The marginal buyer in equities: http://www.acting-man.com/?p=22909

Modern Money Mechanics:How the Fed Works. Also, view this video: http://www.garynorth.com/public/department29.cfm

The marginal buyer in equities: http://www.acting-man.com/?p=22909

Modern Money Mechanics:How the Fed Works. Also, view this video: http://www.garynorth.com/public/department29.cfm

Posted in Economics & Politics, Humor & Entertainment

Tagged Complacency, Federal Reserve, Sixth Sense

“Find the trend whose premise is false,” says George Soros, “and bet against it.”

Gold bugs seem schizoprenic. Gold prices are manipulated downward; buy more gold! I think the recent fall in gold has to do with increasing recessionary conditions and "disinflation". But when people realize that real money (financial reserves) can not be replaced by credit and debt then the price decline will reverse.

Imagine you are a major holder of new Lexus cars. Imagine you are in financial trouble. The market for Lexus cars anticipates the upcoming supply. Prices of drop. OK… but are Lexus the same as gold?

Imagine that, instead of Lexus cars, you held cash — a big wad of cash in your vault. Then, in financial trouble, you need get out your cash and use it to pay your creditors. Does the market for cash go down? Does the value of your cash decline because people know you will have to give it to someone else?

The premise is false. Real cash does not become less valuable when people find themselves in financial difficulty; it becomes more valuable. The demand for cash goes up, not down.

But wait. Today’s bills are payable in paper cash…not gold. Debtors must raise paper cash by selling their gold for paper. It’s paper they need… not real money.

Our current system runs on irredeemable, fiat, paper money. People spend it. People borrow it. Now people need more of it to pay their bills. So they sell their valuables — namely, gold — to get more paper money. The Gold price in dollars goes down, while central banks print up more paper money — just to make sure there’s plenty to go around.

One day people will stop worrying about the quantity of the paper and begin worrying about the quality of it. I am saying gold is commodity money–real money with no liabilities (promise of acceptance). But I haven’t proven anything, I am putting down thoughts. Next week I will need to prove why I believe that idea has merit. Our goal is to improve our understanding of reality.

I will need to define my terms and prove my premises to debate the reader who provided his thoughts on gold.

First, What is inflation?

The reader in his comments below says inflation is rising consumer prices.

I define inflation as any increase in the economy’s supply of money not consisting of an increase in the stock of the money (gold) metal.

Money is a commodity serving as a medium for exchanges, and–because there has been a recent prior history of exchanges–money can serve as a store of value for future exchanges.

Here is another description: Inflation is tn extension of the nominal quantity of any medium of exchange beyond the quantity that would have been produced on the free market. This definition corresponds to the way inflation had been understood until WWII. The 1941 Funk and Wagnalls Dictionary defined inflation as an “expansion of extension beyond natural or proper limits or so as to exceed normal or just value, specifically over issue of currency.”

A free market is social cooperation conditioned by the respect of private property rights,” Therefore the meaning of inflation is that it extends the nominal money supply through a violation of property rights. In this sense, inflation can also be called a forcible way of increasing the money supply (by fractional reserve banking, by monetization of government debt, by counterfeiting, by forgery, etc.) as distinct from the “natural” production of money through mining and minting.

The difference is vast and important. Friedrich A. Hayek stated that his chief objection against monetarist theory is that it pays attention only to the effects of changes in the quantity of money on the general price level and not to the effects on the structure of relative prices. In consequence, it tends to disregard what seems to me the most harmful effects of inflation: the misdirection of resources it causes and the unemployment which ultimately results from it.

So next week I will lay out my premises and show why the distinction is important. A debate without definition and/or agreement of terms is like having a contest to nail jello to a wall.

—

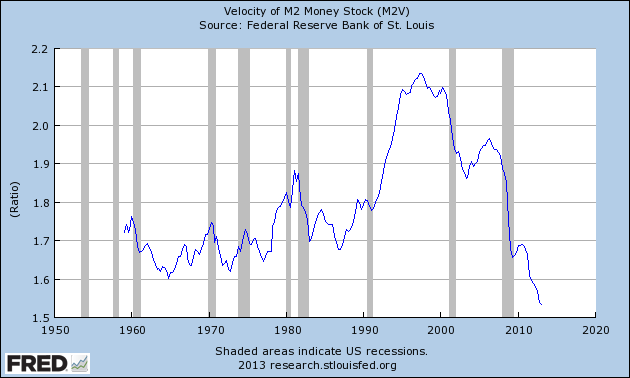

Pop Quiz: If the FED wanted to increase the velocity of money what could it do? Hint, the effect would be immediate. Why do you think the FED is not doing that? Where are the errors in this report: HIM2013Q1NP

—

A Reader Discusses Gold

I was a bull on gold for years, but switched bearish during the mania of summer 2011 and have been bearish ever since. I don't think anybody can argue that central banks are flooding the world with money. Everyone knows this is occurring and laments about it, and professional investors keep pushing gold. You'd be hard pressed to find a big name manager who doesn't like gold.

The problem is that gold doesn't actually protect you from anything - unless everyone else thinks it does.When Greece imploded back in 2010, almost all assets went down except gold and the US dollar. People thought that gold was a safe haven, and therefore it was a safe haven. Now, the situation is almost the exact opposite.Gold bulls have gotten everything they wanted in terms of bullish gold fundamentals, yet the price keeps going down. The problem is that gold is purely a psychological asset, and it's only worth what the next guy is willing to pay for it. With most senior miners cash cost well south of $1000/oz, gold is clearly more expensive than pure marginal cost analysis would suggest. That premium is the amount that people are willing to pay for "protection" against inflation, the collapse of fiat currencies, or whatever other event they think they are being shielded from. But that premium is now falling because investors realize that other assets protect them from these events much better.

If concerned about inflation, I would much rather own multifamily real estate than gold.

Rents reset every year, so they should be well-indexed to inflation, and real estate is traditionally

favored in inflationary times. Moreover, real estate produces substantial current yield, something

that gold does not.

If worried about sociopolitical unrest, the US dollar or US treasuries are a much better alternative

than gold. The US dollar is being debased at a much lower rate than other competing currencies

(i.e. GBP or JPY, and likely soon EUR), and remains the world reserve currency, making it an

attractive safe haven. US treasuries also produce yield, and I believe are unlikely to fall much in

value over the next few years because inflation will need an increase in the velocity of money,

which will take much more time.

I also agree with you that the stock market is fundamentally overvalued (although I have thought

this for over a year now and been wrong), but I would even buy equities rather than gold if I was

worried about inflation. In an inflationary stance, companies should have pricing power and

grow their earnings near the rate of inflation, so equities should be able to keep pace with inflation

over a longer run.

I believe gold owners are figuring out this argument, especially as it pertains to the nascent bull

market in real estate, and that is why they are selling. I also think the "gold is just another currency"

argument is terribly flawed, as I have yet to go to a country where I can walk into Subway and buy

a foot-long with gold or silver. Moreover, if gold were a currency, it would be viewed with a great

deal of skepticism considering it has fallen over 10% in one day before, something that has never

happened with a major currency.

I think as gold ETF holders continue to turn elsewhere to hedge their fears, the price of gold will

continue to fall, regardless of what happens in the risk market. If stocks continue to rise, people

will sell gold and buy stocks. If stocks fall, people will sell gold and buy real estate or treasuries.

I strongly believe the bull market in gold is over, and over the course of the next couple years, we

will see substantially lower prices, eventually falling well below $1000/oz.

My definition of inflation is rising prices, with a bias towards consumer

prices vs. asset prices. In the past few years, US consumer prices have been flat or falling in my

estimation, while asset prices have been going through the roof.I believe a large part of the gold bull

market was an expectation of CPI inflation, that has simply failed to materialize.

I agree that gold prices have never tracked the CPI. Gold prices have risen and fallen for many

different reasons over the past few decades, but that is largely my point: gold's price is purely a

psychological function. That would also be my answer to your question about gold's utility,

its utility is simply what the next buyer is willing to pay, or said another way, its utility is the

reason the next buyer is buying it. That price had risen for a decade straight because of fears over

monetary debasement, inflation, and general pessimism on the effectiveness of central banking,

but it appears there are no more marginal buyers left.

The advent of gold ETFs brought a huge number of new players in the market, and they were

largely responsible for the run-up in prices from 2008 to 2011. However, many of these players

were simply allocating to gold because their advisors were telling them to, without truly

understanding why they were doing it. They were doing what investors do in any mature bull

market, they buy because the price is rising. Now, these same investors are selling because the

price is falling. Teoretically, they could turn around and start buying again, but the problem is,

what would actually cause this? What positive surprise is there left for gold that has not already

been disclosed?

When gold prices ran up to $1900/oz in September 2011, it was not quantitative easing that caused

it, but rather the expectation of QE3. At this point, the Fed has already indicated they will print

an unlimited amount of money, only varying the size of their asset purchases, with no time limit set.

It is already on the table that the Fed will print unlimited, so what positive surprise is left? Every

other central bank has stepped up their liquidity too over the past 1.5 years, yet the price of gold

continues to drop. My point is that, in the past, gold has served as protection against future currency

debasement, but it has now ceased to serve that function. This is a problem because gold only protects

us from anything if the rest of the market thinks it does. This key change in sentiment and market

thought on gold is why I believe the price is falling.

As I said before, with marginal cost on gold way below where it is now, there is plenty of room

for the metal to fall. In the long run, commodities must return to their marginal cost, even after

moving up or down according to demand shocks.As for central banks, I do not believe them to be a

reliable indicator of anything. If they knew what they were doing, the GFC would never have

happened in the first place. Also, central banks were massive net sellers of gold at the bottom i

in 2000, yet are big buyers of gold now that prices are near their all-time high. If anything,

they are a contrarian indicator.

Lastly, countries like Germany will probably continue to repatriate their gold because they

are broke. European countries are some of the largest holders of gold inthe world, and\

considering how high the price of gold is, I would want mine back too if I were them.

With their failing economies and possibly soon to be failing currency, gold is their asset of highest

worth. If Germany, Italy, and the EU were to sell their gold or have less of it, the credit of these

countries would almost certainly drop, in the same way that if they had less currency reserves.

However, with the Cypriot central bank selling gold to finance their bailout recently, the writing

is on the wall that gold reserves may be tapped. This would turn the EU into net sellers of gold,

potentially dumping huge amounts onto the market if their debt crisis ever flares up again. END

Human decisions affecting the future…cannot depend on strict mathematical expectation, since the basis for making such calculations does not exist;….it is our innate urge to activity which makes the wheels go round, out rational selves choosing….but often falling back for out motive on whim or sentiment or chance.” John Maynard Keynes, 1935

This is just one tiny tool and not one to place all your marbles, but with high sentiment there isn’t room for error (witness AMZN today–down in price by over 6%). I expect that if a downturn occurs in asset prices, the monetary fire hoses will be turned on high. But if monetary growth continues to decline (unless the “air” being pumped into the debt balloon increases, the balloon begins to sag). I will add to my shorts in CRM, GE gingerly.

From www.economicpolicyjournal.com

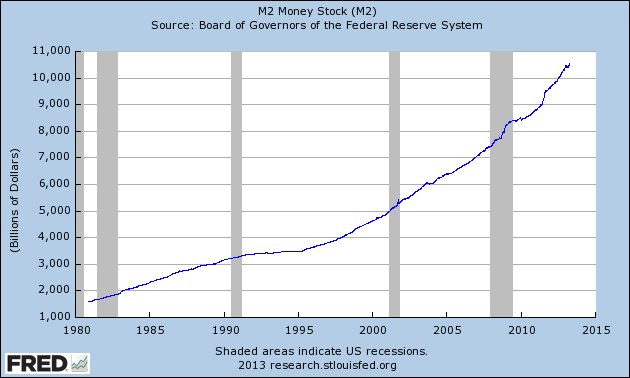

Money supply (M2 NSA) growth continues to decline. The latest data for annualized quarterly 13 week growth is at 3.8%. This is a dramatic change from just 12 weeks ago when money growth was at 11.4%. Below are the money growth figures for recent weeks, with the last number being the most current. The first data point, 5.1% is for the week of October 8, 2012

5.1%, 5.6%, 6.6%, 7.1%, 7.5%, 7.8%, 8.2%, 8.4%, 8.7%, 9.0%, 9.3%, 9.6%, 9.9%, 10.7% 11.4% 11.4% 11.4% 11.0% 10.5% 9.8% 9.5%

Here are the steps one can use to calculate this data, which all comes from the Federal Reserve weekly release identified by the Fed as H.6. From the H.6 release, go to table 2 and look for the non-seasonally adjusted, 13-week M2 data. then use non-seasonally adjusted data. You want to know how much money is out in the system bidding for goods and services.

Second, use 13 week average rather than single week data because there can be a lot of noise in the system from week to week, depending upon where money is flowing to and from in the system. This causes the data set to move more slowly, but it also means it is less volatile and less likely to set off “false positives”.

Finally, take the 13 week average of a 3 months ago (12 weeks) and calculate the change against the current week, then annualize this result by multiplying by four.

The reason you should annualize the quarterly change rather than look at the full 12 month period is that money entering the system now will have an impact now. If I use a full 12 month data set, the change may not be detected for months, if at all–especially given the up and down changes in money supply witnessed during the Bernanke era.

A further note on the current decline in money growth is that it is not occurring because the Federal Reserve is not pumping money into the system. During this same period, the last 12 weeks, the monetary base has been growing at 25% plus. (See the Fed’s H.3). The high-powered money the Fed is creating is simply ending up back at the Federal Reserve as excess reserves. Banks are not lending the money out and are content to place the funds at the Fed. Excess reserves from end December 2012 to End March 2013 have gone from $1.5 trillion to $1.7 trillion, an annualized growth rate of 53%.

Perhaps that is why commodities and gold have been weak?

Go here:http://www.federalreserve.gov/releases/h6/Current/

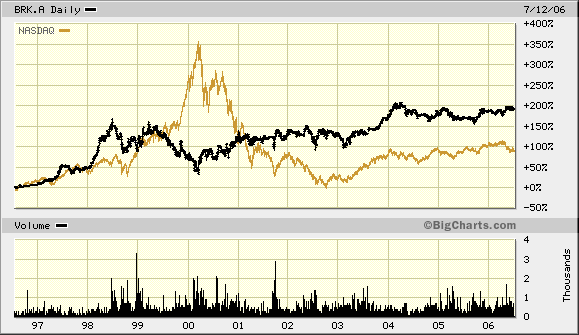

A Reader’s Question

I hope you would be willing to give me some advice, I am currently sitting on 150k in cash right now. That I don’t know what do to do with it, I have a watch list of:

Therefore, I am looking for a sanity check. Right now I feel that Small or Micro Cap’s are out of my circle of competence.

My game plan is to hold cash until the next major market down turn, and hope Berk A comes down to a point where I can purchase.

So I guess my questions are:

Thanks for your time,

Reply: I can feel your pain. The financial repression is pushing many people to take on risk to preserve and grow their wealth. I am assuming that this money is what you have totally dedicated to equities. 10 to 12 names gives adequate diversification and 20 is probably too much to to follow.

Don’t forget that your best opportunities may not be today, but tomorrow.

I will come back to answer your question in more detail in a few days because I am on the road, but you should not get caught up in whether the stock market will go up or down. NASDAQ was about to crash, but would that knowledge have kept you from buying Berkshire. I hope not. Buy Berkshire/Short the NASDAQ!

You first have to value each company then determine your required rate of return–what price will you pay. This blog has several case studies on valuation–use the search box in the right hand corner.

Perhaps some readers can advise until I return. Hang in there. Patience.

I feel a bit like the Vet last in line to board the plane before leaving ‘Nam when offering advice–see last 15 seconds of this clip.

Posted in Economics & Politics, Risk Management, Valuation Techniques, YOU

Are conditions deflationary or inflationary? Do bonds have lower to go? If I wanted to short long-term bonds, I would choose corporate bonds over U.S. treasuries because you are fighting a subsidized market of central banks buying government debt.

WHAT IS AN INTEREST RATE?

An interest rate is the discount that individuals place on the value of future goods compared to present goods. This discount applies to money and everything else. Mises said, “Originary interest is a category of human action. It is operative in any valuation of external things and can never disappear” (Human Action, page 524).

This discount “is a ratio of commodity prices (note contango between June Gold and Dec. Gold), not a price in itself” (p.523. “Originary interest is not ‘the price paid for the services of capital’….It is, on the contrary, the phenomenon of originary interest that explains why less time-consuming methods of production are resorted to in spite of the fact that more time-consuming methods would render a higher output per unit of input” (p. 523). Interest is not profit. Profit is the difference between the purchase price of a good and its sale price, after having deducted the income that would have been earned by placing the money at interest. Profit originates in the entrepreneur’s perception –his guess–that his competitors have underbid the price of some resource, and that future consumers will bid more than his competitors think (p. 532).

Money transmits value, Mises taught, but money does not measure value. This distinction is fundamental in Mises’s theory of money. “Money is neither an abstract numeraire nor a standard of value or prices. It is necessarily an economic good and as such it is valued and appraised on its own merits, i.e., the services which a man/woman expects from holding cash. (Human Action, pp. 414-415). Gary North, Mises on Money

Read more on the value of money: http://www.mises.org/daily/6380/The-Value-of-Money

What is, then, the best monetary policy? He argues that in light of his previous considerations “the state should at least refrain from exerting any sort of influence on the value of money. A metallic money, the augmentation or diminution of the quantity of metal available for which is independent of deliberate human intervention, is becoming the modern monetary ideal.”[17] He adds: “The significance of adherence to a metallic-money system lies in the freedom of the value of money from state influence that such a system guarantees.”[18]

The Case for Owning Gold Has Collapsed; Yellow metal could be headed much, much lower http://is.gd/h5KW6v. Gold could be headed not much lower, but much much lower. This was written on April 18, when the value assigned to the monetary relic (AKA its nominal price) resided at $1391 per ounce. So be warned, Mr. Gold advises that gold could go much much lower. Gold bugs take heed; Mr. Gold himself has put the double ‘much’ whammy on you!

The article: The Gold Dilemma. The article is riddled with logical fallacies. Using CPI and GDP to measure anything meaningful is a fantasy–even forgetting that those indexes are politically constructed by bureaucrats.

Another view of gold’s history: 99816519-Special-Report-Gold-2012-In-GOLD-We-TRUST.

Why I own gold bullion–as a hedge against monetary chaos. Own what the government can’t print.

All the Silver Ever Mined

All the Silver Ever Mined

A reader’s question from the prior post: Am I 100% in cash? No, I have cash, gold bullion, selected precious metals mining companies, a few other companies, and a tiny short position in certain stocks like GE and CRM. If you think holding on through thick and thin after buying at the highs EVEN with UNSUSTAINABLE Fed manipulation of money and credit is a good plan, then view page 8 here: A Lesson in Financial History by Mish. Also, for more perspective on the unsustainability of current corporate mean-reverting profit margins see: An Unsustainable Equilibrium_Hussman. View the video presentations here and consider a donation to cure ALS: http://www.winecountryconference.com/2013-speaker-presentations/. People love to follow the crowd and momentum while mal-investment increases, so expect more S&P 500 movement to the upside until–unexpectedly–a surprise hits and people need to sell their “hot potato.”

But if you own great franchises at good prices then you have few worries. I wish I could find them now.

Short the SPY and Long PHYS for fun (not for real) at the highest offer for PHYS ($10,000 at $12.30 for PHYS) and lowest bid for SPY ($10,000 shorted at $158.10) on April 25 and lets see where we are in 12 months.

Short the SPY and Long PHYS for fun (not for real) at the highest offer for PHYS ($10,000 at $12.30 for PHYS) and lowest bid for SPY ($10,000 shorted at $158.10) on April 25 and lets see where we are in 12 months.

Update on April 29, 2013:

This won’t end well–Chicago Slim

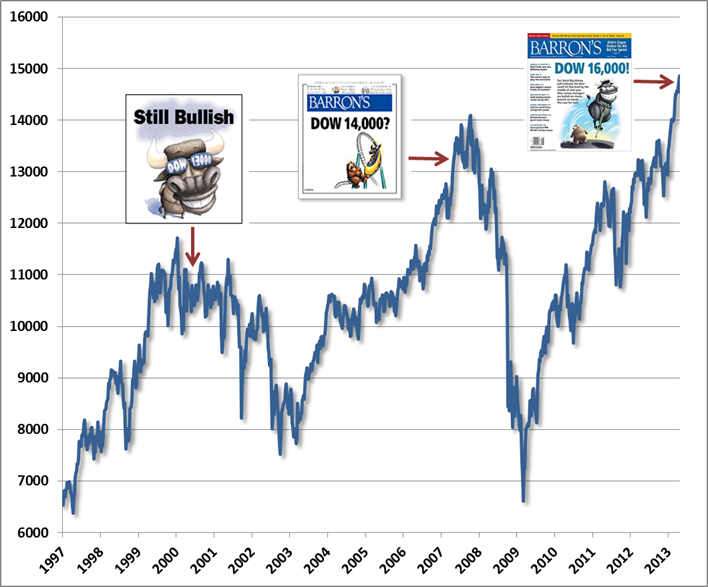

Only Barron’s semiannual Big Money poll of professional investors also is setting a record — for bullishness, that is. In our latest survey, 74% of money managers identify themselves as bullish or very bullish about the prospects for U.S. stocks — an all-time high for Big Money, going back more than 20 years. What’s more, about a third of managers expect the Dow Jones industrials to scale the 16,000 level by the middle of next year, notwithstanding a dismal week of selling that left the blue-chip index at 14,547.51 on Friday.

This spring’s survey is notable, as well, for the dearth of bears: A mere 7% of respondents are pessimists today, down from 27% last fall.

A contrasting view:

A few reminders…

“Still Bullish! (Dow 13000)” – Barron’s Magazine Big Money Poll, May 1, 2000

The May 2000 Big Money Poll was published with the Dow Jones Industrial Average at 10733.91. The Dow had already peaked nearly a thousand points higher in January of 2000, and would go on to lose about 40% of its value in the 2000-2002 bear market, with the S&P 500 and Nasdaq faring far worse.

“Dow 14000?” – Barron’s Magazine Big Money Poll, May 2, 2007

http://www.hussmanfunds.com/wmc/wmc130422.htm

http://www.hussmanfunds.com/wmc/wmc130415.htm

Government finance and the nation’s medium of exchange have in the future to be two separate things. -Ludwig von Mises

The real secret of magic lies in the performance.–David Copperfield

Lecture 3 was here:http://wp.me/p2OaYY-1Sh

===

Lecture 4: Listen to the lecture:

https://www.yousendit.com/download/UVJpYnUrK3huSlFzeHNUQw

while viewing the lecture slides:Econ400 Lecture 4

Readings: Money and Credit_Mises Ch 7 and 8

Quiz: Quiz for Lecture 4 Readings Chapters 7

Supplementary Readings:

—

Conditions Today

Video Presentation from an “Austrian” Money Manager, John Hussman http://www.winecountryconference.com/2013-speaker-presentations/

Beware of profit margin REVERSION TO THE MEAN! http://greenbackd.com/2013/04/19/jeremy-grantham-profit-margins-are-probably-the-most-mean-reverting-series-in-finance/

Great Blog on gold, money and markets from an Austrian perspective: www.acting-man.com

Great Attitude for an investor (Rick Rule)

HAVE A GREAT WEEKEND.

Let me know how to improve this blog………

Posted in Economics & Politics, Free Courses

Tagged Gold Wars, Hones Money, Mises, The Theory of Money and Credit

Read about a contrary indicator: http://theshortsideoflong.blogspot.com/

http://theshortsideoflong.blogspot.com/2013/04/daily-notes_18.html

From www.grantspub.com:

But for those who buy this and anything related to precious metals mining:

then this is what it feels like: http://youtu.be/2Nax7YiPDfI

The Investment Hunter: L_AR12_Graphic_Novel_v12

To be long gold is, in a grand thematic way, to be short the socialization of risk –James Grant

Listen first econ400_lecture3 as you view these: 2012 1Q Mises on Money and Banking Lecture 3. Then read the chapters along with the study guide: CHAPTER 3. Supplements to the chapters: Chapter 3 Sanchez Supplement to the Readings

Extra Credit

Take the quiz: Quiz Lecture 3 on Chapters 5 and 6 in Money and Credit

———-

What Does Cheap Really Mean?

http://www.adventuresincapitalism.com/post/2010/03/15/What-Does-Cheap-Really-Mean.aspx

Everyone tells you that they want to buy cheap stocks. What does that mean? There are so many metrics out there: price to sales, price to book, price to earnings or cash flow. Which are the key ones?

I think people get caught up too often looking at a few key metrics and they lose sight of the bigger picture. In the end, most little companies never become the next General Electric. They either burn out, they hit some plateau and stagnate, or they get acquired by a larger company. When thinking of smaller companies, you really need to ask yourself; what will this company be worth a few years from now and what will a much larger company pay for this business? Remember, acquisitions create cost savings and synergies. For this reason, an acquirer is likely to pay a lot more for a company than the broader market is willing to.

This leads to a bigger question; do this year’s earnings even matter? Probably not. Most people know roughly what this year’s earnings will look like. They even have a reasonable guess about next year’s earnings. No one knows what will happen in three or five years. That’s where you should focus your attention. Look for businesses that can earn many times what they are going to earn this year. Look for growth.

….read more: What Does Cheap Really Mean

Is this company cheap? EGD-FinancialStmt-2012 and research here: http://www.energold.com/s/InvestorVideo.asp

Posted in Free Courses

Tagged Mises, small cap investing, Theory of Money and Credit, What is cheap?