Read all four parts of this study of shady pump and dump schemes in the Pink Sheet World. (Must Read) https://theintercept.com/2016/09/22/the-money-is-gone/

Read all four parts of this study of shady pump and dump schemes in the Pink Sheet World. (Must Read) https://theintercept.com/2016/09/22/the-money-is-gone/

Read the financials: SEC-OMEX-1193125-13-326785 Who in their right mind would own this? Next, a detailed research report on the company (worth a read) omexreport. Also, thanks to www.classicvalueinvestors.com

The company’s typical response:

November 1, 2013

TAMPA, Fla., Nov. 1, 2013 (GLOBE NEWSWIRE) — Yesterday afternoon, a commentary about Odyssey Marine Exploration, Inc. (Nasdaq:OMEX) was distributed by Ryan Morris of Meson Capital Partners LLC. The author never contacted the company for clarifications or answers to his questions. Had he done so, Odyssey would have pointed out factual errors, incomplete information and erroneous conclusions which are rebutted by Odyssey’s public filings and other publicly available information. Odyssey is confident its existing public disclosures are accurate in all material respects, and that the company has provided a clear and concise explanation of all material information about the company and its relationships with associated companies and individuals.

Odyssey’s management believes that it is in the best interest of our shareholders to remain focused on business rather than debating or responding to rumor and innuendo. However, due to the number of inquiries to the company, management felt it important to reaffirm and stand by the accuracy of all information which has been released by the company. It is also important for interested parties to carefully consider the statement the author made on the first page of his editorial attacking the company (emphasis added):

“You should assume that as of the publication date of our reports and research, Meson Capital Partners, LLC (possibly along with or through our members, partners, affiliates, employees, and/or consultants) along with our clients and/or investors has a short position in all stocks (and/or options, swaps, and other derivatives related to the stock) and bonds covered herein, and therefore stands to realize significant gains in the event that the price of either declines.”

The company believes this statement by the author, and the likelihood that this is part of an attempt to profit from a “short and distort” strategy, calls into question the motivation and intent behind the allegations as well as the timing of its release. Accordingly market authorities have been notified. (CSInvesting: So any bullish research report from an author who owns stock should also be questioned.)

Next week Odyssey management plans to host a conference call to discuss corporate developments and to address the false and misleading statements and innuendo in the Meson Capital piece. The call date and dial-in instructions will be issued in a press release early next week. (This might be FUN to listen to–see website address below)

About Odyssey Marine Exploration

Odyssey Marine Exploration, Inc. (Nasdaq:OMEX) is engaged in deep-ocean exploration using innovative methods and state of-the-art technology for shipwreck projects and mineral exploration. For additional details, please visit www.odysseymarine.com. The company also maintains a Facebook page at http://www.facebook.com/OdysseyMarine and a Twitter feed @OdysseyMarine.For additional details on Odyssey Marine Exploration, please visit www.odysseymarine.com.

CONTACT: MEDIA CONTACT: It is always good to refresh yourself on WHAT NOT to invest in.

A Reader’s Question

VENICE – The run-up in gold prices in recent years – from $800 per ounce in early 2009 to above $1,900 in the fall of 2011 – had all the features of a bubble. And now, like all asset-price surges that are divorced from the fundamentals of supply and demand, the gold bubble is deflating.

Roll a dog turd in sugar doesn’t make it a donut–Chicago Slim

Invert, always Invert

Carl Gustav Jacob Jacobi was a German mathematician who lived in the 1800s. Jacobi once said “man muss immer umkehren” which translates to “Invert, always invert.” Jacobi believed that the solution for many difficult problems in mathematics could be found if the problems were expressed in the inverse. —http://amarginofsafety.com/2011/01/09/456/ (recommended)

This is a lesson in reverse search or what to avoid, though I am seeking shares (GWBU) to short. We will study:

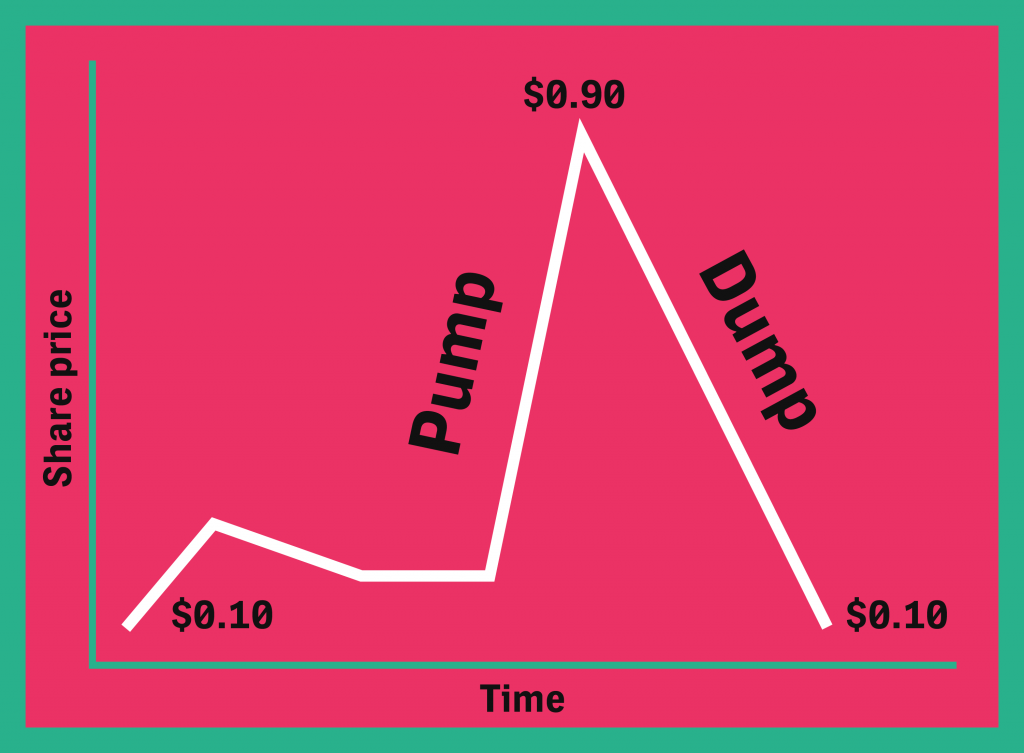

In the U.S., shares trading for less than one dollar are known as microcap or penny stocks. Their low valuation and low trading volumes make them susceptible to price manipulation schemes. Penny stocks also lack transparency in their underlying business and operations and often do not have a verifiable financial history, making them susceptible to securities fraud schemes.

Our first case study in early March 2012 on Pump and Dumps (Frauds) was SNPK, last mentioned here http://wp.me/p1PgpH-LC

I call these types of promotions, “Death Stocks” because their stock charts eventually look like this (Note the flat line, similar to the chart of vital signs of a dying/dead patient:

Current Stock Price as of June 5, 2012: $1.75. 360 million outstanding shares at $1.75 = $630 million market cap. Tangible Net Worth ($70,500). Price above value??? More than $600 million for negative net worth. No revenues. Mr. Daniele Brazzi is both the CEO and CFO. Located in Baloney, Italy. This company and all its affiliates exist for one purpose only–to sell pumped up stock to the unsuspecting, greedy and ignorant.

Now GWBU is in the early stages of a Pump. Ultimate Value—IMHO–within 22 months $0.00, where the stock will find excellent “technical” support.

A detailed (38 pages) tutorial on the GWBU Pump and Dump with current financial statements are here:Great Wall GWBU Pump and Dump The Horror! The document is almost comical, but this stock is a DEATH STOCK.

But where are the Feds? The SEC? Here they are: http://www.youtube.com/watch?v=jocRd-aajW0

Updates to follow………….

The “night singer of shares” sold stock on the streets during the South Sea Bubble. Amsterdam, 1720.

The “night singer of shares” sold stock on the streets during the South Sea Bubble. Amsterdam, 1720.

I had told readers in previous posts about the pump and dump stock, SNPK (“Sunpeaks Ventures, Inc.) that eighteen months would pass before the stock hit the sub $0.01 level.

But when I saw this:

I was WRONG. SNPK may disappear altogether in a matter of weeks, so to complete this case study, I would visit company headquarters and find out the truth.

My visit to Sunpeak’s HQ: http://www.youtube.com/watch?v=-AzzUjgPHOY.

What I saw gave me a shocked face: http://www.youtube.com/watch?v=srw3RdiIlrQ. Police cars and yellow crime-scene tape prevented further investigation. This brings the case to a close. Even a 96% drop from the high price of $2.00 a month ago is meaningless. This is an eventual, inevitable $0.00.

2-minute video http://www.fraudcast.ca/docs/Pump_And_Dump_Fraud.php

For those who wish to learn more about this seamy part of the securities market then you can read here:

Microcap stock fraud is a form of securities fraud involving stocks of “microcap” companies, generally defined in the United States as those with a market capitalization of under $250 million. Its prevalence has been estimated to run into the billions of dollars a year. Many microcap stocks are penny stocks, which trade at below $1 a share.

Microcap stock fraud generally takes place among stocks traded on the OTC Bulletin Board and the Pink Sheets Electronic Quotation Service, stocks which usually do not meet the requirements to be listed on the stock exchanges. Some fraud occurs among stocks traded on the NASDAQ Small Cap Market, now called the NASDAQ Capital Market.[4]

Microcap fraud encompasses several types of investor fraud:

Pump and dump schemes tend to take place either on the Internet including e-mail spam campaigns or through telemarketing from “boiler room” brokerage houses (for example, see Boiler Room). Often the stock promoter will claim to have “inside” information about impending news. Newsletters that purport to offer unbiased recommendations then tout the company as a “hot” stock. Messages in chat rooms and email spam urge readers to buy the stock quickly.[1]

Unwitting investors then purchase the stock, creating high demand and raising the price. This seemingly “real” rise in prices can entice more people to believe the hype and to buy shares as well. When the people behind the scheme sell their shares and stop promoting the stock, the price plummets, and other investors are left holding stock that is worth significantly less than what they paid for it.

Fraudsters frequently use this ploy with small, thinly traded companies—known as “penny stocks,” generally traded over-the-counter (in the United States, this would mean markets such as the OTC Bulletin Board or the Pink Sheets), rather than markets such as the New York Stock Exchange or NASDAQ—because it is easier to manipulate a stock when there is little or no independent information available about the company.[2] The same principle applies in the United Kingdom, where target companies are typically small companies on the AIM or OFEX.

A more modern spin on this attack is known as hack, pump and dump.[3] In this form a person purchases penny stocks in advance and then uses compromised brokerage accounts to purchase large quantities of that stock. The net result is a price increase, which is often pushed further by day traders seeing a quick advance in a stock. The holder of the stock then sells his stock at a premium.[4]

During the dot-com era, when stock market fever was at its height and many people spent significant amounts of time on stock Internet message boards, a 15-year-old named Jonathan Lebed showed how easy it was to use the Internet to run a successful pump-and-dump. Lebed bought penny stocks and then promoted them on message boards, pointing at the price increase. When other investors bought the stock, Lebed sold his for a profit, leaving the other investors holding the bag. He came to the attention of the U.S. Securities and Exchange Commission (SEC), which filed a civil suit against him alleging security manipulation. As is commonly the case in SEC actions, Lebed settled the charges by paying a fraction of his total gains. He neither admitted nor denied wrongdoing, but promised not to manipulate securities in the future.[5]

As late as April 2001, before the company’s collapse, Enron executives participated in an elaborate scheme of pump-and-dump[6] in addition to other illegal practices that fooled even the most experienced analysts on Wall Street. Studies of the anonymous messages posted on the Yahoo board dedicated to Enron revealed predictive messages that the company was basically a house of cards, and that investors should bail out while the stock was good.[7] Enron had falsely reported profits which inflated the stock price, and then covered the real numbers by using questionable accounting practices. 29 Enron executives sold overvalued stock for more than a billion dollars before the company went bankrupt.[8]

In April 2007, the SEC brought charges against Park Financial Group as a result of an investigation into a pump and dump scheme during 2002-2003 of the Pink Sheet listed stock of Spear & Jackson Inc.[9]

Pump and dump stock scams are prevalent in spam, accounting for about 15% of spam e-mail messages. A survey of 75,000 unsolicited emails sent between January 2004 and July 2005 concluded that spammers could make a return of 6% by using this method, while recipients who act on the spam message typically lose 5% of their investment within two days.[10] A study by Böhme and Holz[11] shows a similar effect. Stocks targeted by spam are almost always “penny stocks“, selling for less than $5 per share, not traded on major exchanges, are thinly traded, and are difficult or impossible to sell short. Spammers acquire stock before sending the messages, and sell the day the message is sent.[12]

A chop stock is an equity, usually trading on the Nasdaq Stock Market, OTC Bulletin Board or Pink Sheets listing services, that is purchased at pennies per share and sold by unscrupulous stock brokers to unsuspecting retail customers at several dollars per share.[9][10]

This practice differs from a pump and dump in that the brokerages make money, in addition to hyping the stock, by marketing a security they purchase at a deep discount. In this practice, the brokerage firm generally acquires the block of stock by purchasing a large block of the securities (usually from a large shareholder who is not affiliated with the underlying company) at a negotiated price that is well below the current market price (generally 40% to 50% below the then-current quoted offer/ask price) or it acquires the stock as payment for a consulting agreement.[11]

The subject stocks usually have little or no liquidity prior to the block purchase. After the block is purchased, the firm’s participating brokers will sell the stock to their brokerage customers at the then-current quoted offer/ask price, to the often victimized investors who are generally unaware of this practice. This large difference, or “spread” between the then-current quoted offer/ask price and the deeply discounted price the block of stock was purchased is almost always shared with the stockbroker at the firm who solicited the trade. For this reason, there is a large benefit and an inherent conflict of interest for the firm and the broker to sell these “proprietary products”.

Because the firm is technically “at risk” on the block of stock (if the price of the stock drops below the price at which the block was purchased, the firm will be at a loss on the stock) and stock is usually sold at or even slightly below the then-current prevailing market price offer/ask, the practice is still legal in the United States. In fact, it is not required that this profit spread be disclosed to the client, since it is not technically a “commission”. When a brokerage house sells such stock from its own inventory, a client will receive a trade confirmation stating the transaction was done as “Riskless Principal” or “Markup”, which in fact, just like commissions, is also revenue to the firm, and such a practice is often subject to abuse. Only the amount of fees charged over and above the offer/ask are commissions, and must be disclosed. But even though it is still legal, it is frowned upon by the Securities Exchange Commission, and they are using other laws and methods of attack to indirectly thwart the practice.

Microcap fraud has been a major source of income for organized crime.[12] Mob figures from each of the Five Families of the New York mafia, as well as the New Jersey mob, have become involved in stock scams.

Mafia involvement in 1990s stock swindles was first explored by investigative reporter Gary Weiss in a December 1996 Business Week article.[13] Weiss later explored the Mafia’s Wall Street scams in a book.[14]

Organized crime elements were believed to have been short-selling chop stocks in the late 1990s.[15]

We last discussed the scam, illusion and/or fantasy of SNPK http://wp.me/p1PgpH-E7 and our first mention of this impending disaster was on March 13, 2012:http://wp.me/p1PgpH-E7

Expect to see SNPK trading BELOW (sub 5 cents) at the levels of this other Pump and Dump, NSTR, within the next 12 months. Anybody want to take the other side of that bet?

This post was to keep you abreast as a warning and learning exercise–you don’t have to flush your hard-earned cash away to know that the above “company” exists solely to fleece “shareholders.” How many innocents are saying, “What the F! #$%& happened?” I am sure the SEC will start their “investigation” a year or two after the fleecing. Oh well….

You can learn more about how Pump and Dumps work here: http://www.pennystockresearch.com/snpk-rsrs-ewsi-pump-and-dump-alerts-april-27-2012/

This week we’re exposing these three popular Pump & Dumps: Sunpeaks Ventures (SNPK), Regency Resources (RSRS), and E-Waste Systems (EWSI).

On Pump and Dump Friday, we identify a few of the potentially “bogus” promotions going on in penny stocks today.

If you don’t know how these schemes work, be sure to check out the free report.

Without further ado, here are today’s “disasters waiting to happen”:

For the second week in a row, I have to say “I told you so!”

It’s like shooting fish in a barrel. The pumpers telegraph their moves so plainly it’s scary! Last week I told you to watch out for a dead cat bounce and then shares would take another dive…Well they have!

—

Have a great weekend and thanks for the generous contributions on advising a reader about transitioning/learning to become a value investor.

Back again on Monday with case study analysis on Kiwi Airlines from Competition Demystified.