The author of this blog when he lived with cannibals in Irian Jaya (Western Papua New Guinea). How this picture came to be is a long, long story told over several beers. I urge readers to think of these skulls as representing investors who did NOT read the proxies and financial footnotes of the companies they bought. Be careful and always think for yourself. Please! A moment of silence for the many who did not survive. More on cannibals here: http://www.smithsonianmag.com/travel/cannibals.html.

Bernanke’s money printing is certainly having his intended effect in the stock market today. The joys and inevitable sorrows of manipulation. Eventually, the Fed will have to stop having its foot on the monetary gas pedal. This blog has been updating you on the 8% to 9% money growth and you are all aware of the current negative real interest rates ( a war on savers).

Irrational Behavior

Don’t forget to improve by signing up for A Beginner’s Guide to Irrational Behavior (Dan Ariely). “In this course we will learn about some of the many ways in which people behave in less than rational ways, and how we might overcome these problems.” https://www.coursera.org/course/behavioralecon

A Special Situation

A Leveraged Stub Stock Remember to do your own work and if you invest, size your position accordingly in a company that could either pay down debt and turnaround or be crushed by debt. The author of the blog below addresses many of the issues that need to be thought about. One key is to look carefully at maintenance capital expenditures (“MCX”) because if management skimps on MCX to pay down debt, then the company really is in liquidation and the asset values may not be there to support the turnaround. You can learn as much about investing/companies that you analyze and pass on as the ones you invest in. You just need to keep track of your omissions and see if your thought process was correct. I bet you 10 to 1 that not 1 in 100 professional money managers do that on a systematic basis. What a chance to learn, but you have to be diligent.

Debate about the efficacy of the Austrian Business Cycle

This debate is somewhat similar to the debate of efficient market theory. How can entrepreneurs be fooled time and time again by the Fed’s market manipulations that consistently lead to booms and busts. What about rationality?

Here is the Perhsing Square website on Herbalife. Sign up and learn:

Pershing has their HLF deck up on the website: http://factsaboutherbalife.com/

Verdict: This will get ugly but my money would be on Ackman since there is no competitive advantage, so I would place the value no more than tangible book value at best with no more than a 90 second look at the financials.

The purpose of this post is also to study a Ponzi scheme. The response of the company to Ackman’s research leads me to say this company’s days are numbered.

BOOM and BUST

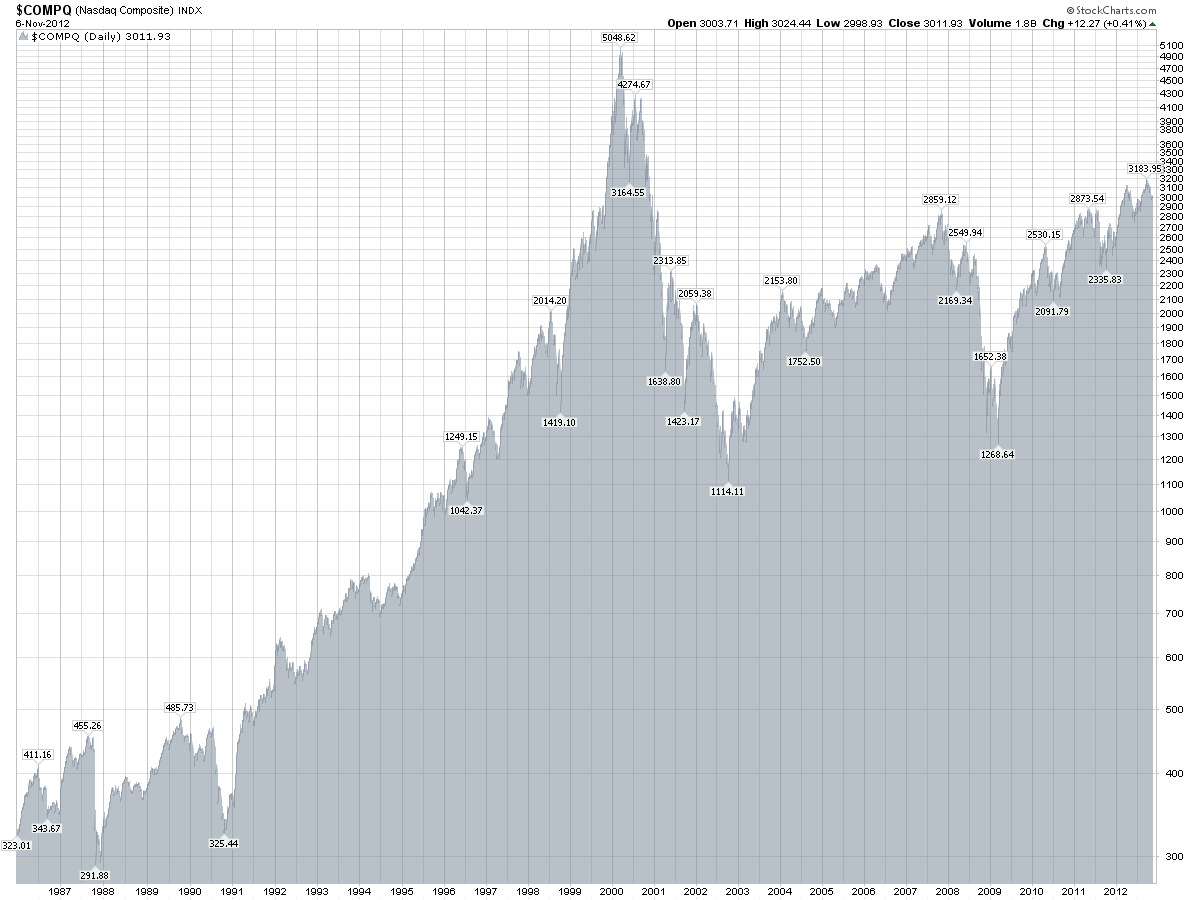

Could Austrian Business Cycle Theory Dotcom Boom and Bust have helped you as an investor? Buffett’s presentation on the Dotcom Bubble in early 1999 (See page 64) A Study of Market History through Graham Babson Buffett and Others. Note how the market went into a speculative frenzy, rising more than 50% AFTER Buffett’s speech. Human action can’t be predicted like a physics experiment.

An excellent book that predicted the bust was the The Internet Bubble: Inside the overvalue World of High Tech Stocks–and What you Need to Know To Avoid The Coming Shakeout by Anthony Perkins and Michael Perkins (1999 and 2001 editions).

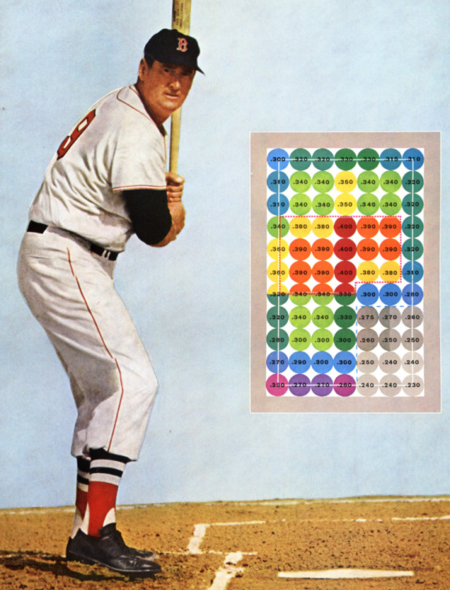

In his book The Science of Hitting, Ted explains that he carved the strike zone into 77 cells, each the size of a baseball. Swinging only at balls in his “best” cell, he knew, would allow him to bat .400; reaching for balls in his “worst” spot, the low outside corner of the strike zone, would reduce him to .230. In other words, waiting for the fat pitch would mean a trip to the Hall of Fame; swinging indiscriminately would mean a ticket to the minors.

If they are in the strike zone at all, the business “pitches” we now see are just catching the lower outside corner. If we swing, we will be locked into low returns. But if we let all of today’s balls go by, therecan be no assurance that the next ones we see will be more to our liking. Perhaps the attractive prices of the past were the aberrations, not the full prices of today. Unlike Ted, we can’t be called out if we resist three pitches that are barely in the strike zone; nevertheless,just standing there, day after day, with my bat on my shoulder is not my idea of fun.

When the above was written, the party that ultimately led to the tech bubble era valuations* had already begun in the equity markets.

Our last case on earnings quality was National Electric found by going into the case study value vault found in the blog post in the following link: http://wp.me/p2OaYY-1ub I promised to provide an answer. Before submitting my write-up on that case, perhaps the following case would be a good supplement to learn more about uncovering earnings quality. This case should be pretty obvious. Don’t cheat! Just use the material provided in the link below and answer the three questions in the HBS Case Study.

If you get stuck, here is a hint: (don’t look until you have tried to solve the case on your own! http://youtu.be/l-O5IHVhWj0With practice, certain figures and phrases in the notes to the financials should SCREAM OUT at you. Whatever happened to the CFO?

A Christmas Vault with goodies for all will be posted if someone posts their solution.

Behavioral economics and the closely related field of behavioral finance couple scientific research on the psychology of decision making with economic theory to better understand what motivates investors, employees, and consumers. This course will be based heavily on my own research. We will examine topics such as how emotion rather than cognition determines economic decisions, “irrational” patterns of thinking about money and investments, how expectations shape perceptions, economic and psychological analyses of dishonesty by presumably honest people, and how social and financial incentives combine to motivate labor by everyday workers and CEOs alike. This highly interdisciplinary course will be relevant to students with interests in General Management, Behavioral Finance, Entrepreneurship, Social Entrepreneurship, and Marketing.

This class has two main goals:

To introduce you to the range of cases where people (consumers, investors, managers, and significant others) make decisions that are inconsistent with standard economic theory and the assumptions of rational decision making. This is the lens of behavioral economics.

To help you think creatively about the applications of behavioral economic principles for the development of new products, technology based products, public policies, and to understand how business and social policy strategies could be modified with a deeper understanding of the effects these principles have on employees and customers.

About the Instructor(s)

Dan Ariely is the James B. Duke Professor of Psychology and Behavioral Economics at Duke University, with appointments in the Fuqua School of Business, the Center for Cognitive Neuroscience, and the department of Economics. As one of the foremost leaders in psychology and behavioral economics, Dr. Ariely has published his research in top economic, medical and psychology journals and is the author of Predictably Irrational (2008), The Upside of Irrationality (2010), and The (Honest) Truth About Dishonesty (2012), three bestselling general audience books about research in behavioral economics. In addition, he is the founding member of The Center For Advanced Hindsight. More information about Dan can be found at: www.danariely.com

The 2012 Holiday Book Survey has been tallied and the results can be found here. I want to thank everyone who participated in the survey.

The biography & memoir genre continues to lead the survey (Steve Jobs – Walter Isaacson & new comer The Passage of Power – Robert Caro) with social science still having a strong showing (The Signal and the Noise – Nate Silver & Thinking, Fast and Slow – Daniel Kahneman). Atlas Shrugged continues to breach the top 5 although falling from its #2 spot in the last two years to #5. Overall, biography & memoir and business & finance showed the strongest growth.

I hope you enjoy this years’ book list and find something of interest to read or gift. If you have any suggestions on how to improve on the survey, please let me know.

All the best and happy holidays.

—

Barry Pasikov, Managing Member of HazeltonCapitalPartners in Highland Park, IL 60035 Tel: 312-970-9202

Corporate treasurers have been driving the bull market in stocks, not retail and institutional investors. The Fed’s Flow of Funds data show that net issuance of corporate equities over the past year through Q3 was minus $274 billion. In other words, buybacks well exceeded gross issues. Nonfinancial corporations registered net buybacks of $419 billion, while the financial sector had net issuance of $119 billion and foreign corporations issued $25 billion, according to the Fed’s data.

The financial sector data include stock issuance by all ETFs, which rose to $174 billion over the latest four-quarter period. Excluding these ETFs, net issuance by financial corporations was minus $55 billion.

The Fed also compiles monthly data for total gross equity issuance. Over the past 12 months through October, corporations raised $152 billion. However, that was overshadowed by buybacks. Data available for the S&P 500 show that they totaled $406 billion over the past four quarters through Q2.

Expecting to invest successfully in a company like the one discussed in the prior post http://wp.me/p2OaYY-1ubwould be like expecting to win at this game (turn up the volume):

One trick that has helped me when analyzing a company for the first time is to go right to the back of the financial statements and look at the figures before I read what the CEO has to say. Be careful of hearing the story before you look hard at the numbers. Accounting is a rules based system that management can use (legally) to obscure economic reality from those who do not connect the numbers. Practice will help.

Let’s hear what a Pro (a reader, AGEDWISDOM) has to say:

This post should be a supplement to a two-year course in learning how to invest http://wp.me/p2OaYY-1u1

*** Purpose of this Article

When beginning the journey of value investing, one of the more technical questions that every non-accountant or non-finance personnel might face is the dreaded necessity to interpret financial statements. This post is a primer to get you started on the path to financial statement analysis. Rather than trying to read 50 books on accounting and getting hopelessly lost, this article can serve as a map in times of distress (or when you want to rip your hair off) in trying to interpret some arcane financial statements. Let’s get started, shall we?

Who am I?

Suffice to say, I am an accountant trained in the British tradition somewhere in Asia which means I’m more used to IFRS (accounting standards for mostly the rest of the world) as opposed to those trained in the US. With the convergence of accounting standards worldwide, there’s not that great a disparity between accounting standards between countries anymore. I have worked as an auditor for some years, so you can have some comfort in what I say. But as the saying goes, “Listen to everyone but judge for yourself”

Questions, questions and more questions

When you start your journey with value investing, you’ll be asking yourself many questions but the basic three might likely be:

1. How important is financial statement analysis to value investing?

Very. For those of you that have been following John’s blog, you can see a common thread in many of his posts. And that is, the X-Files motto (cue in the theme song…), “Trust No-one”. At the risk of sounding cliché, the financial statements is literally the last bastion of objectivity in the reporting of financial results.

What I mean by this is that if you rely on secondary sources, you’ll very likely run into people with interests or bias that may misinterpret the results for you. A prime example would be financial newspapers. Since most of these papers are owned by large conglomerates, they tend to report on the positive sides of things and keep the less savory things hidden. Prime example might be the recent Facebook IPO.

2. Is there a formula, models or a short-cut to interpreting financial statements?

No. There’s a very good reason for this.

Short-cuts, instant results… I’m too busy (ugh! typical mentality these days…) Whatever short-cuts or formulas that you intend to use… my advice, better BEWARE! You see, although financial statements is the so-called last bastion of objectivity, this doesn’t mean that the bastion is under daily assault by aggressive CEO’s and their Financial Controllers that do their darn best to try to present a pretty picture when it’s anything but. These CEO’s know whatever beautiful models that the analyst use. In the hands of a capable accountant, it’s entirely possible to subvert or render certain models useless.

Look in layman’s terms – it’s pretty simple. Let’s say my criteria for a value investing book is based Graham’s Security Analysis. Now, I find that I want to buy other good value investing books… but I want to know FAST… I want SHORTCUTS. I don’t actually want to ask other people or skim through the book (too busy, you see…), so using Graham’s book as a sample, the book must be:

1. Over 600 pages long

2. Be prohibitively expensive.

3. Have some foreword by prominent value investors of the day

Now, if a million other value investors use this so-called short cut as criteria to buy books on value investing, what will likely happen is that some publisher will start churning out huge amounts of titles to cater for these short-cuts… So, the publisher will in a sense pervert whatever models or indicators that you are using. These books could be utter rubbish, for all you know.

Hope I’m clear.

3. Why is it so mind-boggling, so arcane, so supercalifragilisticexpialidocious?

Elementary, my dear! It’s designed to be that way silly. We need to have some barriers of entry don’t we? Otherwise, a lot of professionally trained people would be out of a job.

Seriously though, the financial reporting world is much like an arms race. On one hand, you have the accounting profession trying to report results objectively and consistently. Unfortunately, on the other side, you have very aggressive, highly intelligent and extremely well paid consultants, accountants and investment bankers that find very creative ways to report profits in both good times and bad. Guess who’s winning the war?

As such, financial statements are becoming more and more complex, especially for those companies listed on the stock exchange.

Your job as a value investor is to attempt to separate the wheat from the chaff and attempt to weed out the distortions and look at the company’s results in an objective view so that you can access the value of the company.

The Journey

My advice on learning accounting is less reading, more doing. What do I mean by that? Financial statement analysis is a language on its’ own. Granted, it’s a more esoteric form of language but it’s still a language – the language of finance. You don’t learn a language by reading it but by applying it!

So, start small. Take baby steps. Grab a hold of financial statements of companies you are intimate with. These could be companies you are currently working in, or those you used to work for. It could be the financial statements of your relatives’ business. Something, anything…

Get 3-5 years’ worth of financial statements. Go through these financial statements and see what you can glean out of it. Find out how much you do know or don’t. Then, get a good book on financial statement analysis that you like and use it to help you analyze the financial statements further.

Write a short report summarizing what you think happened to the company during the 3-5 years. Was the sales improving? Are margins improving? Are profits improving? Are cash flows improving? More importantly, why, why, why? After that, talk to the person in-charge of the business and see whether your understanding of the business from interpreting the financial statements was correct or wrong. This will help you sharpen your skills when you tackle listed companies later on.

The Bottom-Up Approach

I am a firm believer of starting from the bottom up. Try to understand the nuts and bolts of interpreting financial statements especially the cash flow statement. No point trying to analyze the financial statements of a huge multinational with operations spanning several countries with hundreds of businesses and subsidiaries that run into several hundreds pages when you haven’t even tried your hand at something simple, yes?

Yes, you can start with a top-down approach later on… but always try to start with something small and build up on it.

Books, what Books?

Rather than starting with books, I suggest simple exam questions of accountancy bodies that try to test students abilities to interpret financial statements. That way, you get to try to speak in the language of finance and see how good you really are at it. There’s an added benefit of not dozing off whilst reading those books on accountancy…. phew… some are great (at putting people to sleep 🙂

Conclusion

So, there you have it. My 5 cents view on accounting. Hope it’s a useful guess post. Take it for what you will and hopefully, some of you find some value to it. Good luck!

You can never hear this lesson enough–beware of experts. In the end, no one knows the future. In fact, market gurus or experts have a greater than even chance of being wrong than a coin toss. Skip those odds and save yourself a lot of time.

Jon Stewart Puts CNBC on Trial. Cramer is roasted.

For a more detailed video of CNBC’s expert predictions (11 minutes) with more of Jon Stewarts’ savage commentary: http://youtu.be/N3LCZ3wTDoQ

Stewart is really going after CNBC’s promotional stock hyping while masquerading as a knowledgeable news source. Jim Cramer is part of the market ecology just like his famous predecessor, Gerald M. Loeb, the author of The Battle for Stock Market Survival (1935). Loeb, whom Forbes once tagged “the most quoted man on Wall Street,” became synonymous with the Hutton brokerage firm in the 1950s–and, not coincidentally, a flamboyant method of trading that generated brokerage commissions. Meanwhile, his visibility in the press was, as it often is, mistaken for respectability.

Despite all the ink that was spilled about him (and Cramer, today), there is no real contribution there of enduring value. Separate what is fundamental and new, or for that matter fundamental and old, from the kind of superficial sales-driven froth that Loeb and his PR machine have delivered. Loeb was the personification of the saying that” you can’t believe everything you read.” (Source: 100 Minds That Made The Market by Ken Fisher).

More proof that Chimps could pick stocks better (at least 50% randomly choosing stocks that will do better or worse) than “experts.”

Louis Rukeyser Shelves Elves Missed Market Trends Tinkering didn’t improve index’s track record for calling market’s direction.(MUTUAL FUNDS)

Investor’s Business Daily

November 01, 2001 Byline: KEN HOOVER

Louis Rukeyser, host of the popular “Wall Street Week” TV show, has quietly shelved his Elves Index, which was made up of his panel of experts’ stock market forecasts.

On Sept. 14, in the aftermath of the World Trade Center attack, he told his audience he was going to “give our elves a rest for a while.” He hasn’t mentioned them in weeks. And he declined to be interviewed on the subject.

He’s doing viewers a big favor. The index had a terrible track record. The elves said buy when they should have said sell, and vice-versa.

They were giddy with optimism as stocks crumbled the past two years. Maybe their darkest hour came in 1999 when an elf was indicted by a federal grand jury.

There’s a lesson here for investors. Pay no attention to experts, even if they are handpicked by the venerated Rukeyser. Sure, his show has helped PBS viewers gain an understanding of the arcane world of the stock market for three decades. But all investors need to learn to separate fact from opinion. And be especially leery if there’s a consensus about the market’s direction from Wall Street’s best minds. Chances are the market will go in the opposite direction.

“As far as I’m concerned, the experts are nothing more than the herd,” said Don Hayes, a money manager who closely follows market psychology. “Most people get their current market opinion from current market news. And news looks backward. The market is always looking forward six to 12 months.”

Rukeyser’s index worked like this: Each of 10 panelists voted on the Dow’s direction. A bullish vote counted +1. A bearish vote was -1. Zero was neutral. A +5 reading was supposed to be a buy signal. A -5 was a sell signal.

This system went against decades of research about market psychology. Several widely watched and reliable market indicators are built around the principle that markets are likely to do the opposite of consensus opinion.

After The Fact

The elves index started in 1989. It was reading +3 on July 27, 1990. That was a market top. It read -4 on Oct. 12, 1990. That was a market bottom. It gave its lowest reading ever, -6, on April 1, 1994.

That was after a nasty correction. The problem was the correction was almost over. The elves stood at -5 on Nov. 25, 1994, just as a powerful advance was about to begin.

The index was working just like any other contrarian sentiment indicator. Some market strategists started watching it that way.

The elves never gave another negative reading after May 1995. Rukeyser tinkered with the elves’ makeup, adding bullish votes. In May 1996, he purged five elves, replacing them with new blood.

That moved the index from +1 to +6, just in time for a correction that made some elves nervous. It fell back to +3.

On July 31, 1998, just as the market was starting to sink into a quick but painful bear market, the elves were a chipper +6. A 21% Dow plunge moved them down only to +3.

Rukeyser gave the elves another bullish boost just as the bubble was about to burst. In November 1999, he expelled long-time bear Gail Dudack. She was replaced with pension-fund manager Alan Bond.

Bond voted with the bulls, pushing the index to an all-time high of +7. A few weeks later it reached +8. If Dudack had stayed, she would have finally been right a four months later.

Bond was on the panel only five weeks. He was indicted on charges of taking $6 million in kickbacks. Last August while awaiting trial, he was arrested on new fraud charges. Trials are pending.

Nurock’s Record

As the market peaked in March 2000, the elves were bullish at +7. For 11 weeks during the worst bear market in a generation, the elves gave readings of +9. Late last year, Rukeyser started a parallel index for the Nasdaq. Its readings differed little from that of the Dow.

Before Rukeyser had the elves, he had Robert Nurock, who cobbled together 10 technical indicators into a composite that actually had a decent record, according to a study by technical analyst Arthur Merrill.

From 1974 to the end of 1986, the index correctly forecast the Dow’s direction 26 months in advance 79.5% of the time. That’s according to Merrill’s study, which was reported in the book “The Encyclopedia of Technical Market Indicators,” by Robert Colby and Thomas Meyers.

Nurock and Rukeyser parted company after the 1987 crash.

In The Intelligent Investor, Benjamin Graham sums up his investment philosophy by saying that an intelligent investor must be “businesslike” in approach. Investing in shares in a company is just like owning a share in a business enterprise and the investment must be approached as if one were buying a business, or a partnership in one.

There are four guiding principles for Graham:

1. Know the business

The investor needs to become knowledgeable about the business or businesses carried on by the company in which they propose to invest – what it sells, how it operates, what is the competitive environment, what are the threats and opportunities, the strengths and weaknesses.

An investor who bought a fruit shop, or a shoe factory, without investigating these things, and knowing them, would be foolish. The same applies to share investment. An investor who does not understand the business should not be investing in it.

2. Know who runs the business

An investor who cannot operate the business for himself or herself, needs a manager. This is the position of the average share investor, who owns a share of an enterprise that is run by others.

The owner of a business in this position would want a manager who will manage the business competently, efficiently and honestly. The share investor should not be satisfied with less. Unless the investor believes, through sound research, that the company is managed efficiently, competently and honestly, in the best interests of the shareholders, the investment should not be made.

3. Invest for profits

An investor would not normally buy a business that did not, on proper research, appear to have reasonable expectations of producing good profits over time. Share investors should take the same approach and buy, as Graham says, “not on optimism, but on arithmetic”.

4. Have confidence

Graham encourages investors to properly research their investments and, if they believe their investment judgment to be sound, to act on it. He cautions investors in this position against listening to others.

“You are neither right nor wrong because the crowd disagrees with you. You are right [or wrong] because your data and reasoning are right [or wrong].”

You can feel the fear, anger, and despair (visit the Yahoo Finance Board for JCP to get a feel for what small investors think), because you own the company. Whom do you blame, what can you do? The only way to stop the price from going down is to turn off your screen. 🙂

To gain a more realistic view of J.C. Penney’s prospects, however, here is the Deutsche Bank analyst Charles Grom: “Trends at J.C. Penney are obviously getting worse, not better, and we are becoming more and more convinced that sales in 2013 will also decline, which could lead to a going-concern problem next year.” (CS Editor: OK, if that were the case would the management and Board of Directors take a different course? Slow spending, sell off assets, etc. OR is the analyst just linearly extrapolating to come up with his thesis?)

The company’s stock has fallen nearly 50 percent since the beginning of the year. Even its online sales, through jcp.com, fell 37.3 percent last quarter from a year ago. Yet Mr. Johnson, a well-regarded and charismatic retailer who worked at Target before his meteoric rise at Apple, appears to be trying to mimic Steve Jobs and create what Mr. Jobs’s biographer, Walter Isaacson, called a “reality distortion field.” An opinion not a fact.

Andrew Burton/ReutersRon Johnson, chief executive of J.C. Penney, says the store renovation plan is a success. Mr. Johnson has spent the last several months trying to persuade investors that his transformation of J.C. Penney was the equivalent of Mr. Jobs’s efforts to turn around Apple a decade ago.

“You know, I watched this movie before. When I joined Apple in 2000, Apple was a company dwindling. Everyone said to me, ‘What are you doing there?’ ” Mr. Johnson told investors in September. “Apple wept through 2002 and I think sales were down 38 percent as we dreamed about becoming a digital device company. But Apple invested during that downturn. That’s when Apple built, started to build its chain of stores. That’s when Apple transitioned to Intel. That’s when Apple started its app division. That’s when Apple imagined and built the first iPod.”

O.K., Mr. Johnson, but that was Apple. And J.C. Penney is not Apple — and let’s be honest, it can never be Apple. The company doesn’t make its own magical, revolutionary products that bring tears of joy to its customers. It is a low-end department store that Mr. Johnson is hoping to turn into a slightly higher-end department store that sells clothing made mostly by other manufacturers.

Still, Mr. Johnson has sought to remake the company quickly, perhaps too quickly, by eliminating promotions and discounts, moving the stores more upscale, rebranding the company as JCP and putting in place a “fair and square” pricing model. (J.C. Penney is, however, putting on a special sale for the holidays.) Granted, JCP is no Apple, but what did Ron Johnson accomplish at Target–probably a better comparison.

Yet the renovations are hardly finished — or in some cases even started. Only 11 percent of its stores’ floor space has been remodeled with his successful specialty-store-within-a-store concept, in which he has opened up outposts for brands like Levi’s, Izod, Liz Claiborne and the Original Arizona Jean Company.

J.C. Penney may have been dying a slow death before Mr. Johnson’s arrival — some rivals used call it “death by coupon,” given the retailer’s penchant for discounts — but the company’s decline has only accelerated.

But the lessons, and successes, of the rollout of Apple stores are proving that they do not apply to Penney. While the customer experience at Apple is in a class by itself, and Mr. Johnson should rightly receive credit for that, the success of the stores was in large part a function of stunning products with a fan base that would stand outside stores for days in the rain to get their hands on them without any chance of a discount. Do you think there are customers who will ever stand outside J.C. Penney overnight for the next Liz Claiborne sweater? (J.C. Penney bought the Liz Claiborne brand last year.)

“Ron Johnson’s remake of JCP has assumed the consumer — the only one who matters — is the one who shops at Target or Macy’s or Nordstrom’s. Instead of pivoting on and strengthening the historic JCP brand (What brand?), Johnson’s decided to recreate the Target and Apple wheel, a move akin to Toyota suddenly deciding it’s Porsche. In short, a ridiculous and condescending move,” Margaret Bogenrief, a partner at ACM Partners, a boutique crisis management and distressed investing firm, recently wrote.

There is something romantic about watching Mr. Johnson try to remake a dying classic icon (So why did Sorkin call JCP a brand in the prior paragraph). At some gut level, you have to root for him. He’s making a bold bet. Transitions are inherently painful. And everyone loves a great comeback story.

Here’s the good news: In the stores that have been transformed, J.C. Penney is making $269 in sales a square foot, versus $134 in sales a square foot in the older stores. So the model itself is working. And Mr. Johnson has the support of the company’s largest shareholder, Pershing Square’s Bill Ackman, who personally recruited Mr. Johnson. If Mr. Johnson were starting with a blank slate, it might be a great business.

Mr. Ackman declined to comment. J.C. Penney did not make Mr. Johnson available.

Now here’s the bad news. Mr. Johnson still has to convert nearly 90 percent of his square feet of shopping space. That will very likely take $1 billion and as long as three years. If the sales decline that occurred last quarter accelerates, the company could run out of money. It now has about a half-billion in cash and access to a credit line for as much as $1.5 billion.

Of course, it remains possible that Mr. Johnson, who people close to him say is a realist, could always decide that the transformation is not working and change course to return to the old model of J.C. Penney and save all that money remodeling. But that would be a huge setback.

The question Mr. Johnson may be asking himself now is: What would Steve do?

A version of this article appeared in print on 11/13/2012, on page B1 of the NewYork edition with the headline: A Dose Of Realism For the Chief Of J.C. Penney.

So What is JCP worth? Forget the price today, what is the value of JCP? Since this is NOT a franchise, then this would be an asset type of investment. What is the real estate worth for JCP? I would start there and review with a critical mind my valuation of the company. Oh, and forget blaming anyone for the price being below your purchase price, perhaps or perhaps not, today is your luckiest day.

Part 1 of Graham’s Chapter 39 Newer Methods for Valuing Growth Stocks (Security Analysis 4th Ed.: http://wp.me/p2OaYY-1qQ

Also, what Graham said prior to this chapter on growth-stock investing:Growth in 2nd Edition

We will have another valuation case study next post to break-up this fusty theory. Read on.

Part 2: Valuation of DJIA in 1961 by this method.

In a 1961 article, Molodovsky selected 5 percent as the most plausible growth rate for DJIA in 1961- 1970. This would result in a ten-year increase of 63 percent, raise earnings from a 1960 “normal” of say, $35 to $57, and produce a 1970 expected price of 765, with a 1960 discounted value of 365. To this must be added 70 percent of the expected ten-year dividends aggregating about $300—or $210 net. The 1960 valuation of DJIA, calculated by this method, works out at some $575. (Molodovsky advanced it to $590 for 1961.)

Similarity with Calculation of Bond Yields

The student should recognize that the mathematical process employed above is identical with that used to determine the price of a bond corresponding to a given yield, and hence the yield indicated by a given price. The value, or proper price, of a bond is calculated by discounting each coupon payment and also the ultimate principal payment to their present worth, at a discount rate of required return equal to the designated yield. In growth-stock valuation the assumed market price in the target year corresponds to the repayment of the bond at par at maturity.

Mathematical Assumptions Made by Others

While the calculations used in the DJIA example may be viewed as fairly representative of the general method, a rather wide diversity must be noted in the specific assumptions , or “parameters,” used by various writers. The original tables of Clendenin and Van Cleave carry the growth-period calculations out as far as 60 years. The periods actually assumed in calculations by financial writers have included 5 years (Bing) , 10 years (Molodovsky and Buckley), 12 to 13 years (Bohmfalk), 20 years (Palmer and Burrell), and up to 30 years (Kennedy) . The discount rate has also varied widely –from 5 percent (Burrell) to 9 percent (Bohmfalk).

The Selection of Future Growth Rates

Most growth-stock valuers will use a uniform period for projecting future growth and a uniform discount or required-return rate, regardless of what issues they are considering (Bohmfalk, exceptionally divides his growth stocks into three quality classes, and varies the growth period between 12 and 13 years, and the discount rate between 8 and 9 percent, according to class.) But the expected rate of growth will of course vary from company to company. It is equally true that the rate assumed for a given company will vary from analyst to analyst.

It would appear that the growth rate for any company could be established objectively if it were based entirely on past performance for an accepted period. But all financial writers insist, entirely properly, that the past growth rate should be taken only as one factor in analyzing a company and cannot be followed mechanically in setting the growth rate for the future. Perhaps we should point out, as a cautionary observation, that even the past rate of growth appears to be calculated in different ways by different analysts.

Multiplier Applied to “Normal Earnings”

The methods discussed produce a multiplier for a dollar of present earnings. It is applied not necessarily to the actual current or recent earnings, but to a figure presumed to be “normal”—i.e., to the current earnings as they would appear on a smoothed-out earning curve. Thus the DJIA multipliers in 1960 and 1961 were generally applied to “trend-line” earnings which exceeded the actual figures for those years—assumed to be “subnormal.”

Dividends vs. Earnings in the Formulas. A Simplification

The “modern” methods of growth—stock valuations represent a considerable departure from the basic concept of J.B. Williams that the present value of a common stock is the sum of the present worths of all future dividends to be expected from it. True, there is now typically a ten-to-twenty – year dividend calculation, which forms part of the final value. But as the expected growth rate increased from company to company, the anticipated payout tends also to decrease, and the dividend component loses in importance against the target year’s earnings.

Possible variations in the expected payout will not have a great effect on the final multiplier. Consequently the calculation process may be simplified by assuming a uniform payout for all companies of 60 percent in the next ten years. If T is the tenth-year figure attained by $1 of present earnings growing at any assumed rate, the value of the ten-year dividends works out at about 2.1 + 2.1 T. The present value of the tenth-year market price works out at 48 percent of 13.5T, or about 6.5T. ? Hence the total value of $1 of present earnings –or the final multiplier for the shares—would equal 8.6T + 2.1.

Table 39-1 gives the value of T and the consequent multipliers for various assumed growth rates.

These multipliers are a little low for the small growth rates, since they assume only a 60% payout. By this method the present value is calculated entirely from the current earnings and expected growth; the dividend disappears as a separately calculated factor. This anomaly may be accepted the more readily as one accepts also the rapidly decreasing importance of dividend payments in the growth-stock field.

To be continued……

An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return.” Graham says “thorough analysis” means “the study of the facts in the light of established standards of safety and value” while “safety of principal” signifies “protection against loss under all normal or reasonably likely conditions or variations” and “adequate” (or “satisfactory”) return refers to “any rate or amount of return, however low, which the investor is willing to accept, provided he acts with reasonable intelligence.” (Security Analysis, 1934, ed., pp. 55-56)

Our Nation Today

The one aim of all such persons is to butter their own parsnips. They have no concept of the public good that can be differentiated from their concept of their own good. They get into office by making all sorts of fantastic promises, few of which they ever try to keep, and they maintain themselves there by fooling the people further. They are supported in their business by the factitious importance which goes with high public position. The great majority of folk are far too stupid to see through a politician’s tinsel. Because he is talked of in the newspapers all the time, and applauded when he appears in public, they mistake him for a really eminent man. But he is seldom anything of the sort.**

** This quotation is on page 67 of the 1991 collection, edited by Marion Elizabeth Rodgers, The Impossible Mencken; specifically, it’s from Mencken’s August 19, 1935 Baltimore Evening Sun essay entitled “The Constitution.”

Investment vs. Speculation

As Graham once put it, investors judge “the market price by established standards of value,” while speculators “base (their) standards of value upon the market price.” For a speculator, the incessant stream of stock quotes is like oxygen; cut it off and he dies.

You may think investing in a bank below book value is cheap and you may be correct on a grouped basis, but I don’t know how one truly can value a complex, huge financial company like Bank of America.

If you are analyzing a good company based on its normalized return on capital, you first have to identify economic capital. Financial groups (Banks, insurance companies, mutual funds) carry “third party capital” such as depositors, policyholders, and investors. This capital does not belong to shareholders, and is not provided by lenders. These are the assets deposited by the clients of these companies; bank deposits, for example. Due to the complexity of these groups, accurately segregating only the capital financing the company’s own assets is nearly impossible, especially since most of these assets are ‘market to market’, in other words, revalued every day at their market value.

Segregating capital and identifying cash flows for financial groups is difficult because, fundamentally, these businesses do not produce profits in the same way as non-financial groups. The latter simply add some value, via a proprietary process, to a certain amount of operating costs, and sell units (goods and services) of the total cost to its clients. The former capture capital flows, often thanks to a high financial leverage (partly from debt, partly from ‘third party capital’). Transform them and clip a remuneration for this process. Even if it were possible precisely to identify cash flows and economic capital for financial groups, the difference in balance sheet leverage would demand the calculation of an expected return (‘cost of capital’) specific to them.

Investors may find that excluding financial companies from their portfolio would, at worst, not put them at a disadvantage.

It is OK to speculate and invest, just know the difference.

Ponzi Finance

Carlo Ponzi, Alias Uncle Sam by Gary North Reality Check(Nov. 2, 2012)Carlo “Charles” Ponzi was a con man who was the Bernie Madoff of his era. For two years, 1918 to 1920, he sold an impossible dream: a scheme to earn investors 50% profit in 45 days. He paid off old investors with money generated from new investors. The scheme has been imitated every since.Every Ponzi scheme involves five elements:1. A promise of statistically impossible high returns

2. An investment story that makes no sense economically

3. Greedy investors who want something for nothing

4. A willing suspension of disbelief by investors

5. Investors’ angry rejection of exposures by investigatorsStrangely, most Ponzi schemes involve a sixth element: the unwillingness of the con man to quit and flee when he still can. Bernie Madoff is the supreme example. But Ponzi himself established the tradition.

The scheme, once begun, moves toward its statistically inevitable end. From the day it is conceived, it is doomed. Yet even the con man who conceived it believes that he can make it work one more year, or month, or day. The scheme’s designer is trapped by his own rhetoric. He becomes addicted to his own lies. He does not take the money and run.

This leads me to a set of conclusions. Because all Ponzi schemes involve statistically impossible goals, widespread greed, suspension of disbelief, and resistance to public exposure,

All fractional reserve banking is a Ponzi scheme.

All central banking is a Ponzi scheme.

All government retirement programs are Ponzi schemes.

All government-funded medicine is a Ponzi scheme.

All empires are Ponzi schemes.

All Keynesian economics is a Ponzi scheme.

But there is a difference between a private Ponzi scheme and a government Ponzi scheme. The private scheme relies on deception and greed alone. A government Ponzi scheme relies on deception, greed, badges, and guns. Read more:http://www.garynorth.com/public/10280print.cfm

Editor: Mr. Einhorn recognizes the dangers of the Federal Reserves Zero (manipulative) Interest Rate Policy. Where I take a different view is that the Fed’s Zero interest rate policy hurts savers and thus capital accumulation. Less capital hurts productivity and future economic growth. Regardless, no centrally planned economy has ever worked so why expect the Fed’s manipulated price control of interest rates to not end in tears? I do agree with Einhorn’s assessment of Bernanke’s theory of lowering interest rates to increase the “wealth” effect. Only a Ph.D can lack so much common sense.

Those guys have been reading csinvesting or von Mises.

Dr. De Soto on the Cause of the Current Financial Crises

Jesús Huerta de Soto, author of the thought-provoking book on economics ‘Money, Bank Credit and Economic Cycles’ and Professor of Political Economy at Rey Juan Carlos University, Madrid, explains the motivations behind British Prime Minister Robert Peel’s Bank Act of 1844. Prior to this Act, the free issuance of bank notes with claims on gold bullion wasn’t limited by British law, resulting in wild economic cycles that often led to bank runs and large gold flows out of the country as foreigners sought to exchange claims on gold for actual bullion.

He discusses why Robert Peel’s Bank Act of 1844 was a failure, despite its good intentions. Although the Act placed legal limits on banks’ issuance of paper notes, its failure to place the same limits on deposits allowed banks to pyramid deposits, which ultimately led to the fractional reserve banking that we have today.

The professor also explains the problem with the practice of fractional reserve banking, and why it leads to credit expansion that ultimately results in “boom and bust” economic cycles. “Virtual money” that is created easily by banks in the process of credit expansion during the boom contracts just as easily during the bust, resulting in recession.

Furthermore, he discusses the importance of capital theory and the nexus between interest rates, savings and prices. Huerta de Soto argues that Austrian Business Cycle Theory offers the best explanation of how and why economic cycles work, and the best explanation of the pay-offs between present consumption and long-term investment.

Also, he explains how artificial credit expansion leads to a temporary economic boom, and why it inevitably results in recession. Huerta de Soto uses the example of his native Spain, and how European Central Bank credit expansion distributed unevenly around the Eurozone, resulting in housing bubbles in periphery Eurozone countries like Spain, Greece and Ireland.

He lists the six microeconomic effects that result in the crack-up boom. Crucially, credit expansion leads to over-investment in capital goods. The credit expansion leads to first rising prices and then higher interest rates, and thus lower prices for capital goods. There are not enough real savings to support the demand for the increased number of capital goods, leading to recession.

The professor questions why central banks even exist, and why there is no free market in interest rates and money supply. Huerta de Soto wonders why people are happy with socialism for the banking system, and why more people are not correctly blaming central banks and fractional reserve banking for the financial crisis.

Huerta de Soto also explains why recessions are a necessary corrective to the excesses of the boom period. Huerta de Soto argues that in his native Spain, job losses in the construction and housing sector are necessary owing to over-investment in housing during the boom. He also criticises “stupid” politicians who thought that they had abolished boom-and-bust.

He criticises those who argue that currency devaluation is a cure for the recession, and argues that his native Spain is far better off with the euro than the peseta. Huerta de Soto argues that the euro is forcing politicians and the public to make honest choices about spending and is acting, beneficially, as a kind-of gold standard.

Further he argues that the European response to the financial crisis is preferable to the wildly expansionary policies chosen by the United States. Huerta de Soto argues that for this reason, he is more optimistic about the euro than the dollar.

Huerta de Soto wraps up with three key measures needed to improve our financial system. First, Peel’s Bank Act needs to be completed which means a 100% reserve is required for demand deposits. Second, central banks need to be abolished. And lastly, the issuance of money should be privatised, leading to a free gold standard.