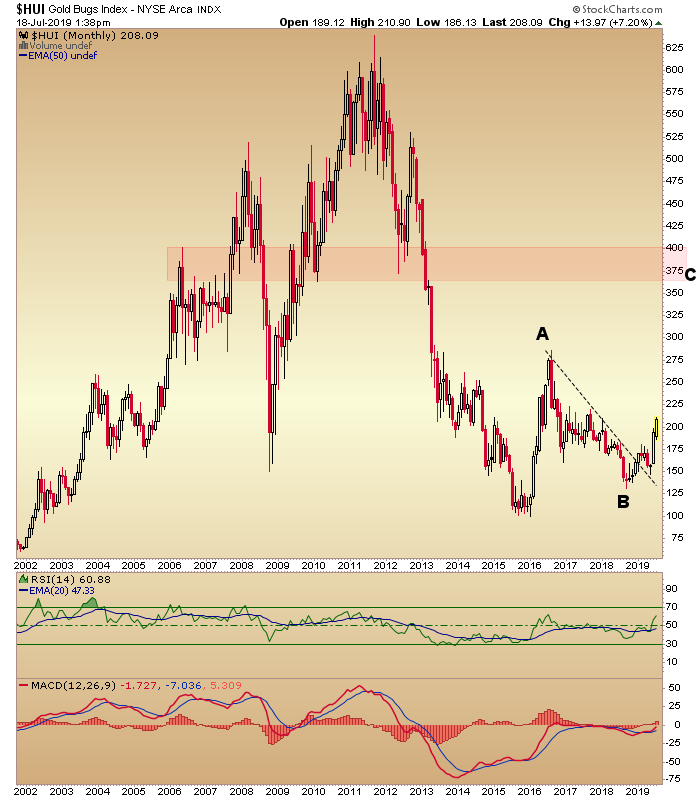

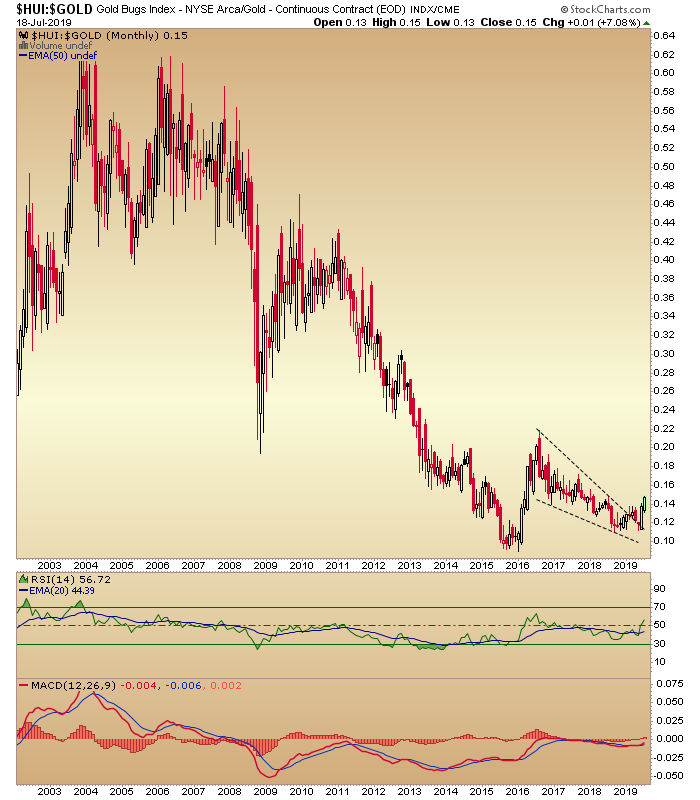

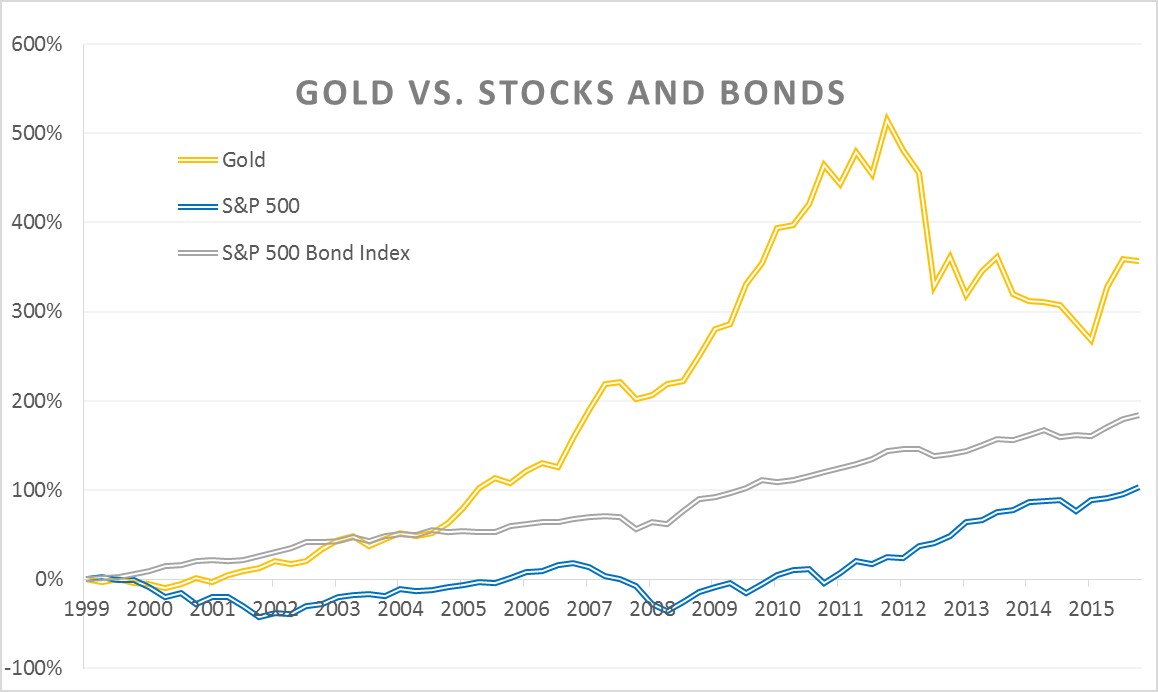

Nobody wants to be the bearer of bad news. Nobody wants to crush people’s dreams. But in the world of investing, cold, hard facts, not dreams, are what make you money. And the fact of the matter is, historically speaking, buying gold is the worst possible investment you can make.

I am very sensitive to the fact that what I just said has probably caused some readers to go apoplectic, and for that I apologize. I know that I will never convince the gold bugs, inflation hawks or doomsday preppers of this thesis, nor my own personal position that gold will eventually be worthless. But for the rest of you, let me lay out the case to avoid gold as an investment.

The Numbers Don’t Lie

In his seminal book “Stocks for the Long Run,” renowned economics professor Jeremy Siegel looked at the long-term performance of various asset classes in terms of purchasing power — their monetary wealth adjusted for the effect of inflation.

With a $1 investment each in stocks, bonds, T-bills and gold, beginning in 1802 and ending in 2006, Siegel calculated what those assets would then be worth.

Stocks were the big winners, growing the initial dollar investment into $755,163. Bonds and T-bills trailed dramatically, returning only $1,083 and $301 respectively. But the big surprise was in how badly gold fared during that time, only growing to $1.95.

An Inefficient Investment Vehicle

In addition to its miserable historical performance, gold also has many other failings as an investment, not least of which are the cumbersome and inefficient options available to own it and the prevalence of less than reputable salespeople in the precious metals space.

Owning physical gold in the form of bullion has many drawbacks. Wide bid and ask prices on physical gold ensure that the moment you purchase it you are already underwater on your investment. In addition, shipping costs for the heavy metal will further add to your cost basis.

Once you get your gold, you then have to decide how to store it. Keeping it at home exposes it to the risk of theft, fire or natural disaster. Taking it to the bank requires the rental of a safe deposit box, the cost of which will eat into your profit as well.

Firms will store your physical gold on site, but they charge for the service, and the idea of having your yellow treasure held by someone somewhere else, commingled with that of others, is not very appealing.

Ultimately, gold is a legacy investment vehicle from a time before mass communications, ease of global travel, and the internet. It no longer is the default store of value that it once was, and financial and technological advances have made it an investment best suited for collectors and hobbyists, but certainly not for serious investors.

For Full Article Click WayBack

Even money says this post attracts the GOLD IS DOOMED advertisement on the page

Editor: Too bad gold isn’t an investment but just money.

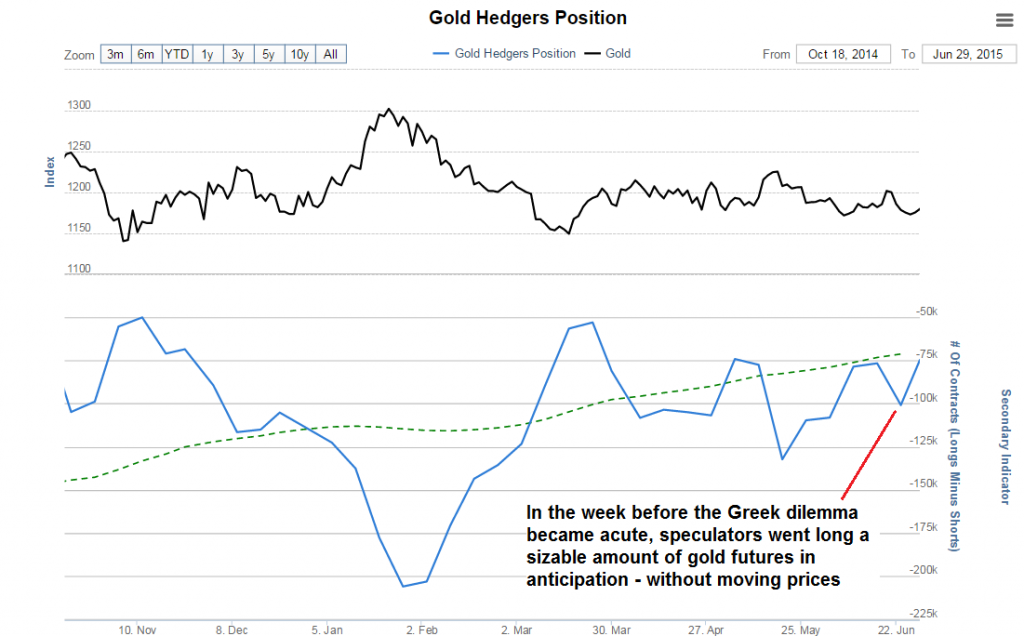

http://tocqueville.com/insights/gold-strategy-investor-letter-3Q16

Misconceptions about gold S&D

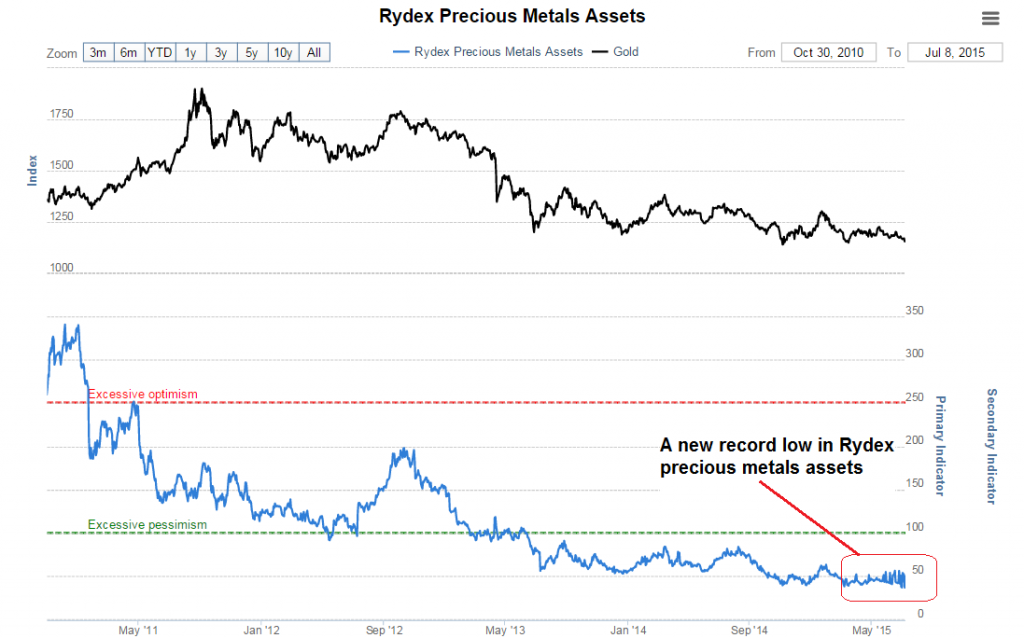

I just thought it would be fun to join the herd, band-wagon, chorus, and media for a change.

As you can see above, attendance was sparse this year at the New York Metals and Minerals Conference: http://www.metalsandmineralsevents.com/ehome/index.php?eventid=81632&

A Clue?

Time to dig in…………and uncover opportunity in the neglected, abandoned sector.

Studying Pre-Production Mining Companies

See videos: http://www.goldsilverdata.com/mining-101.html

https://www.explorationinsights.com/pebble.asp?t=150

http://www.sprottglobal.com/natural-resource-investing/site-visits/

http://www.sprottglobal.com/natural-resource-investing/investment-university/

How to read a technical report: Mining Fundamentals

Posted in Humor & Entertainment

Tagged Contrarianism, NY Metals and Mining Conference, Psychology

“The intelligent investor is a realist who sells to optimists and buys from pessimists.” ~ Benjamin Graham, Jason Zweig in The Intelligent Investor, Rev. Ed.

Editor: Great advice! Now, how do we act on it? See the articles below and view the short videos at the end of this post.

Look who bought Facebook:http://www.youtube.com/watch?v=wPvF97_q00s&feature=related OUCH! Please, no small children should see this video.

From www.marketpsych.com

As a psychiatrist I’ve born witness to many extremes of mood. I’ve tried to steer manic venture capitalists away from spending their life savings on cocaine and sports cars. And on the other extreme I’ve born witness to the deep pessimism and despair of suicidal clients, trying to help them choose life over oblivion. My efforts are not always successful, and I’ve learned a lot about the limits of rationality when faced with extremes of mania and despair. At both extremes many of the people I’ve worked with are highly intelligent and believe they are acting with perfect rationality. Yet despite their innate intelligence, deeper emotions occasionally sweep away their anchor to reality.

In Ben Graham’s quote above, one could be mistaken for thinking of the “intelligent investor” as a robot or algorithm. Human investors feel the extreme optimism and pessimism of the markets. And the effect of this optimism and pessimism is, almost universally, to bias their interpretations of real events. While the best investors feel the moods of the market (that is, they are empathic), they also have the almost super-human ability to act contrary to their emotional biases. Graham’s vision of intelligence in the 1950s is what we today call emotional intelligence.

Warren Buffett called Graham’s book, The Intelligent Investor, “By far the best book on investing ever written.” I think it’s worth looking for lessons in Graham’s thoughts on optimism.

Today’s letter will examine the nature of optimism in the financial markets: How we experience it, how it distorts our investing, how it plays out in markets, and how we can succeed while being both optimistic AND realistic. As we go through these themes, we will look at French and Dutch optimism in the Euro-zone, the delusional optimism at the launch of the Facebook IPO (see Dr. Murtha’s hilarious Part 2 video), how portfolio managers can use optimism to their advantage, and visit some tools and techniques for making ourselves better investors.

—

| Facebook Face-plant |

| It has been a sport in the media to level snarky criticism at the Facebook IPO. But if you’re a long-term investor you might appreciate that not every stock goes up. The IPO went reasonably well given its huge dollar size, massive trading volumes, and the usual banker conflicts-of-interest.What is most concerning to me is why anyone wanted to buy into the IPO, much less overvalued Facebook stock, especially after the shares were sold publicly. Apparently the marketers did their job well, and some of the uninformed investing public took an optimistic gamble.While most Facebook IPO investors had a “rationale” based on some sort of personal logic for their investment, we offer the following – the brain will make up a good ationale to justify us doing what we really feel inclined to do for EMOTIONAL reasons (i.e., Graham’s optimism). Who bought Facebook shares? Probably those who were excited, optimistic, and caught up in the hype. Trouble was, there were a lot of those people (MorganStanley didn’t get so big by products alone – marketing is key). Dr. Murtha created a humorous follow-up video to his popular first-take on the Facebook IPO. Part 1 showed what financial advisors are up against when talking to optimistic (and under-informed) clients. Part 2demonstrates the mind-bending effects of what we call “toxic optimism” or what the layman might call “sheer AWESOMENESS” as a client ponders Facebook stock.Please take a look at Part 2 and let us know what you think. |

| Researcher’s Corner: Optimism in the Markets |

| Given that Graham’s book has been available since the 1950’s, and he has many wealthy disciples such as Warren Buffett, we all know what to DO to make money investing – Buy low, sell high. Buy cheap, sell dear. Buy from pessimists, sell to optimists.But the reality is not so simple because WE are not so simple. “Buy from pessimists,” Ben Graham advises. But it’s fair for us to ask, “which pessimists?” And, “pessimistic for what reasons and for how long and …?”Researchers have found that optimistic investors make a characteristic mistake – they act as if good times will last forever. In a 2009 study, Sentiment and Momentum, co-authors Doukas, Antoniou, and Subramanyam found that small investors hold onto losing positions too long during optimistic phases in the stock market: “An analysis of net order flows from small and large trades indicates that small (but not large) investors are slow to sell losers during optimistic periods.” The researchers also found that during bull markets investors betting on the current trends continuing suffer losses: “Momentum-based hedge portfolios formed during optimistic periods experience long-run reversals.” These findings bolster the evidence for the “Confirmation Bias” – the tendency of optimistic people to believe information that supports their sunny outlook and discount information that contradicts it.On the one hand, what are we to do if a country or investment has been optimistic for years (e.g., 2003-2007) and then a shock occurs that causes a brief dip on fear (e.g., the credit freeze of August 2007)? In such situations, you don’t want to immediately buy on pessimism. Turning the Titanic of public opinion takes time. Best to watch from the lifeboat. On the other hand, as we emerge from the financial crisis, the brief periods of investor optimism (e.g., the spring rallies of 2011 and 2012) have been quickly followed by selloffs fueled by talk of imminent European financial apocalypse. In those instances, we DO want to buy from pessimists.One interesting investment simulation, based on our older ETF sentiment data, was buying fundamentally strong and low Joy/pessimistic ETFs (buying a good value from pessimists) and shorting fundamentally strong but high Joy/optimistic ETFs (selling a good value to optimists). In both cases we were looking at Fundamentally strong sectors (good values) based on investors’ perceptions. The returns of such an arbitrage of the 40 most liquid ETFs, with monthly turn-over, are below. This was only a quick study we did, there are likely much better variations possible:

|

| The above study implies that Graham was correct, the emotional component adds value to understanding fundamental valuations. Value strategies can be improved by adding psychological data on optimism and pessimism.We seem the same delayed effect in places such as Burma. There are more horse-carts than cars in Burma. There are loads of natural resources. There is huge potential for growth there, so no wonder investors are optimistic. And they should be. Over the long term the country will likely do very well and buying optimism may be short-term painful, but long-term rewarding in a place like Burma. |

| Overconfident? |

| The human problem with investing is that our perspective changes in reaction to the markets. Our moods shift as prices shift. Our time horizon lengthens or contracts based on our blood levels of stress hormones. Monday the markets are up and we are analytical long-term investors. On Tuesday Greece defaults, the S&P500 dives 7%, and we become traders.We’ve tested over 20,000 people in our free online personality testssince 2004. We’ve found some key indicators of overconfidence that correlate with lower reported investment and trading returns. Please take a personality test if you haven’t already before reading these results. EXTROVERTSPeople who are more Extroverted (outgoing, gregarious, and optimistic) are more likely to have lower overall investment and trading returns. This result is true in all three of our personality tests – businesspeople, investors, and traders – all report lower long-term returns in their line of business if they are extraverted. In one studyextroverts were more likely to gravitate towards short-term investing, thus increasing their risk of loss.MEN VS. WOMENThe last question on our personality tests asks: Comparing myself to other investors, I think my abilities place me: (users answer in ranges: “Among the top 5 percent”, “Among the top 10 percent“, etc…). We found that this question seems to speak to men’s pride, and women’s sense of humility. On average men rate themselves as better investors than women do. Yet men’s actual reported returns are significantly lower than those of women. This disconnect between men’s returns and self-perceptions is most significant in relation to risk. Men suffer significantly greater lifetime drawdowns than women. Men have more trouble resisting the temptation of a “sure thing.” Yet sometimes men actually find a sure thing. In those cases, men are more likely to sell out too soon – they have a shorter attention span when it comes to investing, perhaps because they take too much risk due to testosterone effects on risk-taking, and they are more easily shaken out by volatility.Short of taking a personality test, how do we know if our own optimism is excessive? – First of all, are you open to believing you are wrong? Excessively optimistic people cannot comprehend or objectively consider that they could be incorrect in their beliefs. “Of course Facebook stock will go up, it is AWESOME!” – Overoptimistic people do not look for contrary facts, due to the point above. – Overoptimistic people have no plan. What if volatility increases? What if the price drops 2% tomorrow? No contingencies are considered (again, see point 1 above). How do we get out of the over-optimism habit? – Use a system that requires you to check the potential downsides. Force yourself to look at objectively contrary information. – Use only objective criteria that are relevant. “Facebook is the third largest country in the world.” Is an interesting “fact”, but it is not relevant (nor is it accurate, obviously). To remain analytical, consider facts such as, Facebook has 955m users. Then figure the revenue from each. Then look at the growth rate of revenue. Those are facts. How many users does Facebook need to have, at the same servicing cost, for its P/E ratio to be 15 (that of Apple)? About 5 billion? How many people live on earth, again? Hmmm…. |

While most of this letter has been about the troubling effects of social and investor optimism, recall that individual optimism is a good thing – it stimulates resilience and can help us stay active and engaged. Furthermore, optimism can help us to see opoportunties when all around us are despairing and pessimistic. For investors, optimism is most critical to maintain when the world around appears to be falling apart.

Positive psychologists have found strong empirical evidence for several simple exercises to build our mental habits of optimism. Successful investors need to develop a placebo habit (seeing the opportunities) when others are pessimistic and a nocebo habit (seeing the dangers) when others are optimistic.

Just as our mouths emit an unpleasant if we don’t brush our teeth every day, so too will our attitudes become noxious without ritual cleansing. Some people use prayer, others use morning routines to get in the right headspace. Below are two exercises to help you quickly get your noggin screwed on straight. Practicing these once per day takes 2-3 minutes and improves quality of life dramatically, according to research.

1) Visualize your best possible self. Imagine yourself in your work in a state of peak performance. Next see yourself in at least one scenario involving achievement (e.g., executing an excellent investment) and one dealing with challenges (e.g., problems in an investment). Take on the peak performance attributes and imagine how you achieve. Then imagine how you work through the challenge. Close your eyes and visualize yourself with your peak performance characteristics for thirty seconds before reading on.

2) Create a gratitude list. Every day write three things you feel grateful for to a list. Each item should be unique. The simple act of thinking of three things you feel grateful for strengthens your sense of solidity and groundedness. Moving forward in your day, you are likely to think more creatively and proactively and with less vulnerability.

We have much more about these exercises in our books and training workbooks – please email if you’d like more information or to share experiences. Now let’s turn to one of our prior predictions, one we’re not happy about.

Video Part 1 of Facebook IPO http://youtu.be/-bXevO_gafg Funny but true

Video Part 2 of Facebook IPO http://youtu.be/KD2TBIKiJwM

—

The vault is under heavy construction. The folders that have been REORGANIZED are:

Grham, Price, Klarman and Buffett in the INVESTORS FOLDER

Greenblatt in the Investing Lectures Folder

Do not panic if you see folders change or disappear—when finished an email will go out to everyone that has sked for a key.

The farther back you can look, the farther forward you are likely to see.–Winston Churchill

Study history, study history, study history–Seth Klarman.

Contributing to….euphoria are two further factors little noted in our time or in past times. The first is the extreme brevity of the financial memory. In consequence, financial disaster is quickly forgotten. In further consequence, when the same or closely similar circumstances occur again…they are hailed by a new, often youthful, and always supremely self-confident generation as a brilliantly innovative discovery….There can be few fields of human endeavor in which history counts for so little as in the world of finance. Past experience, to the extent that it is part of memory at all, is dismissed as the primitive refuge of the those who do not have insight to appreciate the incredible wonders of the present. — John K. Galbraith.

Read the two articles below. The Death of Equities was written in 1979 proclaiming a perpetual bear market for stocks while the other, Why Stocks are Riskier Than You Think, was recently written on March 12, 2012. The point is not that these articles have no merit, but what are the illogical premises and conclusions in the articles? Can you think of at least three? What lessons of history can you learn?

http://www.businessweek.com/investor/content/mar2009/pi20090310_263462.htm

The Death of Equities: How inflation is destroying the stock market

Editor’s Note: The huge declines in U.S. stocks in recent months have revived interest in a Business Week cover story from August 1979 entitled “The Death of Equities.” At the time the story was written, the stock market had sustained serious losses and the long-term health of the U.S. economy was a significant concern. The story has aroused some controversy over the years, as the stock market staged a strong comeback in the decades that followed its publication. But few, if any, market forecasters were willing to call such a recovery at the time, and the story provides a telling look at how inflation had ravaged the market landscape—and investor psychology—at the close of the 1970s. So step back in time with us and read BW’s take on the state of the market in August 1979, as originally published in the Aug. 13, 1979 industrial edition of Business Week.

http://online.wsj.com/article/SB10001424052970204795304577221052377253224.html

Why Stocks Are Riskier Than You Think (March 12, 2012)

Most people can get the money they need for retirement without gambling heavily on equities, say Zvi Bodie and Rachelle Taqqu

If you can’t find at least three fallacies, then you will have to meet my Ex. Here she is: http://www.youtube.com/watch?feature=endscreen&NR=1&v=E55ni_xc4ww

Several fallacies from the two articles that you were asked to read are discussed in Howard Marks’ article: It’s Déjà vu All Over Again.

http://www.oaktreecapital.com/MemoTree/D%C3%A9j%C3%A0%20Vu%20All%20Over%20Again%2003_19_12.pdf

If two major business publications–Business Week and The Wall Street Journal–have articles with such muddled thinking then imagine what you encounter in your daily reading.

As Mr. Marks writes, “History amply demonstrates the tendency of investors and commentators alike to be pessimistic when the negatives collect, depressing prices, and optimistic when things are going well and prices are soaring. The lessons of history are highly instructive. Applying them isn’t easy, but they mustn’t be overlooked.”

Be on guard!

Posted in Investing Gurus, Investor Psychology

Tagged Death of Equities, Galbraith, Howard Marks, Media, Psychology, Zvi Bodie

Hard work pays off in the future. Laziness pays off now.–Steven Wright

Please take the following quiz. Listen to your intuition and solve the problems as quickly as you can—instantly or in under 2 seconds!

Quiz 1:

A bat and a ball cost $1.10

The bat costs one dollar more than the ball.

How much does the ball cost? ANSWER:____________

Quiz 2:

Try to determine if the argument is logically valid. Does the conclusion follow from the premises? Y or N?

All roses are flowers.

Some flowers fade quickly.

Therefore some roses fade quickly

—

Ok, now take a minute and go back and try to answer the questions with deliberate thought.

The answers and further elaboration will be posted tonight.