is not a malfunctioning entrepreneurial impulse, but an artificial lengthening of production and overcapacity in fixed assets induced by the fractional reserve banking system. Everyone who keeps funds in the market or in a bank is vulnerable, since it is cash deposits that banks use to fund the reckless expansion. When the banking system blows up—as it must—conservative savers lose their savings just as surely as ardent speculators: that is the real horror and also why the existence of a dynamic sector in the economy does not change the credit bubble analysis.

I wonder how Mr. Pabrai thinks the market misprices a security by 90%. It has been my experience that when you think you have a company priced at $10 per share but worth $100, you had better check your valuation. For a stock to go up 10 times, you are betting on profitable growth or a change in the environment.

The value of the video is given in the reminder to go through your value lines or stock guides to give you context and ideas! In the course I am designing, we will have access to Value-Line to constantly search.

Go where they ain’t (but patience is needed in huge dollops):

HEDGE FUND ANALYST QUIZ

Your boss calls you into his office and asks if the Fed should keep raising rates? Then he asks if the Fed should lower rates? What do you tell him? There is ONLY one correct answer. To KEEP your job you must answer correctly.

June 19, 2017

Hyman Minsky was an economist who popularised the idea that “stability leads to instability”. According to Minsky and his followers, credit expands rapidly during the good times to the point where a lot of borrowing is being done by financially fragile/vulnerable entities, thus sowing the seeds of a financial crisis. That’s why the start of a financial crisis is now often referred to as a “Minsky moment”. Unfortunately, Minsky’s analysis was far too superficial.

Minsky described a process during which financing becomes increasingly speculative. At the start, most of the debt that is taken on can be serviced and repaid using the cash flows generated by the debt-financed investment. At this stage the economy is robust. However, financial success and rising asset prices prompt both borrowers and lenders to take on greater risk, until eventually the economy reaches the point where the servicing of most new debt depends on further increases in asset prices. At this stage the economy is fragile, because anything that interrupts the upward trend in asset prices will potentially set in motion a large-scale liquidation of investments and an economic bust.

This description of the process is largely correct, but rather than drilling down in an effort to find the underlying causes Minsky takes the route of most Keynesians and assumes that the process occurs naturally. That is, underpinning Minsky’s analysis is the assumption that an irresistible tendency to careen from boom to bust and back again is inherent in the capitalist/market economy.

In the view of the world put forward by Keynesians in general and Minsky in particular, people throughout the economy gradually become increasingly optimistic for no real reason and eventually this increasing optimism causes them to take far too many risks. The proverbial chickens then come home to roost (the “Minsky moment” happens). It never occurs to these economists that while any individual could misread the situation and make an investing error for his own idiosyncratic reasons, the only way that there could be an economy-wide cluster of similar errors at the same time is if the one price that affects all investments is providing a misleading signal. The one price that affects all investments is, of course, the price of credit.

Prior to the advent of central banks the price of credit was routinely distorted by fractional reserve banking, which is not a natural part of a market economy. These days, however, the price of credit is distorted primarily by central banks, and the central bank is most definitely not a natural part of a market economy. Therefore, what is now often called a “Minsky moment” could more aptly be called a “central-bank moment”.

I expect the next “central-bank moment” to arrive within the coming 12 months. I also expect that when it does arrive it will generally be called a “Minsky moment” or some other name that deftly misdirects the finger of blame, and that central banks will generally be seen as part of the solution rather than what they are: the biggest part of the problem.

Does “Momentum” Investing work with “Value” Investing?

See the research paper by Nicholas Barberis below. Barberis concludes that value and momentum are driven by biases that mirror one another. Value is driven by an overreaction problem in which humans are too quick to draw conclusions from a small amount of recent data. In contrast, momentum is driven by an underreaction issue, which is the opposite of verreaction. With underreaction, humans are slow to update their views based on new evidence, which could be due to a systematic behavior bias and/or due to the fact human beings simply have limited cognitive power.

A lot to ponder. I recommend Quantitative Investing by Wesley Gray. Momentum investing is NOT growth investing (buying price at high multiples to underlying fundamentals), because momenum investing is strictly based on recent price movements not fundamentals.

Strategic Presentation May 2017b What would show you that this management team allocates capital well in their resource sector? Are their actions EXTREMELY rare in the Junior Resource Mining industry?

In a blog post in March of this year I discussed the limitations of sentiment as a market timing tool. I wrote that while it can be helpful to track the public’s sentiment and use it as a contrary indicator, there are three potential pitfalls associated with using sentiment to guide buying/selling decisions. Here are the pitfalls again:

The first is linked to the reality that sentiment generally follows price, which makes it a near certainty that the overall mood will be at an optimistic extreme near an important price top and a pessimistic extreme near an important price bottom. The problem is that while an important price extreme will always be associated with a sentiment extreme, a sentiment extreme doesn’t necessarily imply an important price extreme.

The second potential pitfall is that what constitutes a sentiment extreme will vary over time, meaning that there are no absolute benchmarks. Of particular relevance, what constitutes dangerous optimism in a bear market will often not be a problem in a bull market and what constitutes extreme fear/pessimism in a bull market will often not signal a good buying opportunity in a bear market.

The third relates to the fact that regardless of what sentiment surveys say, there will always be a lot of bears and a lot of bulls in any financial market. It must be this way otherwise there would be no trading and the market would cease to function. As a consequence, if a survey shows that almost all traders are bullish or that almost all traders are bearish then the survey must be dealing with only a small — and possibly not representative — segment of the overall market.

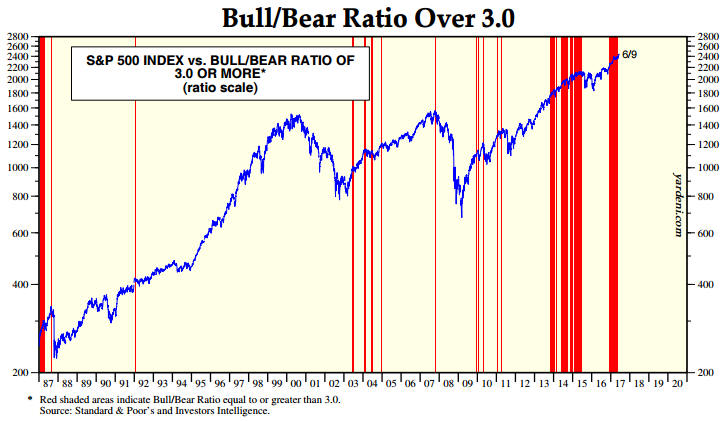

I went on to write that there was no better example of sentiment’s limitations as a market timing indicator than the US stock market’s performance over the past few years. To illustrate I included a chart from Yardeni.com showing the performance of the S&P500 Index (SPX) over the past 30 years with vertical red lines to indicate the weeks when the Investors Intelligence (II) Bull/Bear ratio was at least 3.0 (a bull/bear ratio of 3 or more suggests extreme optimism within the surveyed group). An updated version of the same chart is displayed below.

The chart shows that while vertical red lines (indicating extreme optimism) coincided with most of the important price tops (the 2000 top being a big exception), there were plenty of times when a vertical red line did not coincide with an important price top. It also shows that optimism was extreme almost continuously from Q4-2013 to mid-2015 and that following a correction the optimistic extreme had returned by late-2016.

Sentiment was at an optimistic extreme late last year, at an optimistic extreme when I presented the earlier version of the following chart in March and is still at an optimistic extreme. In effect, sentiment has been consistent with a bull market top for the bulk of the past four years, but there is still no evidence in the price action that the bull market has ended.

Regardless of what happens from here, four years is a long time for a contrarian to be wrong. See more at http://www.tsi-blog.com

Lesson? Always place data into context and do not rely on any one piece of information. Sentiment can be useful as part of an over-all picture of a market or company.

This time, the Fiat Chrysler CEO went a step further than usual by declaring that the latest plan for the company is essentially a one-way bet on cheap gas. Production of compact cars will end to free up production capacity for high-margin, low-mileage Jeeps and RAM trucks.

This, combined with Fiat’s more or less complete lack of a fuel economy or electrification strategy beyond buying emissions credits from other manufacturers “foolish” enough to produce electric and hybrid “compliance cars,” is quickly making Marchionne, if not an industry joke, then certainly yesterday’s man.

At least, that is what people are saying. I have an alternate hypothesis. The Auto Industry Is Not Heading to a Good Place (The author, in my opinion, has the correct thesis. Ride sharing, Uber, Tesla, more complex electronics mean less demand and more investment to run in place).

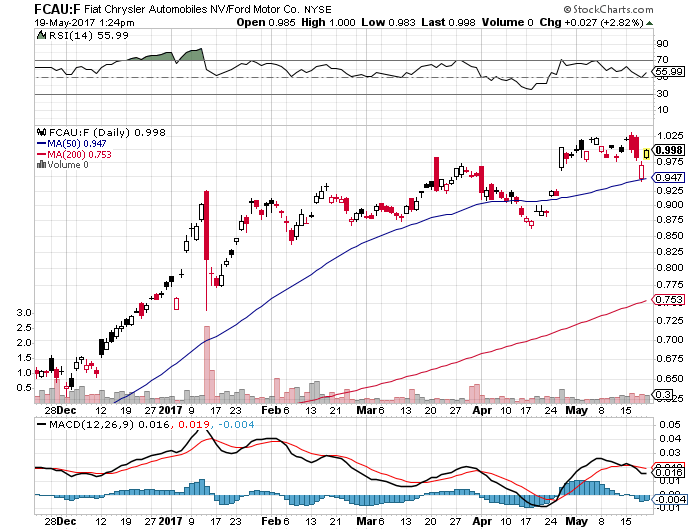

Fiat vs. Ford above

Fiat (FCAU) has done slightly better than GM and much better than Ford (F). However, the auto industry is in a bad place that will worsen.

The context is frightening. Global fuel economy and emissions regulations are becoming so strict that it is possible to meet them only with partial or full electrification of the automobile. And the existing automobile production system, based primarily on stamping sheet metal and amortizing heartbreaking development costs and capital expenditures over millions of units, is incredibly capital inefficient.

What’s more, the industry’s move towards electric vehicles represents a significant challenge to the traditional strategic landscape an automaker faces. An electric vehicle has drastically fewer moving parts than an internal combustion vehicle and is, by design, far more modular, meaning that barriers to new entrants are significantly lower.

Electric vehicles are also far more uniform in their driving dynamics, because there is little scope for refining an electric motor with one moving part. Swathes of engineering and marketing investments become irrelevant. And both ride-sharing enterprises and developments in automation seem increasingly likely to grow beyond niche markets into something properly disruptive to the car ownership business model.

Marchionne Knows This

Last year, Marchionne presented a uniquely critical slide deck about the way the auto industry destroys capital. His argument was that, unless the industry consolidates and stops duplicating engineering costs (e.g., every car manufacturer has its own separately developed but fundamentally identical 2.0L 4-cylinder petrol engine), then the market will eventually force its hand, having gotten sick of miserly returns on billions in investments.

The industry response to this slide deck was more or less complete agreement, with the caveat that competitors would not have to outlast the market so much as merely outlast Fiat Chrysler. Marchionne then pursued an odd and ultimately unsuccessful merger with GM’s Mary Barra, who confidently rejected Fiat Chrysler’s plan, noting, “We are merging with ourselves.” (This presumably referred to GM’s decades-long quest to bring rationality to its stable of brands.)

GM is not only merging with itself, it is also “disrupting” itself — as evidenced by their recently announced Chevy Bolt long-range, affordable electric car. The company claimed the Bolt was designed to be the perfect car for ride-sharing apps. Just before launching the Bolt, GM announced a $500 million investment into Lyft, the main competitor to Uber.

This no doubt surprised competitors who have been making efforts to disabuse markets and investors of the notion that they would become mere providers of hardware to ride-sharing companies like Uber or autonomous car suppliers like Google. Dieter Zetsche, CEO of Daimler, remarked “We do not plan to become the Foxconn of Apple.”

Manufacturers Are Going to Have to Invest

In fact, the bosses of Daimler, BMW, and Audi went looking behind the couch for some spare change to buy joint ownership of Nokia’s (remember them?) mapping service HERE, and did so primarily to stop their rival bidder – Uber – from buying it. High-resolution maps are crucial to autonomous cars; Uber’s CEO has said that, if Tesla can make good on their promise of a long-range, autonomous electric car, he would buy “all” of them.

The Germans are thus investing billions into electric vehicles made out of carbon fiber that pilot themselves using super-high resolution maps, all the while fighting back against Apple and Google’s requests for access to their cars’ infotainment systems. Their global leadership of the auto industry will have to be pried from their cold, dead hands.

Meanwhile, all the difficult bits of the Chevy Bolt (“custom-built” for Lyft, remember) are built in large part by Korea’s LG. One wonders why Lyft (or Uber) would not simply buy the next model directly from LG? I guess even if there is no Foxconn for cars yet, there may be soon. Remember, electric cars are far more modular than internal combustion cars.

Marchionne Says “No Thanks”

Or, if not him, then certainly the Agnelli family. A sort of Italian royalty who control Fiat Chrysler (and Marchionne) via their ownership of the Exor holding company, the Agnellis have been showing signs that they are tiring of the endless drama surrounding Fiat and the auto industry in general. They bought a stake in The Economist in 2015 in a move towards media, but the recent de-conglomeration of Fiat has been noticeable in other ways.

First, in 2013, Fiat’s industrial division was de-merged and combined with CNH Global (maker of tractors under the Case IH and New Holland brands) into a separate company, CNH Industrial. Most recently, Ferrari, the jewel in the Fiat Chrysler stable of brands, was floated in New York.

Speaking of Ferrari, Marchionne took advantage of a recent dip in the fortunes of Ferrari’s eponymous Formula 1 team to unceremoniously eject Luca di Montezemolo as president and chairman of Ferrari and replace him with . . . himself. It should be noted that di Montezemolo was appointed by Gianni Agnelli himself after the death of the founder, Enzo Ferrari, and is a bona fide business superstar in Italy. Marchionne has been playing an increasingly active part in the politics of Formula 1 recently, something that will no doubt continue to make for a less stressful (but still stimulating) retirement when Marchionne puts on his famous blue sweater for the last time in 2018.

But for now, Marchionne has seen the future. Large subcontractors will produce partially or fully autonomous electric vehicles, with the sole differences between them being brand value and design. The car makers that survive may well simply produce cars for Google (Ford recently signed an agreement along these lines), Apple, or Uber. Some, like BMW or Mercedes-Benz, may survive because of their brand and design qualities. Fiat Chrysler does not have this.

Marchionne doesn’t care about expensive gas or electric vehicles because his plan is simple:

Sell the profitable Jeep/RAM brands to another conglomerate that does not compete in these segments (for example, Hyundai KIA).

Sell the unprofitable Fiat to anyone who will take it. Perhaps synergies in the lucrative European light commercial vehicle segment will attract another European maker, such as PSA Peugeot Citroën, whose CEO, Carlos Tavares, has ambitions that were thwarted at his previous employer, Renault.

Sell Alfa Romeo and Maserati to someone who could use a strong brand. Perhaps Volkswagen will finally get hold of its prized Italian trophy if they can sort out their global legal woes.

Retire to play with his giant Formula 1 Scalextric set. Marchionne has been mocked for his firms’ strategy, which has been attributed to hubris. But perhaps he is the one seeing clearest of all.

Is the best way to deal with disruption simply to step out of the way?

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

Tit-for-Tat Competitive Analysis

Question: Who wins when–in a perfectly competitive market–competitors fight each other? Prize awarded for best answer.

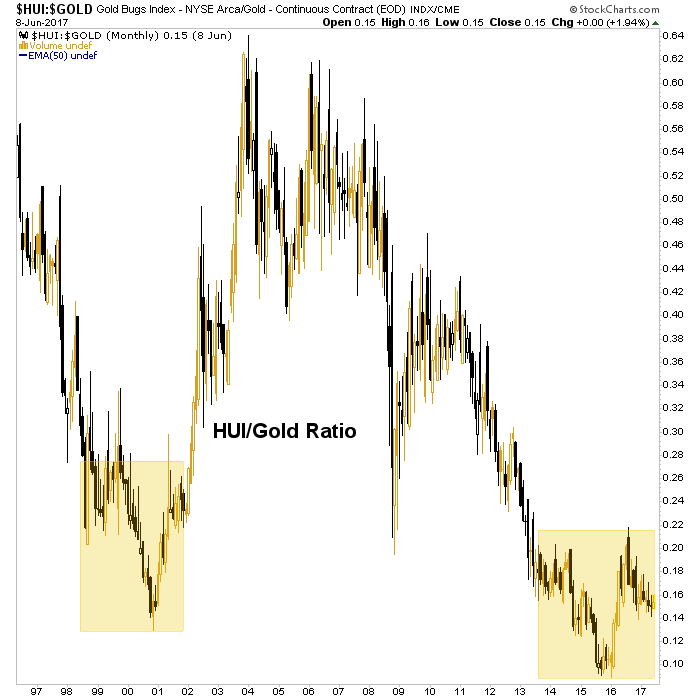

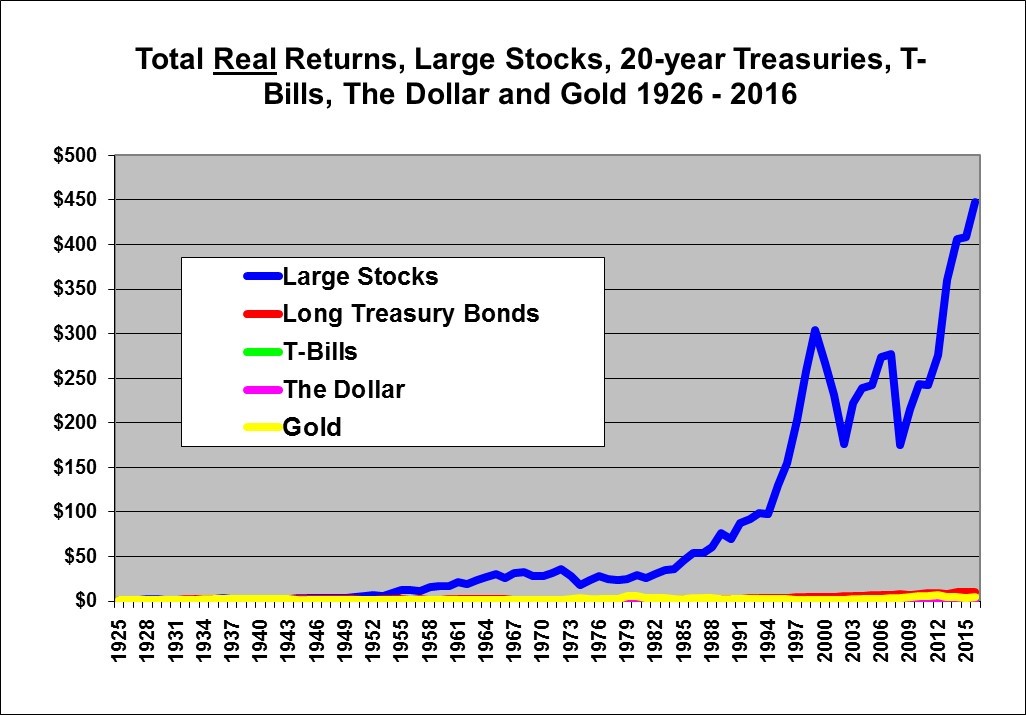

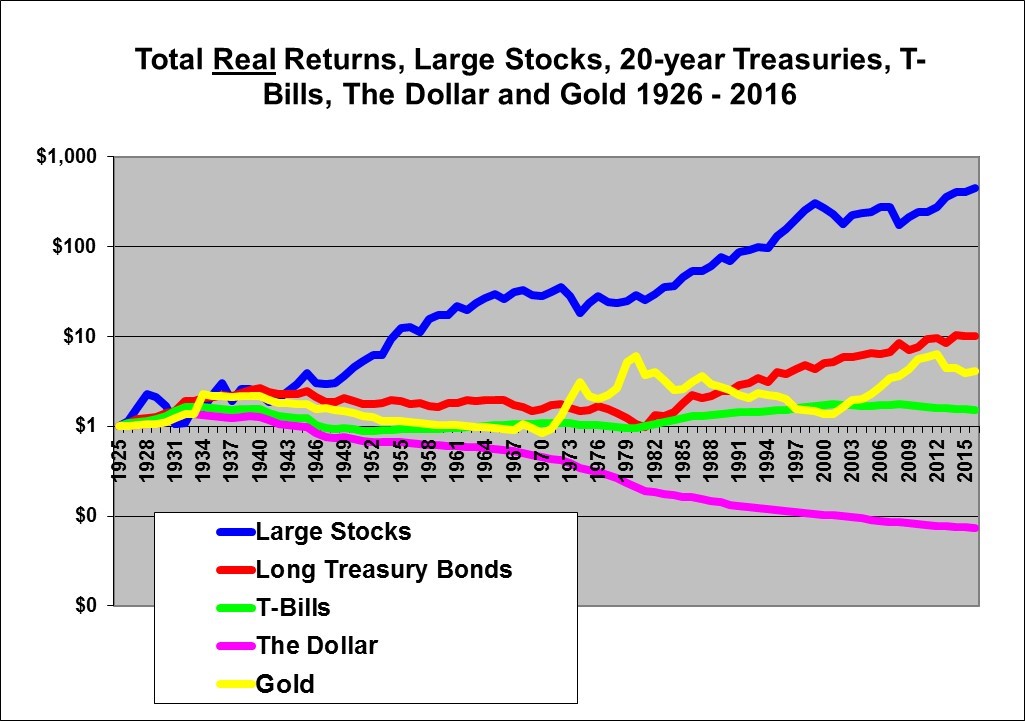

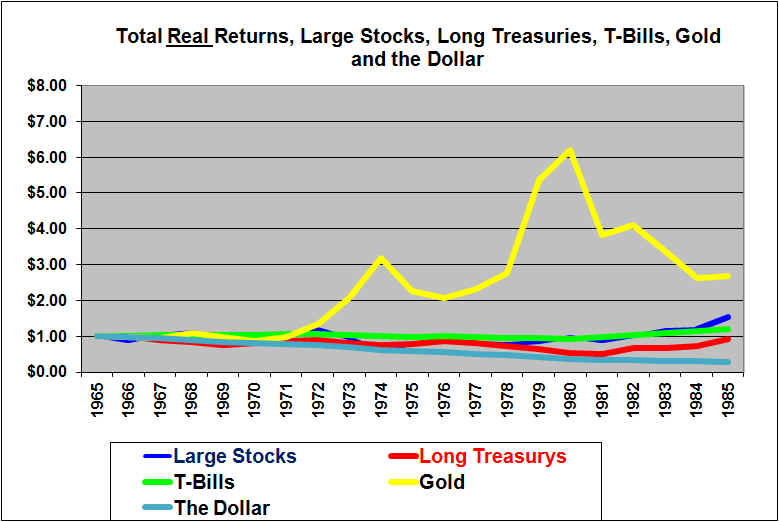

The chart above shows gold “outperforming” stocks, but note the time period. 1971 was when President Nixon unhinged the dollar from gold. Be careful when assessing performance over a set time period.

I don’t always agree with Dr. Damodaran, but the video can help any analyst writing a research report. You have to link your story to numbers. He mentions that he prefers to teach history majors how to value than teach engineers how to be creative/tell a story with their numbers.

The mistake Prof. Damodaran made on Vale was not normalizing the biggest cyclical boom in iron ore prices in the past five hundred years.

Follow the discussion on valuing UBER. This is a good exercise for valuing platform/network companies: Damordaran on UBER FiveThirtyEight