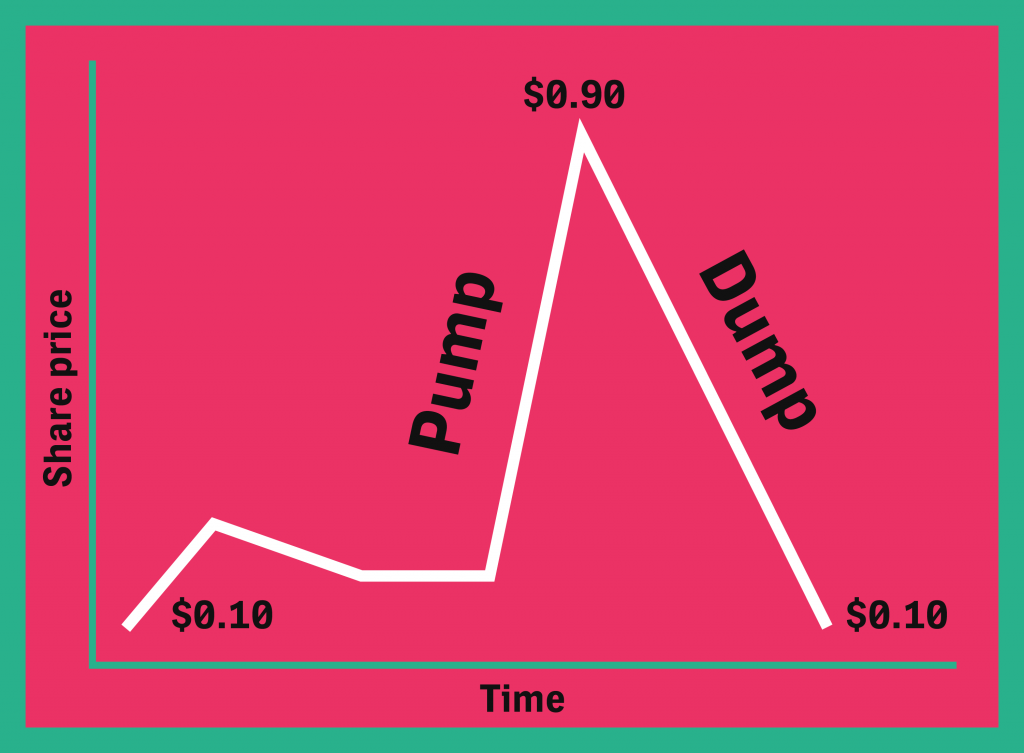

Read all four parts of this study of shady pump and dump schemes in the Pink Sheet World. (Must Read) https://theintercept.com/2016/09/22/the-money-is-gone/

Read all four parts of this study of shady pump and dump schemes in the Pink Sheet World. (Must Read) https://theintercept.com/2016/09/22/the-money-is-gone/

https://www.brandes.com/institute/knowledge-center

—

As always, I try to also post the criticisms of investing legends:

Victor Niederhoffer, tireless critic of Benjamin Graham, Graham’s investment idea, and Warren Buffett, is blown up once again —to the tune of some 75% losses for his funds —as reported for a story in this week’s The New Yorker. Whereas Niederhoffer’s latest catastrophic losses might serve as schadenfreude for some students of value investing, this self-described Ayn Rand Objectivist is a living testament to the lethal nature of some spectacularly subjective biases, including a disdain for anything resembling a margin of safety.

The New Yorker article is a bit heavy on Niederhoffer’s personal life, but is still worth a read. Here’s the link:

http://www.newyorker.com/reporting/2007/10/15/071015fa_fact_cassidy

Several years ago, Victor Niederhoffer was questioned during a radio interview about his rejection of the value investment paradigm as espoused by Benjamin Graham. The interviewer asked Niederhoffer how he might then explain the half-century success of Graham students such as Walter Schloss and others, given his rejection of Graham’s ideas. Niederhoffer replied that such success was “random.”

In Niederhoffer’s book, Practical Speculation, an entire chapter is devoted to refuting Graham’s pursuit of bargain issues. Only Niederhoffer hardly gets around to doing so. Instead, this sophisticated statistician attempts to stigmatize Graham and dwells on a small, essentially anecdotal sampling to prove his points about the lameness of value investing. One fellow Niederhoffer knew bought a stock below book value and watched as the stock proceeded to trade lower.

See? Graham’s ideas are useless.

When he is done expounding on the value investment discipline’s futility and ineffectualness, Niederhoffer allows as how he is troubled by the discipline’s ostensibly cynical premise: a dollar bought for fifty cents means that the seller is exploited. It seems odd that this cultivated observer of free-enterprise fails to recognize a couple of cold, hard facts: the business that fails to sell at half-price is likely to be sold for even less, and buyers of these ailing businesses are, in effect, upholding a competitive counterpoint to stronger businesses that might otherwise have a stranglehold in a capitalist system.

“Random”, the quality that Niederhoffer attributes to successful value investors and any successful value investments as defined by Benjamin Graham, might more aptly be attributed to Niederhoffer’s own quest for an intellectually sound speculative framework. This tendency is displayed in living color by Niederhoffer and other participants on dailyspeculations.com, the website Niederhoffer hosts, as these traders engage in frothy examinations of the parallels between non-related phenomena, such as the evolved habits of exotic animals seen while on safari, and “trading”. Niederhoffer himself is especially fond of drawing wisdom from Captain Jack Aubrey, the main hero in Patrick O’Brian’s 18th century British Navy epics, as that wisdom might pertain to the markets. But after reading Practical Speculation, it is painfully obvious that if Captain Aubrey ever sashays into Niederhoffer’s trading-room and hands him a copy of The Intelligent Investor, Niederhoffer will politely accept the book, and promptly throw it overboard when the good Captain is out of site.

It’s easy to take potshots at this outspoken speculator gone off his trolley. But in the spirit of inquiry that Niederhoffer offers in his book, MSN articles and website, it seems reasonable to ask whether two catastrophic losses and one near-catastrophic loss offered to investors over a 10 year investment period —nearly 4 years of which were spent on hiatus— are more or less “random” than the market-beating investment success that Schloss, et al, offered to investors for over 50 years using a value framework. In any case, the simple fact is that the alternatives to a value framework in the securities markets frequently lead to misery, and by all accounts, Victor Niederhoffer is currently altogether miserable. In the manner that Walter Schloss’ 50-plus years of risk-averse investment returns are “random”, it may be safely said that Victor Niederhoffer’s self-inflicted misery is also randomly rendered.

http://boards.fool.com/niederhoffer-and-the-quotrandomquot-success-25976330.aspx?sort=whole

and http://www.bearcave.com/bookrev/practical_speculation.html

Posted in Investing Gurus, Valuation Techniques

Tagged Ben Graham, Brandes Institute

I approach natural resource investing through the prism of history and cycles. and tend to look for where the supply/demand fundamentals are improving marketedly, yet where, as John Templeton put it, Maximum Pessimism is the prevailing sentiment. –Tom Kaplan (Novagold Annual Report 2014)

Precious-Metals-Summit-Conferences

and an excellent interview of Tom Kaplan: The Historian-an-interview-with-thomas-kaplan/ and ng_ar_2015

i-did-nothing-mark-mckinney-final (A cyclical investor)

Prominent metals investor Thomas Kaplan raised $200 million, more than expected, from investors eager to join him in making acquisitions in an industry starved for cash.

Kaplan’s Electrum Group LLC raised the money in Electrum Special Acquisition Corp, according to a prospectus filed with the U.S. Securities and Exchange Commission on Tuesday.

Electrum had expected to raise $150 million, it said in the prospectus. The “blank check company” expects to use the money to buy a company or assets with a focus on gold and other precious metals.

Details about the money raised were revealed on Thursday.

Kaplan, an Oxford-educated historian turned metals expert with a long track record of success, is betting that he and his team can spot an unloved company to buy and help it flourish again as demand in the sector improves.

“We are building up a war chest, given what we think is a unique buying opportunity in the metals and mining industry,” said Electrum Chief Executive Officer Eric Vincent. He would not describe what the target might be.

http://www.reuters.com/article/us-funds-kaplan-spac-idUSKBN0OR21O20150611p

Kaplan previously made big bets on NovaGold Resources Inc and Gabriel Resources, earning money as the price of gold climbed some years ago but suffering when it later dropped.

In 2007, Kaplan sold Leor Exploration & Production LLC, owner of natural-gas wells in Texas, for about $2.6 billion.

Last year Electrum started Electrum Strategic Opportunities, a private equity fund whose clients include the Municipal Employees’ Retirement System of Michigan.

(Additional reporting by Josephine Mason in New York; Editing by Lisa Von Ahn)

|

The Santangel’s Investor Forum invites eligible students to apply for a free ticket to attend the 2016 Forum, to be held in New York City on November 3, 2016.

The Leonard Family has endowed a table at the upcoming conference to enable a select number of talented students to attend the annual invitation-only event.

The contest was very beneficial for last year’s winners, including one who met his current employer through the event. We were excited recently to receive the following feedback about this 2015 Forum Winner:

“[He] started working here a couple months ago and he’s been terrific so far, and I just wanted to give you a big thanks for the connection. He has a bright future.”

All enrolled undergraduate and graduate students are eligible. Interested candidates should apply by emailing their resume and a current investment idea write-up to Steven Friedman (sfriedman@santangels.com). The idea can be for any type of security or asset class, but the write-up must be limited to 300 words. Preference will be given to unique and original ideas. Please submit ideas by October 15, 2016.

Please feel free to pass this along to anyone who may have an interest.

|

Amazon’s Business Is ‘Disappearing,’ Columbia’s Greenwald Says

December 1, 2011 — 11:25 AM EST

http://www.bloomberg.com/news/articles/2011-12-01/amazon-s-business-is-disappearing-columbia-s-greenwald-says

Amazon.com Inc. shares are overvalued because its core business of selling books and music online is “disappearing” and it’s competing with larger rival Apple Inc. in tablet devices, according to Columbia University’s Bruce C. Greenwald.

“Amazon trading at 100 times earnings is almost a joke,” Greenwald, a professor of management and asset management at the New York-based university, said today at the Bloomberg Hedge Fund Conference hosted by Bloomberg Link. “If Amazon doesn’t deliver profitability in the long run, it’s not going to stay at 100 times earnings.”

Amazon, based in Seattle, trades at 103 times reported earnings for the past year, down from this year’s peak of 129.8 in October, according to data compiled by Bloomberg. The company’s shares gained 2.5 percent to $197.16 in New York trading, and have climbed 9.4 percent this year.

==

January 4, 2013 | Comments (3)

Bruce Greenwald: Now, Amazon I think is completely different. I think, if Apple is a current profit machine, Amazon is trading on vapors. [laughs]

They make no reported profit; the whole story is a growth story. They’re buying customers on the theory, presumably, that those customers are going to be profitable in the future. Now, for customers to be profitable you have to dominate segments.

The segment that Amazon has traditionally dominated is, of course, books, music, and video. Well, we know what happened to the music business when it went digital, which is the profit vanished and even Apple doesn’t make any money on iTunes.

The same thing is happening to books, with the connivance, by the way, of Amazon. The same thing is happening to video, so their core business is dying. The business that they dominated, where they made all their money, is dying.

What have they decided to do? Go into a lot of businesses where they have no competitive advantage. First they’ve gone into every variety of retail: TV sets against Wal-Mart and Best Buy, who have better distribution economics…

They can buy the business, but in the long run, unless they can get bigger share than those companies, their pricing is going to be at a disadvantage to those companies, because those companies can distribute the TVs and other devices more cheaply.

Then what did they decide? They said, “Oh, that wasn’t a big enough challenge. Let’s go after the Oracles and the IBMs and all the companies that do cloud computing, and the SAPs and so on, and the Googles,” and they went into that business.

Now, if you think they’ve got a competitive advantage in that business while they’re going after everybody in retail, lots of luck. But then they decided that was not enough, so they decided to go after Apple and the others in the device business.

This looks, to me, like a company that makes no reported profit, which I think is fair, that’s trying to buy growth in all sorts of areas where, because it has no competitive advantage, the growth is going to be value-destroying, not value-creating.

http://www.fool.com/investing/general/2013/01/04/bruce-greenwald-amazon-is-trading-on-vapors.aspx

—

![]()

Amazon launched its first smartphone last week – the Amazon Fire phone.

It doesn’t represent any sort of leap forward in smartphone technology, according to reviews. So it probably won’t take a huge amount of market share from Apple or Samsung/Google.

Meanwhile, both Apple and Google are eating into one of Amazon’s traditional core businesses, selling music and video content.

So is Amazon’s new smartphone just a desperate bid to preserve market share? Or is it another ballsy, far-sighted move by Amazon’s boss, Jeff Bezos – one that will pay off in the end?

I think it’s the latter. And that’s why I’m willing to hang on to my Amazon shares – even although they trade on an eye-watering price/earnings ratio (P/E) of 500.

You might think I’m mad – but let me try to persuade you otherwise…

I’ve not seen one of Amazon’s phones, but it sounds like they’re pretty similar to your average iPhone, but with two fresh add-ons.

One is a semi-3D capability that has been greeted with a ‘meh’ reaction by most reviewers. In truth, I don’t really understand how this 3D function works – I’ll have to wait and see a phone before I can do that.

The other improvement is a ‘recognition engine’ which has been received much more warmly. It’s called Firefly and is a sort of audiovisual search tool. It recognises books, various consumer goods, music, video and more. And once the phone has recognised the item, you can immediately put it in your Amazon shopping basket.

“Not only was it effective”, says Gizmodo, “it was kind of beautiful”.

So it’s pretty obvious that Amazon is launching the phone in an effort to sell more stuff. Purchasers of the phone will also get a year’s free membership of Amazon Prime, which normally costs £79.

Prime offers free delivery on many purchases, the opportunity to ‘borrow’ books to read on your Kindle, and access to a wide selection of video titles. Amazon says that Prime customers spend four times as much on Amazon as other users, and that half of Amazon’s sales are to Prime customers.

So if the Fire phone can significantly boost the number of Prime customers, it will probably prove to be a savvy move by Bezos.

Now, not everyone is convinced that the phone launch is a smart move.

For example, Bruce Greenwald, a finance professor at Columbia Business School, made some negative comments to the Guardian. “This sequence of crazy initiatives in areas where they have no competitive advantage is about sustaining an unsustainable stock price… Amazon owns the books market, but what is happening to the value of that monopoly? They have a core business in which they are dominant, it’s going away and they are thrashing around trying to justify their $150bn market capitalisation.”

Is Greenwald right? I don’t think so.

Yes, Amazon faces growing competition. In digital content, it is competing with Apple, Google, music streaming service Spotify, and many others.

And on the physical consumer goods side – in other words, items that are delivered from its warehouses rather than online – the likes of Tesco, Argos and Walmart are all growing smarter about online retail. These chains also benefit from owning large store networks which are useful for customers who like to “click and collect.” Amazon isn’t so well placed for ‘click and collect.’

Greenwald is also right to highlight Amazon’s high valuation. However, I believe that valuation can be justified and that’s why I’m happy to hang onto my shares.

No other online retailer offers such a large variety of products for sale. And Amazon is still growing its sales faster than the growth rate for overall e-commerce around the world. Last year, Amazon was the ninth-largest retailer in the world. Consultancy Kantar expects it to be the second-largest by 2018.

Amazon’s network of warehouses is also a very useful asset. It has 106 ‘fulfilment centres’ around the world, of which ten are in the UK. It is also trying to improve its ‘click and collect’ capacity by offering collection points at some London Underground stations.

Amazon also has a great record of investing for the long term. When Amazon launched Amazon Web Services in 2005, many observers doubted that the company could become a major player in this field – providing services to businesses. But, according to The Motley Fool, it now controls more than 30% of infrastructure for the ‘cloud’.

The point is, there will come a time when Amazon can afford to slow down the pace of growth and allow its profits to rise dramatically. When that happens, today’s valuation won’t look so crazy.

I’ll freely admit that Amazon is probably the highest-risk stock in my portfolio, but I’m happy to hold for further growth to come. And the Fire phone will play its part in achieving that growth.

—

So what do YOU think? How would you value Amazon? What major adjustment would you need to make? What is the business trying to do?

If you need a hint: http://ben-evans.com/benedictevans/2014/9/4/why-amazon-has-no-profits-and-why-it-works

Does anyone want to bet $200 that Prof Greenwald will NEVER admit he might have miscalculated or misunderstood Amazon’s business?

What if he read their annual report: amazon-shareholderletter97

What caused the above?

Using Technical Analysis for a Fundamental View: https://nftrh.com/2016/09/03/gold-the-good-and-the-not-yet-good/

Using Technical Analysis for a Fundamental View: https://nftrh.com/2016/09/03/gold-the-good-and-the-not-yet-good/

The Trend is not your friend

There’s an old saying in the financial markets that the trend is your friend, meaning that you will do well as long as you position your trades in line with the current price trend. This sounds good. The only problem is that you can never know what the current trend is; you can only know what the trend was during some prior period. How is it possible for something you can never know to be your friend?

Market ‘technicians’ often make comments such as “the trend for Market X is up” and “Market Y is in a downward trend” as if they were stating facts. They are not stating facts, they are stating assumptions that have as much chance of being wrong as being right.

A statement such as “Market X’s trend is up” would more correctly be worded as “I’m going to assume that Market X’s trend is up unless proven otherwise”. The proving otherwise will generally involve the price moving above or below a certain level, but the selection of this level is yet another assumption and the price moving above/below any particular level will provide no factual information about the current trend.

More http://tsi-blog.com/2016/09/sorry-the-trend-is-not-your-friend/

Mea Culpa: sequoia-may-2016-transcript Not much to glean.

However, a question for you: Is it better to buy franchises or net/nets?

If you could choose between a fair coin that was gold or a rusty tin coin that each paid off 4 to 1 on choosing heads or tails, which one would you prefer?

In October those near Philly Microcap Conference http://microcapconf.com/conferences/philadelphia-2016/

HAVE A GOOD WEEKEND!

Pitching an investment idea is the life-blood of Wall Street analysts —whether at money management firms and investment banks or with CEOs to potential investors. Those who do it well win, and win big. Sonkin and Johnson teach professional analysts, sophisticated private investors and ambitious young analysts how to uncover the perfect investment and pitch it to critical decision makers, to advance their careers and increase their wealth.

No other book like this one exists. There are plenty of books that focus on investment strategy, company analysis and critical thinking. Yet, there is no book that combines investment analysis with persuasion and sales – in Wall Street vernacular—pitching. In our increasingly competitive world, being able to pitch your idea is becoming as critical as being able to find and analyze great investment opportunities. It is imperative to get clients or superiors to take action on your ideas. The teaching of this skill is sorely lacking on Wall Street. Pitching the Perfect Investment will present a two-step process: 1) finding the perfect investment; and 2) crafting the perfect pitch. The book will show that to be successful the reader will require two very different skill sets: the first is investment analysis and decision making; and, the second is persuasion and sales.

Pitching the Perfect Investment presents world-class insights into search strategy, data collection and research, securities analysis, risk assessment and management, combined with the use of critical thinking, to uncover the perfect opportunity for professional analysts, sophisticated private investors and ambitious young analysts as well as mergers and acquisition specialists advising clients, financial consultants and corporate financial analysis teams. Pitching draws from the disciplines of psychology, argumentation and informal logic. It instructs the investor analysts of all types how to craft this perfect investment into the perfect pitch. Pitching an investment is an essential skill to securing and then excelling at your job on Wall Street.

This is an essential skill for the ambitious young investment analyst looking to begin a career on Wall Street as well as the seasoned veteran discussing an idea on CNBC, and every investor in-between.

Aspiring analysts should be aware of this book, but I am not recommending since I have not read it. Common-sense writing helps. Clearly state your thesis then provide supporting facts and risks. Done. But if you can’t state your case to a child in less than a paragraph, then go back to your desk.

For example, Navigator Holdsings (NVGS) has a dominant position in handy-size petrochemical transportation and it trades at 55% of net asset value, its balance sheet and flexible fleet allows it to be profitable despite a perfect storm in the LPG shipping market. One of the most famous value investors, Wilbur Ross bought into NVGS at an average price of $8.73 over three years ago for a 50% stake. NVGS is now 20% below that price. The current lows in freight rates due to A, B, C are unsustainable due to 1, 2, 3, therefore normalized rates will mean much higher values. Timing is, of course, uncertain, but there are considerations for building more US ethylene plants for export. NVGS has the dominant position for transporting that product which requires special handling (super low temperatures and pressure). Price is about 50% below asset value and earnings power value.

Probably too long-winded, but you get the point.

—

Beware the echo chamber http://graphics.wsj.com/blue-feed-red-feed/ A serious concern for your research. Scary.

More on psychology for contrarians.

| Latest NewsJune 10, 2016 – We’re pleased to announce a new website launching in the coming week. Please let us know any questions or comments about the transition.

June 08, 2016 – Check out our latest 1-hour free webinar “Trading on Sentiment Strategies to Profit from Media Analytics in Global Equities.” Recent PressMay 14, 2016 – How To Time The Stock Market Using Media Sentiment — Ky Trang Ho Forbes |

||

| The World&39;s Greatest Stock Picker

Manny introduced himself to me as “the world’s greatest stock picker.” He explained that one key to his success was that he only needed two hours of sleep a night. He pored over details in every significant financial publication and in those quiet morning hours when all others slept, he let information percolate. By the morning he had brilliant new insights into the industries and companies that were poised to outperform over the following months. Some of the world’s top fund managers subscribed to his research, he told me. I asked if his clients knew he was housed in prison, in solitary confinement. He explained that of course they didn’t, and he asked that I kindly keep his secret. He distributed his stock research through his secretary, who kept his office open. In the intervening days I checked out Manny’s story. Much was true – he was in fact publishing highly-regarded financial research to large AUM clients from prison. On the surface his research analysis sounded brilliant – the creative ramblings of an out-of-the-box Wall Street-obsessed thinker. But as we talked in depth it became clear that his thought process was laced with irrational and circumstantial connections. He was often confusing wishful thinking with objective analysis. He was hypomanic, with grandiose claims and excessively optimistic projections. As a psychiatrist I’ve worked with many people with grandiose delusions. In each case the client has fixed beliefs that are contrary to reality – beliefs that guide much of their waking actions – beliefs that are entirely untrue. Delusions aren’t limited to manic prisoners, in fact we spend most of our days navigating the world based on assumptions, many of which are entirely unfounded. Because the financial markets are imbued with uncertainty, assumptions are more dangerous in that environment. Regardless of the fragility in our collective understanding of markets, there are enormous payoffs for those who can discern reality more accurately. In fact, academic research on trading models finds that most are delusional. “Most of the empirical research in finance, whether published in academic journals or put into production as an active trading strategy by an investment manager, is likely false.” ~ Campbell Harvey and Yan Liu, “Evaluating Trading Strategies,” 2014 This quote is particularly relevant to us at MarketPsych because we are restarting our trading business. We’re currently trading a unique media-based machine learning strategy and re-registering as an investment adviser. It has been a long road to find a strategy worth deploying capital into, and based on our prior experience, trading delusions can easily become enshrined in predictive models. Today’s newsletter examines the nature of false beliefs among investors, how beliefs shift (with an Amazon case study), honest investment strategy development, and examines what, if anything, we can do to find the truth about what moves markets. |

|||

When Delusions Crack – Brick and Mortar Retailers

(The following was written by our own Tate Hayes and a longer version will appear in Investopedia this weekend.) Nordstrom’s and Macy’s have both seen a 50% drop in stock price over the last year on the back of deceasing revenues. Wal-Mart and Best Buy shares have taken just under a 10% hit over the last 12 months. In contrast, Amazon’s stock price is up almost 70% in the last year and 135% in the past two years. Investors’ beliefs about the retail sector have changed dramatically in the past 2 years. In examining media optimism data since July 2014, a clear decline is evident. Over the last 24 months, investors became more optimistic about Amazon, but increasingly pessimistic about a number of the top brick-and-mortar retailers (Wal-Mart, Nordstrom, Macy’s, and Best Buy are charted below). The media sentiment of these individual companies are compiled in the Thomas Reuters MarketPsych Indices (TRMI). The TRMI Optimism index represents the frequency of positive, future-tense references about a company verses those that are negative in millions of articles daily from thousands of news and social media sources. The 200 day-averages of media optimism about each retailer are plotted in the chart below.

What is remarkable is both how long the delusion of bricks-and-mortar retailer safety stayed afloat, and also how quickly it is unraveling as optimism about the individual retailers plummets. First optimism about Amazon rose, and then, on cue, optimism about bricks-and-mortar retailers declined. Our new book, Trading on Sentiment: The Power of Minds Over Markets (Wiley, 2016), explains in detail how media sentiment is quantified and used to time markets and select investments. |

|||

| How We Know What Isn&39;t So

Throughout the twentieth century, a variety of stock market leading indicators achieved notoriety. The Super Bowl indicator was oft-cited in media. It was so-called because the U.S. stock market was said to rise in years that an NFL team won the American football Super Bowl. This indicator was 90 percent accurate in predicting the annual stock market direction from 1967 to 1997. However, the Super Bowl indicator is a random coincidence, the result of overfitting to a limited data set. Such spurious correlations are often repeated in the media and by the statistically illiterate. As we are seeing in the U.S. election cycle, in politics there is an advantage to sincere assertions of half-truths and lies. But in scientific disciplines like healthcare and (aspirationally) finance, objective truth is the bedrock of all subsequent activity. In 2005, Dr. John Ioannidis wrote an academic article that has become the most widely read paper on PLoS One (Public Library of Science) and the first to surpass one million views. The paper contains a proof that the majority of published medical research results are false positives (i.e., untrue).(1) Dr. Ioannidis’s statistical insights have been extended to finance by Marcos Lopez Del Prado, Campbell Harvey, Yan Liu, and others.(2,3,4,5). If a test result is considered true at a 95 percent confidence interval (two sigma), then that confidence interval must be expanded as additional tests are performed on the dataset to achieve a simile level of confidence that the result is not a random coincidence. Yet with massive data sets available, statistical overfitting is inevitable. It is tempting to believe in strategies that do not meet solid statistical thresholds because (1) it is difficult to find novel and outperforming investment strategies, and (2) the thrill of thinking one might have found such a strategy is more compelling than the repeated frustration of intellectual honesty. The incentive to find a good result often leads to short-cuts in testing hygiene and spurious correlations. Essential to identifying useful predictive relationships in data is to adopt techniques to achieve statistical confidence in positive findings. Also important is to understand the probable rationale – the underlying assumptions – for the findings. Amidst so much hype, how can we know what is real? |

|||

Our Own Trading

While trading MarketPsych’s hedge fund, we adopted numerous datamining hygiene techniques, including: rigorous data exploration of the training set only; using multiple out of sample sets and k-fold cross-validation; utilizing universal concepts and language in our ontologies; visual inspection of output; and using a human filter to exclude strategies that are not empirically supported or based on “common sense.” We are confident in the validity of our statistical hygiene and testing techniques because of these efforts to debias. However, without real-time performance and common-sense explanations, it is difficult to establish the robustness of quantitative investing strategies. To address these concerns, we have (1) an independently audited track record from our hedge fund, (2) live forward tested strategies launched online in 2013, and (3) empirical support for the validity of our strategies from psychological research. Each of those factors increases confidence, but nonetheless, modeling is very difficult to get right. Our equity curve is below.

As markets recovered from the financial crisis, our fear-based trading strategy was no longer suited to the positive momentum of prices. Yet we did not successfully pivot on the strategy, and we shut down the fund. We have a new strategy being traded currently, and it is adaptive – as media delusions shift, it compensates. This strategy appears less vulnerable to regime changes, but it’s not open for outside investors yet. Among traders the most common techniques for establishing the statistical validity of a finding include data division into training/test/out-of-sample sets and k-fold cross-validation. When data is divided into sets, typically 60% of the data is used for feature selection (identifying the best indicators), while 20% is used for testing to verify that the findings in the training set hold true in data that was “blinded”. Then once the model has been tweaked and risk management set on the training and testing sets, the model is run on the out-of-sample set to verify that it still holds true. K-fold cross-validation is another technique for verifying the predictive value of a trading system. After studying the performance of indicators on an external training set (maybe 30% of the study data), and selecting the best, then the testing set (60%) and training set (90% of alll data) are utilized for cross-validation. If k = 10%, then the data set is divided into deciles. The overall model is learned on 90% of the data and tested on 10%. The 90% and 10% data sets are randomized each pass and dozens of passes are performed. The range of performance on each 10% set gives an approximation of the model’s stability. If the model is declared useful, then a final 10% study is performed on the final out-of-sample set to verify the model’s value. In all cases of developing trading models, it also helps to watch real-time trading on paper first and then to forward-test with a small amount of real money before going live. |

|||

| Housekeeping and Closing

I met Manny well before the financial crisis while I was working part-time in a prison (to fund the launch of MarketPsych). His optimistic research tone reflected the mood of the times. Many of the popular Wall Street delusions are simply beliefs that fit the current social mood. Eventually I asked Manny, “Do your clients know you’re manic?” He replied “Of course not!” He was trying to milk his manic energy for all he could by producing as much research as possible to pay for his legal bills. I haven’t kept track of Manny, so I don’t know if he saw the financial crisis coming or how his life turned out. Nonetheless I wish him well. We love to chat with our readers about their experience with psychology in the markets. Please send us feedback on what you’d like to hear more about in this area. Learn more about improving your investment returns with insights from sentiment analysis of the herd in our new book, “Trading on Sentiment: The Power of Minds Over Markets.” If you represent an institution, please contact us if you’d like to see into the mind of the market using our Thomson Reuters MarketPsych Indices to monitor real-time market psychology and macroeconomic trends for 30 currencies, 50 commodities, 130 countries, 50 equity sectors and indexes, and 8,000 global equities extracted in real-time from millions of social and news media articles daily. Keep It Real, |

|||

| References

1. J. P. Ioannidis, “Why Most Published Research Findings Are False,” PLoS Medicine 2, e124 (2005), pp. 694–701. |

||

more here: https://www.marketpsychinsights.com/blog/

Posted in Free Courses, Investor Psychology, Risk Management

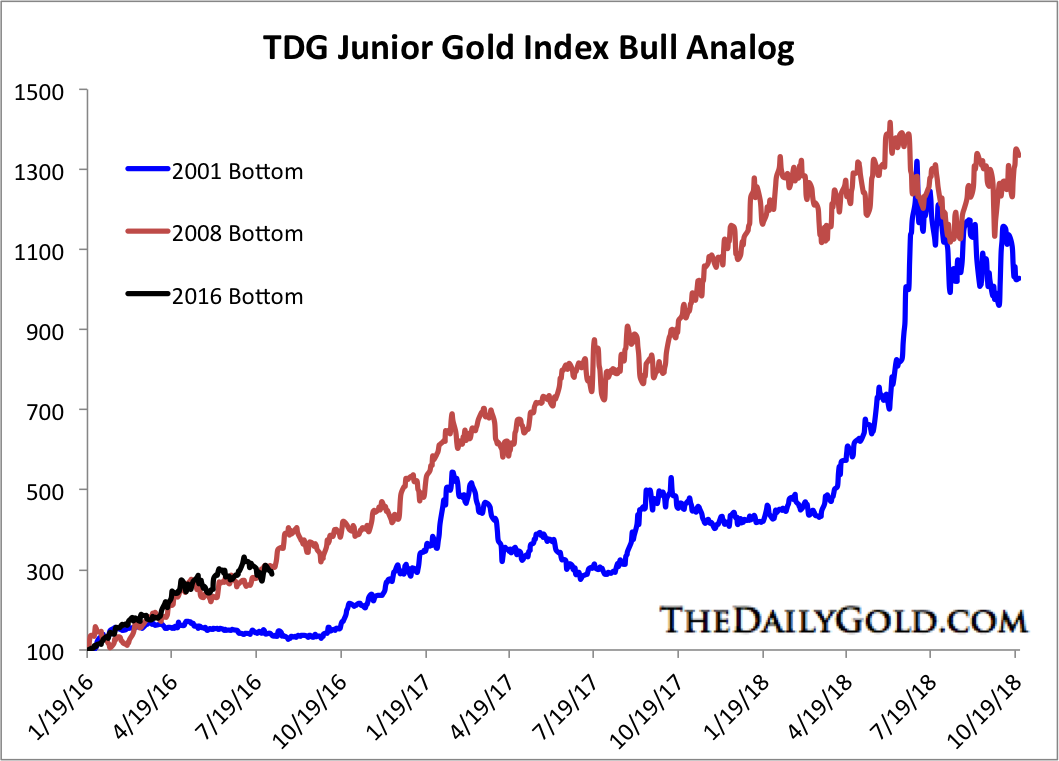

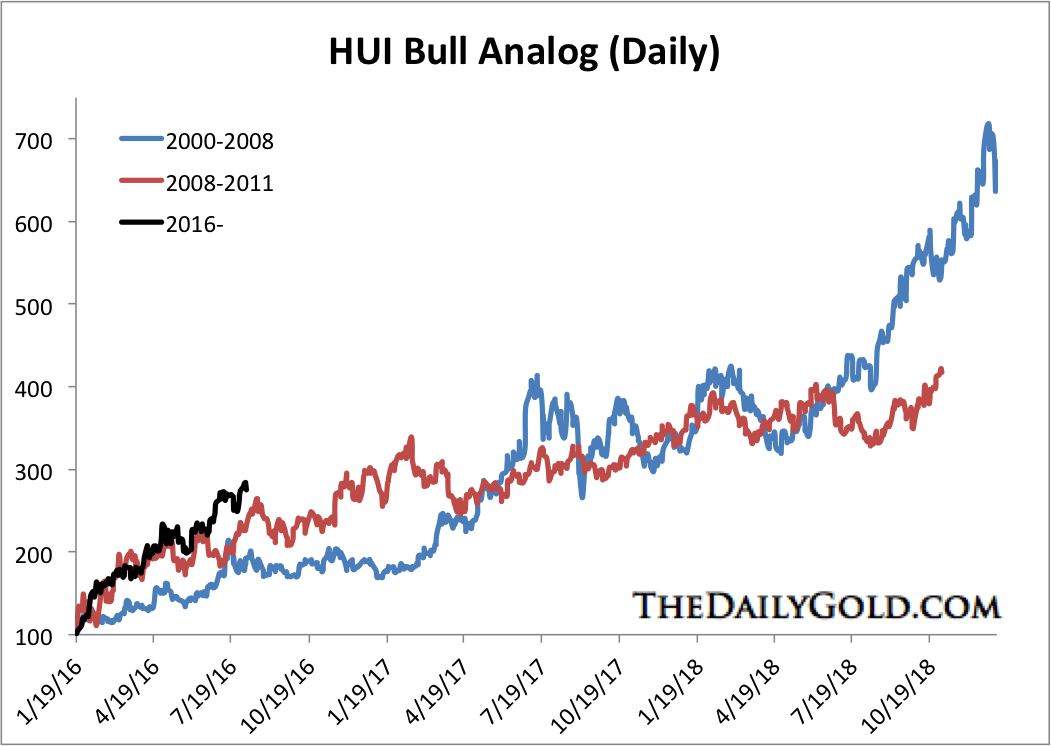

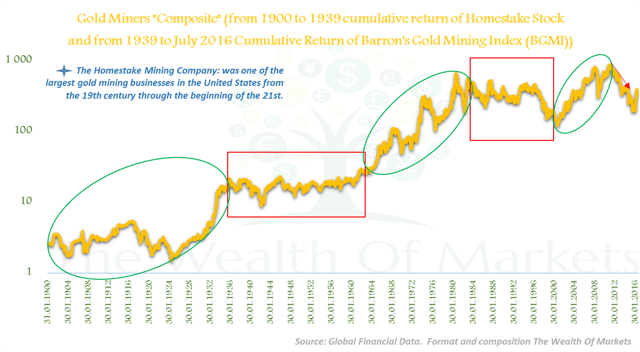

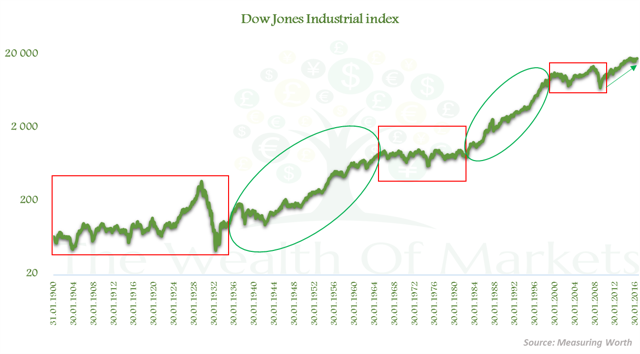

See the lows put in Jan. 11th in both the HUI Goldbugs index and Freeport McM (FCX). Only six days after the publishing of this article.

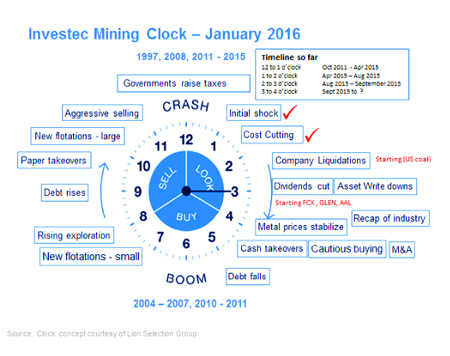

Five years ago, the FTSE 350 Mining index reached a post-financial crisis peak at just over 28,000. It currently sits at 7,134, down 75% at an 11-year low, and share prices remain vulnerable.Global commodities markets remain massively oversupplied and Chinese demand is waning, but there will come a point at which mining shares are a ‘buy’ again. (You always want to buy commodities and/or commodity stocks at the point of MAXIMUM PESSIMISM or when supply is greatest and demand lowest!).

Investec Securities has built a “Mining Clock”, which brilliantly illustrates the mining cycle, including when to buy and when to sell. It’s a real “cut-out-and-keep” for every investor.

Investec writes:

“Please see the updated Mining Clock below where we indicate that it appears still too early to be buying the mining sector. This is despite five straight years of underperformance from mining equities globally, in every sector, save Australian listed gold equities which outperformed the ASX in 2014 and 2015.” (Where is the article that told you WHEN, exactly, to buy?). Rearview investing doesn’t work.

—

The above article proves once again that no one can time a sector–except when (like in this article) there is no hope for a rebound.

http://prostedywagacje.blogspot.co.uk/2016/08/how-to-play-this-bull-market-in-gold-in.html

Last time I sold a few of my miners back in July

http://csinvesting.org/2016/07/08/time-to-sell-some-miners-but-not-much/

And now over the next few days and weeks, a time to rebuy at the margin. But if you are in a bull market Sentry__Com_BullishGold_MacLean___E then sitting tight is what you must do. At most, I think we are in six to seven on the mining clock. So far, the public is not yet participating except perhaps in the last month.

WHAT do YOU think?

HAVE A GOOD WEEKEND!

P.S.: http://donmillereducation.com/journal/ Work on yourself!

Posted in Investor Psychology, Risk Management, Search Strategies, Valuation Techniques, YOU

Tagged Cyclical Stocks, the mining clock

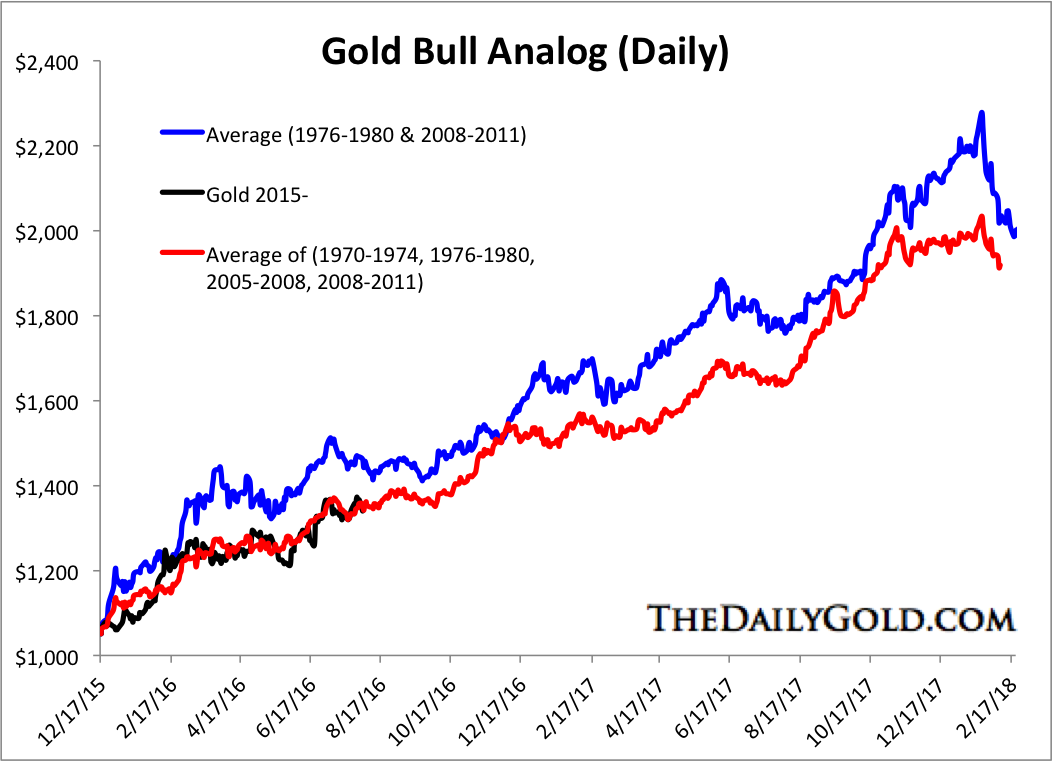

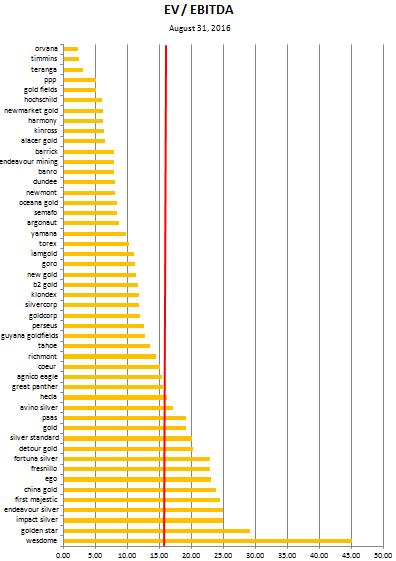

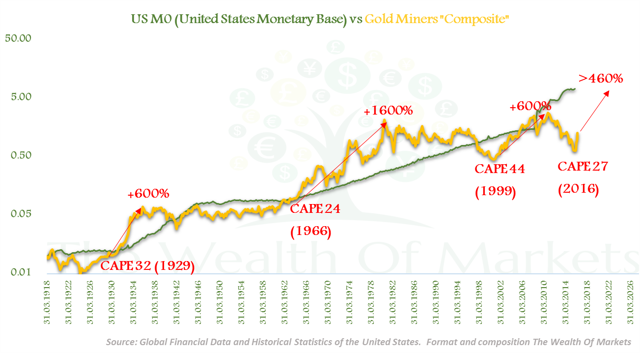

2Q 2016 Tocqueville Gold Strategy Letter – Final

The above charts came from this article. I would ignore the conclusions but focus on the historical perspective.

http://seekingalpha.com/article/4003004-gold-mining-stocks-best-investment-asset-next-decade

—

GOOD MANANGEMENT

Enterprise Product Partners August 2016 Presentation

Note the information they give investors. How management communicates is important. Do they provide sufficient detail for you to assess their capital allocation skills and operational performance. Note page 5.

Celebrate when your stock gets downgraged

Evidence suggests the professional investors in my sample have significant stock-picking skills. Interestingly, these skilled investors share their profitable ideas with their competition. I test various private information exchange theories in the context of my data and determine that the investors in my sample share ideas to receive constructive feedback, gain access to a broader set of profitable ideas, and attract additional arbitragers to their asset market. The proprietary data I study are from a confidential website where a select group of fundamentals-based hedge fund managers privately share investment ideas. The investors I analyze are not easily defined: they exploit traditional tangible asset valuation discrepancies, such as buying high book-to-market stocks, but spend more time analyzing intrinsic value and special situation investments.

Can Investors Pick Stocks on VIC 01272010-Wesley Gray

Bubble in Safety? http://intrinsicinvesting.com/2016/08/24/wd-40-a-case-study-of-the-bubble-in-safe-stocks/

Posted in Investing Careers, Investing Gurus, Special Situations

Tagged Obscure, VIC, Wesley Gray

The source and root of all monetary evil is the government monopoly on the issue and control of money. –Friedrich Hayek

An interesting discussion

Pivotal to the investment process is interest rates. For entrepreneurs to control capital, interest rates must reflect its real cost rather than merely the cost of printing money. Otherwise the money printers will dominate investment.

Zero interest rates rob future generations by bidding up the value of current government assets and privileges. A bubble of current assets inflated by near-zero –interest loans does nothing to fund the future. Retirees face a prospect of shriveled pensions and support and watching their children and grandchildren live slow motion lives. –George Gilder from The Scandal of Money: Why Wall Street Recovers But The Economy Never Does

—

I’d come to Wall Street for validation. I believed my value was in achievement, that achievement was conferred by instituions and rendered in money. I’d joined an army of bright young men and women dressed in business-casual uniforms, streaming into the service of massive corporation without any sense of why we’d chosen to dedicate our lives to further enriching the already rich, except that we needed proof that we were valuable, because at heart we didn’t really believe we were. –Sam Polk from The Love of Money

—

Moving towards a solution

https://monetary-metals.com/arizona-considers-issuing-a-gold-bond/

Deep Value Investor: 2016-05_conference_transcript

HAVE A GREAT WEEKEND!