Interview-with-benzingas-deep-value-letter-author-tim-melvin-about-my-new-book-deep-value/

Posted in Investing Gurus, Search Strategies

Tagged Deep Value, Net, Nets, Quantitative Investing, Toby, Toby Carlisle

http://orangevaluefund.com/Welcome.html

Learn about “SAFE and “CHEAP.”

Munger’s book recommendations

http://www.farnamstreetblog.com/2014/08/book-recommendations-from-billionaire-charlie-munger/

A case study of Warren Buffett and Charlie Munger’s investment in and management of Blue Chip Stamps. Includes:

If you find any errors or have any other contributions, make a pull request or contact me through the Twitter handle @maxolson.

GO HERE: https://www.gitbook.io/book/maxolson/blue-chip-stamps

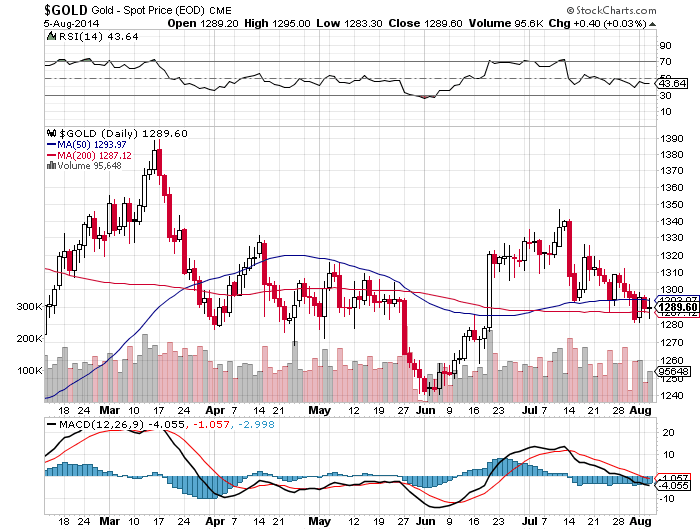

PS: On the road, but I haven’t forgotten about Yamana. I wouldn’t buy above $8.00.

If gold is down because the market thinks the Fed will raise rates and end QE, then those assumptions are based on fantasy. HOW can the FED EVER stop QE without the house of cards collapsing? What does history say: http://www.zealllc.com/2014/goldrrf.htm

Here is the Argentina Peso in free-fall:

HAVE A GREAT WEEKEND!

Jean-Marie Eveillard

Adviser, First Eagle Investment Management

March 13, 2014

Quotes

“We don’t look at gold as a commodity, but as a form of insurance against what Peter Bernstein calls extreme outcomes. In most circumstances in which worldwide equity markets would go down – and not just for a week or two – the price of gold would go up, providing a partial offset to the hits we’d take in our equity portfolio”.

“In general, there aren’t many countries in which we wouldn’t invest. But if a country is too economically or politically prevail, we pass. The main country in which we won’t invest today is Russia. There’s still too much risk for foreign (or even local) investors that you’ll think you own an asset and then Mr. Putin decides you don’t”.

“The knock on diversified funds is that they’re index-huggers, which given the geographic breadth of where we invest, is not at all the case for us. I know the argument that you should only own your best 30 or 40 ideas, but I’ve never proven over time that I actually know in advance what those are”.

“Our cash balance is purely a residual of whether or not we’re finding enough to invest in”.

“If one is wrong in judging a company to have a sustainable competitive advantage, the investment results can be disastrous”.

“Top executives from a Japanese property company and casualty insurer we’ve owned for years just in our office last month explaining the extent of the CDO exposure in their investment portfolio, which was upsetting to us. We said,”Didn’t the fact that you were buying a triple-A rated product with a yield much in excess of what you could get from Procter & Gamble sound too good to be true?”. But that kind of thing happened around the world.

Video Lecture at Ivey School in 2014:

http://www.bengrahaminvesting.ca/Resources/Video_Presentations/Guest_Speakers/2014/Eveillard_2014.htm Worth the time.

…When men live by trade–with reason not force, as their final arbiter–it is the best product that wins, the best performance, the man of best judgment and high ability and the degree of a man’s productiveness is the degree of his reward. (Atlas Shrugged)

Seth Klarman

Below are links to Seth Klarman’s investor letters and appearances. I would try to study his philosophy, attitude, and approach to investing–see if you can integrate some of his approach to YOUR OWN methods.

New material from a reader (generous!) KLARMAN Response to Lowensteins Rational Investors found here:Graham Dodd Revisted by Lowenstein

Seth-Klarmanm-Interview-Financial-Analyst-Journal

klarman-value-investors-different

Klarman_on_running_a_fund_interview

Seth_Klarman-Why_Most_Investment_Managers_Have_It_Backwards

A BLOG DEVOTED TO Klarman http://www.rbcpa.com/klarman.html

Yamana Valuation

Upon returning from vacation, I have put off updating my valuation of Yamana. When there are fish, you must fish. I promise to have it posted by this weekend. I do recommend anyone who wants to hear a good management team explain their strategy for managing assets to listen to Yamana’s second quarter’s conference call:

http://www.gowebcasting.com/events/yamana-gold-inc/2014/07/31/second-quarter-financial-results/play

Yamana Gold Inc_ Q2 2014 MDA Final (SEDAR)_v001_t1ii3h

Presentation: Q2 2014 – Conference Call Final

—

Asking a girl for her phone number

Posted in Investing Gurus, Valuation Techniques

Tagged Gold Stocks, Seth Klarman, valuation, Yamana

An interesting blog:http://alephblog.com/ The writer seems to approach investing through the different lens of actuarial risk–another approach to help you broaden your perspective on investing.

Classic the fundamentals of market-tops

Advice to students of investing (that’s us!)

But if I had control over what Finance students were taught, I would do the following:

1) I would reduce the math content for finance students and increase the qualitative understanding of markets. No more MPT.

2) I would increase the level of understanding on how to relate with people, because that makes a big difference in negotiating trades.

3) I would want them to work in a simple business, like a hot-dog cart, or mowing lawns, so that they could begin to get an idea of how tough it is to earn a profit. My best boss in my life grew up watching his parents’ delicatessen, and it shaped his view of how to make a profit.

4) I would revise the concept of the cost of capital to make it credit-centric. All the efforts to calculate the cost of equity capital from equity market correlations are bogus. They don’t make any economic sense. In most cases, the cost of equity should not exceed the yield on an average CCC bond.

5) I would tell them that changes in inflation and real GDP don’t have as large of an impact on corporate profits as is commonly thought, both positively and negatively. I would tell them to focus on the stock, and drop the complex model. Few in the investment business work off a complex model, and if you need one, you can buy Value Line, which I like, which tries to use a single macroeconomic model for 1700 popular stocks.

—

Mostly, I would teach them to think broadly, and realize the most of the complex investment math is easy to get wrong.

The article:

What I Would & Would Not Teach College Students About Finance

Have a Good Weekend!

HY credit is where the fun may begin. I would be terrified to buy the dip–unless I knew the company cold.

Experience tends to confirm a long-held notion that being prepared, on a few occasions in a lifetime, to act promptly in scale, in doing some simple and logical thing, will often dramatically improve the financial results of that lifetime. A few major opportunities, clearly recognizable as such, will usually come to one who continuously searches and waits, with a curious mind that loves diagnosis involving multiple variables. And then all that is required is a willingness to bet heavily when the odds are extremely favorable, using resources available as a result of prudence and patience in the past. –Charlie Munger

Thanks to a reader:

The-Best-of-Charlie-Munger-1994-2011

Read: https://www.hightail.com/download/ZUcweFlkWkJwTVZBSXRVag

Munger’s analysis to build a Trillion Dollar Business from Scratch

Munger-Talk-at-Harvard-Westlake

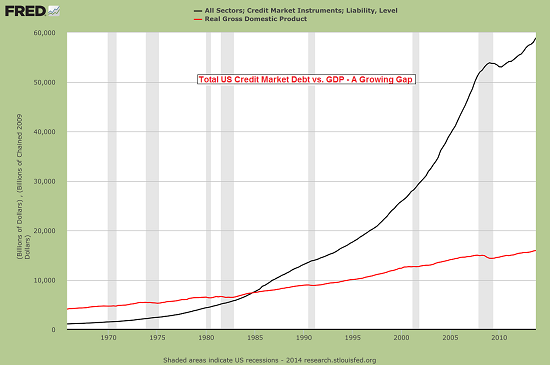

Why we are doomed

http://www.oftwominds.com/blogjuly14/interest-debt7-14.html

Update on Hyperinflation Talk Presented 2010 by Victor Sperandeo,

EAM Partners L.P. May 13, 2013

On February 16, 2010, I first gave a speech titled “Hyperinflation: A Statistical Inevitability” at a charity event in Dallas, Texas. In essence, the talk was a “warning” that unless the growth of the nominal debt versus nominal GDP changed to a more normal balance, the US would “eventually” suffer from hyperinflation.

Hyperinflation is a debt problem whose root cause is when a country’s level of debt rises to a level that when its economy goes into a deep recession (or depression) the country cannot borrow money or raise enough taxes to cover its expenditures, and therefore it is forced to print money to cover a greater percentage of its expenditures than the markets and investors think is sustainable. This concludes in the country’s inability to pay the interest on its debt, which progressively consumes its overall budget, causing the country to continue to print money to pay its ever increasing debts and interest thereon, which ultimately leads to a loss in confidence in its currency, ending with hyperinflation as the result.

Editor: Note the difference between inflation and hyperinflation (hyperinflation is NOT just an ultra-high rate of inflation) See links below.

…

Where the U.S. Stands Today

My original speech was based on the 2010 Congressional Budget Office’s Budget and Economic Outlook Fiscal Years 2010-2020. At the time, total US debt was growing at an unsustainable rate of 11.90% compounded from 2006 -2010 (fiscal years) while gross GDP was growing at a nominal rate of 2.75%. Debt was increasing at 4.3 x’s higher than growth. Clearly, this was an unsustainable situation.

Further, the reason that I state hyperinflation will occur “within” the next 10 years has a logical basis. If one takes the position that the net debt will grow at 5% a year, total U.S. debt will be $27.324 trillion in 10 years (not including current off-balance sheet items or unfunded liabilities). As the CBO does not project total U.S. debt, only public debt, the $27.324 trillion figure is based on my projection.

Now, what will interest rates be in 10 years? The CBO says an average yield is 4.6% (CBO 2/13 Report page 5), but let’s assume it reverts to the mean for bills and bonds of the last 52 years, or from 1961, which was 6.01%. Assuming that spending increases 5.08% a year from 2014-2023 (CBO 2/13 Report page 3), they say annual spending will be $5.082 trillion in 2023 net of annual interest.

However, annual interest in 2023 on my projected $27.324 trillion total U.S. debt (using the historic average interest rate of 6.01%) will be $1.642 trillion, or 32% of projected 2023 annual spending without interest and 24% of projected 2023 annual spending with interest. Today, interest is 6% of the budget. Therefore, one has to ask the question, where does the approximately 20% difference come from? I believe U.S. bond holders will sell what they own, the U.S. dollar will decline, and the Fed will print money at a rate that will make today’s Fed look like they are Shaolin Monks.

See full article here:Hyperinflation by Victor Sperandeo

A history of hyperinflation in pre-revolutionary France: Fiat_Inflation_in_France_by_White

An Austrian economist, Joseph Salerno discusses in nineteen minutes the theory of hyperinflation (High School Lecture) http://youtu.be/xVDZVhdT2gY

I am interested to hear from readers how the U.S. will AVOID hyperinflation assuming our current trends continue. What will politicians try to avoid default. What do YOU think?

Two short, six minute videos discussing Market Wizard, Victor Sperandeo: http://youtu.be/OBkb69tvVqs and http://youtu.be/8XfSz3MT3Xg

—

—

Yamana valuation to be posted Friday.

Posted in Economics & Politics, History, Investing Gurus

Tagged France, hyperinflation, Joe Salerno, Sperandeo

I owe my early success as an investor not to brains or knowledge, because my mind was untrained and my ignorance was colossal, The game taught me the game, And didn’t spare the rod while teaching.

Whenever I have lost money in the stock market I have always considered that I have learned something; that if I have lost money I have gained experience, so that the money really went for a tuition fee. –Jessie Livermore

Mark Sellers and PRXI Value Trap

He put over 50% of his fund into MCF:

I added an update to yesterday’s micro-cap post. http://wp.me/p2OaYY-2tX. The point is to try and understand prior investment successes or failures. Any lessons there?

An excellent book on the inflationary 1970s The-Dollar-Crisis by Percy Greaves

I just like the old photos to capture the spirit of the times: The-Stock-Market-Crash-of-1929

I am still in shock over Brazil’s World Cup blow-out.

A fat tail event?

Posted in Economics & Politics, History, Investing Careers, Investing Gurus, Investor Psychology, Risk Management

Tagged Mark Sellers, MCF, prxi, Risk, The Dollar Crisis, Value Traps

Market Sentiment and Money Supply update: http://www.acting-man.com/?p=31559

James Grant’s Investment Approach (Video) June 12, 2014

Editor: Focus on how Mr. Grant approaches investing not necessarily the current object of his affections.

James Grant: “The Fed’s policy will inevitably fail because hyper-aggressive leveraged finance always seems to step in front of a bus.”

“Macro-economic forecasting is not a useful endeavor. It seems a better way is to consider the panoply of risks and then after having pondered them, look for mis-priced and cheap options on likely but uncertain outcomes.”

http://www.realclearmarkets.com/video/2014/06/12/jim_grant_buy_gold.html

[Note: Grant’s comments on gold begin at the 7:12 minute mark.]

“Gold is an example to me of an opportunity,” James Grant, editor of Grant’s Interest Rate Observer said in an interview this week. “[It] exhibits so many of the characteristics of a corpse, although it does occasionally toss and turn.”

“Gold stocks certainly look as if they were dead—but nobody even bothers to poke them with a stick.”

Gold is a cheap option on the failure of price control. Observe how the future is handicapped. We now have low levels of volatility and terrific embedded complacency. You will be paid well if the consensus makes a mistake. Invest in the monetary failure of an improvised monetary system run by tenured professors (Yellen).

Investing is when you want people to agree with you not now but in the future.

“Gold and gold mining shares are very, very cheap-and certainly widely detested options on the failure of this massive world-wide experiment, or the demonstration of the hopelessness of the technique of price control.”

HAVE A HAPPY FOURTH!

Posted in History, Investing Gurus, Investor Psychology

Tagged Complacency, Gold, James Grant, Sentiment

{kind=link}