The successful investor is a master of paradox. He expects the unexpected, distrusts the experts and loves what the majority hates. He believes that, in markets as in heaven, the first shall be last and the last shall be first.

There’s fool’s gold–pyrite–and then there’s fools’ gold owned by idiots who will trade it for worthless dollars.

History of the trading pits: http://www.tradingpitblog.com/ Great blog!

What is money? What is money_ TTMYGH_17_Feb_2014

Assessing Long-Term Account Performance

http://www.tocquevillefunds.com/insights/secular-lessons

Hard wired for bubbles (Dan Ariely)

http://www.peakprosperity.com/podcast/84804/dan-ariely-why-humans-hard-wired-create-asset-bubbles?

Thinking properly about “cash sitting on the sidelines.” Or how to think properly. http://www.acting-man.com/?p=28594

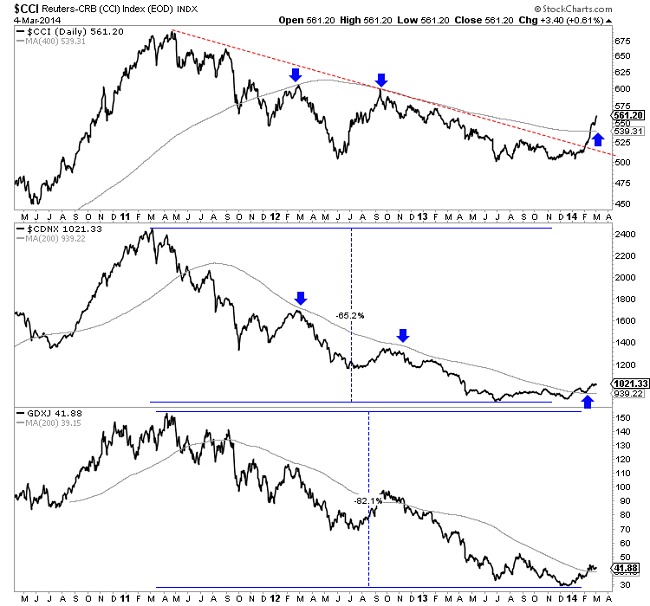

Rick Rule on Gold Miners and Gold (Of course, when you ask a barber if you need a haircut…..But, he has a lot of experience in these markets. Survival is proof enough of competence in the miners!

AUDIO: http://kingworldnews.com/kingworldnews/Broadcast/Entries/2014/2/16_Rick_Rule_files/Rick%20Rule%202%3A16%3A2014.mp3

Rick Rule: We’ve said on your interviews, ‘You’ve suffered through the pain, why not hang around for the gain?’ I think we’re in the beginning of the gain session. Your readers and listeners, at least those who are new to the sector, need to understand that we are in a rising channel, but we are in a rising channel that is going to have higher highs and higher lows….

It’s going to be volatile. You are going to see 15% declines, and you are going to see 20% gains for seemingly no reason. The important thing to note is that I certainly believe the precious metals sector and the precious metals shares have bottomed and they are moving up.

We’re tempted to say that the bottom was reached and the recovery in the junior shares began in July of last year. Certainly, November, December, and January have seen pretty good rises — 40% share price escalations have not been uncommon.

It is not uncommon for well-constructed portfolios in a precious metals market recovery to experience five-fold or ten-fold gains. So for those people who went through the downturn and are now beginning to experience the upturn, firstly, congratulations. And second, keep your seatbelt on. It’s going to be very volatile but I think we are higher, probably substantially higher from here.”

Eric King: “William Kaye, the outspoken hedge fund manager from Hong Kong, was telling King World News that demand (for gold) out of China is just ‘insatiable.’ Your thoughts on the physical demand we’ve seen around the globe — it’s been quite stunning.”

Rule: “He would know better than I with regard to Hong Kong demand, but certainly we’ve seen very strong physical demand from around the world. A lot of the physical demand has taken place right here in the United States.

What’s interesting about his (Kaye’s) statement is the dichotomy between the private physical markets and the long-term markets. I can’t help going back to an announcement about 12 months ago, when the Germans wanted to repatriate their 1,500 tons of gold, and they were told by the US government that it would take seven years (to get back only 300 tons of gold) that was theirs.

At the same time, over 30 days, in the physical market, Chinese retail buyers bought and took delivery of 1,120 tons of gold. One of the things that this points out is the very, very odd dichotomy between central bank and multilateral institutional holdings of gold, and the paper gold market on one side, and the honesty of the physical market on the other side.

My suspicion is that the physical market is prevailing and will continue to prevail over the paper market. And the subtext of this is that the documented large (gold) short positions that exist in the paper market may get their long awaited religious experience as they are unable to deliver against futures obligations.”

from www.kingworldnews.com

Seth Klarman on investing vs speculating:

Mark Twain said that there are two times in a man’s life when he should not speculate: when he can’t afford it and when he can. Because this is so, understanding the difference between investment and speculation is the first step in achieving investment success.

To investors stocks represent fractional ownership of underlying businesses and bonds are loans to those businesses. Investors make buy and sell decisions on the basis of the current prices of securities compared with the perceived values of those securities. They transact when they think they know something that others don’t know, don’t care about, or prefer to ignore. They buy securities that appear to offer attractive return for the risk incurred and sell when the return no longer justifies the risk.

Investors believe that over the long run security prices tend to reflect fundamental developments involving the underlying businesses. Investors in a stock thus expect to profit in at least one of three possible ways: from free cash flow generated by the underlying business, which eventually will be reflected in a higher share price or distributed as dividends; from an increase in the multiple that investors are willing to pay for the underlying business as reflected in a higher share price; or by a narrowing of the gap between share price and underlying business value.

Speculators, by contrast, buy and sell securities based on whether they believe those securities will next rise or fall in price. Their judgment regarding future price movements is based, not on fundamentals, but on a prediction of the behavior of others. They regard securities as pieces of paper to be swapped back and forth and are generally ignorant of or indifferent to investment fundamentals. They buy securities because they “act” well and sell when they don’t. Indeed, even if it were certain that the world would end tomorrow, it is likely that some speculators would continue to trade securities based on what they thought the market would do today.

Speculators are obsessed with predicting – guessing – the direction of stock prices. Every morning on cable television, every afternoon on the stock market report, every weekend in Barron’s, every week in dozens of market newsletters, and whenever businesspeople get together, there is rampant conjecture on where the market is heading. Many speculators attempt to predict the market direction by using technical analysis – past stock price fluctuations – as a guide. Technical analysis is based on the presumption that past share price meanderings, rather than underlying business value, hold the key to future stock prices. In reality, no one knows what the market will do; trying to predict it is a waste of time, and investing based upon that prediction is a speculative undertaking.

Market participants do not wear badges that identify them as investors or speculators. It is sometimes difficult to tell the two apart without studying their behavior at length. Examining what they own is not a giveaway, for any security can be owned by investors, speculators, or both. Indeed, many “investment professionals” actually perform as speculators much of the time because of the way they define their mission, pursuing short-term trading profits from predictions of market fluctuations rather than long-term investment profits based on business fundamentals. As we shall see, investors have a reasonable chance of achieving long-term investment success; speculators, by contrast, are likely to lose money over time. www.shortsideoflong.com