![]()

VALUE VAULT VIDEOS AND BOOKS

|

||||||||||||||||||||||||||||||||||||||||

|

![]()

VALUE VAULT VIDEOS AND BOOKS

|

||||||||||||||||||||||||||||||||||||||||

|

The first secret to success is discipline; the second is being able to buy or sell when almost everyone else is telling you to do the opposite.

Why the idea that miners can’t earn money at $1,200 gold is absurd.

Agnico Eagle reports third quarter 2013 results – Strong operational performance leads to record quarterly gold production and positive revision to 2013 guidance.

Miners are bottoming.

VIDEOS

Tonight when I have 30 minutes, I will post links to all the folders that contain videos so folks will have fresh links and one place to find them. Check back tomorrow.

Only 3% of All Money Managers See Gold Prices Higher in the Next Twelve Months! A contrarian’s wet dream.

http://www.acting-man.com/?p=26719#more-26719

Chetan Parikh, of India’s Capital Ideas Online, regularly publishes extracts from investment classics, to educate his readers and clients. In the early 2000s, he selected a 1971 speech by iconic investor David L. Babson. It is eerie how timely this speech, delivered 42 years ago, remains today. The italicized quotes below are from that speech.

I arrived in Wall Street in the spring of 1969, too late to be allowed to join in the late 1960’s fads and bubbles, but early enough to observe how complacency reined. Several well-known economists had proclaimed that the United States had “conquered the economic cycle”, and “Buy on weakness” was a widespread credo as it was believed that any market weakness would never last long. Yet, Parikh reminds us, the market’s postwar Bull Run, which had seen a 400 percent rise in the Dow Jones Industrial Average, came to an abrupt end in 1970. Between January 1 and May 26 of that year, the DJIA lost a third of its value, falling to its lowest level since the beginning of the 1960s. So, in 1971, Babson commented:

Asking the performance investors of the late 1960s what went wrong is like someone in 1720 asking John Law what went wrong with the Mississippi Bubble. Or in 1635 asking Mynheer Vanderveer what went wrong with the Dutch Tulip Craze. Nevertheless, this panel interests me because if we can identify what really did go wrong it may help to avoid a future speculative frenzy. And if we are serious about getting to the bottom of what went wrong then we ought to say what really did go wrong. So let me list a dozen things that people in our field did to set the stage for the greatest bloodbath in 40 years.

First, there was the conglomerate movement and all its fancy rhetoric about synergism and leverage. Its abuses were to the late 1960s what the public utility holding companies were to the late 1920s.

Already then, financial analysts and portfolio managers who had never themselves run a company were urging actual corporate managers to engage into mergers and acquisitions in order to boost reported results through growth synergies and cost savings from the merged entities. Very few of these conglomerations were lastingly successful. Yet, today, a new wave of “activist” investors is arguing for more share buy-backs, increased balance-sheet leverage and other gimmicks intended to give a short-term boost to reported earnings per share.<

Second, too many accountants played footsie with stock-promoting managements by certifying earnings that weren’t earnings at all.

At the time, for example, the then-legal “pooling-of-interest” method of accounting for business combinations allowed companies to acquire a business that had been growing very fast and to restate its own past record as if the two companies had always been merged. This would not boost the combined entity’s current earnings, but it would show the past record (and thus the implied quality of management) in a much better light. Few analysts would order and study five or six years of printed annual reports (no computers, then) to check if originally reported earnings were as good-looking as the “pooled” earnings as restated on the most recent document. I am ashamed to admit that I, too, got fooled once. But I don’t think I made the same mistake again.

Today, if a glamour company seems to show a lot of promise but does not have the level of reported earnings necessary to justify its stock valuation under Generally Accepted Accounting Principles, it simply convinces analysts to use other measures of “operating” earnings, where many expenditures or write-offs are simply not counted.

Third, the “modern” corporate treasurers who looked upon their company pension funds as new-found “profit centers” and pressured their investment advisors into speculating with them.

I am not sure if today’s treasurers are speculating or not with their pension fund assets, but many of them still use actuarial figures assuming that the pension fund portfolio will have an annual investment return of 7%-8%. Obviously, it will be difficult for a balanced portfolio to achieve these targets with interest rates as low as they are and stock market valuations (price/earnings ratios, for example) at levels that historically have not engendered high future returns. The result is that required contributions to the pension funds are understated and reported earnings are thus overstated.

Fourth, the investment advisors who massacred clients’ portfolios because they were trying to make good on the over-promises that they had made to attract the business in the first place.

Promises that will fool naïve, greedy of even fearful investors still proliferate in the advertising sections of the media, with claimed “guarantees” often of a dubious or unattainable nature. The imagination of promoters (including some presumably reputable ones) is inexhaustible, but the younger the investment market, the more alluring and more preposterous the promises generally are. Currently, the new class of Chinese investors may be among the most vulnerable prey to such schemes.

Fifth, the new breed of portfolio managers who churned their customers’ holdings on the specious theory that high “turnover” was a new “secret” leading to outstanding investment performance.

Envy and gambling are two of the biggest investment dangers. Many (maybe most) investors believe that there exist a few people out there, who “know” things and use methods that the general public is not privy to. These people eagerly bought asset-backed securities on the way to the subprime-mortgage crisis, for example, even as many of promoters of these products were privately making fun of the naïve buyers, as subsequently discovered e-mails have documented.

Recently, high-frequency trading, where computer-heavy organizations use algorithms to enter orders fractions of a second before more traditional traders, is again raising the allure of short-term profit seeking. Investors who may be tempted to engage in trading themselves often confuse highly successful investors, who are rare, and successful salespeople, who can make a lot of money fast but usually not for long. It is good to keep in mind the old Wall Street question:

“Where are the customers’ yachts?”

Sixth, the new issue underwriters who brought out the greatest collection of low-grade junky offerings in history – some of which were created solely for the purpose of generating something to sell.

Interestingly, I don’t believe the term “junk bond” had yet been invented when Babson spoke, nor had asset-backed securities been assimilated to higher-grade securities. But we know how all these more recent inventions turned out.

Seventh, the elements of the financial press who promoted into new investment geniuses a group of neophytes who didn’t even have the first requisite for managing other people’s money, namely, a sense of responsibility.

CNBC, which invented the style of presenting business news as if they were football or hockey competitions, was only launched in the 1980s and Bloomberg television followed as recently as 1994. Both all-day channels are voracious consumers of “expert” interviewees, but entertainment comes before information.

Eighth, the security salesmen who peddled the items with the best “stories” or the biggest markups even though such issues were totally unsuited to their customers’ needs.

I find it ironical that this disdain for what is appropriate for customers has further developed in earnest since regulatory agencies have imposed questionnaires defining investment styles (“conservative”; “growth and income”; “aggressive”, etc.). Questionnaires do not make people responsible – or responsive.

Ninth, the sanctimonious partners of major investment houses who wrung their hands over all these shameful happenings while they deployed an army of untrained salesmen to forage among a group of even less informed investors.

My recollection of old-style brokers, among whom I started my career, is that they were true professionals and decent analysts, who really knew a lot about the shares they recommended. Later, the proliferation of products, both pooled like mutual funds and synthetic concoctions full of derivatives, made it almost impossible for brokers to know each product from the inside, so to speak. As a result, it befell to marketing departments to create new products and organize their sale. Research became an assist of marketing and investment banking departments, with a shrinking freedom for sales people to exercise judgment.

Tenth, the mutual fund managers who tried to become millionaires overnight by using every gimmick imaginable to manufacture their own paper performance.

Actually, I believe this manufacturing of performance has become more difficult in recent years – one of the few areas where regulation may have visibly improved transparency. But consultants and asset allocators invented many other measures, often with enough Greek letters and complicated mathematical formulae, to confuse matters for neophytes.

Eleventh, the portfolio managers who collected bonanza “incentive” fees – the “heads I win, tail you lose” kind – which made them fortunes in the bull market but turned the portfolios they managed into disasters in the bear market.

The fashion in recent years of participating fees, where managers share in the realized portfolio gains, was made popular by hedge-fund and private-equity partnerships. It can be extremely profitable for managers that experience a winning streak of five or ten years, since they receive a share of the gains they have realized without putting much of their own capital at risk. On the other hand, it carries some dangerous features for shareholders. If a manager has had a bad investment period, for example, the incentive to accept disproportionate risks to make up for poor prior results must be high. This kind of “double or nothing” temptation is obviously not in the best interest of clients.

Early hedge or private equity funds offered access to special skills, either in research or in types of investments. More recently, many investment funds have adopted the fee structure without offering either special skills or unusual investment opportunities.

Twelfth, the security analysts who forgot about their professional ethics to become “story peddlers” and who let their institutions get taken in by a whole parade of confidence men.

I believe that most analysts are honest people. But the top management of Enron may have said it best when, before being convicted for fraud, they reportedly described financial analysts as glorified stenographers.

Babson concluded:

These are some of the things that “went wrong”. But for those who stuck to their guns, who tried to follow a progressive but realistic approach, who didn’t prostitute their professional responsibilities, who didn’t get seduced by conflicts of interest, who didn’t get suckered into glib “concepts,” nothing much really did go wrong.

As in earlier periods of delusion most investors tried so hard to be “smart” that they lost the “common sense” that pays off in the long run.

François Sicart*

October 12, 2013

*With considerable help from David L. Babson and Chetan Parikh

Author: Francois Sicart

Investor_Presentation_05-14-2013

Buy, Sell, or Hold? Why? Is this a good business? Can costs be passed through to customers? Is growth profitable?

Wrong answers will result in: http://youtu.be/6eXFxttxeaA

Free On-Line Finance Course from a Nobel Prize Winner: http://oyc.yale.edu/economics/econ-252-11#sessions

Posted in Risk Management, Search Strategies, Valuation Techniques

Tagged ABFS, Case Study, Schiller

A Reader’s Question

I was taking a look at Prof. Greenblatt’s lecture notes and have doubts with Duff and Phelps case. Can you help me?

EBIT of $43.72 x .6 for taxes = $26.23 x 13 P/E = $341. I shrank the number of shares due to the buy backs down to 3.5 million outstanding shares. I assumed that they were buying back shares with the shares increasing in price by 8% a year. Don’t forget to make assumptions about what they would do with their excess cash

Where did he get the value of $43,72 for the EBIT? Why did he use the 13 PE to valuate the company?

My response.

Below are my notes and the 10K on Duff & Phelps

Lecture 11_Balance Sheet Analysis Duff & Phelps ROE vs ROC

Class Notes #2 Intro and Duff and Phelps Case Study Analysis

If you look at the 10-K then EBIT is $15.7 million not 43.72. I don’t know why there is a discrepancy, but go with the actual figures in the 10-K.

The main points are to realize that this is an outstanding business with high returns on capital and profitable growth. 14 P/E is about the average P/E on an average American businesses. So a conservative 13 on a much better business that is growing in excess of 15% (at least for a few years) and can reinvest capital at high rates is worth more than an average multiple. I think he chose 13 as a normal/bad scenario for the multiple. Valuation is judgment not a science.

You are right to track the cash in your valuation. Either the cash builds up or is used in paying dividends or buying back stock.

I don’t know why I have 28.4 EBIT in my notes, but go always with the original 10-K figures. Hope that helps.

A GREAT POST FOR INVESTORS

http://wexboy.wordpress.com/2013/06/07/why-i-read/?blogsub=confirming#subscribe-blog

The immediate & obvious answer, as with most things in life, is ‘What else would I bloody do…?!‘ But I have to admit, I’m an autodidact – always have been, always will be, ever since childhood – which unfortunately made organized education increasingly intolerable** the older I got. However, when it comes to investing, the odds are stacked in my favour – organized education doesn’t offer you a hope in hell of becoming a good, let alone agreat, investor. As people often notice with regard to MBAs… [Again, I can’t resist this classic!].

Excellent blog, www.oftwominds.com, on current issues. Read the article on why China’s Yuan can’t easily become the world’s reserve currency. Yes, the dollar is under pressure, but no viable alternatives exist–for now.

The Difficult Escape from Student Loan Debt-Serfdom

October 17, 2013

Are We Approaching Peak Retirement?

October 15, 2013

The Impossibility of China Issuing a Reserve Currency **** must read!

October 14, 2013

Have We Reached Peak Entitlements?

October 11, 2013

Obama Administration Proposes 2,300-Page “New Constitution”

October 10, 2013

It’s Definitive: We’ve Reached Peak Jobs

(October 8, 2013)

The (Needed) Revolution Emerging in Higher Education

(October 7, 2013)

Five Goals for the Era Ahead

(October 5, 2013)

Have We Reached Peak Federal Reserve?

(October 4, 2013)

The Shutdown Political Game: Inflict Maximum Pain to Score Cheap Points

(October 3, 2013)

Have We Reached Peak Government?

(October 2, 2013)

One More “The Status Quo Is Saved” Rally and Then…?

(October 1, 2013)

Trapped in Net/Nets

The danger of even net/net, “cheap” stocks or camouflaged value traps.

Barron’s Sept. 19, 2011.

James Grant: I invested in Japanese value stocks, and had occasions to regret over and over on the reluctance of the Japanese to admit error and re-price. Companies that deserved bankruptcy would often not be allowed to meet their just deserts, but were carried on the back of banks that themselves had no true claim to solvency but were supported by the government. Capitalism is not just about success–that is the easy part. It is also about failure, recognizing it, dealing with it, liquidating it, properly pricing it. The Japanese have been unable to do that, and this characteristic was on display in the 1920s as well, so I take this to be a salient Japanese trait.

You were a great believer in Japanese equities. What happened?

With my friend Alex Porter, I was a general partner in Nippon Partners from 1998 through the end of 2010. We invested in Japanese value stocks. We closed it in December of 2010, because we weren’t making money, and it was immensely frustrating. Japanese corporate managers, by and large, don’t own equity. They have a platonic interest in the stock price. In the absence of a lively market for corporate control, there is no check on management doing nothing. In 1998 we began investing in companies whose shares are trading well below their pro-rata share of net cash on the balance sheets. In this country, in 1974, 1975, there were a lot of companies like that they did rather well in the 1970s and the 1980s. But in Japan, many (companies like these) remained at these compelling valuations for year upon year upon year. You get tired. The last straw was when one of our companies was selling at a huge discount to everything, and announced that it would undertake a capital investment larger than its stock-market capitalization.

Posted in Economics & Politics, Risk Management, Search Strategies, Valuation Techniques

Tagged gravity, oftwominds.com

The modern banking system manufactures money out of nothing. The process is perhaps the most astounding piece of sleight of hand that was ever invented. Banking was conceived in iniquity and born in sin. Bankers own the earth. Take it away from them, but leave them the power to create money and control credit, and with a flick of a pen, they will create enough money to buy it back again. But if you want to continue as the slavers of bankers and pay the cost of your own slavery, let them continue to create money, and to control credit. –Sir Josiah Stamp, Director The Bank of England.

How the Federal Reserve System Works (Short Video-MUST WATCH) http://www.hiddensecretsofmoney.com/

If you are unclear about what you see in the above video, then read more:

The Case Against The Fed by Murray Rothbard: http://mises.org/books/fed.pdf

For the most detailed study of banking and credit cycles: http://mises.org/books/desoto.pdf

Question: Why aren’t you rioting in the streets over this?

Who Predicted the Housing Bubbles?

Monetary policy during the 2000s: http://mises.org/daily/2936

thornton13 and Debate between Austrian and Mainstream

A reader asked about CEF:

One of the best sentiment gauges for precious metals is whether investors are paying a premium, or if they are buying precious metals at a discount.

Central Fund of Canada (CEF) is a closed-end mutual fund that owns gold and silver exclusively — the metals, not stocks — at a ratio of about 45 oz. of silver to 1 oz. of gold. Closed-end funds trade based upon the bid and ask, without regard to their net asset value (NAV). Because of this, they can trade at a price that is at a premium or discount to their NAV. By tracking the premium or discount we can get an idea of bullish or bearish sentiment regarding precious metals.

Very recently CEF has been selling at about a –7.5% discount to the net asset value of the gold and silver it owns. Considering that CEF has experienced a -54% decline from its 2011 top, that is a remarkably small discount when compared to historical discounts of -15% to -20%. Even more remarkable it the fact that after the -50% CEF correction in 2008, CEF was still selling at about a +15% premium!

Borrowers want capital, but they get money–newly created credit money. More credit money has been issued by the banking system than savers have deposited (“fiduciary media”). Those participants in the economy who suffer losses due to price changes were not parties to the original credit transactions. They are participants in the economy who receive the new money late in the process, after prices have been bid up by the credit money. –Mises (so much for the harmless actions of the Fed)

What Happens When You Buy Quality: October_Quest_2013

CAPITULATION IN THE MINERS

When I use the word capitulation it implies an ending to the bear market in precious metal equities, however NOTHING is certain in markets. I know not all public gold stocks will go to zero. Eventually, the laws of supply and demand assert themselves and you can only buy assets super cheap if sentiment is SUPER bearish. I think in late June when gold hit $1,180, gold stocks made a FEAR bottom while today they are going through despair/throw in the towel selling.

People see no hope so why own. Volume is relatively low and the selling persistent–day after day.

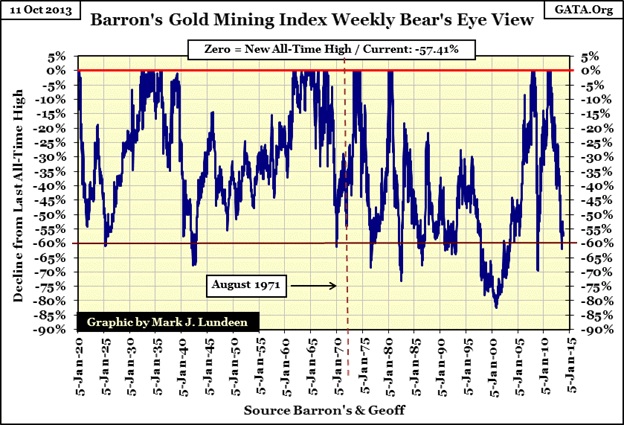

The above chart shows the sell-off from new highs over the past 90 years in the BGMI, the Barron’s Gold Mining Index). Currently, 2013 shows about a 63% loss or in the range of the past 10 bear markets.

Read more: http://www.gold-eagle.com/article/dow-jones-and-barron%E2%80%99s-gold-mining-index-1885-2013

The low relative volume, the historical depth of the sell-off and the demarcation of price movement between high quality (RGLD, FNV, SLW) and low quality gold stocks (NEM, GLDX) as the chart above shows, leads me to believe that we are closer to the end of the decline.

From: http://www.acting-man.com/?p=26553

We continue to get one ‘do or die’ moment after another in the charts of gold and gold-related instruments. So far, the outcomes have obviously been bearish every time since the 2011 peak, but at some point that is bound to change, as the fundamental backdrop continues to be gold-friendly (note that not every aspect of the fundamental backdrop is – for instance, the declining federal deficit is probably viewed as a negative by market participants). Often it is precisely at those times when nothing seems capable of turning a market around that surprise changes in trend can and do occur.

Note that gold sentiment remains absolutely dismal. Recently Mark Hulbert’s HGNSI (gold newsletter writer sentiment index) stood at minus 20 (meaning gold timers recommended a 20% net short position on average), while the daily sentiment index among gold futures traders (DSI) stood at 9 (all time low: 5). Bearish sentiment in the sector rarely becomes as extreme as it is at the moment. Of course it has been quite negative for some time now, but the current readings are rather extreme even so.

A major reason why we continue to maintain that the fundamental backdrop remains gold-friendly even though the price action suggests a bear market is still in progress, is that we believe that mainstream analysts are quite mistaken when they assert that it is back to ‘business as usual’ in the economy. It clearly isn’t.

History is being made today!

Of course, if you believe QE will lead to sustainable growth without monetary mayhem then stay away from anything to do with gold.

SHORTING SOCIALISM

The company exists as a social transfer mechanism between Western investors and Brazilian government officials and Petrobras workers. No hope.

Posted in Investor Psychology, Search Strategies

Tagged Acting Man, Bakshi, BGMI, Gold Stocks, Quality Companies