When an investor turns to the research on regression to the mean and investors overreacting to poor company performance/bad news in Richard Thaler research, he or she sees that prices of the winner and loser portfolios take three-to-seven years to revert. See also The New Finance: The Case Against Efficient Markets by Robert A. Haugen and Inefficient Markets by Andrei Schleifer.

I couldn’t repair your brakes, so I made your horn louder. –Steven Wright

A Reader shares good news.

Hi John,

Partly motivated by your blog and lectures on value investing, I decided to quit my dead-end Hedge Fund job, and open my own investment management firm, Apatheia Capital. Think Schloss, and early Greenblatt special situations.I intend to use the best from quant and value investing in terms of buying cheap special situation stocks consistently.

So far it has been fun, exciting and anxiety-ridden process, and few friends and family have been misguided to be infected by my optimism. Please keep up the good work! I cannot stop thinking about my ideas (about ever-present fat tails in special situation value stocks). So far in the process, I have filed for state registrations etc. and finalized a mission document for the firm.

—

I wish you a great journey. Be flexible and patient. Use your small size to your advantage by going anywhere there is value. Keep good records of your investment journey and keep in touch!

The Relation Between The Enterprise Multiple and Avg Stock Returns 2010 more research on the efficacy of using the enterprise multiple as an indicator of value. Remember to adjust for normalization because at the top of a cycle you will see low EV to EBITDA (like in housing circa 2005/06) or high EV/EBITDA (11 x) BTU VL Dec 2014 near a depressed cycle. Coal reserves are priced low and production doesn’t generate high enough cash flows for the industry to generate a normal return, so mines are being closed, production shuttered, mines consolidated. The cure for low prices is low prices.

Why can’t 70% of professional money managers beat chimps?

High fees/costs, index hugging, inconsistency, overconfidence in their ability to be above average, lovers of stories, herding, and the institutional imperative? Don’t forget incentives that differ from achieving performance like asset gathering. See the case study at the end of this post.

We left off with a reader asking why do money managers do better or follow a deep value approach? http://wp.me/p2OaYY-2IZ

One goal of our Deep Value journey is to find a method that suits us. This method should have a large base case rate of beating an index over a long period of time, say fifty years. The lesson learned so far—I hope—is that CHEAPNESS wins whether that is price to book value, price to sales, price to cash flow. My recent reading of the most recent 4th Edition of What Works on Wall Street shows that high EBITDA-to-EV has beaten out Price-to-Sales (3rd Edition) What Works on Wall Street, Third Edition as the best metric as a value factor. However, combined with quality of earnings metrics, it performs even better or about 18% to 19% per year since 1964 to 2009. Our goal is to put the odds on our side and CONSISTENTLY play the odds through thick and thin. Our other edge is to realize how flawed our thinking is and thus we build protection against ourselves by developing a disciplined approach.

What Works: Notes from Joel Greenblatt’s class 2002:

Read: What Works on Wall Street by James P O’Shaughnessy. He started a fund in 1996-1997 but he underperformed the market by 25% and after three years in business of underperforming he sold his company at the bottom of the cycle. The guy who wrote the book quit his system! It seems like it is easy to do, but it is not easy to do.

This book, What Works on Wall Street, has born out its wisdom. The two funds that are patented that follow his strategy have been phenomenal. HFCGX is the patented fund based on his top idea of Cornerstone Growth; over the last 5 years it has had an average return of 13.44% per year vs. the Vanguard 500’s -2.01% per year (6/1/00 through 5/31/05). HFCVX is the patented fund based on his 2nd to best idea of Cornerstone Value; over the last 5 years it has had an average return of 6.47% per year vs. the Vanguard 500’s -2.01% per year (6/1/00 through 5/31/05).

The most interesting point is that the author points out those investors often are too emotionally involved to have the discipline to see the strategy through. Not only did the first reviewer bash the book because he did like the returns strategy JUST one year after the book came out, but Mr. O’Shaughnessy sold the funds to Hennessy Funds at the end of 1999 after it failed to surpass the returns of the bubble that soon after collapsed. Seven years after it was published an investor would be much wealthier had they followed the books top strategy instead of the investors who dog-piled onto the stocks of the market’s bubble.

We are going to try to understand why it works. Why it has to work over time. That is the only way you can stick it out. The math never changes: 2 + 2 = 4. That is the level of your understanding I want you to have by the time we are done. If I get that right, forget all this other stuff and noise, I will get my money. No genius required. Concepts will make you great and your ability to STICK IT OUT.

There is a lot of experience involved in valuation work, but it doesn’t take a genius or high IQ points to know the basic concepts. The basic concepts are what will make you the money in the long run. We are all capable of doing the valuation work.

—

Notes from the 4th Edition of What Works on Wall Street

Why Indexing Works

Indexing works because it sidesteps flawed decision-making and automates the simple strategy of buying the big stocks that make up the S&P 500. The mighty S&P 500 consistently beat 70 percent of traditionally managed funds over the long-term by doing nothing more than making a disciplined bet on large capitalization stocks.

Money Management Performance

Past records of most traditional mangers cannot be predictive of future returns because their behavior is inconsistent. You can’t make forecasts based on inconsistent behavior.

Common Sense Prevails

We now have the ability to empirically compare different investment strategies and their ongoing performance over time. What you will see in coming chapters is that almost all of them are deeply consistent with what common sense would tell you was true. Strategies that buy stocks that are selling at deep discounts to cash flow, sales, earnings , EBITDA-to-enterprise value (Yeah, but don’t forget MCX), and so on do extraordinary better than those that are willing to buy stocks with the richest valuation. WE will be sensitive to data mining.

Systematic, structured investing is a hybrid of active and passive management that automated the buy and sell decisions. If a stock meets a particular criteria, it’s bought. If not, not. No personal, emotional judgments enter into the process. Essentially, you are indexing a portfolio to a specific investment strategy and, by doing so, uniting the best of active and passive investing. The disciplined implementation of active strategies is the key to performance. Traditional managers usually follow a hit-and-miss approach to investing. Their lack of discipline accounts for their inability to beat simple approaches that never vary from the underlying strategy.

The ONE thing that unites the best money managers is consistency.

Successful investing requires, at a minimum, a structured decision-making process that can be easily defined and a stated investment philosophy that is consistently applied.

Goeth said, “In the realm of ideas everything depends on enthusiasm; in the real world, all rests on perseverance.” While we may intellectually understand what we should do, we usually are overwhelmed by our nature, allowing the intensely emotional present to overpower our better judgment.

Human Judgment is limited

Why models beat humans

Models beat the human forecasters because they reliably and consistently apply the same criteria time after time. It is the total reliability of application of the model that accounts for its superior performance.

We are ALL above average.

Base rates are boring

We prefer gut reactions and stories to boring base rates.

Stocks with low PE ratios outperformed the market in 99 percent of all rolling 10-year periods between 1964 and 2009.

The best way to predict the future is to bet with the base rate that is derived from a large sample.

Base rates are boring while experience is vivid and fun. Never mind that stocks with high P/E ratios beat the market less than 1 percent of the time over all rolling 10-year periods between 1964 and 2009.

Montier in his book, Value Investing writes: “One of the recurring themes of my research is that we just can’t forecast There isn’t a shred of evidence to suggest that we can.

We prefer the complex and artificial to the simple and unadorned.

Nowhere does history indulge in repetition so often or so uniformly as in Wall Street. When you read contemporary accounts of booms or panics, the one thing that strikes you most forcibly is how little either stock speculation or stock speculators today differ from yesterday. The game does not change and neither does human nature.—Edwin Lefevre.

Brain Research

Because of the interrelated nature of the emotional and rational centers of our brain, we will never be able to fully overcome our tendency to make irrational choices. Simply being aware of this problem does not make it go away. To break from our human tendencies to chase performance and perceive patterns where there are none, we must find an investment strategy that removes subjective, human decision-making from the process and relies instead on smart, empirically proven systematic strategies. We can become wise by realizing how unwise we truly are.

Rules of the Game

It is amazing to reflect how little systematic knowledge Wall Street has to draw upon as regards the historical behavior of securities with defined characteristics. –Ben Graham

Richard Brealey, a respected data analysis, estimated that to make reasonable assumptions about a strategy’s validity (95% confidence level or statistically relevant) you would need 25 years of data.

Short periods are valueless

Consider the “soaring sixties” when the go-go growth managers of that era switched stocks so fast that they were called gunslingers. The go-go investors of the era focused on the most rapidly growing companies without even considering how much they were paying for every dollar of growth. Between Jan 1, 1964, and Dec. 31, 1968, $10,000 invested in a portfolio that annually bought the 50 stocks in the Compustat data base with the best annual growth in sales soared to $33,000 in value , a compound return of 27.34 % a year. That more than doubled the S&P 500’s 10.16% annual return, which saw $10,000 grow to just $16,200. Unfortunately, the strategy went on to lose 15.7% per year for the following five years compared to a gain of two percent for the S&P 500.

Had this same hapless investor had access to long-term returns, he would have seen that buying stocks based just on their annual growth of sales was a horrible way to invest—the strategy returns just 3.88 percent per year between 1964 and 2009. Of course, the investor received similar results if he repeated the experiment between 1995 and 1999 and then the next five years.

EBITDA to EV was the best on an absolute basis for all the individual value factors we examine from 1964 to 2009 such as price to cash flow, price to earnings, etc.

EV/EBITDA in the lowest decile (the most EBITDA per EV) generated a 16.58% CAGR vs. 11.22% for the All Stocks universe with a standard deviation of returns of 17.71 percent, more than 1 percent below that of All stocks, 18.99 percent. The worst five-year period for the metric was 2000 during the Internet Mania. These ups and downs for a strategy are all part of the bargain you must strike with yourself as a strategic investor. Pages 103 to 124 in What Works (4th Ed.) The EV/EBITDA in the highest decile (the most “expensive) did the worst of all the value metrics studied!

EV works well as a guide to under-and-over valuation when contrasted to EBITDA, SALES, and Free cash flow.

Price to book value ratios are a long-term winner with LONG periods of underperformance.

Accounting Ratios can help identify higher quality earnings:

Total accruals to total assets

Percentage change in net operating assets (NOA)

Total accruals to average asses.

Depreciation expense to capital expense.

We are looking for stocks with high earnings quality.

Accounting variables mater. How companies account for accruals, how quickly they depreciate capital expenses and their additions to debt all have a serious impact on the health of their stock price.

Successful investing relies heavily on buying stocks that have good prospects, but for which investors currently have low expectations. Stocks with great earnings gains and high net profit margins are basically high expectations stocks.

History shows that using high profit margins as the SOLE determinant for buying a stock leads to disappointing results. The only lesson here is that it is best to avoid stocks with the lowest net profit margins.

A Case Study in Why Money Managers Lose Even With a Winning Hand

Winning Stock Picker’s Losing Fund

Value Line Research Service Has Beaten Market Handily, But Its Own Fund Suffered By Jeff D. Opdyke and Jane J. Kim Staff Reporters of THE WALL STREET JOURNAL Updated Sept. 16, 2004 12:01 a.m. ET

Value Line Investment Survey is one of the top independent stock-research services, touted for its remarkable record of identifying winners. Warren Buffett and Peter Lynch, among other professional investors, laud its system.

But the company also runs a mutual fund, and in one of Wall Street’s odder paradoxes, it has performed terribly. Investors following the Value Line approach to buying and selling stocks would have racked up cumulative gains of nearly 76% over the five years ended in December, according to the investment-research firm. That period includes the worst bear market in a generation.

Why the Fund Lagged

Past managers bought stocks that in some cases were well below the company’s top-rated choices, hurting performance.

Style drift: The fund has swung among small-, mid- and large-cap shares.

High turnover of fund managers meant little consistent investment discipline.

By contrast, the mutual fund — one of the nation’s oldest, having started in 1950 — lost a cumulative 19% over the same five years. The discrepancy has a lot to do with the fact that the Value Line fund, despite its name, hasn’t rigorously followed the weekly investment advice printed by its parent Value Line Publishing Inc. It also highlights the penalty investors often face when their mutual fund churns its management team and plays around with its investing style. In fact, late last night the person running the fund, Jack Dempsey, said that as of yesterday he had been reassigned and no longer had responsibility for managing the assets. Value Line couldn’t be reached to comment.

Most of all, the discrepancy between the performance of the fund and the stocks it touts shows that investors don’t always get what they think they’re buying in a mutual fund. For even though Value Line’s success is built around stocks ranked No. 1 by the company’s research arm, the fund’s managers have in recent years dipped into stocks rated as low as No. 3.

Ironically, even while Value Line’s own fund struggles to match the Value Line Investment Survey’s success, an independent fund company that licenses the Value Line name is doing much better with Value Line’s investment approach.

The First Trust Value Line 100 closed-end fund, run by Lisle, Ill.,-based First Trust Portfolios, adheres far more rigorously to Value Line’s investment principles, owning only the top-rated stocks.

Each Friday, First Trust managers log on to the Value Line site to download the week’s list of Value Line’s 100 most-timely stocks. During the next week, they sell the stocks that have fallen off the list and buy those that have been added. The result: Since its inception in June 2003, the First Trust Value Line fund’s net-asset value is up 12.4%, slightly better than the 11.6% gain the Standard & Poor’s 500-stock index posted in the same period.

Value Line’s own fund, meanwhile, gained 3.1% in that same time. Because the fund has been such a laggard in recent years, investors have been walking away. Assets in the fund — in the $500 million range as recently as 1999 — are now less than $200 million, though some of that stems from market losses.

Part of the underperformance stems from previous fund managers who didn’t rely entirely on Value Line’s proven model, opting instead to venture into lower-rated stocks, betting that active fund managers could unearth overlooked gems that one day would shine as top-rated stocks. Thus, investors who thought they were buying into Value Line’s winning investment strategy instead were buying into fund managers who thought they could outperform by second-guessing the company’s research — a tactic that didn’t work well.

Because the fund wasn’t performing well, the company changed managers frequently, searching for one who could post winning returns.

Value Line appeared to be moving back toward its roots in March, when it put Mr. Dempsey in charge of the fund. He isn’t the traditional mutual-fund manager; he’s a computer programmer who for a decade helped refine Value Line’s investment models. Value Line, which uses a team-managed approach, has had at least five lead fund managers since 1998, including Mr. Dempsey, according to Morningstar.

In an interview prior to his reassignment, Mr. Dempsey said he had been restructuring the fund to follow the ranking system “in a much more stringent fashion.” Today, about 95% of the stocks in the fund are rated No. 1. Mr. Dempsey said his goal was to liquidate within a week stocks that fell below Value Line’s No. 1 ranking.

The Value Line survey produces independent research on Wall Street stocks. The weekly view of 1,700 stocks, which costs $538 a year online (www.valueline.com) and nearly $600 in print form, is particularly popular with do-it-yourself investors and the abundance of investment clubs in the U.S. Value Line rates stocks in a variety of ways, but is especially known for its so-called timeliness rank. Stocks ranked No. 1 are timely and expected to outperform the market; those ranked No. 5 are expected to lag.

Instead of running an actively managed fund in which a manager cherry-picks the stocks the fund owns, Value Line could operate what amounts to an index fund that simply owns the highest-ranked stocks in the survey. However, active managers believe they can improve the performance of a fund.

“As a fund manager, you want to add value,” Mr. Dempsey said. Still, he acknowledged that “it’s hard to beat our quantitative system.” In the short time that Mr. Dempsey was in charge — a nearly six-month period in which he transformed the portfolio — he accumulated losses of about 2%, compared with losses of 0.2% at the S&P 500. However, he topped the First Trust fund, which is down about 2.5% in the same period. Under Mr. Dempsey, the fund accumulated significant positions in stocks such as Research In Motion Ltd. and added new positions in Yahoo Inc. and Arrow Electronics Inc., among other companies, according to Morningstar.

Value Line, based in New York, doesn’t detail the inner workings of its proprietary stock-picking model. By and large, though, the strategy is built around stocks displaying price and earnings momentum and posting earnings surprises, says John James, chairman of the Oak Group, a Chicago company that runs hedge funds, some of which try to anticipate changes in Value Line’s stock rankings and then invest based on which stocks will rise to No. 1 from No. 2.

However Value Line’s model works, there’s no question the company’s research produces winning choices. Value Line’s list of stocks ranked No. 1 produced cumulative gains of nearly 1,300% from Dec. 31, 1988 through June, 30, 2004, according to Value Line. The S&P 500, by comparison, posted cumulative gains of 311%.

I must say lot of valuable advice from a seasoned investor.

I read the linked article, but I wonder if the folks here took away the key lesson(s)

OK, why was this investment a “Value Trap?” What can we learn from this example or ignore in this article? Are you investing when buying this bank? What makes a bank very different from investing in a widget factory? The article goes on to say you should wait for a catalyst. Is there a flaw to that argument? What about checklists? Can checklists save you from faulty thinking?

—

A Frustrated Reader:

Moreover, I wonder if it would be possible to have an index or anything like that in order to program and coordinate all classes and materials.

I teach under the chaos-and-mayhem method to force you to choose what is important to you. In a more serious light, we are going chapter-by-chapter in DEEP VALUE and it is supplement by Quantitative Value and other readings.

Next, use the search box in the upper right corner of this blog to type in: Lesson 1 Deep Value. Then scroll to the links and begin there. The blog supplements the readings. You should have already received a link to the book folder. Much of the materials are supplementary. For example, we read in Chapter 3 in Deep Value about Buffett’s career, so various case studies were linked in the various posts that correspond to the chapter like See’s Candies or Dempster Mills. Also, the Essays of Warren Buffett were sent out, but that is up to you if you want to read further (I highly recommend that you do and reread every year).

—

A Reader provides links:

Was on reddit’s Security Analysis sub (www.reddit.com/r/securityanalysis) and stumbled upon these notes from some other readers, good supplementary reading:

While I agree completely with your analysis, I think its worth noting additionally that:

Quant Value proponents (e.g. Graham, Greenblatt & Carlisle) are not arguing that any given filter (EV to EBIDTA for instance) accurately measures the intrinsic value of a given company. Agreed

But rather they argue that some filters (or combinations of filters) can capture mis-pricings in a basket of stocks. Agreed

And on average, over time the captured mis-pricings will deliver a return that dramatically exceeds the index and all but the most exceptional stock-pickers. Agreed. “Experts” may even degrade the results of a quant model!

So while a given filter (EV to EBITDA for instance) may be just the beginning of the analysis for a stock-picker working a concentrated portfolio,

that same filter alone may be enough for a Quant Value portfolio to outperform 99%+ of stock-pickers,

and with far less work.

To the extent this finding is true and replicable in real time, it is a remarkable finding. What puzzles me is this:

Given a huge economic opportunity–some screens deliver 2X market returns in back tests

Given the Quant Value idea has been around for 75+ years–since Graham described the Net Net idea in Security Analysis

And given the vast resources dedicated to optimizing portfolios

Why are there so few examples of this simple idea being executed effectively in real time?

The best answers I’ve heard to this question (most of which were mentioned by Greenblatt in TLBTBTM) are:

Quant Value strategies are difficult to stick with because they will under-perform the market for years at a time

Much of the excess return is found in small cap stocks so it cannot be run in a large portfolio

The stocks selected by the Quant Value screens are “ugly” stocks which are difficult to own and defend

While all these explanations make sense, it still appears to me that the lure of 2X market returns would be enough to overcome them. So I am left with the puzzle: why is this opportunity not more widely exploited? I would be interested to hear any thoughts from the group on this…

I will post tomorrow my thoughts on your other questions.

Imagine diligently watching those stocks each day as they do worse than the market average over the course of many months or even years….The magic formula portfolio fared poorly relative to the market average in five out of every 12 months tested. For full-year period…failed to beat the market average once every four years. Joel Greenblatt discusses the role that loss aversion plays in deterring investors from following his ‘magic formula’. (Montier)

A Summary

Greenblatt reinterpreted Buffett’s return on equity capital measure as RETURN ON CAPITAL, which he construed as the ratio of pre-tax operating earnings (earnings before interest and taxes, or EBIT or EBITDA-MCX or operating earnings that are sustainable) to tangible capital employed in the business (Net Working Capital + Net Fixed Assets) defined as:

Return on Capital = EBIT divided by (Net Working Capital (NWC) + Net Fixed Assets)

The use of EBIT makes the return on capital ratio comparable across different capital structures. EBIT makes an apples-to-apples comparison possible.

For tangible capital Greenblatt uses NWC + Net Fixed Assets rather than total assets to determine the amount of capital each company actually requires to conduct its business.

The higher the return on capital ratio, the more wonderful the company.

To determine a fair price, Greenblatt uses earnings yield, which he defines as follows:

Earnings Yield = EBIT divided by Enterprise Value (EV).

EV gives a more full picture of the actual price an acquirer must pay than market capitalization alone. EBIT is agnostic to capital structure so we can compare companies on a like-for-like basis.

The higher operating earnings are in relation to enterprise value, the higher the earning yield, and the better the value.

Greenblatt has quantified Buffett’s wonderful company at a fair price strategy.

Enterprise Multiple (EV) = EBITDA divided by EV or (EBITDA – Maintenance Capital Expenditures) divided by EV.

BEWARE!

The EV to EBITDA ratio is useless without a discussion on asset lives, capital intensity, technological progress or revenue recognition.

EBITDA, or any of its derivatives (EBDIT, EBITDAR, etc.) is simply a crude measure of gross cash flow.

The gross cash flow margin is simply a measure of the capital intensity of the business. A manufacturing business will have a significantly higher gross cash margin than, say, a retailer, because it needs to pay for the capital (via in the accounting sense the depreciation charge) of all its plant and equipment which consumes more of it than a superstore.

What matters is not gross cash flow but net of free cash flow, which is the amount of cash available after reinvestment.

Case Study:

In the heyday of the technology bubble, the EV to EBITDA ratio was a favorite among telecom analysts. Sadly, as new entrants came into the system and pushed up the price of the UMTS licenses (the third generation of mobile networks) to insane levels, the cost of replacement went sky-rocketing; expected free cash flow plummeted, and the telecom shares got more and more ‘attractive’ on an EBITDA basis, which could not capture any of this. Eventually, some went bankrupt, some had to undergo a debt rescheduling exercise or issue new capital, and all saw their share price collapse.

James Murray Wells, a 21-year-old law student in Bristol, UK, needed a pair of glasses, and was faced with a bill of 150 stg. He found that the manufacturing cost off standard spectacles (frame and glasses) was less than 10 stg. This prompted Mr. Murray Wells to set up an Internet-based company to challenge what he claimed was a lack of price competition among the four major high street opticians in England. Three months into his venture, he was selling hundreds of pairs for as little as 15 stg to apparently delighted customers.

The replacement value of the asset, ‘making spectacles and selling them’ is rather low. A 21-year old student with no expertise in the field is apparently able to replicate it from his student room, with a few thousand pounds borrowed from his father. On the other hand, the market value is enormous because, as previously discussed, it equals the net present value of free cash flow discounted to infinity.

The market value is a direct function of the economic profitability of the asset in question and, in this example with a cost of goods sold at 10 and sales at $150, it is plain that economic value added is truly staggering. Making spectacles and selling them has a high ROIC, and an equally impressive asset multiple—the ratio of market value to the replacement value of invested capital.

If the entrepreneur is successful in his venture, he will collapse the marginal return on capital invested of the industry by accepting a lower margin than his competitors. The entrepreneur made an arbitrage between the market value of existing capacity and the replacement value of new capacity, which he found cheaper to create.

Investors in incumbent firms my find out that they have paid too much for the economic value of their asset in the belief that a very high economic return on capital invested was sustainable. Investors who ignore the workings of the capital cycle, the ultimate driver of share prices, do so to their disadvantage.

Investment should just be a replication of the process of arbitrage between market value and replacement value. Good stock pickers are brilliant strategy analysts. They understand the business case for the company. (TATOO that to your forehead!)

—

Questions:

Why is the EV so good at identifying undervalued stocks?

What drives the returns of the magic formula? What Metric? What does this mean for us as Deep Value Investors?

Assuming you read the entire chapter, what two main points about investing did you learn? Anything surprise you?

Supplementary Readings:

What Has Worked in Investing by Tweedy Browne Why do low price-to-book, low price to cash flows, etc tend to generate higher returns than a market average? What is the principle behind the returns? Also, note the Richard Thaler link below for a hint.

When an investor turns to the research on regression to the mean and investors overreacting to poor company performance/bad news in Richard Thaler research, he or she sees that prices of the winner and loser portfolios take three-to-seven years to revert. See also The New Finance: The Case Against Efficient Markets by Robert A. Haugen and Inefficient Markets by Andrei Schleifer.

You just got hired as a junior analyst for a hedge fund. Your boss calls you in and asks for your opinion on whether he should buy IRDM. He heard about it from a hedgie friend in New York who heard about it from another hedgie friend in New York who heard about it from…….you get the picture–a daisy chain of independent-thinkers.

You remember something about Buffett saying that the tooth fairy doesn’t pay for capex? What will you tell your boss this afternoon?

If you want more clues (after trying hard) go to the search box on this blog and type in IRDM–follow the links.

Good luck!

PS: I will resend the book folder to new students and I will send value vault folders to the folks who have been asking for the past three weeks. I try only to check email once a day and I group the various email requests over time.

I will be next focusing on ROIC for Chapter Four in Deep Value because we already covered EBITDA and its use and ABUSE. And EV/EBITDA multiples. Remember that multiples are simply a short-hand for cost of capital. I remember when Blockbuster(US Video Chain) looked cheap in an EV/EBITDA analysis (from a broker report) but Blockbuster was being dis-intermediated by Netflix and planned to reinvest in its stores to sell popcorn and toys along with DVDs. How do you think that turned out? Rear-view looking at past multiples may mean being entombed in a value trap. When I heard of Blockbuster’s plan, I thought of entering a mule in a horse race–what are my chances?

Have faith but don’t be overconfident! Have a great weekend from sub-zero New England.

What multiples and metrics to use for different industries?

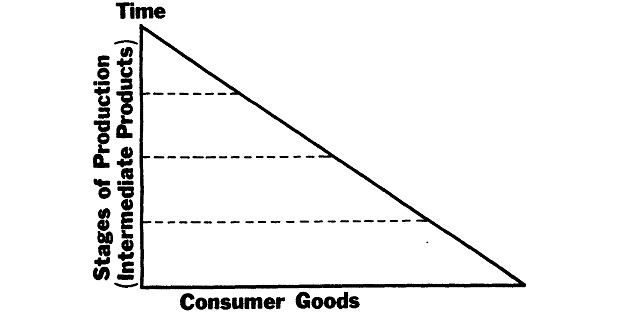

A reader struggles with how to value cyclical industries. First you have to understand the particular industry. How to do that–read the reports and financials of dozens of companies in that industry, then note what is important to value such a business. Take several months. If you are looking at highly-cyclical businesses, then you should read : Skousen-Structure-production.pdf.

Note how long the cycles are in the gold mining industry. A mine may take a year or two to close or years to open. From discovery of the deposit until extraction may take a decade or more. A gold miner is valued on production, reserves, cost to extract, etc.

Now if you have access to a Bloomberg (expensive!) or go to a library and look at Value-Line, Moody’s Manuals, or industry articles of the industry. You can scrub around the Internet, but you have to grind through company reports to get a feel. Obviously, “heavy industries” require analysis of tangible book, replacement value, capital costs, industry capacity and utilization–note what happened in the airline industry when capacity was taken off-line. Go to search box and read my post on CRR, Carbo-ceramics–below TBV and replacement value, for example.

If I seem abrupt with your questions, here is the reason why.

What happens if you get scared half to death twice? –S. Wright

We were unable to discover any ‘magic’ qualities associated with stocks selling below liquidation value. — Joel Greenblatt (How the Small Investor Can Beat the Market)

Enterprise Multiple = Earnings before interest, taxes, and depreciation & amortization, (“EBITDA”) divided by Enterprise Value (“EV”).

We need to understand the use of EBITDA, Why we must use EV, and the requirement to use pre-tax owner’s earnings or EBITDA – maintenance capex (“MCX”).

I intend to live forever. So far, so good–Steven Wright

—

We will tackle Chapter 4 in Deep Value next week and I will find out the status of the forum for advanced students this weekend. I am swamped.

—

POP QUIZ

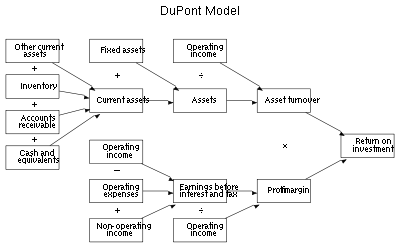

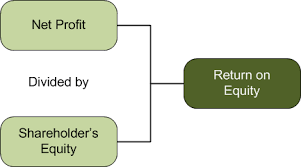

If a company is increasing its Return on Equity (“ROE”) over time, is that an attribute of a good business?

Since you are skeptical, you whip out your ROE diagrams:

Even better, you are hired as the investment banker to help advise the CEO how to enhance ROE (bonuses are based on rising ROE and increasing earnings per share).

Today, the company receives 0.00000000000001% on its money market accounts, while the CEO’s company stock trades at 34 times earnings and earns its cost of capital, 10%. Remember, you work for JP Morgan and you have student (MBA) loans to pay off. You sharpen your pencil and……………….?

My thoughts posted this weekend after I pass out grades.

—

Post: Feb. 16, 2015

Damn! I am unable to flunk anyone. There was a good discussion looking at the question from many sides because I didn’t give you much detail. The key point is: “It depends.” Context is key. You could have a situation like Microsoft’s where its core businesses (Office, etc.) generate so much cash without incremental investment that cash builds up and in turn drags down ROE (equity grows without a high return on the cash). Then the issue becomes what will Microsoft do with its excess cash? Squander on new ventures and acquisitions or return it to shareholders? Microsoft over the past six years has done a little bit of both. Perhaps low ROE means the company has no debt and thus a buffer during cyclical down turns?

Maybe this company’s ROE is suppressed by last year’s investment into new stores and more time is needed before the stores earn their expected return. Perhaps, like Costco or Philip Morris, future growth will be so profitable and persistent that buying in shares means reducing shares below intrinsic value–a long shot, how many emerging Wal-Marts, Costcos or Whole Foods are there?

The popular move which I, as a JP Morgan banker, would advise the CEO to buy back his stock with his low yielding cash (about a 0%) return and lather on low cost debt to buy stock back to earn an approximate 3% return (1 divided by 34) despite being a mundane business (10% ROE). Even at inflated prices. You shrink share count and equity to drive up EPS and ROE. The CEO collects another bonus and you can chirp about your value enhancement strategies. But when you buy an average company at 34 times earnings, you are paying over intrinsic value (let’s assume). Earnings and ROE rise but book value drops. Long-term wealth is reduced. Look at tech and consumer good companies today where managements are buying in their stock near all-time highs after a six year run-up. Few bought shares in the depths of the 2008/09 crisis. Borrow money today at 3.5% to buy-in your stock at a 5% earnings yield. Brilliant–until the next economic downturn.

This is another lesson in incentives. CEOs are incentivized to get a short-term bump in their stock prices, long-term value be damned.

Thanks for all the comments. A student from Germany kindly offered to host a discussion board for anybody who wants to analyze investment ideas, cases and/or investment subjects in more detail. The infamous Dr. K has also offered to moderate the board. If he upsets too many people, I will referee. As long as differing views are respected then we will be fine.

My overall goals for this course are to study deep value investing while encouraging independent and skeptical thinking. We will try to read original sources and apply principles to our own situations.

I don’t “like” deep value investing or mechanical investing but I was curious why investing in business disasters is so profitable (Preface in Deep Value). I also find it odd at first glance that Ben Graham the father of detailed security analysis gravitated to rule-based (my substitute for “mechanical”) investing. Joel Greenblatt who was the master of special situation, heavily concentrated investing also moved towards the “magic formula” style of investing. Another great investor I know used to visit companies and be highly concentrated into 8 or so businesses. Now he buys a diversified group of STABLE franchises when they go on sale. He also has a rules-based valuation method. What is going on?

Also, as more time passes, you realize that our human flaws are tough to overcome. Toby in Deep Value mentions that experts often DEGRADE mechanical systems. In other words, human tendencies hurt investment performance. Perhaps “mechanical” investing is worth exploring further without preconceived notions.

I often feel investing is like this situation:

Killing a child is wrong. Those soldiers acted, but then the unexpected happened. What now? Morally you know what is right but can you face the consequences?

It isn’t hard to find cheap companies in this pile (but many worth $0), but there is every reason not to act. Can you endure the ridicule?

Gold mining is a tough business–when wasn’t it a bad business? Managements are bad (true, but note how US tech firms are buying back stocks near their all-time highs—their managements are no better than the miners yet their stock prices are stratospheric), and on and on.

Altucher writes of Buffett’s early career. Even in the 1990’s Buffett was buying net/nets and companies in Korea trading at 2 to 3xs earnings.

So I chose Deep Value as a guide/textbook to pursue these topics with this group.

The direction of the course will be easy to follow:

We will go chapter-by-chapter in DEEP VALUE by Toby Carlisle while reading the footnotes and original sources as best we can. Let’s understand terms in the book like enterprise value and EBITDA, for example, before moving on to the next chapter.

We just finished Chapter 3, Warren Buffett: Liquidator to Operator where we had the case study of See’s Candies. Buffett moved from investing in deeply discounted tangible assets like Dempster Mills to a franchise like See’s Candies. Buffett was willing to pay a premium over book value because the assets of the business generated returns far in excess of its cost of capital. See’s takes commodities like sugar, milk and chocolate and turns them into boxed chocolates that customers are happy to pay a premium for. Why? The company has a brand built through the customer’s experiences with the product. As a deep value guy, I gave a second-hand box of chocolates to my EX. I said, “Here, ignore the half-eaten chocolates, the rest look OK. I got this on a 95% off sale!” Tense!

So what can WE learn from the case that we can apply in our investments? So rather than try to be like Buffett let’s take his principles and find applications which we can apply going forward. Why is See’s a great business? Taking commodities and turning them into a product that consumers pay a premium for seems like a business to buy. Note that Bicardi was the best business in Cuba and still is going strong. Bicardi takes sugar and water and turns it into premium Rum. I see similarities—brand name built upon quality and good distribution within its geographical boundaries. See’s is strong in southern California, for example. Perhaps, Sherwin-Williams is a bit like See’s Candies. People are willing to pay a premium for paint because 98% of the cost of a painting job is the labor while you want the job to last and look good. Good distribution coupled with service (color tinting/application advice) is also critical. I could go on but the point is to take the general concepts and apply them in your own way. Don’t be Buffett, but be yourself in applying Buffett’s lessons.

Chapter 4: The Acquirer’s Multiple: Fair Companies at Wonderful Prices in Deep Value