Below are supplementary readings and original sources for Chapter 2, Contrarians at the Gate, in Deep Value. This is an important chapter because we are introduced to the father of security analysis. He was the first person to systematize his analysis and separate the price of a security from its intrinsic value.

I realize that some may find Graham fusty and his prose turgid/boring, but Graham was a Renaissance man who had a razor-sharp intellect and integrity. You can’t lose by reading his works. Note his attitude, skepticism, and logic.

So far in the course I am surprised by the ironies and subtleties of Deep Value investing–picked up in the preface of the book, Deep Value. Our Deep Value Group has close to 400 members, yet, currently (Jan. 17, 2015), the number of net/nets in the US market is negligible. Financial assets (with a few exceptions) are sky-high in valuation due to Central Bank intervention, negative interest rates, and a six-year upward trend in US bonds and stocks. I am surprised at the interest.

We invest today for the future, but the future is unknowable. Look at the predictive record of experts! Investors tend to extrapolate the past into the future just in time for a reversal of fortune–reversion to the mean reverses the trend.

Deep value investing takes advantages of the cognitive biases of others to gain profits, but if we are human too then how do we avoid the same? Cheapness or the discount from intrinsic value is the main determinant of margin of safety. The cheaper you buy the less risk and MORE reward. This smashes academic finance theory in the face.

Here I am quite surprised that the highest returns to the net/net strategy go to the MONEY-LOSING companies. The worst of the ugly gain the most. Perhaps because price drops the most due to fear and earnings trend extrapolation. Like assuming the driver of the car will continue to motor off the cliff instead of turning or stopping the car.

A TEST: Let’s say a company earned $5 per share and it is growing at 5% per year, the cost of capital is 10%, and it is trading at $85 per share. Then the next year earnings drop to $1 per share and the following year earnings drop to $0.05 or five cents, the next year earnings go up to $3 and in the fifth year back to $5.25 and 5% growth. After ten years the company will continue to grow but only at 3%. Guess the price drop quickly and write it down. Now do the DCF and see where the intrinsic value is compared to your guess.

Last year $5.00

Year 1 $5.25

Year 2: $1.00

Year 3: $0.05

Year 4: $3.00

Year 5: $5.25

Year 6: $5.51 (5% growth)

…. next year, next year, etc.

After year 10, then terminal value 10% cost of capital with 3% perpetual growth. Can a financial wizard post in the comments section? Was anyone surprised by your initial reaction the Intrinsic value result vs. their initial thoughts on how price would react?

—

Back to the post….

The higher probability (Montier, 5%) for each INDIVIDUAL company to go down 90% or more vs. 2% of non net/nets may cause other investors to shy away from investing. HOWEVER, the GROUP of net/nets STILL outperforms. You have certain companies go to zero and some rebound multiple times but you don’t know which ones. You have to deal with much uncertainty but believe you are playing the odds like an insurance company.

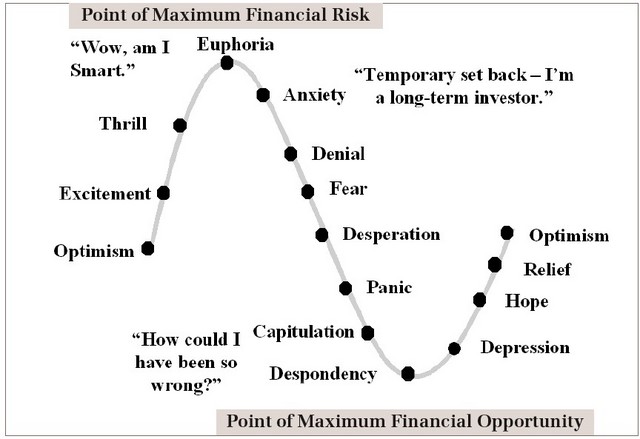

When net/nets are abundant like in 1932, the world appears to be ending. Investor fear is off the charts. The question is whether you will have the capital to buy and the courage to act. Again we come round and round to temperament or character or whatever you want to call acting in the face massive fear.

But knowing that a company is too cheap when it trades at less than 2/3rds to net asset value (Asset value is tenuous, liabilities are 100 cents on the dollar) does not seem difficult, but probably the surrounding circumstances for the company and/or market are ugly! “Don’t you read the papers!” an outsider might say if he or she learned of your purchase.

Remember 2009? Jim Cramer in a panic. http://youtu.be/rOVXh4xM-Ww?t=1m35s (just paste into your browser)

Those are my thoughts and questions so far as I keep reading.

Graham’s Writings and Testimony

Graham Testimony to Congress (note his remarks on the MYSTERY of price eventually closing the gap with intrinsic value)

Important writings on Liquidation Values during the 1930s

1932_American Corporations Worth More Dead than Alive 3 Parts by B Grahams (Please read). You can’t understand the depths of despair in the financial markets (and thus the net/nets and prices below liquidation values) without understanding the preceding boom.

Historical perspective

A Study of Market History through Graham Babson Buffett and Others The 1920s BOOM.

A Great Depression_Rothbard Obviously, you don’t have time to read this, but IF you do want to understand the causes of the biggest bear market in US history then this is the definitive work. The book destroys the common wisdom that the depression was caused by the Fed’s tight monetary policy.

The Outperformance of Net/Nets

Net NEt Strategy in London

97001708-Case-for-Quantitative-Value-Eyquem-Global-Strategy-20120613

Benjamin-Graham-s-Net-Nets-Seventy-Five-Years-Old-and-Outperforming I imagine that some net/nets are micro/nano-cap stocks under 50 million in market cap and with wide (5% to 10% bid/offer spreads) perhaps the studies do not deduct the spread?

There is a lot here so I will refrain from posting until the middle of the week. Take your time with Chapter 2. I will be posting next on Klarman’s thoughts on liquidation and valuation.

Traditional finance savaged: The Dumbest Ideas in Finance_Montier

How NOT to take this course

You don’t have to read EVERYTHING, but you do have a choice. Better to understand what you read.