Investors have put their faith not in a fact but in a concept. As my friend John Mauldin puts it, “Faith in central banks today is equivalent to faith in the word dot-com in 1999 or faith in the eternal rise of housing prices in 2006.” No doubt, Warren Buffett was right that “a pack of lemmings looks like a group of individualists compared to Wall Street once it gets a concept in its teeth.” But QE is also a concept that is rather fully played out, especially with a likely tapering ahead. Notably, the shift toward tapering is not driven by substantial economic improvement or victory of the policy, but rather by an increasing recognition within the Fed itself that its actions are creating dangerous financial distortions.

www.hussmanfunds.com

Hundreds of Video Interviews with Klarman, Buffett, and new Fund Managers through the Manual of Ideas. For more videos click on the manual of ideas link at the top of the page in the link below:

There are hundreds of short videos on value investors. If you find any that are particularly enlightening, interesting, or helpful, let me know so others can see it.

Economic Calendar by Yahoo!

This is a great calendar of past and upcoming economic announcements, including both actual and expected results.

www.wetfeet.com

This site is a great resource for students seeking either an internship or a job. The site provides descriptions of various careers and positions in finance, interviewing questions and tips, profiles of firms, job listings, etc.

www.vault.com

Vault.com is another source for career and internship information. Under the internships section, it provides “a day in the life” descriptions for several careers. It also provides job listings, interview questions, and interviewing advice.

www.careers-in-finance.com

Check out this site for descriptions of various careers in finance and for a very useful set of books and references related to finance jobs and interviewing tips.

RISK: My grandfather invested his fortune in Russian bonds. This was before the Russian Revolution. At the time, he was told he couldn’t lose money. Because the bonds were pegged to gold. So there was no currency risk. And these were bonds of Russian railways, which were the most solid businesses in the world, and they were guaranteed by the Tsarist government. No currency risk. No default risk. No business risk. They were as close to risk-free as you can get. But when the Bolsheviks took over they seized the railways. They stopped paying the bonds. And they executed the Tsar and his family.”

It didn’t make any difference if the bonds were pegged to gold or not. They were worthless. It just reminds you of how things can go very bad in a way you don’t expect. Who would have imagined a communist revolution in Russia? (Could a Dictator take over the U.S.A.?) www.acting-man.com

The letter alone is quite amazing. In it, Buffett identifies the pension problems that others would key in on only a decade or so later. But he also lays out perhaps for the first time — Buffett was 45 when he wrote it and years away from attaining the investment fame he has today — his philosophy behind what it takes to be a successful investor. His main pieces of advice: Think like an owner, look for a discount, and be patient. Full article: http://finance.fortune.cnn.com/2013/08/15/warren-buffett-katharine-graham-letter/?iid=EL

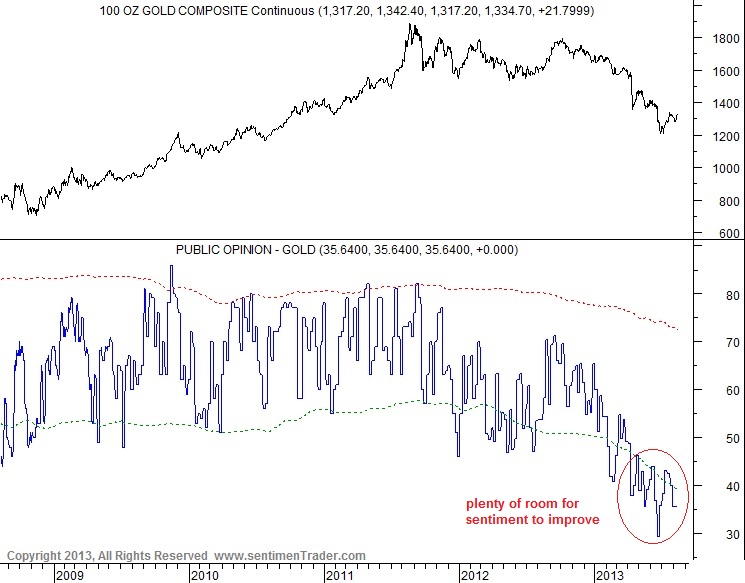

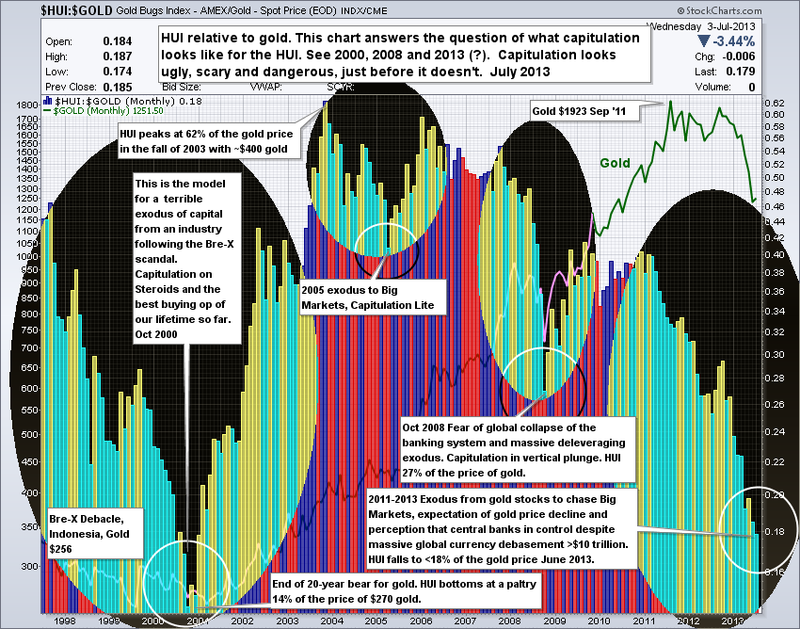

Gold and Gold Stock Capitulation (GLD represents gold while GDX represents an index of major gold producers and GDXJ represents junior gold miners). Note the date of the low prices in End June/Early July. We last mentioned capitulation here: http://wp.me/p2OaYY-25W

Today news hit that John Paulson has finally sold a big chunk of his position in GLD. It is not terribly surprising that this happened in the quarter when gold made its low. After Paulson sold his holdings in bank stocks, the group soared, with many of the stocks he had sold at the lows rising by 200% and more thereafter. However, this time it has probably less to do with his bad timing, but very likely more with the bad timing of investors in his funds. As the Bloomberg article mentions:

“Paulson & Co., the largest investor in the SPDR Gold Trust, the biggest exchange-traded product for the metal, pared its stake to 10.2 million shares in the three months ended June 30 from 21.8 million at the end of the first quarter, according to a government filing yesterday. The New York-based firm, which manages $18 billion, cut its ownership for the first time since 2011 “due to a reduced need for hedging,”according to an e-mailed response to questions.”

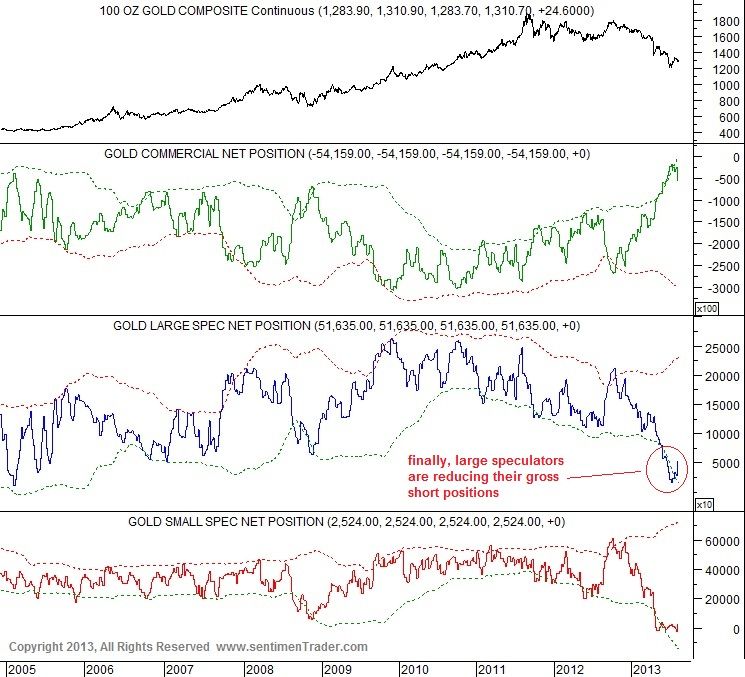

CSInvesting Editor: As mentioned before, I have been unable to find attractively priced franchises so in the past four months I have bought “quality” miners and related companies like RGLD, SLW, FNV, AUY, AEM, NGD, EGO, etc. I place the word, QUALITY in quotes because those companies are not franchises and each struggles with the cyclical risks of their product–metals. So beware, I am biased to seeking out information that bolsters my bullish outlook like Commercial Hedgers having a low short position:

and extremely negative speculative sentiment–a contrary signal.

And….

A very seasoned mining executive I’ve known for years (www.grandich.com) sent me the following email, along with the latest World Gold Council report. He made a very keen observation is his email. Here it is:

“As an aside FYI, attached is the WGC’s first ½ 2013 report – skip to page 14 and look at the highlight yellow I put in. Of ~2000 supply and demand tonnes , ~578 tonnes are sold by ETF’s. If ETF’s sales were zero there would be a 29% supply shortfall. Total mine production is 1377 tonnes, ETF’s sold 42% of all mine production first ½ this year. My math is that if the ETF’s get cleaned up and go to 0 sales, we are looking at quite a gold supply problem. Old fashioned thinking I know, but alas, I am just a simple guy.”

We have a very serious mine production shortfall that has been masked during the gold raids and sell-offs. I think it will get exposed going forward.

—

I need evidence against my thesis, so please send any negative information against owning precious metals miners and gold. I am reading:

Next week, I will post a valuation on Royal Gold (RGLD) so get a head start and visit the websites of Franco-Nevada (FNV), Silver Wheaton (SLW) and Sandstrom Gold (SAND) to learn about this business.

Marty Whitman is an asset based investor who prefers safe and cheap. Unfortunately, the 2008/2009 crash put a dent in his mortgage insurer stocks which turned out to be neither safe nor cheap. Third Avenue Value Fund (TAVFX) tumbled 63% in a year. Humbling.

A respected value investor, Martin Whitman, is going toe-to-toe with another well-known value investor, the hedge fund manager William Ackman, over the future of the bond insurance industry.

Mr. Whitman, founder and co-chief investment officer of Third Avenue Funds, increased his holdings in the two largest bond insurers — MBIA and the Ambac Financial Group — during the fund’s first quarter, which ended Jan. 31. He also increased his stakes in the mortgage insurersMGIC Investment and the Radian Group.

In doing so, Mr. Whitman, has, in effect, put his reputation up against that of Mr. Ackman, whose big bets on share price plunges in the industry have received wide media attention.

There is “much profit to be made in” the bond insurers, whether the companies continue as going concerns or write no new policies and sell off their existing business, in part or in whole, Mr. Whitman said in a letter to fund shareholders.

The 82-year old Mr. Whitman devoted a substantial chunk of the letter to defending his MBIA stake, saying that the company appears to be “very well financed” — a claim William Ackman has disputed vigorously.

Mr. Whitman, who has made a name by buying assets most other investors shun, in January increased his stake in MBIA, the largest bond insurer, at $12.15 a share and now holds about 10 percent of its outstanding shares. Third Avenue also has bought $326 million of the $2.6 billion MBIA has raised in new capital through note sales, which Mr. Whitman said made the company “strongly capitalized.”

“It ought to qualify easily for an AAA rating with a $17 billion claims-paying ability. If so qualified, MBIA would be in a position to underwrite a large amount of profitable new business,” Mr. Whitman wrote in the letter.

But Mr. Whitman noted that among the impediments that might prevent MBIA from winning a stable outlook was the possibility that Mr. Ackman might adversely affect the company.

Mr. Ackman, who has been shorting the bond insurers for some time, has argued that they do not have enough capital to handle a surge in claims.

“MBIA is being victimized by an apparently well-organized bear raid headed by William Ackman of Pershing Square Capital Management,” Mr. Whitman wrote.

Mr. Whitman said that while Mr. Ackman’s bearish views had made it possible to buy MBIA at depressed prices — he noted that the common stock of the four companies has been selling at discounts of about 70 percent from tangible book value — his arguments are “off-base.”

“Ackman believes the bond insurer model does not work because the insureds are able to buy an AAA rating so cheaply,” Mr. Whitman wrote. “The facts are that bond insurance is one of the more profitable P&C businesses.”

Mr. Whitman has proven a master at turning debt bought at distressed prices into something far higher value. For example, he paid about $10 a share for Sears Holdings, some of which he later sold at more than $130 a share and higher.

In 2002, Ackman began research which concentrated on challenging MBIA‘s AAA rating, despite an ongoing probe of his trading by New York State and federal authorities. He was charged copying fees for copying 725,000 pages of statements regarding the financial services company, in his law firm’s compliance with a subpoena.[6] Ackman has called for a division between MBIA’s bond insurers’ structured finance business and their municipal bond insurance side, despite statements from the insurance companies that this would not be a viable option.[7]

He argued that the billions of dollars of CDS protection MBIA had sold against various mortgage backed CDOs was going to be a problem. He also argued that it was not proper for MBIA, which was legally restricted from trading in CDS, to instead do it through a second corporation, LaCrosse Financial Products, which MBIA described as an “orphaned transformer”. Ackman bought credit default swaps against MBIA corporate debt as a way to bet that it would crash. When MBIA did, in fact, crash as the financial crisis of 2008 came to a head, he sold the swaps for a large profit. Ackman reportedly attempted to warn regulators, rating agencies and investors about the bond insurers’ high risk business models. The story of Ackman’s battle with MBIA was turned into a book called Confidence Game (Wiley, 2010) by Bloomberg News reporter Christine Richard.[8] He reported covering his short position on MBIA on January 16, 2009 according to the 13D filed with the SEC.[9]

—

Bill Ackman is a “slick salesman who does not know much about insurance and certainly doesn’t know much about restructuring secure debt”

If you said Carl Icahn you are incorrect.

The previous statement was made by Mr. Martin Whitman – octogenarian and Chairman of Third Avenue Funds Inc.

During the financial crisis, Bill Ackman was short MBIA. Mr. Whitman took a large long position in MBIA and Ambac after the stocks dropped in the crisis and after Mr. Ackman revealed his short. Not only was Mr. Whitman determined to state that MBIA was worth $35 per share, but he also made particular efforts to insult Mr. Ackman’s research efforts and intelligence.

This article on Dealbook summarizes some of Mr. Whitman’s arguments.

What can we learn from this history?

1) Both parties were convinced they were correct.

2) Both parties took significant stakes in the company in question/backed-up their trades.

CSInvesting: So what are the lessons for us, the mortal, individual investors?

First, anyone and everyone can err. Don’t rely on a guru. Do your own work.

Second, financial firms can be laden with unforeseen risks based on their dependence on outside capital and ratings.

Third, Mr. Whitman underestimated the amount of bad debt and the quality of the assets that the mortgage insurers insured. Knowledge of the Austrian Business Cycle Theory might have helped.

Ackman challenged the conventional wisdom and saw the flaw in the ratings game.

You may not love financial history as much as I do, but you will enjoy reading about the following themes:

The characteristics of winning and losing speculators

Wall Street during periods of war

How operators attempted to “corner” the markets for individual stocks

The causes and consequences of Wall Street panics

The influence of Wall Street on national politics

How individuals like Jay Gold, Daniel Drew, and Commodore Vanderbilt made their fortunes.

Book: Fifty Years in Wall Street (1859 to 1900) https://www.hightail.com/download/bWJxTG05R0Z1Yk5Yd3NUQwThanks to a generous contributor. The book is worth reading for a feel of Wall Street during the 19th Century and for learning that human nature does not change especially on Wall Street. Add this to your Reminiscences of a Stock Operator from the last post http://wp.me/p2OaYY-26h. You now have reading material on Wall Street (1850 to 1930) from the speculators’ point of view. Place this in your financial history section of your learning library!

Ok, I am burnt out on Buffett! And, I don’t think this is the best book on Buffett–better to spend the time on Snowball(soon to be posted), but I don’t censor, I leave it up to YOU, dear reader, to decide. See Amazon Review below:

A review: I was very much looking forward to this book – to be able to read a comprehensive and organized treatise on Buffett’s many philosophies and strategies. What a disappointment!

Be warned that the book is nothing but tidbits and random bits and pieces of articles written about him (and a few by him) over the last 46 years.

But don’t expect to learn anything you probably already didn’t know.

Any normal person wanting to learn about what really makes this man tick, and what his investing philosophies and strategies are, would do better to read Alice Schroeder’s comprehensive and impressive biography of Buffett – “The Snowball.”

—

I received the dropbox keys to a treasure chest of 80 books so I will parcel out over the next few weeks.

If you find any books that helped you become a more insightful investor, then please let me know so I can share with the group. Thanks.

Editor: It seems as though the traffic crashed the links, so I will need to find another storage/sharing method. Patience while I work on it.

This leads me to wonder if starting a private web-site/blog with a csinvesting analyst manual would be an improvement. A person could have a book with links to videos/case studies and books in an organized fashion to become a knowledgeable investor–more learning materials than any other web-site/university times ten! Imagine a private library/study area/discussion lounge for learning value investing. The site could be self-sustaining with a nominal fee per annum. It would weed out the people who are not very committed.

Also, sharing info would be easier. Thoughts for the future………

Meanwhile I will try to find another way to share those books.

In the absence of the gold standard, there is no way to protect savings from confiscation through inflation. There is no safe store of value–Alan Greenspan

Pop Quiz:

Do you think the U.S. Gold price will go up to the moon as inventories of gold bullion drop? Will there be a short squeeze? If inventories drop it means demand is going through the roof and the price will soon follow? Go to www.kingworldnews.com to see this argument used/hawked as a bullish case for gold.

What do you think of this argument? How is gold different than copper, oil or steel?

What happens when 63.5K ounces of registered gold in your warehouse (16% of total) just has their warrants detached and the vault is about to finds itself 63.5k ounces of gold emptier? If you are JPM you call the gold vault with most inventory in town, that of HSBC, and politely request that they transfer as much eligible gold as they can on short notice – in this case a tiny 6,444.936 oz to be exact.

None of which changes the fact that in a few days, the inventory in JPM’s gold vault will drop to another record low of only 380K ounces and the JPM “rescue” pleas from HSBC and other Comex members will become ever louder and more desperate until one day they may just go straight to voicemail.

QUIZ: Discuss in a few words the mistakes made in these recent acquisitions in the newspaper business. If you wanted to develop an advantage in newspapers how would you do it. (Hint: What is the most profitable news magazine in the world–or close to it?)

How would you advise Bezos to enhance his purchase of the Washington Post?