About 400 students from 40 different countries are enrolled.

I will cease to enroll after 1 pm today (Monday) New York City time.

Sorry, but time constraints rule.

Thanks for the interest and the journey begins.

About 400 students from 40 different countries are enrolled.

I will cease to enroll after 1 pm today (Monday) New York City time.

Sorry, but time constraints rule.

Thanks for the interest and the journey begins.

Posted in Uncategorized

Contrariwise, if it was so, it might be; and if it were so, it would be; but as it isn’t, it ain’t. That’s logic.

~ Lewis Carroll

When dealing with people, remember you are not dealing with creatures of logic, but creatures of emotion.

~ Dale Carnegie

Mastering others is strength. Mastering yourself is true power.

~ Lao Tzu

Your goal should be to find an investment approach that works for you. You will need to determine your investment edge.

You should read:

the Preface from Deep Value (Toby Carlisle)

Chapter 20_Margin of Safety Concept

Buffett Klarman and Graham on Mr Market

Behavioral Portfolio Management

Questions from the readings:

You can email me at Aldridge56@aol.com with LESSON 1 in the title with questions and answers or post here in the comments section. If you don’t have time or wish to pass then come back to this lesson later.

I will be asking for one or two volunteers who wish to research the article BEHAVIORAL PORTFOLIO MANAGEMENT. You will need to read the articles below and then determine if the author’s five criteria will work. Over this course, I will probably assign twenty or so special projects. Then we will share your work/efforts.

SSRN_Behavioral Measures of Expected Market Return

SSRN The Importance of Investment Strategy_Howard

SSRN Behavioral Portfolio Management_Thomas

Taking-the-emotion-out-of-investing

Making Money Out of Emotions How investors fail because of their own brain. Solution: Pre-program your portfolio.

—

I will post the review of the lesson/readings by the end of the week. There will be supplementary material posted throughout the week. You will also be emailed any postings.

STATUS

Right now we have about 250 fanatics signed up. As a skeptic, I wonder if there are really that many fanatics spread across the globe. “Students” range from raw beginners to forty-year veterans with CFAs, MBAs, MAs, and dozens of letters after their names. Students (men and women) are located in India (a lot!), Germany, France, Sweden, North Africa, South American, Canada, and Alaska.

The only requirement is to be skeptical. Try to prove/disprove what you read and hear–especially what you might think is true. Can you apply concepts and principles to your own unique location/situation?

If you sent me an email as instructed by the prior post on this blog at http://wp.me/p2OaYY-2BU, then you should have received the first lesson and two emails with attachments. If not, then email me again with the title DEEP VALUE. If within twenty-four hours you haven’t received an email, then do it again, and I will make sure you receive the lesson.

I have to close the course because handling incoming students will be very cumbersome after the first class. For those too late to “register” then follow along with the blog since I will be posting questions on the readings. There are no grades; the market will do that for you.

Posted in Uncategorized

My Idea:

This is an experiment to see if a group of serious students of value investing can learn from each other and an in-depth reading of the course materials to become better investors. If you send me your email to aldridge56@aol.com (DEEP VALUE COURSE) in the title, I will send you the course materials (Thanks to a reader for contributing!). There is a catch however. You are expected to do the readings and comment/participate in the discussion in the comments section. So don’t seek unless committed to being an active participant. Since there will be supplementary readings for each chapter of the book (see chapter titles below), we will take one to two weeks per chapter. You may have homework or be asked to research investment questions further. I won’t think any less of you if you decide to pass–this course is only for fanatics. Course will start a week or two into the New Year.

Description of the book below (also type in DEEP VALUE) in the search box of this box and view some of the videos on deep value and the author, Toby Carlisle. Also, go to www.greenbackd.com and look at the past ten posts.

Book blurb from Wiley:

Deep Value: Why Activist Investors and Other Contrarians Battle for Control of Losing Corporations is a must-read exploration of deep value investment strategy, describing the evolution of the theories of valuation and shareholder activism from Graham to Icahn and beyond. The book combines engaging anecdotes with industry research to illustrate the principles and methods of this complex strategy, and explains the reasoning behind seemingly incomprehensible activist maneuvers. Written by an active value investor, Deep Value provides an insider’s perspective on shareholder activist strategies in a format accessible to both professional investors and laypeople.

The Deep Value investment philosophy as described by Graham initially identified targets by their discount to liquidation value. This approach was extremely effective, but those opportunities are few and far between in the modern market, forcing activists to adapt. Current activists assess value from a much broader palate, and exploit a much wider range of tools to achieve their goals. Deep Value enumerates and expands upon the resources and strategies available to value investors today, and describes how the economic climate is allowing value investing to re-emerge. Topics include:

Table of Contents

Chapter 1 The Icahn Manifesto 1

Chapter 2 Contrarians at the Gate 19

Chapter 3 Warren Buffett: Liquidator to Operator 35

Chapter 4 The Acquirer’s Multiple 53

Chapter 5 A Clockwork Market 77

Chapter 6 Trading in Glamour: The Conglomerate Era 99

Chapter 7 Catch a Falling Knife 119

Chapter 8 The Art of the Corporate Raid 151

Chapter 9 How Hannibal Profits From His Victories 169

Chapter 10 Applied Deep Value 187

Posted in Free Courses, Search Strategies, Special Situations, Valuation Techniques

Tagged Course, Deep Value, value investing

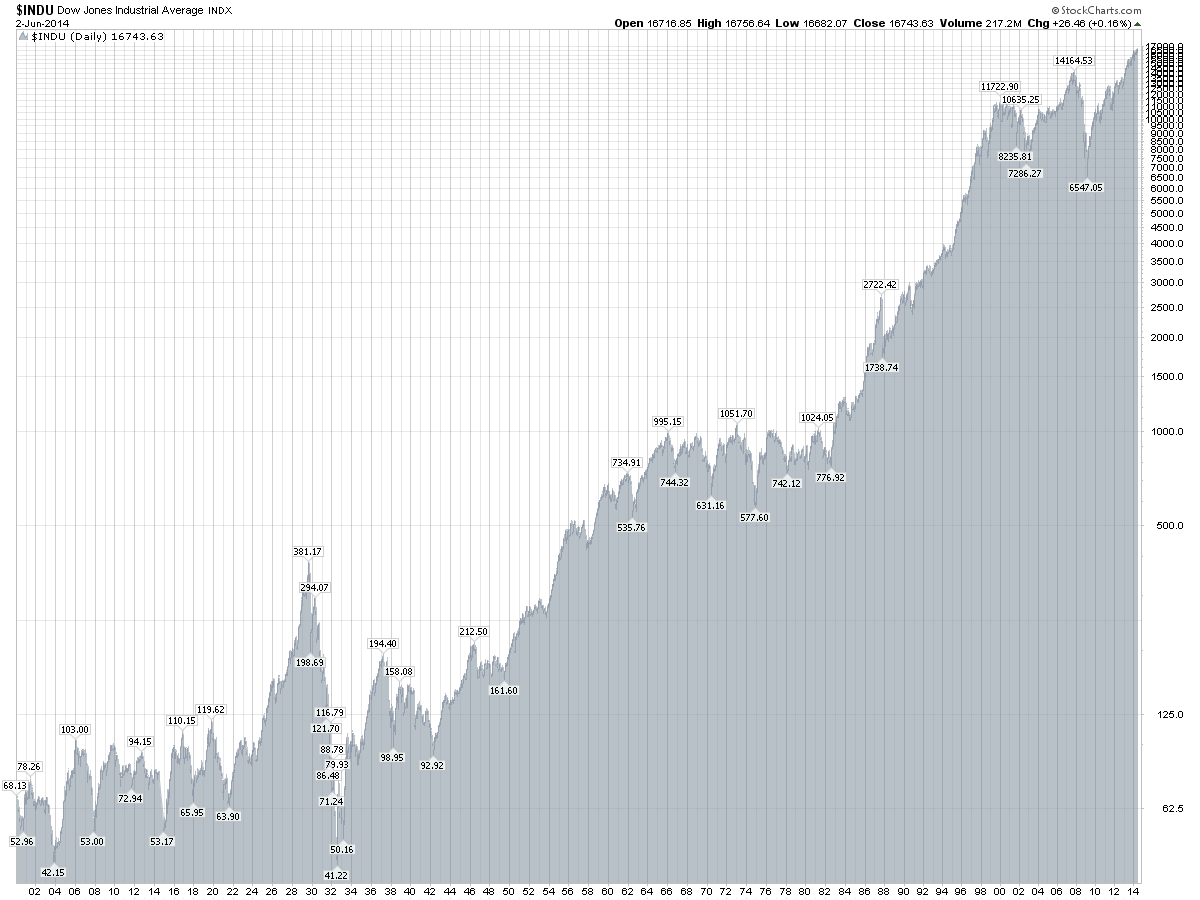

The Money Game by Adam Smith:

We are at a wonderful ball where the champagne sparkles in every glass, and soft laughter falls upon the summer air, we know at some moment the black horsemen will come shattering through the terrace doors, wreaking vengeance and scattering the survivors. Those who leave early are saved, but the ball is so splendid no one wants to leave while there is still time, so everyone keeps asking, ‘What time is it?’ But none of the clocks have hands.

This link provides an excellent video of deep value or contrarian investing; See it!

http://greenbackd.com/2014/12/29/deep-value-at-authorsgoogle/

I am still waiting on a reader to send a copy of Deep Value. Then we can go into a close analysis of the book.

More:

2014-Year-in-Review-Collum from a long-term investor.

Line between rational speculation and market collapse

HAVE A HAPPY AND PROSPEROUS NEW YEAR!

Posted in Special Situations, Uncategorized

Tagged Contrarian Investing, David Collum, Deep Value, The year in review, Toby Carlisle

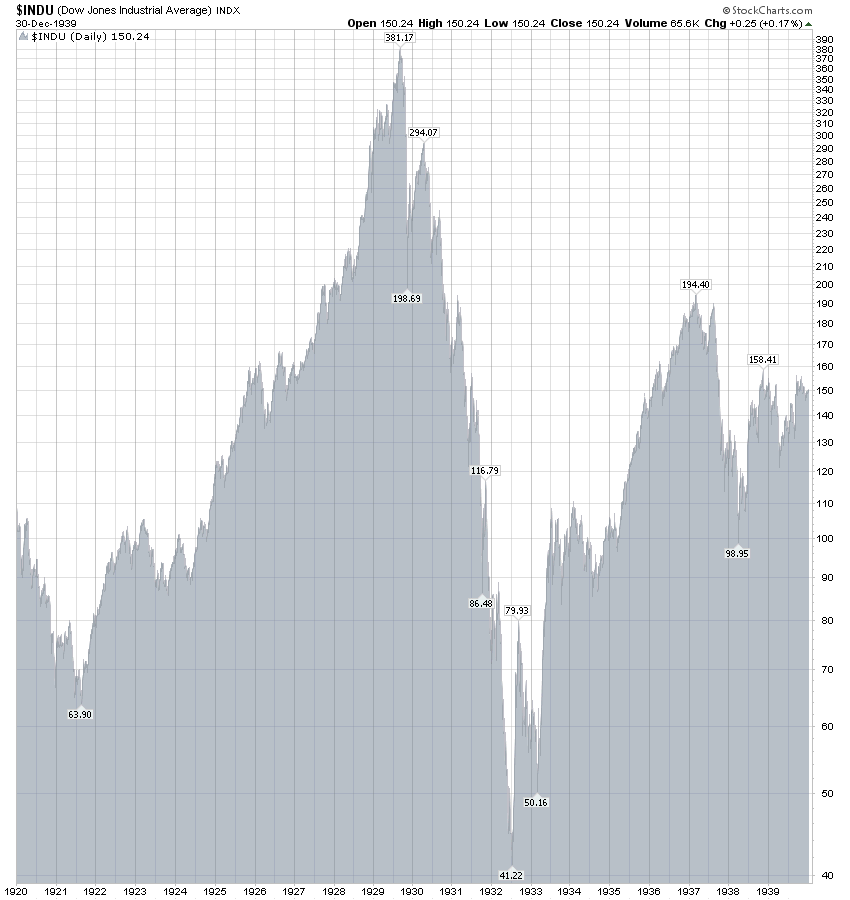

Chapter 19: America on the Bargain Counter (The Forgotten Depression, 2014) (pages: 197 to 200)

On August 24, 1921, the low point of the Dow, many stock prices translated into multiples on 1923 earnings of less than five times. That held true of the steel companies but also of the kind of consumer-products companies that had enjoyed a relatively prosperous depression. Thus, Coca-Cola, at $19 a share—500,000 shares were outstanding, providing a stock market capitalization of all of $9.5 million—was valued at what would prove 1.7 times 1922 earnings and 2.5 times 1923 earnings; the shares provided a dividend yield of 5.26%. Gillette Safety Razor Company, which was selling as many razors and blades in 1921 as it had in 1920, was quoted at a little more than five times forward earnings and yielded 9.23 percent. Radio Corporation of America, not yet revealed as one of the great growth stocks of the 1920s, could be purchased in the market for about as much as the company earned in 1923: $1.50 a share.

As a matter of course on Wall Street, bargains hold no appeal at the bottom of the market. In August 1921, stock prices had been sliding for almost two years. At such junctures, the memory of losing money is usually more vivid than the imagined prospect of making it.

It didn’t take much imagination to recognize the value of F.W. Woolworth Company, the five-and-dime chain merchandiser that was finishing its tenth year as a fused corporate unit. Frank W. Woolworth himself, founder and builder of the gothic corporate headquarters tower at 233 Broadway in lower Manhattan, had died in 1919, but his successors had distinguished themselves in the depression. They had stopped buying any but essential merchandise after the break in whole sale price in June 1920, while customers, happily, had kept right on buying. Now 1921 sales were on track to surpass the total for 1920. While other chain stores had raised prices, Woolworth hewed to the letter of its five-and dime appellation (15; cents was the top ticket west of the Mississippi). And how was this exemplar of deflation-era merchandising—about to close its year without bank debt and with no mis-priced inventory—valued in the stock market on August 24, 1921? At a price of $105 a share, or 3.7 times imminent 1922 earnings and 3.3 times what would turn out to be 1923 earnings. The stock yielded 7.62 percent.

Posted in Economics & Politics, History, Uncategorized

Tagged 1921, Forgotten Depression, James Grant, Market History

Obama Gives A Green Light on Cuba Sell the rally! Because the initial euphoria will set in after a few weeks or months.

A current investor in Cuba.

Plus, you gotta deal with this:

My experiences in Cuba: A glimpse of Cuba

Posted in Uncategorized

One of my favorite quotes, I think from

@MarkYusko “Investing is the only place where when things go on sale, people run out of the store”

Russias-stock-market-is-very-cheap-but/

Of course, being contrarian requires MUCH PATIENCE. See link (**) above that featured the gold market in my post of Jan. 2014.

OTHER

An intelligent move: sandstorm-gold-announces a buy-back of shares after a 80% decline in share price. The opposite of tech stock managements who are currently buying back shares at their all-time highs after a six-year move up in their stock prices)

Ghost Airports or EU Mal-investment Gone Berserk

A smart way to view gold ownership by an expert This bullion dealer understands that gold is money and NOT an investment.

Financial-crises-during-the-gold-standard-era/ (great blog: www.tsi-blog.com)

The Horror of Herbalife

You can watch Pershing Square’sa 7:45 video at: http://www.factsaboutherbalife.com/herbalife-unmasked/ and the entire 3-hour video is posted at: http://www.factsaboutherbalife.com/herbalife-unmasked/

Posted in Uncategorized

Tagged 16 Rules, Contrarian, John Templeton, RSX, Russian Stocks

An excellent Wealth Track interview of Joel Greenblatt on his portfolio management process (25 minutes): http://zortrades.com/how-to-manage-money-like-joel-greenblatt/

At the ten minute mark Joel makes an amazing statement: 97% of the top quartile money managers from the decade of 2000-2010 (encompassing two big sell-offs) were in the bottom half of performance three years out of ten; 79% were in the bottom quartile and a whopping 47% were in the bottom decile (in tenth place!) in three of the ten years. Talk about fortitude and sticking to your strategy!

Joel Greenblatt’s Magic Formula for those unfamiliar with his approach.

Joel Greenblatt is the founder and a managing partner of Gotham Capital, a hedge fund (also called a private investment partnership). He is also an adjunct professor at the Columbia University Graduate School of Business, and holds a B.S. and an MBA from the Wharton School. According to Greenblatt’s “The Little Book that Beats the Market” (Wiley, 2005) learning to successfully invest in the stock market is simple. Greenblatt said that he wanted to write a book his children could read and learn from. The main point Greenblatt makes is that investors should buy good companies at bargain prices-businesses with high return on investment that are trading for less than they are worth. This is a classic value investing methodology that Benjamin Graham would have espoused.

Finding Undervalued Stocks

To those familiar with Benjamin Graham, Greenblatt’s approach is obvious: buy stocks at a lower price than their actual value. This assumes you are able to somewhat accurately estimate a company’s actual value based on future earnings potential. Greenblatt alleged that stock prices of a company can experience wild swings even as the value of the company does not change, or changes very little. He views these price fluctuations as opportunities to buy low and sell high.He follows Graham’s “margin of safety” philosophy to allow some room for estimation errors. Graham said that if you think a company is worth $70 and it is selling for $40, buy it. If you are wrong and the fair value is closer to $60 or even $50, you will still be purchasing the stock at a discount.

Finding Well Run Companies

Greenblatt believes that a company with the ability to invest in its business and receive a good return on that investment is usually a “well run” company. He uses the example of a company that can spend $400,000 on a new store and earn $200,000 in the next year. The return on investment will be 50%. He compares this to another company that also spends $400,000 on a new store, but makes only $10,000 in the next year. Its return on the investment is only 2.5%. He would expect you to pick the company with the higher expected return on investment.Companies that can earn a high return on capital (the return a company makes after investing in the business) over time generally have a special advantage that keeps competition from destroying it. This could be name recognition, a new product that is hard to duplicate or even a unique business model.

Magic Formula

EBIT to Enterprise Value

Greenblatt compares a company’s ratio of EBIT (earnings before interest and taxes) to enterprise value against the risk-free rate. Enterprise value is a measure of company value that takes into consideration the company’s capital structure (debt versus equity). You could do a simple earnings yield calculation by dividing net earnings by the market value of the company’s stock, but Greenblatt has a different take. He divides earnings before interest and taxes by a stock’s enterprise value. A company’s enterprise value represents its economic value, which is the minimum value that would be paid to purchase the company outright. In keeping with value investment strategies, this is similar to book value.Enterprise value is equal to the market value of equity (including preferred stock) plus interest-bearing debt minus excess cash. Greenblatt uses enterprise value instead of just the market value of equity because it takes into account both the market price of equity and the debt used to generate earnings.Companies with debt must pay interest on the debt and eventually pay off the debt. This makes the debt’s true acquisition cost higher. Adding debt to market capitalization lowers the EBIT to enterprise value, making a company less attractive. Excess cash is subtracted from enterprise value because the un-needed cash reduces the overall cost of acquiring a business. If a company is holding $25 million in cash, the effective acquisition cost is reduced by that amount. Excess cash raises EBIT to enterprise value, making the company more attractively priced.EBIT to enterprise value helps to measure the earnings potential of a stock versus its value. If the EBIT-to-enterprise value is greater than the risk-free rate (typically the 10-year U.S. government bond rate is used as a benchmark), Greenblatt believes you may have a good investment opportunity-and the higher the ratio, the better.

Return on Invested CapitalReturn on capital, or return on invested capital (ROIC) is similar to return on equity (the ratio of earnings to outstanding shares) and return on assets (the ratio of earnings to a company’s assets), but Greenblatt makes a few changes. He calculates return on capital by dividing earnings before interest and taxes (EBIT) by tangible capital. Instead of using net income, return on invested capital emphasizes EBIT, also known as pretax operating earnings. Greenblatt uses this number because the focus is on profitability from operations as it relates to the cost of the assets used to produce those profits.Another difference is Greenblatt’s use of tangible capital in place of equity or assets. Debt levels and tax rates vary from company to company, which can cause distortions to both earnings and cash flows. Greenblatt believes tangible capital better captures the actual operating capital used.The equity value Greenblatt uses to calculate return on equity ignores assets financed via debt, and the total assets value used in the return on assets calculation includes intangible assets that may not be tied to the company’s primary operation. According to Greenblatt, the higher the return on capital, the better the investment.

Greenblatt’s Implementation of the Magic Formula

Greenblatt started his Magic Formula screen with a universe of the 3,500 largest exchange-traded stocks, based on market capitalization (shares outstanding multiplied by share price). He then ranked the stocks from one to 3,500 based on return on capital (the highest return on capital got a ranking of one; the lowest received a rating of 3,500). Next, he ranked the stocks based on their ratio of EBIT to enterprise value, with the highest ratio assigned a rank of one and the lowest assigned a rank of 3,500. Finally, he combined the rankings (if a company ranked 20 for return on capital and 10 for EBIT to enterprise value, the combined ranking was 30).For practical purposes, Greenblatt recommends investing in 20 to 30 stocks by purchasing five to seven every few months. The holding period he advises for each stock is one year. He believes this strategy will allow you to make changes on only a few stocks at a time as opposed to liquidating and repurchasing the entire portfolio at once.

Performance

Greenblatt tested his investing strategy over a 17-year period and earned an average annual return of 30.8%. He held 30 stocks at a time and held each stock for one year.In the book, Greenblatt devotes an entire chapter to explaining that the strategy is not a “magic bullet” that always works. During his test period, he found that, on average, five of every 12 months underperformed the market. Looking at full-year periods, once every four years the approach failed to beat the market.Sticking to a strategy that is not working in the short run even if it has a good long-term record can be difficult, Greenblatt says, but he believes you will be better off doing just that. Greenspan supposed that following the latest fad or short-term investment ideas will not yield market-beating results.

Narrowing the Stock Universe

The first step is to remove all over-the-counter stocks (OTC) and ADRs (shares of foreign companies trading on U.S. exchanges). Greenblatt’s initial database of stocks included only exchange-traded stocks. Next, all stocks in the financial and utility sectors are excluded due to their unique financial structures.

Market Capitalization

While Greenblatt’s original study included stocks with market capitalizations of $50 million or greater, he subsequently modified the minimum value for market capitalization between $50 million and $5 billion, depending upon on liquidity needs and risk aversion.

Return on Invested Capital

Return on capital measures the return a company achieves after investing in the business; the higher the return on capital, the better the investment.Tangible capital is defined as accounts receivable plus inventory plus cash minus accounts payable. This figure is based on the fact that a company needs to fund its receivables and inventory but does not have a cash outlay for accounts payable. For our screen, we require a return on invested capital greater than 25%, as specified in Greenblatt’s alternative screening suggestions.

EBIT to Enterprise Value

The ratio of EBIT to enterprise value helps to measure the earnings potential of a stock versus its value. To calculate, Greenblatt divides EBIT by enterprise value. For this screen, we use the EBIT-to-enterprise-value ratio to narrow the field to 30 stocks by choosing those with the highest ratio.

Conclusion

Like any stock screening strategy, blindly buying and selling stocks is never a good idea. Developing and implementing disciplined buy, sell and hold strategies is a better option. Greenblatt’s Magic Formula is not revolutionary, but does provide a new twist on the old value investing ideas. While his past record is impressive, it will be interesting to see how the screen holds up during this period of market turmoil and its aftermath.

Joel Greenblatt’s Magic Formula Criteria

If those who believe in the value of gold r “gold bugs”, believers in value of financial assets must be “paper bugs” – “bond bugs”, “stock bugs”..

Simon Mikhailovich @S_Mikhailovich · Nov 14

Money is a medium of exchange. That means money is the thing that people ask for in return when they supply goods and services to the market. You often see money being defined as something having three properties: medium of exchange, store of value and unit of account. But my view – and this is in agreement with Austrian school economists Menger and von Mises – is that store of value and unit of account are not the definitional properties, they are derivative properties that money has because of its function as a medium of exchange. There can be other goods in the economy that function as a store value but not as a medium of exchange, like property for example. And I would include gold in that category. It is a store of value, maybe superior to the performance of money proper in that respect.–Robert Blumen

The goal of this post is to understand how prices are set for goods that are not consumed like gold or stock certificates. This is a follow-up to a prior post on Goldbugs http://wp.me/p2OaYY-2Av.

Many analysts covering the gold market lack a basic understanding of reservation demand. Most gold market research is based on the premise that the supply side of the market can be characterized by the quantity supplied and demand side by the quantity demanded. The specific cause and effect relationship between these two variables and price is often unstated; and perhaps rightfully so: is it not obvious that a greater quantity demanded is the cause of a higher price, and that a greater quantity supplied is responsible for a lower price?

NO!

Market forecasts based on quantities of gold are meaningless. “Gold demand was up by 15% in 2012.” are true but only if they are understood in a misleading sense. The supply and demand sides of the market consist of supply and demand schedules, not quantities. A price forecast based on quantities is a non sequitur because there is no causal connection from the quantities to the price. This error has side-tracked the majority of analysts into an obsessive focus on quantities while ignoring the actual drivers of the price.

Read: Misunderstanding-Gold-Demand (1) and for more examples: What determines the price of gold Then to reinforce the concepts, Rothbard shows in detail how supply and demand schedules are derived from individual preference rankings in Man, Economy , and State starting with his discussion in Chapter 2, sections 4-5 and Chapter 2, Section 8: Stock and Total Demand to Hold, and then later as applied to money in Chapter 11 (Money and its Purchasing Power) Sections 2-5. Link here: http://mises.org/library/man-economy-and-state-power-and-market

If you grasp the readings above, you will have a greater understanding than many professional gold analysts. I am willing to take bets on this. Takers?

Then you will not waste your time reading the nonsensical: Global-gold-demand-will-overwhelm-the-manipulators Nathan Mcdonald-sprott-money-news

However, even if you agree/disagree with an analyst’s conclusion, you will know whether the premises are logical if not yet determined to be correct.

Revisiting the Goldman Sachs $1050oz gold forecast/

You might even be able to understand where a forecaster went wrong in their analysis: Eric Sprott sees gold at new high before year-end/

Debt grew and central banks printed so why did the price decline in gold from 2011 to today (Nov. 25, 2014)?

Gold wasn’t always in the dumps. It rose right along with equities, indeed outperformed equities, from the 2009 Great Recession bottom – when central banks the world over first began implementing their unconventional monetary policies – straight through to its September 2011 top. The reason we think it did is quite simple. Coming out of the Great Recession, central bank credibility – their ability to “pull us out” of the Recession – was being severely questioned by investors. Thus, a good portion of investor money found its way into gold. That changed in 2011. Underwritten by these same central bank easy money policies, the as yet unresolved malinvestments of the Housing Bubble turn Credit Bust turn Great Recession, which were in the process of a healthy liquidation, were short circuited, while new, yet to be revealed malinvestments (we think the largest being anything in and around financial engineering) were starting to bear fruit. The belief took hold that the heroic policies of these central banks were finally working, finally restoring long-term vitality to the economy. Gold then sunk while equities marched ever higher.

So here we are… http://www.forbes.com/sites/michaelpollaro/2014/10/12/central-bank-credibility-the-equity-markets-and-gold/

Spend the time to understand how prices are set/determined and you will avoid faulty analysis and think better for yourself.

HAVE A HAPPY THANKSGIVING!

Posted in Uncategorized