A very interesting presentation of how Barrick is planning its future.

—

CORRECTION

I have often mention gold as a “Store of Value.” I never defined my terms.

I apologize. A better explanation by Keith Weiner of www.monetary-metals.com

Store of Value Fallacy

And this leads us to make one final, if tangential point. We often hear people talk about gold as a “store of value”. If you have a tank, that is a store of water. A grain silo is a store of wheat. In both cases, what is being stored is a quantity of a commodity. In this sense, a vault is a store of gold.

However, economic value—as we see above—is whatever the bidder is willing to pay. Gold’s moneyness does not come from it commanding the same amount of wheat today as it did last year or 2000 years ago. In fact, its purchasing power of wheat is not fixed. Over the last ten years, pricedingold.com shows that wheat has ranged from about 0.9 grams gold per bushel to 3.6g. The highest price during this time is 4X the lowest.

One reason for gold’s moneyness is that we value the next ounce of gold—the marginal ounce—the same as the last one. Proof of this extraordinary claim is observed in the extraordinary fact that virtually all gold ever mined in 5,000 years of human history is still in human hands. Gold is not produced to be consumed, but to be held. And we keep on producing, regardless of how much has already been produced.

In other words, we measure the value of gold like we measure the value of all other things in the economy—in gold. Gold does not have constant purchasing power (perhaps we should use scare quotes “purchasing power”). It has a constant price. The price of gold is always 1. This is not expressing a tautology. It is expressing that gold has constant marginal utility.

Gold is the steel meter stick of measuring economic values. Even if we climb in elevation (quantity) the meter (ounce) does not shrink.

My favorite book to recommend is The True Believer: Thoughts on the Nature of Mass Movements by Eric Hoffer. CSInvesting seconds this recommendation.

Review:

The book provides a concise and astute portrait of the personality type that is drawn to authoritarian institutions, whether political or religious. Hoffer makes an excellent case that the mass movements – the fascists, the communists, and the various brands of religious fundamentalists, that have caused so much death, suffering, and chaos throughout history in their attempts to impose their values and belief systems on others, have all depended on people of basically similar character to fill their ranks.

The true believer, as Hoffer portrays him/her, is someone who yearns for certainty and fears ambiguity; who sees the world in dualistic terms, black and white with no gray areas; who prefers to simply follow orders, letting others make the hard ethical decisions; who revels in belonging to an exclusive group and looking down on outsiders, particularly if they belong to a group the leaders have chosen as scapegoats.

Every voter should read this book and then look at the world today – the politics of fear and division, the growth of fundamentalist religion, the strident bigots on talk radio and TV – and then start working to reduce the danger they all pose to the freedoms in our Constitution, to the separation of church and state, and to our standing in the world.

— Back to Mr. Rosenberg…………

There is no discussion about investing in the book, but in my opinion, it is extremely helpful in understanding markets. It conveys the nature of human behavior in mass–how people act as a group. One of his great examples is explaining why people riot. There is no reason and no logic. People just get caught up in it. Riots don’t end all at once, they end person-by-person—that is markets. People panic in a group, but they come back to their sense one by one. That is why stock move incrementally the way the do.

CSIMA (Columbia Student Investment Management Association): How should they think about investment and time horizon?

JR: Young people today in business are much more macro-oriented than micro-oriented. They spend much more time on what is going on in Europe or Federal Reserve policies. They don’t focus much on company specifics. Even when they do they have a very low level of confidence in what they are doing. It’s very unfortunate. I hate that they don’t teach financial history in business schools. If it was up to me, I would make financial history and all history a number one requirement for business schools. Understanding how a spreadsheet works can be learned on the job easily but understanding the continuum of history requires certain intellect. I cannot for the life of me under-stand why business schools are not teaching financial history.

My advice to young people, if they really want to be successful in this business, is to learn financial history. Learn history in general and then dig deeper into financial history and you will not be in such awe of everything that’s going on. I see the same problem in my office. People just don’t know any financial history and they think that everything that is happening is unusual. Everything else can be learned on the job.

—

The Course on The Economics of the Great Depression

In this five-lecture course, Dr. Robert Murphy reviews the causes of the Great Depression, the response of the Hoover administration, and the New Deal. The focus is more on economic analysis rather than historical narratives, contrasting the Keynesian interpretation of various events versus the Austrian explanation in particular. Topics include the operation of the gold standard and the allegation that it inhibited policymakers from implementing the “stimulus,” Herbert Hoover’s supposed austerity program, the Friedman-Schwartz theory that the Fed’s unwillingness to inflate led to the severe downturn in the early 1930s, recent academic research showing the cartelization effects of the New Deal, and the myth of wartime prosperity. Dr. Murphy’s book, The Politically Incorrect Guide to the Great Depression and the New Deal, would be very helpful for students, but it is not required for the course. All necessary reading materials are provided.

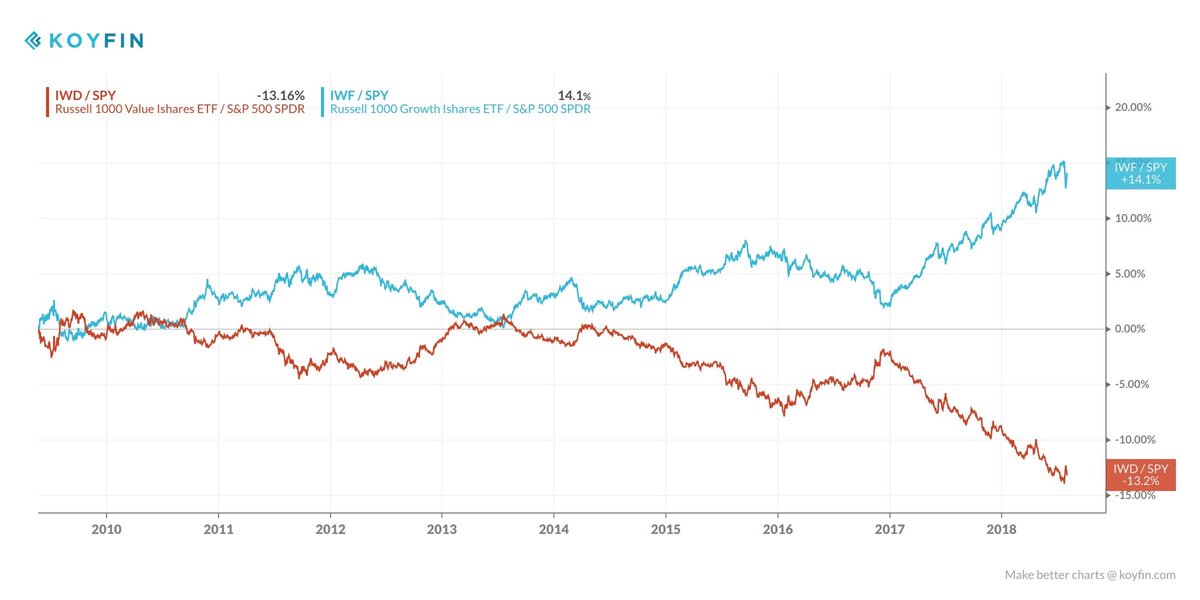

Active Managers Horizon Kinetics Worth a careful read. Note the underperformance of several famous investors. Did they ALL become stupid at the SAME TIME?

Perhaps a way to beat the ETF driven overvaluation is to search for companies that are in few indexes such as TPL or CVEO, for example. And search for owner-operated companies. Owner_Op_Paper With founder or owner-operated companies, there is less float so fewer of these companies end up in ETFs. When you see that Blackrock is a majority owner in a stock that you own but the stock represents only .003% of their five trillion dollar portfolio, you have a festering problem. Look for those founder led companies that treat shareholders fairly:

Karl Pillemer of Cornell University interviewed 1200 people age 70 to 100+ for his book, 30 Lessons for Living,

asking them:

“If you look back over the course of your life, what are the most important lessons you learned that you would like to share with younger people?”

What was the #1 answer?

“Life is short.”

Seneca, in a beautifully worded passage, strongly disagrees:

“It is not that we have a short time to live, but that we waste a lot of it. Life is long enough, and a sufficiently generous amount has been given to us for the highest achievements if it were all well invested. But when it is wasted in heedless luxury and spent on no good activity, we are forced at last by death’s final constraint to realize that it has passed away before we knew it was passing. So it is: we are not given a short life but we make it short, and we are not ill-supplied but wasteful of it… Life is long if you know how to use it.”

No offense to Karl. He did a survey. So he didn’t necessarily get the right answer, he got the most common answer.

I’m with Seneca.

Life doesn’t have to be short.

We all have 24hrs in a day. Every single one of us.

You can use them to create something amazing, to visit that someone special who misses you desperately, to provide for your family, or to savor a great moment.

But don’t waste your hours.

Don’t end up wondering, “What have I been doing with my time?”

Leave a trail of accomplishments or smiles behind you.

– Andrew

—

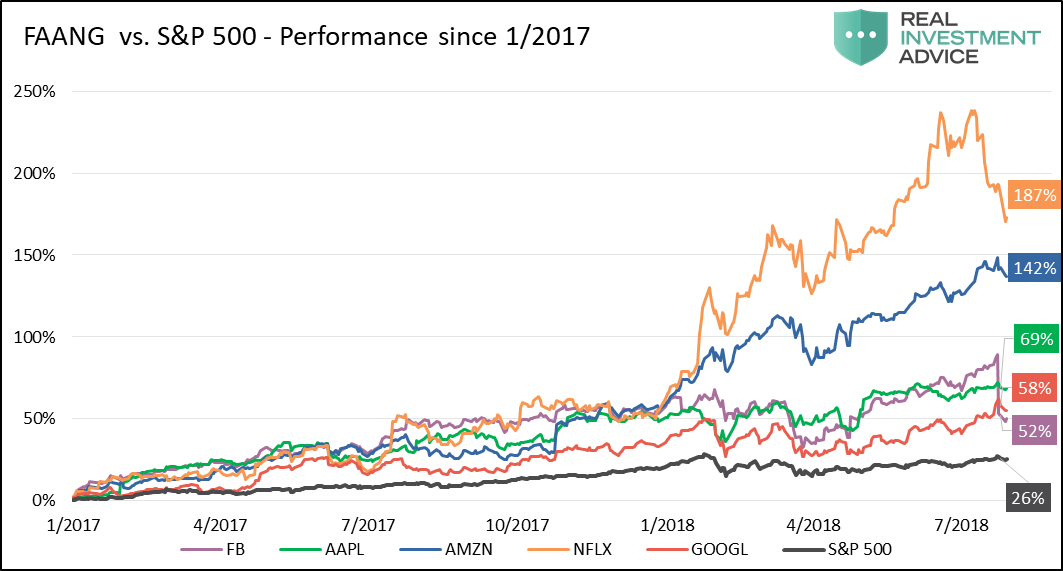

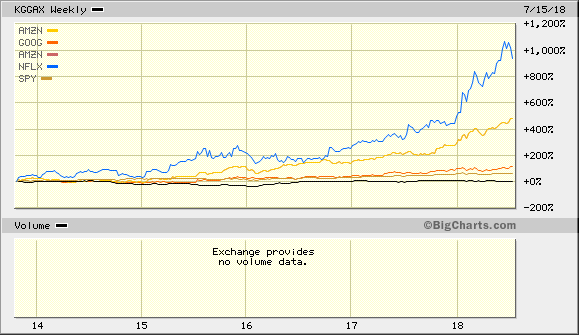

A Deep Value Investor’s Perspective: Kopernik vs, SPY and then FANGs

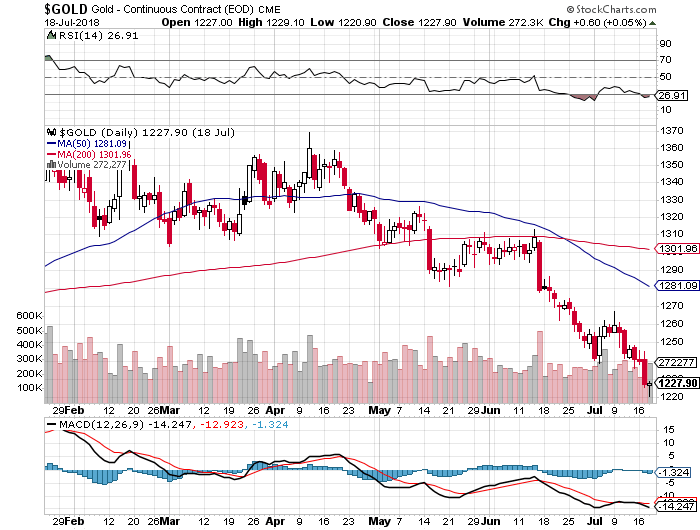

On April 11, 2018, the price of gold in US Dollars was $1,370. This morning on July 19th, the price was $1,2110.90 for a decline of $159 in 99 days. If current trends continue, then in 712 days or less than two years, the Gold price in USD terms will be about $0.00. The trend is your friend!

The single greatest mistake investors make is to extrapolate recent history out into the future. They take the financial returns of the past 5 days or 5 years or even 50 years and assume the next few days or years will look just the same without any consideration for the historical context or conditions that provided for those returns.

They forget that, while ‘history may rhyme, it doesn’t repeat itself’ (Twain). Or that, “the only thing that is constant is change” (Heraclitus). These two famous quotes apply to the financial markets as much as anything.

Ignoring these truths and instead simply extrapolating is why investors are suckered into pouring money into the stock market only after a run of great performance. They believe that the recent gains are about to repeat to their great benefit when they should be thinking about what conditions allowed for those gains to take place and analyzing whether they are still relevant or not.

This is also why they are suckered into selling only after a painful decline as they did at the lows made during the financial crisis. They believe that they are about to suffer another 50% decline on top of the one they just endured when they should really be reminding themselves that change is the only guarantee in life.

I believe this is one of the biggest problems with so-called “passive” investing. It is built upon the faulty premise that it is ‘impossible to forecast’ the future returns of any asset class over any period of time so we should just own all of them all the time. My response to this is that while ‘ignorance may be bliss’ it’s not a valid investment strategy.

In his 1992 letter to Berkshire Hathaway shareholders, Warren Buffett wrote:

We’ve long felt that the only value of stock forecasters is to make fortune tellers look good. Even now, Charlie and I continue to believe that short-term market forecasts are poison and should be kept locked up in a safe place, away from children and also from grown-ups who behave in the market like children. However, it is clear that stocks cannot forever overperform their underlying businesses, as they have so dramatically done for some time, and that fact makes us quite confident of our forecast that the rewards from investing in stocks over the next decade will be significantly smaller than they were in the last.

Much can be learned from this short passage. First, short-term stock market forecasts are, indeed, nearly worthless – essentially a guessing game. Second, long-term forecasts, on the other hand, can be made with ‘confidence.’ “How?” you ask.

It’s actually very simple. Rather than fixate on recent history and extrapolate it into the future you must abandon this natural tendency. And as I said earlier you also need to analyze the conditions that allowed for those returns to see whether they are still relevant to today’s market.

In Buffett’s example he’s referring to the wonderful returns equity investors experienced from 1982-1992. During that span investors roughly quadrupled their money. Over the coming decade they merely doubled their money so Buffett was right that the decade beginning in 1993 would fall far short of the return of the prior decade even if they were still very good.

sc-22

But Buffett made another prescient forecast in November 1999 when he wrote:

Today, staring fixedly back at the road they just traveled, most investors have rosy expectations. A Paine Webber and Gallup Organization survey released in July shows that the least experienced investors–those who have invested for less than five years–expect annual returns over the next ten years of 22.6%. Even those who have invested for more than 20 years are expecting 12.9%. Now, I’d like to argue that we can’t come even remotely close to that 12.9%… you need to remember that future returns are always affected by current valuations and give some thought to what you’re getting for your money in the stock market right now.

You probably already know that stock market returns from 1999 to 2009 were not very kind to investors.

And Buffett tells us how he was so confident that this would be the case. He examined the conditions that allowed for returns to be so wonderful from 1982-1999 but were no longer present in 1999: wonderful valuations. Stocks were so cheap in 1982 that the coming decade was virtually guaranteed to be better than the decade that preceded it. (1972-1982 was another decade that was not fun for investors.) Then in 1999 valuations were so expensive that there was almost no possibility of decent returns going forward.

So let’s take a look at Buffett’s favorite valuation yardstick which he refers to on both of those prior writings. It tracks the total value of the stock market in relation to Gross National Product.

From the chart, it’s plain to see that valuations were extremely attractive back in the early 1980’s. This is why stocks performed so well over the next 20 years. However, I find it absolutely fascinating that stock market valuations today are essentially equivalent to valuations in November 1999 when he wrote that latter passage. Yeah, go back and read that last line again. It’s a doozy and it’s absolutely fact.

This is also why the past 5 years or even the past 50 years are totally irrelevant to equity investors in today’s market. There is almost zero possibility today of achieving a return anywhere close to what those historical returns represent. So shun forecasts if you want. Plead ignorance if it makes you feel blissful. But at today’s valuations you should at least be aware of the fact that it’s exceedingly dangerous to fall into the trap of extrapolating without analyzing.

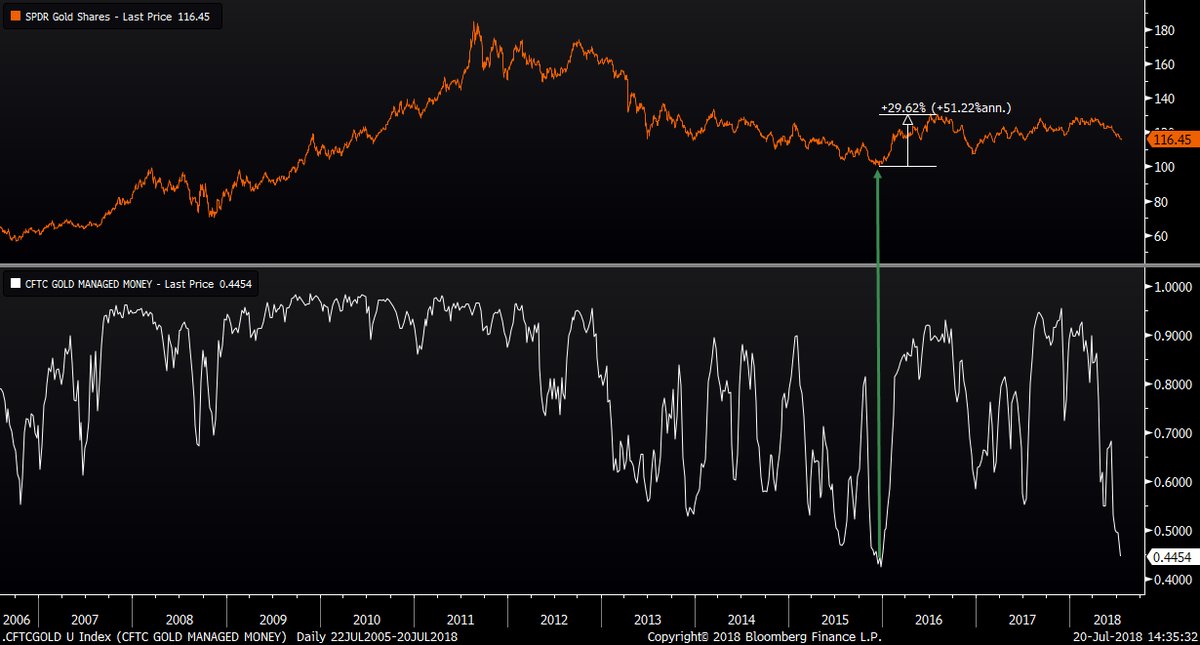

What The Buy-And-Hold Cult Doesn’t Want You To Know

Buy-and-hold, and all of its related strategies like BTFD, garnered a cult following a long time ago and it’s only gotten even more popular in recent years. (There may be no better evidence of this than the StockTwits merch store – which I love, btw). And after one of the longest and strongest equity bull markets in history this should not come as any surprise. Investors are always influenced by recency bias and prone to extrapolation.

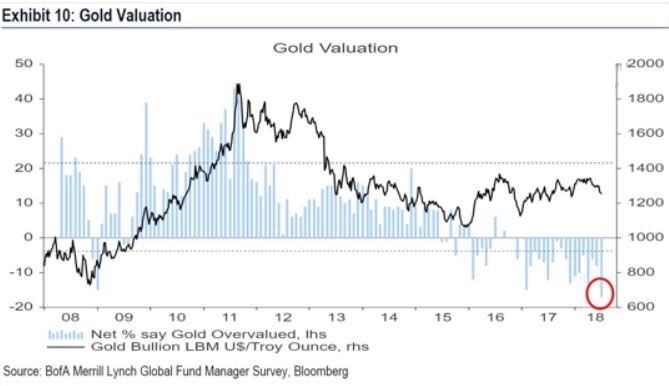

What is surprising, however, is that, despite that fact that it’s long-term (20-year) performance still crushes that of the broad stock market, gold has become so maligned among investors of all stripes, including gold bugs themselves. Yes, the past few years have favored equities over precious metals and I guess that’s where the recency bias kicks in again. But the truth is it has paid far better to be gold bug over the past two decades than to be an equity bull.

The point being to understand your time preference and time reference!

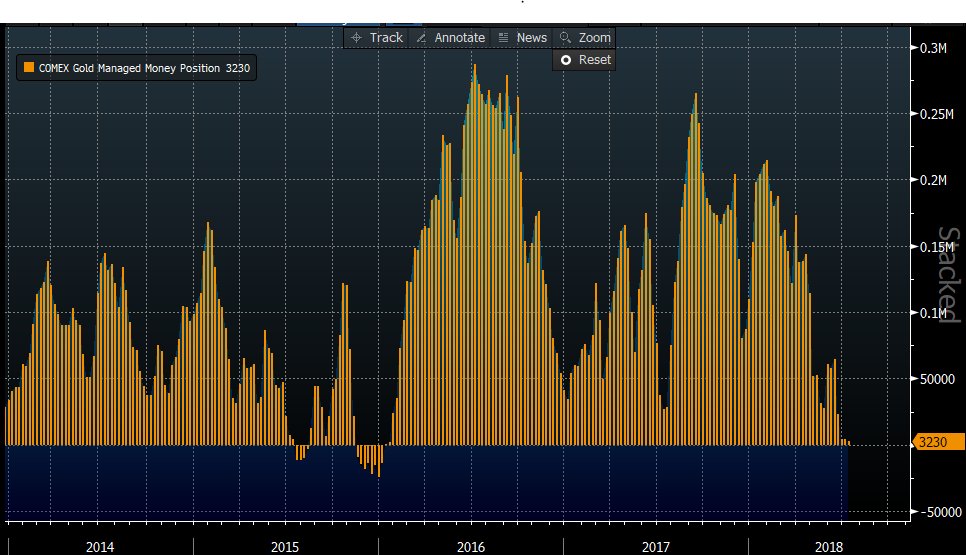

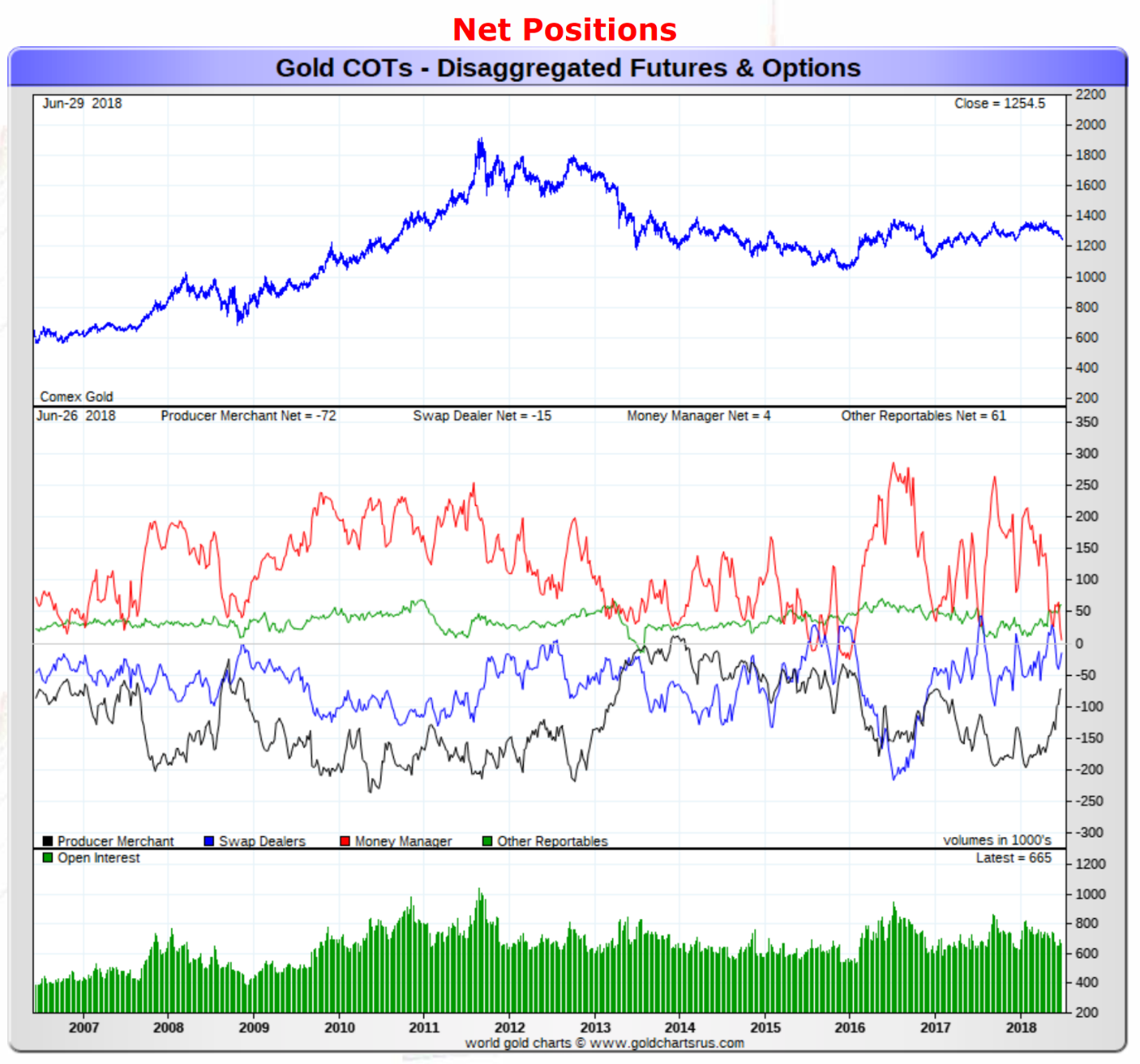

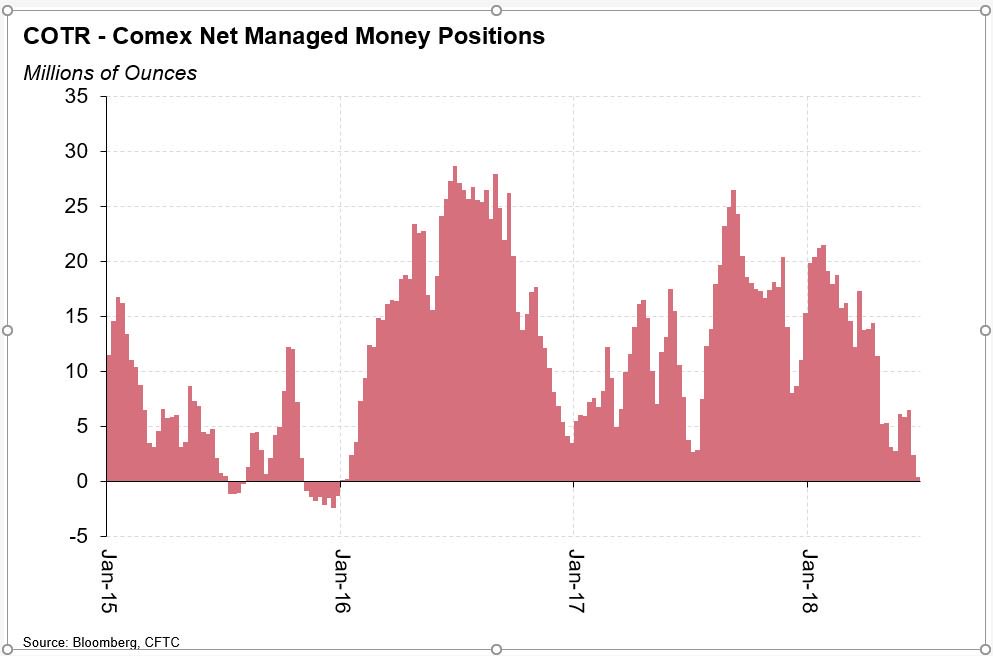

Update:

fred hickey @htsfhickey 20/July 2018 5 PM

Here’s Managed Money(mostly hedge funds) COT details: 134.2K short, 11% higher than highest level (gold’s bottom) seen in 2015, so likely a record.. Net short -26.5k contracts-essentially equal to Dec. 2015 gold bottom. For comparison, at gold’s mid-2016 top they were net 270K long ago

The setup: Gold bugs totally demoralized. Gold sentiment(DSI)down to just 7% with extreme dollar bullishness(92% DSI). Trump beginning to talk $ down (will continue). FY ’19 $1T+ budget deficit. Gold seasonal demand (starts now). Managed Money (hedge funds) net short& have to cover.

It’s likely these are record level shorts. That means there are more shorts than at the bottom in late-2015 – before gold exploded 30% & miners +160% in 6 months and more shorts than at late-2008 bottom before gold soared over 75% in 1 year. Perfect setup-assuming gold’s bottomed.

Whoa Nelly! Just as I suspected it was short traders driving gold down. Thru Tuesday (likely even worse now), a slight increase in longs& another massive 27.7K jump in large spec. futures shorts. In past 5 weeks +121% jump in short contracts to 161K -highest level in at least 11yrs.

BUT, ALWAYS STUDY THE OTHER SIDE–GOLD TO KEEP FALLING.

I am on my knees buying gold/silver/uranium miners with both hand this prior week (ouch!). Since the chart of the futures positions (COTS) is now more extreme–money managers are probably short now like back at end 2015/beginning 2016. I use the blog as a diary/bulletin board on occasion. I hate miners as a business but love the values. Note the vast underperformance of hard (read: miners) vs. financial assets (SPY). Not a recommendation, just a “diary” post.

Buying resource stocks has nearly nothing to do with the commodity. And near zero to do with management or country risk or interest rates or the dollar or what the DOW is doing. Those who are always wrong about markets spend a lot of time mumbling about all those things and they are just wasting ink.

Unbeknownst to GATA or the other PermaBulls who believe some munchkin at the Federal Reserve pulls the levers all of the time, markets go up and markets go down. They all do and they do it constantly. So if someone is telling you silver is the rarest mineral known to mankind and it should go up everyday of the week, forever, he’s lying to you in order to get you to pay for a subscription to his service. In short he’s like a bible thumping preacher or politician, he wants your support, and he specializes in telling you the lies you want to hear.

During the bull phase of the metals markets even the biggest piece of crap stocks go up. During the eventual bear phase of the metals markets even the best run with the most desired commodity in the safest jurisdiction goes down.

So investors in junior resource stocks need to keep two things in mind. You have to trade markets and take a profit when you can or the only alternative is to take a loss. I have had hundreds of investors tell me their biggest mistake was not taking a profit when they could. And given that something like 95% of investors in junior lottery tickets lose money, sell when you can, not when you have to.

You need to align yourself with the phase of the market you are in and let the wind be on your back. We had major lows in 2001 in gold and silver, again in 2008 and late in 2015. Don’t try to second-guess the market. If you were a buyer of anything from 2001 until 2008 you had a wonderful opportunity to profit. If you bought in 2009 or 2016, it was like shooting fish in a barrel. If you didn’t sell in March of 2008 or September of 2011, you got creamed regardless of the merits of the project or company. The phase of the market will either put money in your pocket or extract it regardless of what anyone says about a company.

From: CSInvesting: I have no affiliation with Grants Publication whatsoever, but I am a fan of his work. I post this because if you want access to an incredible library of the past 35 years of financial history, then this is your chance. If you pay $349, ignoring the book and the six future issues, you have access to two issues per month from the past 35 years or about 840 issues at 42 cents per issue. Besides financial data, there are excellent case studies of valuation and financial euphoria/despair.

If you read through those issues (Of course, skimming over articles that don’t interest you.), then you would have the equivalent of an MBA/CFA/PhD in financial history plus a vast course in valuation on certain companies, bonds, and real estate in real-time over more than a third of a century. THIS IS A DEAL! See the offer below

Grant’s versus…

Dear Almost Daily Grant’s reader,

The new edition of Grant’s Interest Rate Observer features a hard look at a zooming stock. The company behind the stock is widely appraised as one of the century’s greatest. Grant’s begs to disagree with that consensus view, as is our wont. Who or what might bring this shooting star down to earth?

Subscribers are also reading about. . .

–the newly crowned holder of the dubious title of America’s most indebted nonfinancial corporation. Would you buy these bonds? Your insurance company probably is.

–one of the few North American industries where value–and bearishness–abounds.

–a pair of struggling foreign debt collectors who may soon be getting a taste of their own bitter corporate medicine.

–a certain Asian behemoth which has managed to spawn a money supply nearly as large as that of America and the eurozone combined.

All this, plus an inspiring Fourth of July quotation by Thomas Jefferson, awaits you.

Sign up today for a trial subscription: six issues, access to the 35-year Grant’s archive and a signed copy of Jim Grant’s latest book, “The Forgotten Depression: 1921, The Crash That Cured Itself,” winner of the 2015 Hayek Prize, all for just $349 ($359 outside U.S. and Canada).

Click Here to begin a six-issue Trial Subscription to GRANT’S. This offer ends MONDAY, July 2, 2018.

Up close and personal interview with Kevin Clayton, CEO of Clayton Homes, the largest factory built homebuilder in the United States and a wholly owned subsidiary of Warren Buffett’s Berkshire Hathaway. For nearly one hour, author Robert Miles interviews Kevin Clayton and covers all aspects of the business from getting started, to taking over from his father, and to selling to Warren Buffett.

This video may help the viewer understand the qualitative aspects that Warren Buffett may consider when making an investment. This interview may also showcase one of the eventual successors to Warren Buffett.

Better yet, view Ken Langone’s interview below: All his investment successes came from investing in good people

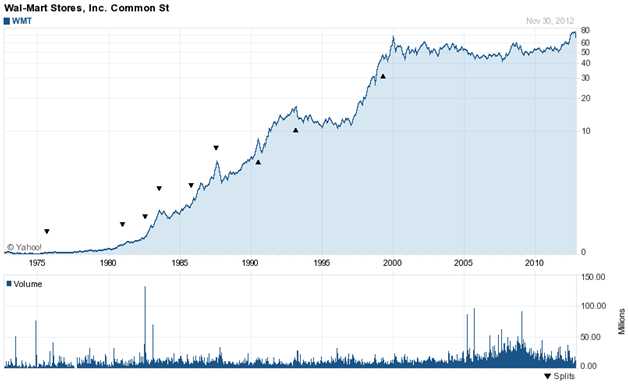

From Best to Worst. There are typically two ways to make 100 to 1 on your money. 1. The preferred way–in my view because the company has more control of its destiny–would be to invest early in a high ROIC company that can redeploy capital at high rates for MANY years.

Note how the chart has gone sideways for 18 years as the ability to redeploy at high rates has declined. WMT can’t grow with regional economies of scale in Germany as it could in Arkansas back in 1965. You have to hold on through the inevitable 50% price plunges which you are able to do because of your understanding of the company’s competitive edge in the market.

2. Or, you find an extremely cheap, beaten-up cyclical company (TECK) in an industry that has had low capital investment, then hold on for the boom which you then sell out at the top–harder and more nerve-wracking than the example above.

The worst performing sectors are where you want to look, but realize that some industries like phone companies may be under structural change.

The Anthesis of Out-of-Favor

The Psychology of Sales

Hedge Fund Pop Quiz (Accounting)

Why is EBITDA so different than operating cash flow? Is that a problem or an opportunity. See: WTTR Mar 31 2018