A reader asked me via email about what books to read to understand history.Please post your questions in the comments section because I most likely will lose your email–let others see your thoughts.

Then read Wall Street, A History by Charles R. Geisst.

That will get you started. Don’t forget to read more general history as well such as The Rise and Fall of the Third Reich-the mother of all bear markets for the human race. Couple that with Winston Churchill’s books on European history and WWII for another perspective.

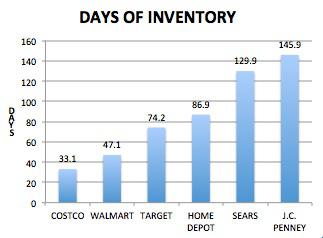

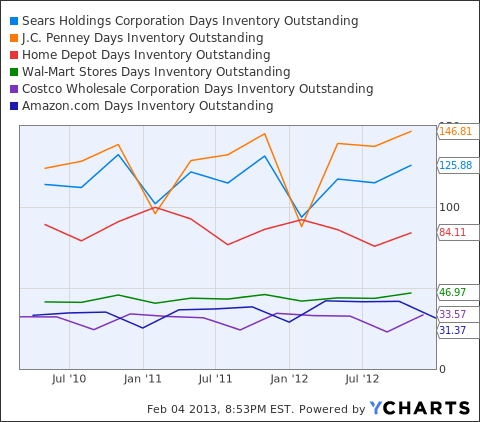

Here is a good article that captures the problem at JCP. Essentially a retailer owns or leases space to sell goods to customers. The wider the mark-up and/or the faster the turnover of goods, the greater the profits, return on capital, etc. JCP HAS to get customers in the door AND then get them to buy–obviously. I don’t agree on all the comparison (Costco vs. a Dept. Store) in the graphs, but you get the picture.

(Days of Inventory = Inventory/Cost of goods x 365 days. Data courtesy of Morningstar.com in TTM time frame.)

Any slower inventory management and Penney and Sears might as well advertise in Frommer’s Guide to museums.

Make no mistake: Sears (SHLD) and J.C. Penney (JCP) act more like museums than retailers. They’ve become simply corridors to get to the rest of the mall. The tip off: The two can’t unload their inventory. Goods move at a trickling pace and it’s killing the bottom line.

Check the length of time it takes these brick-and-mortar retailers to move their goods: Costco (COST), Wal-Mart (WMT), Target (TGT), Home Depot (HD), Sears and J.C. Penney. The chart shows how long it takes to turnover inventory. The longer the days of inventory, the longer dollars are tied up.

JCP dropped below $17 for about a 20% decline. More than 15% of its float has traded in less than 24 hours. 30% of the float is short.

Where to find maximum pessimism and hatred:

Here are the headlines.

“Simply stunning results” from J.C. Penney (JCP), says Tiburon Research’s Rob Wilson, quickly…

Wednesday, February 27, 4:58 PM ET

Sales Sink, Stock Gets Hammered in After-hours Trading (Reuters)

Feb. 27, 2013, 4:44 PM More on J.C. Penney’s (JCP) Q4: No sigh of relief for investors just yet as the firm reports comparable store sales fell 31.7%, below the consensus call of -26.9%. Customer are fleeing, but no give up from CEO Ron Johnson: “…we are energized by our shop roll out plans.” Gross margin was crushed, falling to 23.8% of sales vs. 30.2% last year. Internet sales slumped again, losing 34.4% Y/Y just marginally better than last quarter’s 37% nosedive. Cash position $930M at end of Q4. No guidance is issued, but the retailer says it will open 20 shops geared toward home products in 505 stores with brand partners. JCP -4.4% AH. (PR) Read comments

· Shareholders need to revolt aggressively (Yahoo poster 6 PM 2/27/13)

The Board needs to fire Ron Johnson tonight. They need to then hirte a trustee to rebuild it and then resign en masse for hiring this imbecile. First rule of retail: Don’t f it up! Kill the BOD and Johnson NOW.

Ron Johnson couldn’t sell pus*y to a troop train. How many times will we sell retailers fail due to hiring rock star leadership who is so arrogant to turn away from the existing customers without attracting any replacements? Just desserts Ron. Eat #$%$. Ron is a $%^&*! piece of $%^&!

Where is the class action shareholder lawsuit ? Will RJ fly home tomorrow on the corporate jet ? Will he still be racking up insane bills at the Ritz ?

—

Can you feel the love? Yes, investors are upset, but do you read any deep analysis as to the value of the company?

What happened in this situation–Dillards (DDS)? Perhaps a case study is in order. Ron Johnson is a genius at $40 and now at $17 he receives death threats. I have never seen a turn-around take less than 36 months. Let’s check back in 2014.

Dillards monetized some of its real estate assets through a REIT.

I am not implying that JCP should do the same, but I recon there is a reason JCP has not dropped below $14 per share even in the dark days of 2009. Can the massive hate and fear take us to new lows? Not, if it doesn’t happen in the next month.

Curious to know where you think this flagging market is heading from here. I’m content to sit on the sidelines and watch a little longer.

My reply: The only idea more frightening than someone believing I know where the market is headed, would be if I believed I could predict the market. Predicting the market which is a complex adaptive system falls into the area of important but unknowable.

A complex adaptive system is an open, dynamic and flexible network that is considered complex due to its composition of numerous interconnected, semi-autonomous competing and collaborating members. This system is capable of learning from its prior experiences and is flexible to change in the connecting pattern of its members in order to fit better with its environment. No wonder that neither mathematical formulas nor science can capture or predict human action. I think Ben Graham said roughly in these words, “Don’t confuse fancy math for thinking.”

As a reader recommends:

No need to predict the market

But an investor doesn’t have to predict, he or she has to find lopsided bets or “value.” I try to buy franchise companies–those with competitive advantages evidenced by steady market share and high returns on ivested capital over time–usually a ten year time period. These companies are rare but obvious like Coke, Novartis, General Mills, Stryker, Exxon, etc. The issue is what price to pay. Two years ago, several franchise companies were trading at or below the average company; they were bargains. Why? Perhaps because prices adjusted from the over-valuations of ten years ago (Coke being an example). Most of the time you track these 80 to 140 companies and wait for a sale to occur during a market downturn, “missed” earnings report, product recall or some temporary problem.

You also need to be aware of companies that can become franchises or can dominate a niche–Autozone, WDFC, and Cell Tower Companies, etc.

Then you have special situati0ns where there is some event to unlock value–SHLD spinning out SHOS, for example. the stock is up 50% in three months, so opportunity is everywhere.

Look for where the fear is greatest or where there is MAXIMUM PESSIMISM

Even with the “market” flirting with new highs, you have segments like junior mining c0mpanies (GDXJ) making new multi-year lows as people throw in the towel after years of disappointing returns. Usually, the problems are well-advertised–Mining companies are losing speculative buyers to ETFs, costs are rising faster than revenues, capital is scarcer, companies have misallocated capital in the quest for size, stocks are back to where they were five years ago but the gold price has doubled–and known. A mining company is a hole in the ground with a liar on top, so you better be careful if you wish to pick through the debris or just ignore and look elsewhere.

Focus on the particular

So who cares where the market is going? Focus on particular companies and where the fear, disgust and neglect are greatest. Unfortunately, for me that appears to be the precious-metals mining sector. If I can find several free call options on gold and silver, I will buy as long as I don’t over concentrate. Pray for me.

Pundits

Another trick is to ask yourself why the pundit on CNBC is sharing their prediction of where the market is going. Why tell?

As the two-penny philosopher once opined, “There are many who don’t know that they don’t know while those that know, don’t say.”

Understand the manipulation of hampered markets

That said, this writer suggests any investor go to www.mises.org and download the free books there and understand the Austrian Business (Trade) Cycle. There are huge misallocations of capital going on now, so be prepared.

Jim Grant on our current situation

Listen to what Grant’s has to say about the Fed and the money madness.

I’ve been using eBay to buy designer clothes now for around 7-8 years, since the end of High School. It started out because I didn’t have a lot of money, was dissatisfied with the in store prices on back-to-school shopping, and was (and still am) somewhat vain. So I took to the internet to do shopping, but still was dissatisfied at the lack of quality bargains. After a while of searching for deals at traditional online retailers, I came across eBay and I found a treasure trove of bargains on gently used, mid to high-end designer apparel, items marked down substantially from their MSRP because of depreciation and the “social repulsiveness” of buying used clothes (this may have changed recently with the popularity of http://youtu.be/QK8mJJJvaes/). Since then I’ve been able to do substantially all of my clothes shopping, for school and now work, on the internet, while saving enormous amounts of money. For example, I got very lucky with the fit and bought my suit for ~$20.00-30.00 (I can’t find specific pricing information on this purchase at the moment). This would have easily cost hundreds of dollars if I had bought it off the rack and gotten it tailored. Additionally, I’ve bought everything from designer label jeans to dress shirts, polos, shorts, and pants for well under $50 a piece.

For those interested, some general rules I follow are:

Don’t buy anything that you don’t need. It can be tempting to spend hundreds of dollars on bargains, but it’s not worth buying something you’re not going to get much wear out of

Know what your measurements are before you buy anything. Most of the time sellers will post the clothes measurements for comparison purposes

It’s important to pay attention to the seller’s return provisions to make sure it is refundable if the item doesn’t fit/isn’t as advertised

Set the maximum price level you’d be willing to pay in your mind and stick to it

Be willing to walk away from items that exceed your price threshold

Stick to US sellers to reduce the likelihood of buying counterfeit goods and to save on shipping & handling

I got burned on this one a couple times before I changed my ways

I try to buy clothes that aren’t too trendy or high end, because they’ll likely go out of style in a couple years and I won’t be able to get as much wear out of them

I am ashamed to admit that I once bought a bunch of Ed Hardy stuff (pre-Jersey Shore, but still deplorable) that is now collecting dust in my apartment

This works for me because men’s sizing doesn’t vary that much between brands, but it will be much harder for girls because of the greater sizing disparity in women’s clothing between brands

When I first started out doing this, I would get extremely frustrated that whenever I would put a bid on an item, someone else would undoubtedly come along and top it. This cycle would repeat until the item would approximate fair value and I would either throw in the towel or be left paying much more than I intended. I began looking for ways to work around this and I came upon Auction Sniper (http://auctionsniper.com/). The best way to describe this service is high frequency trading for eBay auctions. For a ~1% fee of the final purchase price (only if you win), you can plug in information on an item along with your bid well before the auction’s end and they will actually place your bid mere seconds before the end (I use a 3 second lead time). This allows you to fly under the radar and get your bid in close enough that if you are the highest bidder, no one has a chance to top it. Additionally, this service helps you maintain pricing discipline because you’re not anchoring your bid to incrementally higher prices. And, it also gives you some peace of mind to go about doing more important things with your life instead of obsessively checking the item listing to make sure you are the highest bidder.

Additionally, I am a relatively small guy (big where it counts) and I’ve found that a number of designers have clothes for their children’s lines which are identical in appearance to those of their men’s lines. While nearly the same thing, the children’s item will be priced meaningfully lower than the men’s item at the retail level. If you can find items like these, in a children’s large or extra large size, you can take advantage of both the inherent MSRP discount and any discount that you can get by buying on eBay. For example, I bought my gray Ralph Lauren half zip sweater (children’s large) that I wear to work every week for $0.99 (excluding shipping & handling). As a point of comparison, this item’s men’s line equivalent has a MSRP of $115.00 and is currently “on sale” for $69.99 (http://tinyurl.com/a4qwryn/). Of course, this strategy isn’t for everyone and will only work for guys who are sub 5’9” tall generally.

Where I’m Currently Looking:

My favorite areas to look into are where the seller has a much lower cost basis (preferably $0.00) in the item relative to the MSRP. Most of the time this is difficult to determine, but if you can find items like this, they provide worthwhile buying opportunities. My assumption is that these arise through some combination of the seller receiving items for free, the seller getting a meaningful discount elsewhere on the item, and/or lack of comparable pricing information. From the beginning of an auction, these items will be priced at a very low level with few, if any, bids. I’ve been capitalizing on this for a few weeks, as I’ve recently gotten a new job which requires me to buy more formal office attire. Specifically, I’ve been looking into picking up some Vineyard Vines ties (this comes from living in the company’s backyard). I’m on the hunt for their custom collection ties, which are made specifically for a company/organization and usually have the latter’s logo displayed on them in a repeating pattern. What I’ve observed is that these are significantly underpriced compared to the regular men’s line on eBay, as (my assumption) the seller likely gets them for free and will profit at any price in addition to there being a narrow market for such an item. While I have no intention of wearing a tie that has “General Electric” or “Morgan Stanley” plastered all over it, I have found a few with generic enough looking patterns, whereby you’d be hard pressed to tell that they were made for a specific company unless you had worked there. So far I’ve been able to pick up a couple of these ties in excellent condition for ~$15.00 each (including shipping & handling). This compares to a $75.00 MSRP for Vineyard Vines ties (excluding shipping & handling), which amounts to a savings of around 80%.

While buying clothes on eBay may not be for everyone, in addition to getting great deals, it is a lot of fun. Maybe I’m weird, but nothing feels better than the knowledge you bought something at the price it cost the company to make it. I hope that I have provided people with useful information they can use the next time they think about making a shopping trip to somewhere like JCPenney or Sears.

Also, I do work currently in investing and am looking to actively network with others in the industry. If you are interested, my email address is mcg881@gmail.com.

—–

Analyst Jobs:

Please check the Job Vault on SumZero.com for details or email liz@sumzero.com. All inquiries and applications are treated with complete confidentiality. Also, email liz@sumzero.com if you would like to post a job opening with your firm and work with SumZero.com on finding buy side candidates to fill a role.

Jr Analyst – China Internet Coverage (Fluent Mandarin Required) – Long/Short Equity Fund – NYC

Jr Analyst – Event Driven Equity/Credit Fund – San Francisco

Jr Analyst (Pre MBA Role) – $3Bn + Multi Strategy Fund – NYC

Event Driven/ Multi Strategy Credit Analyst – Multi $Bn Hedge Fund – Chicago

Over the years, I’ve found that to understand social mood extremes has helped me identify and profit from market turning points, when used in conjunction with the Elliott Wave Principle and other technical analysis. At the 2000 and 2007 tops in developed stock markets, of course, there were plenty of socionomic clues.

I’d say the AOL/Time-Warner merger was one of the best, at the 2000 top. For me, it crystallized an extreme herding point of belief in new technology. In the run-up to the 2007 extreme, in 2006 in the UK, [lenders introduced] a mortgage loan that was dubbed “the mortgage that never dies.” The borrowers needn’t repay the loan and could simply pass it down to their children when they died. I remember thinking that such a manic belief in house prices and credit was just so extreme. Even compared with all else that was happening then, that was one of the all-time best examples of what extremes in social mood can produce. (Source: The Social Mood Conference)

So begins my analysis of Dell. Please be aware that I have been a recent shareholder of Dell, but no longer own shares. These comments should be taken in context of potential self-serving, hindsight bias. My methods may or may not be applicable to your investing, but I will lay out my assumptions.

First, I look at Dell_VL_2013. I love Value-Linefor all the historical information that it packs into one page. However, I use it for a first screen and as a tickler to focus my reading when I go to the proxy and annual reports. Next, I go to the history of Return on total capital (“ROTC”) and ROE. In 2002 Dell had almost a 40% return on total capital averaging close to 50% until the plunge down to 17% in 2009—not unexpected given that computers could be considered a capital good. Use of debt was minimal.

My eye notices that ROTC has not really recovered to the pre-2009 glory days and now averages about 14%, a normal return on assets for an average business. Having read about Dell over the years, I know Dell had a business process advantage. Dell had a lower cost structure in computer assembly and distribution over its competitors. If you go to www.hbs.org you can download dozens of case studies on Dell’s manufacturing advantage. The market and competitors changed. Dell lost its cost advantage RELATIVE to its competitors. Now Dell is a commodity business. The proof lies in the history of its ROTC.

Next, I see sales growth per shareabout quadrupled from 1996 to 2000 during the Internet boom/bubble before flattening out at a ten-year 5.2% compounded annual growth rate from $35 billion in revenues in 2002 to about say $57 billion estimated in 2012. Wow, a big sales deceleration.

Dell has been buying back shares continually since 2001 both to sop up option issuance and shrink share count. My eyeball says management started shrinking the share count by 900 million shares from 2001 at an average price of $25—almost 90% above Dell’s current $13.65 offer. Dell’s management spent roughly $22.5 billion on share buybacks. The shareholders who remain sit with a current market cap at $24 billion (1.73 billion outstanding shares times $13.7 current share price). The shareholders who sold are the ones who benefited while the long-term and long-suffering shareholders saw the firms capital squandered.

If Dell’s management destroyed capital buying their OWN company, what does that say about their ability to make acquisitions outside their area of expertise going forward? I wonder….?

I jump to Dell’s proxies:2012 Dell Proxy and 2010 Dell Proxy. Michael Dell already owns about 13% of Dell which I don’t begrudge him since he did create the company and develop a better way to assemble and distribute than his competitors, for a time.

But why does he receive a dollop of 500,000 options every year? How does receiving more options incentive him more than his 13% stake and on top of his generous salary? My prejudice is that Mr. Dell looks out for number one first and shareholders second. I think Dell comparing itself to Intel in its peer group is absurd. Intel has to spend much more on R&D, for example, than Dell. They are different businesses. Dell’s compensation plan has the makings of fancy consultants. Read more on M. Dell’s compensation: http://www.footnoted.com/perk-city/dells-tale-of-two-proxies/

I’m proud to report we delivered on that promise in fiscal year 2012. We made big investments to expand our portfolio of solutions and capabilities and to build an expert global workforce to deliver them to our millions of customers. By the end of the year, enterprise solutions and services accounted for roughly 50 percent of gross margins—a record result, and great validation that we’re on the right road and delivering the technology solutions our customers need.

I am excited about our future. Information technology is a $3 trillion industry, and we currently have roughly a two-percent share. The opportunity to grow and, more importantly, to help our customers achieve their goals is tremendous. That is—and will always be—our ultimate goal.

That ladies and gentlemen is called the “Chinese Glove Theory.” If I can garner 1% of the Chinese Glove market by getting 1% to 2% of the 2 billion Chinese to wear one glove (like Michael Jackson), we will be rich. Of course, what edge do I have and/or profits will be made doing that relative to competitors?

Ok, Dell has made big investments to grow but how does Dell have a competitive advantage in any of its businesses? If I can’t answer that question—and I can’t—then Dell’s GROWTH has NO value, zilch, nada, none. Returning money via dividends and share purchases is good provided the company shrinks itself faster than the decline in its business or does not squander its cash with overpriced acquisitions or share buybacks.

Note the average annual P/E ratio has moved down from the hyper growth 62 P/E in 1999 all the way down to the current 6 or 7 P/E net of cash. High expectations have collapsed to low expectations. Good, I seek low expectations.

Also, note the wisdom of crowds (the market). See the dotted line showing Dell’s share price relative to the market that declines from the end of 2002 to today. Note the decline accelerating while Dell made a high of $42.60 during 2005. The market (like it is doing with Apple today) was and is handicapping Dell’s future prospects. The “market” sensed the change in competitive dynamics occurring in Dell’s business. Respect the market because the onus is on you to be right or contrary to the consensus.

So what is the business worth?

Post tax “cash flow” is about $1.90 per share. Capex is estimated at 30 cents per share, but it was 38 cents per share in 2011 and back in 2006 and 2007 almost 40 cents. I want to err on the side of conservative so I put 40 cents for capex. $1.90 per share in “cash flow” minus 40 cents leaves me about $1.50 in free cash flow (“FCF”). For a discount rate with NO GROWTH I use about 11% to 12% because that rate is the average equity return for an average business. Yes the 30 year bond (“risk-free”) rate is 4% but normalized the rate is closer to 6% or 7% and I think historically the equity premium has ranged much higher (go read The Triumph of the Optimists for a history of equity premiums by country).

$1.50 divided by my discount rate of 11.5% leaves $13 per share for the operating business. The excess cash is $11.3 billion in cash minus $5.3 billion in long-term debt or $6 billion in net cash or about $3.50 per share. But I can’t get my hands on that cash, and taxes would have to be paid to repatriate that cash—I will knock off 25% and use $2.50 to add back to my operating value. I see that total debt is $9 billion so I need to check out the terms of the debt, but I will use $2.5 per share to add to $12. 50 to $13 per share operating business value with no growth of $1.50 per share FCF using a 11% to 12% discount rate.

My back of the envelope value is $15 to $16.5 per share. Now, that value range assumes no growth but alsono decline. I am receiving about 4% per year of the $1.50 in free cash flow in dividends and share buybacks. On the other hand, I have Mr. Dell’s high compensation, poor capital allocation record on share buybacks, and “me-first” attitude towards shareholders.

Since growth has no value, I am buying a non-franchise type company. Profitable growth will not bail me out, so I need a 30% to 40% discount for my margin of safety AND I can’t make it more than 2% to 3% of my portfolio. A major position for me is 5% to up to 15%. 30% to 40% discount from $15 to $16 leaves me a buying range of about $9 to $11. I will be conservative and look at $15 as my level of value so $9 to $10.50 will be my range. I bought in Sept. 2012 at about $10.60 and again in November at about $9.15 for an average price of $9.80.

Yes, I could be making all this up with hindsight bias, but this is from a simple man.

Upon the announcement of Dell going private, I waited a day and sold at $13.55. Why sell when the minimum value I placed on it was $15 and up to $16 per share? I am not an arbitrageur. I will leave it to them to make the last nickel or dollars. The business seems cheap, but I ride with a poor capital operator in a commodity business. I don’t see much future value and perhaps I was TOO AGGRESSIVE in my valuation. My return for investing in Dell is 39% for six months. Good, but it doesn’t factor in my losses for when I buy a “Dell” and all hell breaks loose and I may have to sell at $5 or $7. But I had excess cash, free cash flow, shareholder angst (Pzena and Southeastern) and LOW EXPECTATIONS at my back. My expectations of management and the business were low as well, but perhaps not low enough. Time will tell.

If you read Southeastern’s letter Dell-Board-Letter_by_Longleaf, they place a value of $24 on Dell (Southeastern paid about an average of $25 for Dell’s stock over the past five years (see 13-FH filings). They mention Dell paying about $12.94 per share at cost for their acquisitions buttressed by Dell’s CFO saying to that point had delivered a 15% internal rate of return. Perhaps, but I am skeptical that Dell’s acquisitions will generate more than an average rate of return. What does Dell bring to the party in its acquisitions? Scale? Technology, Patents? Customer captivity? Ironically, if Dell isn’t worth at least $13 per share for those acquisitions, then Dell’s current bid is another nail in the coffin for its reputation in building shareholder value.

I do agree with Southeastern’s letter that Dell should allow shareholders the option to remain invested in the company if they so choose while breaking up the company. If shareholders have traveled this far, let them decide. Basically, Michael Dell wants to use more cheap debt (available today) as a tax shield to juice his after-tax returns. I don’t blame him, but let the shareholders decide.

Beware of sum of the parts valuations. If you do use them, analyze the competitive advantages of each business segment.

I could spend a year on Dell reading about their divisions but I would have noedge over industry analysts. My edge (I hope) is sniffing out despair with a cynical eye.

Dell is not an obscure, forgotten company/stock, but it was laden with disappointment, despair and low expectations. I just had to wait for my price or walk away.

Hope this helps you to find our own way.

UPDATE: FEB. 12, 2013:

Mason Hawkins Buys More Dell While Opposing the Deal

The future of the Dell (DELL) deal is looking dimmer as its largest outside investor Southeastern Asset Management buys more shares while openly opposing the deal. Southeastern Asset Management bought almost 17 million shares in the past weeks. It now owns 146.8 million shares, which is about 8.5% of the company. Southeastern Asset Management has openly opposed the Dell deal, which is led by Michael Dell and plans to buyout other shareholders at $13.5 a share. Southeastern Asset Management said that the deal “grossly undervalued the company,” and believes that Dell is worth $24 a share, according to Barron’s.

Southeastern Asset Management has been a long-term holder of Dell, and started buying the stock when it was trading at above $30. Its average cost is estimated to be above $25. If the deal went through at $13.5, Southeastern would have lost almost 50% of its original investment, excluding dividends.

All corporate growth has to funnel through return on equity. The problem with growth companies and growth countries is that they so often outrun the capital with which to grow and must raise more capital. Investors grow rich not on earnings growth, but on growth in earnings per share. There is almost no evidence that faster-growing countries have higher margins. In fact, it is slightly the reverse. (CHINA!)

For there to be a stable equilibrium, assets, including entire corporations in the stock market, must sell at replacement cost. If they were to sell below that, no one would invest and instead would merely buy assets in the marketplace cheaper than they could build themselves until shortages developed and prices rose, eventually back to replacement cost, at which price a corporation would make a fair return on a new investment, etc.

The history of market returns completely supports this replacement cost view. The fact that growth companies historically have underperformed the market – probably because too much was expected of them and because they were more appealing to clients – was not accepted for decades, but by about the mid-1990s the historical data in favor of “value” stocks began to overwhelm the earlier logically appealing idea that growth should win out. It was clear that “value” or low growth stocks had won for the prior 50 years at least. This was unfortunate because the market’s faulty intuition had made it very easy for value managers or contrarians to outperform. Ah, the good old days! But now the same faulty intuition applies to fast-growing countries. (www.gmo.com 4th qtr. 2012 letter)

Value Investing News and Links

Don’t forget to go to www.grahamanddoddesville.com and www.santangelsreview.comfor their FREE value investing news emails. I would immediately go on a suicide watch if they ever stopped sending me their great links. SIGN UP! Oh, and visit their blogs as well. Both writers are thoughtful observers of the investment world.

Note what Einhorn says about Apple’s excess cash. Note also that the junk bond market is ebullient, so as night follows day, expect some buyouts–LBOs or MBOs (Dell). One search strategy might be to find companies with steady free cash flows and strong (underleveraged) balance sheet and wait ahead of the buy out announcements–owning a group of 5 to ten names.

Grant’s Feb. 8, 2013 issue quotes Bloomberg on Jan. 31:

With exclusive brands that help build customer loyalty and a FCF yield that is higher than the median of its peers, Kohl’s could be an attractive buyout candidate for a private equity firm…..The company’s real estate also adds to its appeal…. Kohl:KSS_VL 2013

But I think Coach (COH) is an even better candidate: COH_VL_Feb 2013with its higher, more consistent returns and excess cash.

Build your list because Mr. Ben Bernanke wants the $360 billion in committed unspent capital dedicated to buyout funds (Bloomberg estimate) to be spent. Source: www.grantspub.com

Stop the presses! Before reading Longleaf’s valuation of Dell (linked below), go to the 2009 and 2013 Value-linesand value Dell with a back of the envelope calculation using a post-tax free cash flow yield as one signpost.

What do you think Dell is worth—about? What do you think of the valuations mentioned in this article? Does growth have value? Why or why not?

Do you have any criticisms? What in Michael Dell’s prior history makes you (perhaps) not surprised by his current actions? Would you have factored that into your pre-announcement valuation? How? Should Dell offer to do a Tender Offer for the shareholders? If the price callapsed to $9 or $10 based on the deal being pulled what would you do?

I am having difficulty finding value, so now I gotta go small. More on micro-cap investing…..Liquidity as an Investing Style and Microcap_Investing and then More_on_Microcap_Investing. If you can accurately value a business while the company’s stock price is volatile, then you have a gold mine. Smaller companies tend to be more OVER and UNDER-VALUED than larger, well-known names.

Secrets and Lies of the Bailout

The federal rescue of Wall Street didn’t fix the economy – it created a permanent bailout state based on a Ponzi-like confidence scheme. And the worst may be yet to come

So what exactly did the bailout accomplish? It built a banking system that discriminates against community banks, makes Too Big to Fail banks even Too Bigger to Failier, increases risk, discourages sound business lending and punishes savings by making it even easier and more profitable to chase high-yield investments than to compete for small depositors. The bailout has also made lying on behalf of our biggest and most corrupt banks the official policy of the United States government. And if any one of those banks fails, it will cause another financial crisis, meaning we’re essentially wedded to that policy for the rest of eternity – or at least until the markets call our bluff, which could happen any minute now.

An excellent article that shows what has happened to our centrally-controlled, socialist, Ponzi financial system. Of course, the author does not point out the causes or remedies, but he does show the results of the bailout.

My favorite line:

We thought we were just letting a friend crash at the house for a few days; we ended up with a family of hillbillies who moved in forever, sleeping nine to a bed and building a meth lab on the front lawn.