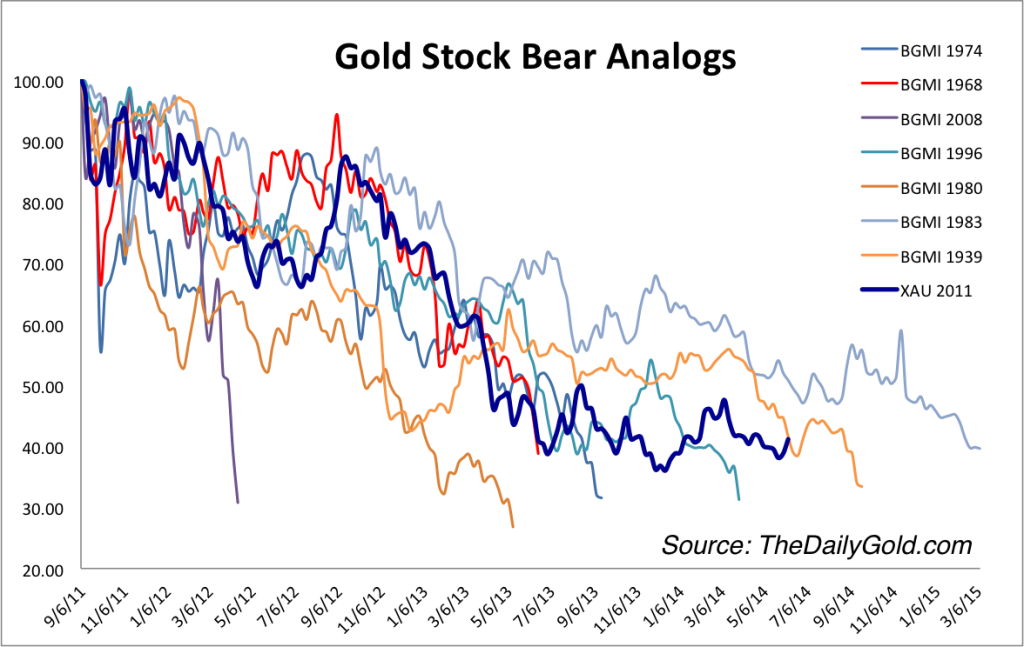

Go where the outlook is bleakest.

Read more http://www.acting-man.com/?p=26866#more-26866

Learn about other investors: http://25iq.com/

A Dozen Things I’ve Learned from Philip Fisher and Walter Schloss About Investing

1. “I had made what I believe was one of the more valuable decisions of my business life. This was to confine all efforts solely to making major gains in the long-run…. There are two fundamental approaches to investment. There’s the approach Ben Graham pioneered, which is to find something intrinsically so cheap that there is little chance of it having a big decline. He’s got financial safeguards to that. It isn’t going to go down much, and sooner or later value will come into it. Then there is my approach, which is to find something so good–if you don’t pay too much for it–that it will have very, very large growth. The advantage is that a bigger percentage of my stocks is apt to perform in a smaller period of time–although it has taken several years for some of these to even start, and you’re bound to make some mistakes at it. [But] when a stock is really unusual, it makes the bulk of its moves in a relatively short period of time.” Phil Fisher understood (1) trying to predict the direction of a market or stock in the short-term is not a game where one can have an advantage versus the house (especially after fees); and (2) his approach was different from Ben Graham.

2. “I don’t want a lot of good investments; I want a few outstanding ones…. I believe that the greatest long-range investment profits are never obtained by investing in marginal companies.” Warren Buffett once said: “I’m 15% Fisher and 85% Benjamin Graham.” Warren Buffett is much more like Fisher in 2013 than the 15% he once specified, but only he knows how much. It was the influence of Charlie Munger which moved Buffet away from a Benjamin Graham approach and their investment in See’s Candy was an early example in which Berkshire paid up for a “quality” company. Part of the reason this shift happened is that the sorts of companies that Benjamin Graham liked no longer existed the further way the time period was from the depression.

3. “The wise investor can profit if he can think independently of the crowd and reach the rich answer when the majority of financial opinion is leaning the other way. This matter of training oneself not to go with the crowd but to be able to zig when the crowd zags, in my opinion, is one of the most important fundamentals of investment success.” The inevitable math is that you can’t beat the crowd if you are the crowd, especially after fees are deducted.

4. “Usually a very long list of securities is not a sign of the brilliant investor, but of one who is unsure of himself. … Investors have been so oversold on diversification that fear of having too many eggs in one basket has caused them to put far too little into companies they thoroughly know and far too much in others which they know nothing about.” For the “know-something” active investor like Phil Fisher, wide diversification is a form of closet indexing. A “know-something” active investor must focus on a relatively small number of stocks if he or she expects to outperform a market. By contrast, “know-nothing” investors (i.e., muppets) should buy a low fee index fund.

5. “If the job has been correctly done when a common stock is purchased, the time to sell it is almost never.” Phil Fisher preferred a holding period of almost forever (e.g., Fisher bought Motorola in 1955 and held it until 2004). The word “almost” is important since every company is in danger of losing its moat.

6. “Great stocks are extremely hard to find. If they weren’t, then everyone would own them. The record is crystal clear that fortune – producing growth stocks can be found. However, they cannot be found without hard work and they cannot be found every day.” Fisher believed that the “fat pitch” investment opportunity is delivered rarely and only to those investors who are willing to patiently work to find them.

7. “Focus on buying these companies when they are out of favor, that is when, either because of general market conditions or because the financial community at the moment has misconceptions of its true worth, the stock is selling at prices well under what it will be when it’s true merit is better understood.” Like Howard Marks, Fisher believed that (1) business cycles and (2) changes in Mr. Market’s attitude are inevitable. By focusing on the value of individual stocks (rather than just price) the investor can best profit from these inevitable swings.

8. “The successful investor is usually an individual who is inherently interested in business problems.” A stock is a part ownership of a business. If you do not understand the business you do not understand that stock. If you do not understand the business you are investing in you are a speculator, not an investor.

9. “The stock market is filled with individuals who know the price of everything, but the value of nothing.” Price is what you pay and value is what you get. By focusing on value Fisher was able to outperform as an investor even though he did not look for cigar butts.

10. “It is not the profit margins of the past but those of the future that are basically important to the investor.” Too often people believe that the best prediction about the future is that it is an extension of the recent past.

11. “There is a complicating factor that makes the handling of investment mistakes more difficult. This is the ego in each of us. None of us likes to admit to himself that he has been wrong. If we have made a mistake in buying a stock but can sell the stock at a small profit, we have somehow lost any sense of having been foolish. On the other hand, if we sell at a small loss we are quite unhappy about the whole matter. This reaction, while completely natural and normal, is probably one of the most dangerous in which we can indulge ourselves in the entire investment process. More money has probably been lost by investors holding a stock they really did not want until they could ‘at least come out even’ than from any other single reason. If to these actual losses are added the profits that might have been made through the proper reinvestment of these funds if such reinvestment had been made when the mistake was first realized, the cost of self-indulgence becomes truly tremendous.” Fisher was very aware of the problems that loss aversion bias can cause.

12. “Conservative investors sleep well.” If you are having trouble sleeping due to worrying about your portfolio, reducing risk is wise. Life is too short to not sleep well, but also fear can result in mistakes.

Walter Schloss

1. “I think investing is an art, and we tried to be as logical and unemotional as possible. Because we understood that investors are usually affected by the market, we could take advantage of the market by being rational. As [Benjamin] Graham said, ‘The market is there to serve you, not to guide you!’.” Walter Schloss was the closest possible match to the investing style of Benjamin Graham. No one else more closely followed the “cigar butt” style of investing of Benjamin Graham. In other words, if being like Benjamin Graham was a game of golf, Walter Schloss was “closest to the pin.” He was a man of his times and those times included the depression which had a profound impact on him. While his exact style of investing is not possible today, today’s investor’s still can learn from Walter Schloss. It is by combining the best of investors like Phil Fisher and Walter Schloss and matching it to their unique skills and personality that investors will find the best results. Warren Buffet once wrote in a letter: “Walter outperforms managers who work in temples filled with paintings, staff and computers… by rummaging among the cigar butts on the floor of capitalism.” When Walter’s son told him no such cigar butt companies existed any longer Walter told his son it was time to close the firm. The other focus of Walter Schloos was low fees and costs. When it came to keeping overhead and investing expenses low, Walter Schloss was a zealot.

2. “I try to establish the value of the company. Remember that a share of stock represents a part of a business and is not just a piece of paper. … Price is the most important factor to use in relation to value…. I believe stocks should be evaluated based on intrinsic worth, NOT on whether they are under or over priced in relationship with each other…. The key to the purchase of an undervalued stock is its price COMPARED to its intrinsic worth.”

3.”I like Ben’s analogy that one should buy stocks the way you buy groceries not the way you buy perfume… keep it simple and try not to use higher mathematics in you analysis.” Keeping emotion out of the picture was a key part of the Schloss style. Like Ben Graham he as first and foremost rational.

4. “If a stock is cheap, I start buying. I never put a stop loss on my holdings because if I like a stock in the first place, I like it more if it goes down. Somehow I find it difficult to buy a stock that has gone up.”

5. “I don’t like stress and prefer to avoid it, I never focus too much on market news and economic data. They always worry investors!” Like all great investors in this series, the focus of Schloss was on individual companies not the macro economy. Simpler systems are orders of magnitude easier to understand for an investor.

6. “The key to successful investing is to relate value to price today.” Not only did Schloss not try to forecast the macro market, he did not really focus forecasting the future prospects of the company. This was very different than the Phil Fisher approach which was focused on future earnings.

7. “I like the idea of owning a number of stocks. Warren Buffet is happy owning a few stocks, and he is right if he is Warren….”Schloss was a value investor who also practiced diversification. Because of his focus on obscure companies and the period in which he was investing, Walter was able to avoid closet indexing.

8. “We don’t own stocks that we’d never sell. I guess we are a kind of store that buys goods for inventory (stocks) and we’d like to sell them at a profit within 4 years if possible.” This is very different from a Phil Fisher approach where his favorite holding period is almost forever. Schloss once said in a Colombia Business school talk that he owned “some 60-75 stocks”.

9. “Remember the word compounding. For example, if you can make 12% a year and reinvest the money back, you will double your money in 6 years, taxes excluded. Remember the rule of 72. Your rate of return into 72 will tell you the number of years to double your money.” Schloss felt that “compounding could offset [any advantage created by] the fellow who was running around visiting managements.”

10. “The ability to think clearly in the investment field without the emotions that are attached to it is not an easy undertaking. Fear and greed tend to affect one’s judgment.” Schloss was very self-aware and matched his investment style to his personality. He said once” We try to do what is comfortable for us.”

11. “Don’t buy on tips or for a quick move.”

12. “In thinking about how one should invest, it is important to look at you strengths and weaknesses. …I’m not very good at judging people. So I found that it was much better to look at the figures rather than people.” Schloss knew that Warren Buffett was a better judge of people than he was so Walter’s approach was almost completely quantitative. Schloss knew to stay within his “circle of competence”. Schloss said once: “Ben Graham didn’t visit management because he thought figure told the story.”