Brian Lund-originally published Feb 5, 2015 Lesson: Think for yourself.

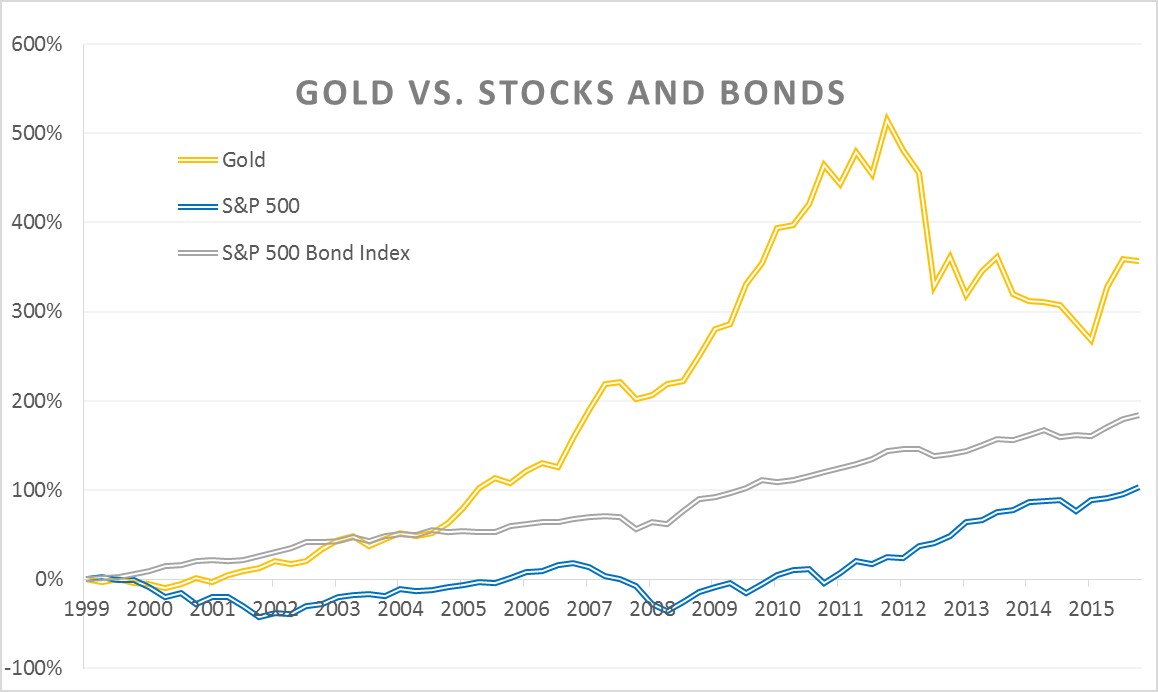

Nobody wants to be the bearer of bad news. Nobody wants to crush people’s dreams. But in the world of investing, cold, hard facts, not dreams, are what make you money. And the fact of the matter is, historically speaking, buying gold is the worst possible investment you can make.

I am very sensitive to the fact that what I just said has probably caused some readers to go apoplectic, and for that I apologize. I know that I will never convince the gold bugs, inflation hawks or doomsday preppers of this thesis, nor my own personal position that gold will eventually be worthless. But for the rest of you, let me lay out the case to avoid gold as an investment.

The Numbers Don’t Lie

In his seminal book “Stocks for the Long Run,” renowned economics professor Jeremy Siegel looked at the long-term performance of various asset classes in terms of purchasing power — their monetary wealth adjusted for the effect of inflation.

With a $1 investment each in stocks, bonds, T-bills and gold, beginning in 1802 and ending in 2006, Siegel calculated what those assets would then be worth.

Stocks were the big winners, growing the initial dollar investment into $755,163. Bonds and T-bills trailed dramatically, returning only $1,083 and $301 respectively. But the big surprise was in how badly gold fared during that time, only growing to $1.95.

An Inefficient Investment Vehicle

In addition to its miserable historical performance, gold also has many other failings as an investment, not least of which are the cumbersome and inefficient options available to own it and the prevalence of less than reputable salespeople in the precious metals space.

Owning physical gold in the form of bullion has many drawbacks. Wide bid and ask prices on physical gold ensure that the moment you purchase it you are already underwater on your investment. In addition, shipping costs for the heavy metal will further add to your cost basis.

Once you get your gold, you then have to decide how to store it. Keeping it at home exposes it to the risk of theft, fire or natural disaster. Taking it to the bank requires the rental of a safe deposit box, the cost of which will eat into your profit as well.

Firms will store your physical gold on site, but they charge for the service, and the idea of having your yellow treasure held by someone somewhere else, commingled with that of others, is not very appealing.

Enter the Modern World

Ultimately, gold is a legacy investment vehicle from a time before mass communications, ease of global travel, and the internet. It no longer is the default store of value that it once was, and financial and technological advances have made it an investment best suited for collectors and hobbyists, but certainly not for serious investors.

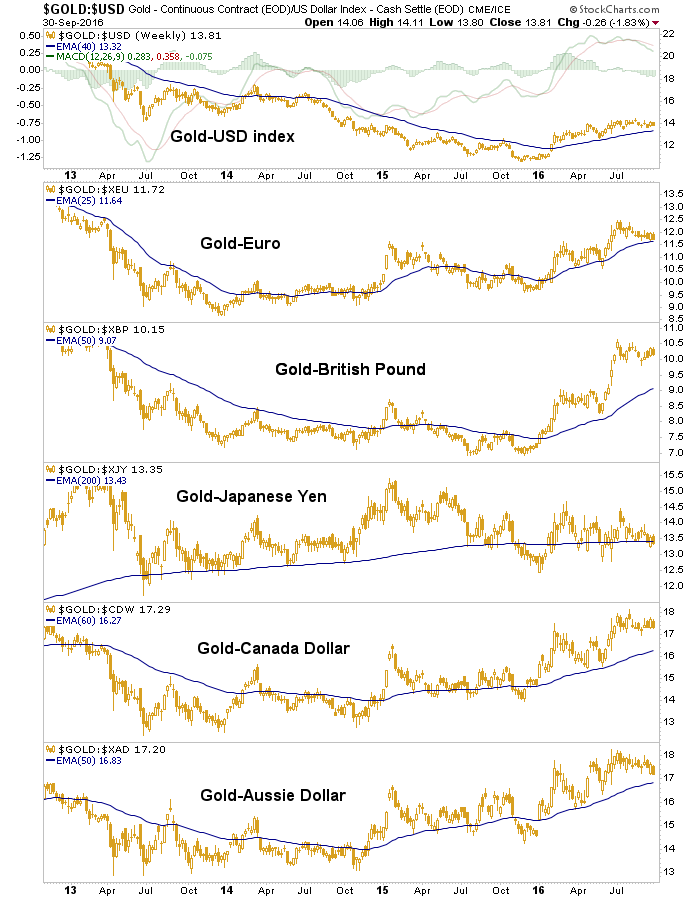

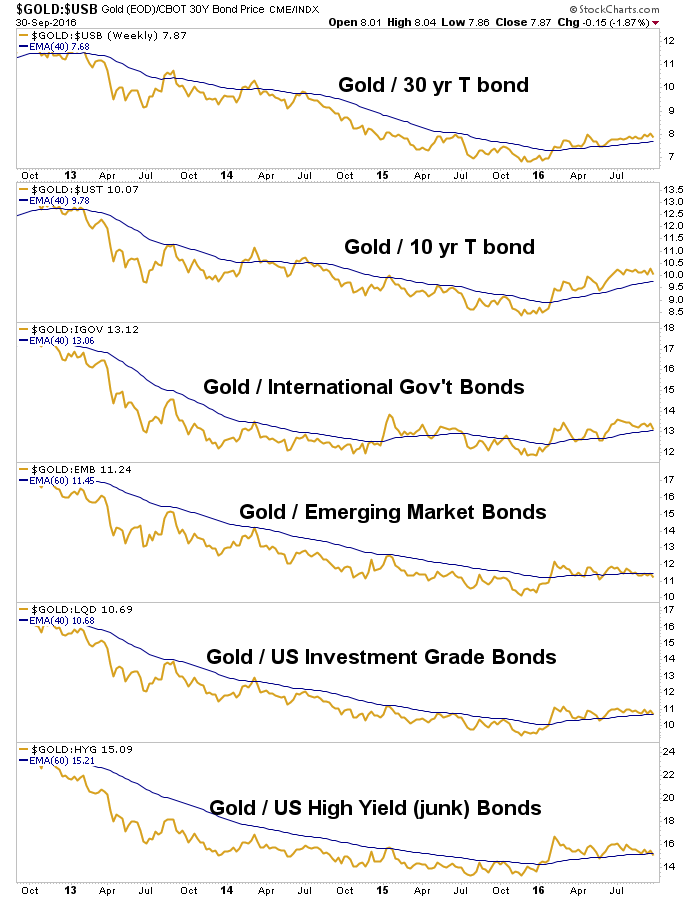

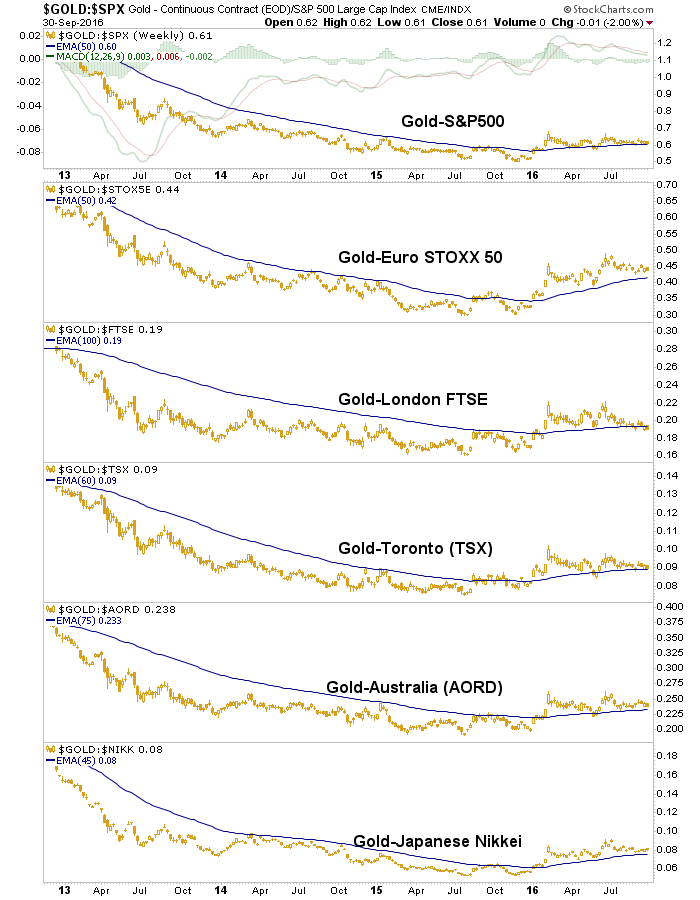

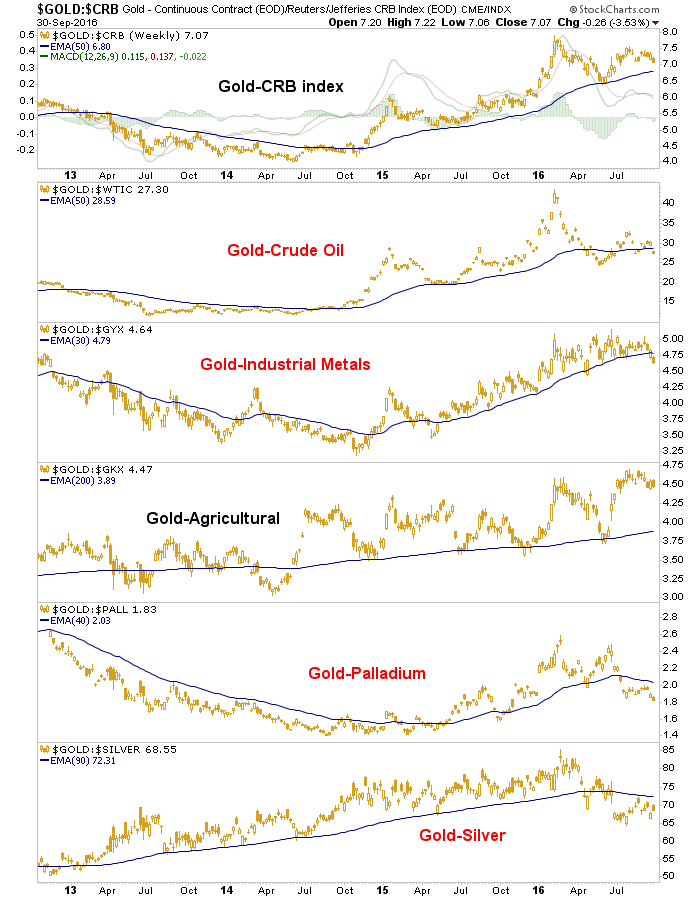

Because I hold gold related investments, I always seek out the opposing views to test my thesis. On the recent 5% fall in gold, a chorus of bears came out.

Natixis offers three main arguments for this call, only one of which makes sense, at least “technically”, if you will:

“For 2017 and 2018, we think that the biggest factor influencing the price of gold is the expected path of U.S. interest rate hikes,” the analysts said. “Also, we do not expect further rate cuts by the [European Central Bank] or [Bank of Japan] as this is likely to damage their banking system especially in the case of Europe.”

Natixis economists are expecting to see the Federal Reserve raise interest rates by 25 basis points three times next year: June, September and December.

Not only will higher bond yields raise gold’s opportunity costs but they will also boost the U.S. dollar, providing another headwind for the precious metals, the analysts explained.”

So when you read the above, always ask for theoretical and empirical evidence of the authors claims. Is there any long-term correlation between US interest rates and the dollar price of gold? And why? More here: Ganging up on gold

……The most successful professional investors like Warren Buffett, Paul Tudor Jones, John Templeton, George Soros and Jim Rogers, know this well. Their methodologies are even built upon the idea that an intelligent investor can get ahead by taking advantage of those times the crowd becomes irrational, the antithesis of the EMH and MPT.

Objective judgement, now at this very moment,

Unselfish action, now at this very moment,

Willing acceptance, now at this very moment, of all external events.

That is all you need.

To me that captures the three disciplines (perception, action, will) very nicely. It tells you how to see the world, how to act in the world, and how to come to terms with the world. It is indeed all one needs. You could spend a lifetime trying to just live that quote.

Understanding Stoic Philosophy may help you as an investor maintain rationality, control unwanted emotional reactions, and develop clear thinking for better choices which is, after all, what investing is all about.

The essense of philosophy is that we should live so that our happiness depends on as little as possible on external causes. –Epictetus

It is the emotional nonprofessional investor who sends the price of a stock up or down in sharp, sporadic and more or less short-lived spurts. The professional investor has no choice but to sit by quietly while the mob has its day, until the enthusiasm or the panic of the speculators and nonprofessionals have been spent.” –J. Paul Getty

Can You Explain This?

Starting on page 4, this money manager explains his firms consistent underperformance. Do you agree or disagree? Why? A lesson for investors.

There’s no such thing as “passive investing.” As Ben Graham defined it in his magnum opus, Security Analysis, “An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.” Because passive strategies entail zero analysis of either of these qualifications they are, by definition, speculative. And those adopting them are speculators, not investors.

Like “jumbo shrimp,” “virtual reality,” “old news,” or “living dead,” the term “passive investing” is thus an oxymoron.

My point here is not to shame everyone who has embraced passive in recent years. There are plenty of good reasons to go passive, namely to dramatically lower your costs. My point is that if you want to call yourself an “investor” you need to do a little bit more thinking about the prices and fundamentals of risk assets than just buy at any price and hope. I think Jesse Livermore said it best in Reminiscences of a Stock Operator:

The average American is from Missouri everywhere and at all times except when he goes to the brokers’ offices and looks at the tape, whether it is stocks or commodities. The one game of all games that really requires study before making a play is the one he goes into without his usual highly intelligent preliminary and precautionary doubts. He will risk half his fortune in the stock market with less reflection than he devotes to the selection of a medium-priced automobile.

Embracing passive investing is exactly this sort of ‘cover your eyes and buy’ sort of attitude. Would you embrace the very same price-insensitive approach in buying a car? A house? Your groceries? Your clothes? Of course not. We are all very price-sensitive when it comes to these things. So why should investing be any different?

I don’t understand why business schools don’t teach the Warren Buffett model of investing. Or the Ben Graham model. Or the Peter Lynch model. Or the Martin Whitman model. (I could go on.)

In English, you study great writers; in physics and biology, you study great scientists; in philosophy and math, you study great thinkers; but in most business school investment classes, you study modern finance theory, which is grounded in one basic premise–that markets are efficient because investors are always rational. It’s just one point of view. A good English professor couldn’t get away with teaching Melville as the backbone of English literature. How is it that business schools get away with teaching modern finance theory as the backbone of investing? Especially given that it’s only a theory that, as far as I know, hasn’t made many investors particularly rich.

Meanwhile, Berkshire Hathaway, under the stewardship of Buffett and vice chairman Charlie Munger, has made thousands of people rich over the past 30-odd years. And it has done so with integrity and a system of principles that is every bit as rigorous, if not more so, as anything modern finance theory can dish up.

On Monday, 11,000 Berkshire shareholders showed up at Aksarben Stadium in Omaha to hear Buffett and Munger talk about this set of principles. Together these principles form a model for investing to which any well-informed business-school student should be exposed–if not for the sake of the principles themselves, then at least to generate the kind of healthy debate that’s common in other academic fields.

Whereas modern finance theory is built around the price behavior of stocks, the Buffett model is centered around buying businesses as if one were going to operate them. It’s like the process of buying a house. You wouldn’t buy a house on a tip from a friend or sight unseen from a description in a newspaper. And you surely wouldn’t consider the volatility of the house’s price in your consideration of risk. Indeed, regularly updated price quotes aren’t available in the real estate market, because property doesn’t trade the way common stocks do. Instead, you’d study the fundamentals–the neighborhood, comparable home sales, the condition of the house, and how much you think you could rent it for–to get an idea of its intrinsic value.

The same basic idea applies to buying a business that you’d operate yourself or to being a passive investor in the common stock of a company. Who cares about the price history of the stock? What bearing does it have on how the company conducts business? What’s important is whether you can purchase at a reasonable price a business that generates good returns on capital (Buffett likes returns on equity in the neighborhood of 15% or better) without a lot of debt (which makes returns on capital less dependable). In the best of all worlds, the company will have a competitive advantage that allows it to sustain its above-average ROE for years, so you can hang on to it for a long time–just as you would live in your house–and reap the power of compounding.

Buffett further advocates investing in businesses that are easy to understand–Munger calls it “clearing one-foot hurdles”–so you can come up with more reliable estimates of their long-term economics. Coca-Cola‘s basic business is pretty staid, for example. Unit case sales and ROE determine the company’s future earnings. Companies like Microsoftand Intel–good as they are–require clearing much higher hurdles of understanding because their business models are so dependent on the rapidly evolving world of high tech. Today it’s a matter of selling the most word-processing programs; tomorrow it’s the Internet presence; after that, who knows. For Coke, the challenge is always to sell more cases of beverage.

Buying a business or a stock just because it’s cheap is a surefire way to lose money, according to the Buffett model. You get what you pay for. But if you’re evaluating investments as businesses to begin with, you probably wouldn’t make this mistake, because you’d recognize that a good business is worth buying at a fair price.

Finally, if you follow the Buffett model, you don’t trade your investments just because our liquid stock markets invite you to do so. Activity for the sake of activity begets high transaction costs, high tax bills, and poor investment decisions (“if I make a mistake I can sell it in a minute”). Less is more.

I’m not trying to pick a fight with modern finance theory enthusiasts. I just find it unsettling that basic business-school curricula don’t even consider models other than modern finance theory, even though those models are in the marketplace proving themselves every day.

the-base-rate-view-by-mauboussin I wonder if readers will find this useful. We last discussed base rates here: http://csinvesting.org/2016/09/29/hedge-fundfamily-office-consulting-job/

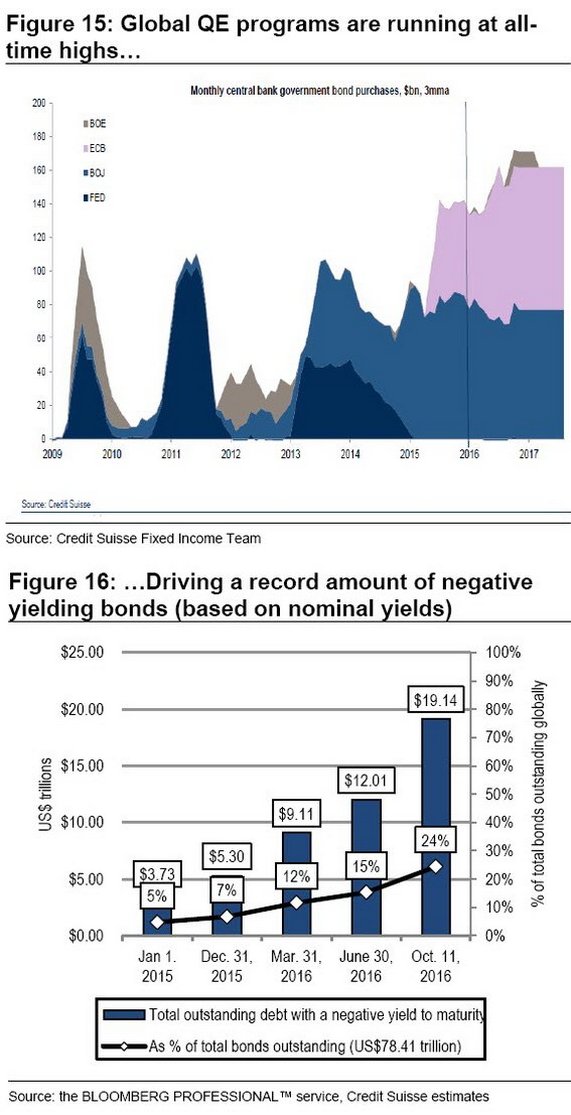

I post these charts for a historical reference point. I do not use them to predict where prices will go. Note though that rising CinC (currency in circulation) doesn’t always correlate to rising asset prices.

https://www.thestockmarketblueprint.com/asset-based-analysis-does-it-work/ A great blog for NCAV stocks and more!

Extra

Hi John:

A while back you took my Investment IQ Test questionnaire. As you may recall, it was based on the character traits of the world’s most successful investors I outlined in my book, The Winning Investment Habits of Warren Buffett & George Soros.

Here, very briefly, are a few of the “highpoints” of the investment behaviors that made them so successful.

I trust you enjoy it and I appreciate your comments.

Best regards,

PS: If you prefer to read it in your browser just go here.

7 Investment “Tips” From the World’s Richest Investors

Warren Buffett, Carl Icahn, and George Soros are the world’s richest investors. Their investment styles are as opposite as night and day. Buffett buys companies that he considers to be good bargains; Soros is famous for his speculative forays into the currency markets, which is how he came to be known as “The Man Who Broke the Bank of England.”

But—as I have shown in The Winning Investment Habits of Warren Buffett & George Soros—they both practice the same 23 mental habits and strategies religiously. As do Sir John Templeton, Bernard Baruch, Peter Lynch, and all the other successful investors I’ve ever studied or worked. It doesn’t matter whether you buy stocks, short currencies, trade commodities, invest in real estate, or collect ancient manuscripts: adding these mental strategies to your investment armory will do wonders for your bank account.

To make it easy to get going, I’ve distilled these 23 mental habits into these seven simple (though not always easy to follow) rules:

1. If you’re not certain about what you’re intending to do, don’t do it

Great investors are always certain about what they are doing whenever they put money on the table. If they think something is interesting but they’re not sure about it, they do more research.

So next time, before you call your broker (or go online), ask yourself: “on a scale of 1 to 10, how certain am I that I will make money?” Choose your own cut off point, but if it’s less than a 7 or an 8, you definitely need to spend more mental energy before making a commitment.

Remember: the great investor’s sense of certainty comes from his own experience and research. If your sense of “certainty”doesn’t come from your own research, it’s probably a chimera.

2. Never take big risks

Warren Buffett, George Soros, Peter Lynch . . . they only invest when they are confident the risk of loss is very slight.

Okay, what about that person you heard about who made a bundle of money in copper or coffee futures or whatever by taking on enormous leverage and risk? A few simple questions:

Did he make any other big profits like that?

Did he do this last year as well, and the year before that, and the year before that?

If not, chances are that’s the only big profit he ever made.

(And what did he do with the money? If he spent his profits before he got his tax bill . . . )

The great investors make money year in year out. And they do it by avoiding risk like the plague.

3. Only ever buy bargains

This is another trait the great investors have in common: they’re like a supermarket shopper loading up on sale items at 50% off.

Of course, the stock exchange doesn’t advertise when a company’s on sale. What’s more, if everybody thinks something is a bargain, the chances are it’s not.

That’s how Benjamin Graham, author of the classic The Intelligent Investor, averaged 17% a year over several decades of investing. He scoured the stock market for what he considered to be bargains—companies selling under their break-up value—and bought nothing else.

Likewise, Warren Buffett. But his definition of a bargain is very different from Graham’s: he will only buy companies he can get at a discount to what he calls “intrinsic value”: the discounted present value of the company’s future earnings. They’re harder to identify than Graham-style bargains. But Buffett did better than Graham: 23.4% a year.

Even George Soros, when he shorted sterling in 1992, was convinced that the pound was so overvalued that there was only one way it could go: down. That’s a bargain of a different kind, but a bargain nonetheless.

4. Do your own leg work

How do they find investment bargains? Not in the daily paper: you might find some good investment ideas there, but you won’t find any true bargains.

The simple answer is: on their own. After all, almost by definition, an investment is only a bargain if hardly anybody knows about it. As soon as the big players discover it, the price goes up.

So it takes time and energy to find an investment bargain. As a result, all the great investors specialize. They have different styles, they have different methods, and they look for different things. That’s what they spend most of their time doing: searching, not buying.

So the only way you’re going to find bargains in the market is the same way: by doing your own legwork.

5. “When there’s nothing to do, do nothing”

A mistake many investors make is to think that if they’re doing nothing, they’re not investing.

Nothing could be further from the truth. Every great investor specializes in a very few kinds of investments. As a result, there will always be stretches of time when he can’t find anything he wants to buy.

For example, a friend of mine specializes in real estate. His rule is to only buy something when he can net 1% per month. He’s a Londoner so—aside from collecting the rent!—he’s been sitting on his thumbs for quite a while.

Is he tempted to do something different? Absolutely not. He’s made money for decades, sticking to his knitting, and every time he tried something different, he lost money. So he stopped.

In any case, his real estate holdings are doing very well right now, thank you very much.

6. If you don’t know when you’re going to sell, don’t buy

This is another rule all great investors follow. It’s a major cause of their success.

Think about it. You buy something because you think you are going to make a profit. You spend a lot of time so you feel sure you will. Now you own it. It drops in price.

What are you going to do?

If you haven’t thought about this in advance, there is a good chance you will panic or procrastinate while the price collapses.

Or . . . what if it goes up—doubles or triples—what then? I’ll bet you’ve taken a profit many times only to see the stock continue to soar. How can you know, in advance, when it’s likely to be the right time to take a profit? Only by considering all the possibilities.

The great investors all have; and will never make an investment without first having a detailed exit strategy. Follow their lead, and your investment returns should soar.

7. Benchmark yourself

It’s tough to beat the market. Most fund managers don’t, on average, over time.

If you’re not doing better than an index fund, then you’re not getting paid for the time and energy you’ve spent studying the markets. Much better to put your money in such a fund and spend your time looking for that handful of investments you are so positive are such great bargains that you’re all but guaranteed to beat the market.

Alternatively, consider the advice from a great trader. When asked what the average trader should do, he replied: “The average trader should find a great trader to do his trading for him, and then go do something he really loves to do.”

Exactly the same advice applies to the average investor.

Find a great investor to do your investing for you, and focus your energy on something you really love to do.

An example of my short corporate careerQUIZ: You are called in to interview for a six-figure consulting job for a family office. The family wants to establish an investment policy and procedure for investing. You are asked whether you would recommend investing in IPOs or other hedge funds. You reply that before recommending any asset class you would first determine:__________________________? Also, as a “value” (redundant) investor you would seek to buy from _______________ sellers. In case you need a hint, Ben Graham would have given you the answer in The Intelligent Investor.

One of the family members plops two annotated charts: 1 shows a reverse head and shoulders pattern on pork bellies and chart 2 shows blood spatter on the right of the chart. Which one has more predictive value as to where the market is headed?

Please answer in a few words–two or three–but no more than a sentence. GOOD LUCK!

Warren Buffett, Carl Icahn, and George Soros are the world’s richest investors. Their investment styles are as opposite as night and day. Buffett buys companies that he considers to be good bargains; Soros is famous for his speculative forays into the currency markets, which is how he came to be known as “The Man Who Broke the Bank of England.”

Warren Buffett, Carl Icahn, and George Soros are the world’s richest investors. Their investment styles are as opposite as night and day. Buffett buys companies that he considers to be good bargains; Soros is famous for his speculative forays into the currency markets, which is how he came to be known as “The Man Who Broke the Bank of England.”