John Chew asked me to post while he goes through his stem cell transplant. He says, “I’ll be back.”He thanks the many readers for their kind words of encouragement.

Novagold Annual Report 2015 This annual report’s shareholder letter including the links provides an excellent example of how several investors view the capital cycle for an asset. History does provides a guide.

A short summary of the tug of war over Valeant. Setting aside the noise about fraud, greed, and accounting issues, The Valeant Casino, this is a company that financed fast asset growth with cheap debt (at the time) while taking advantage of the flawed quasi-socialized medical system in the US. Valuation depends on a normalization of truelong-term cash flows–VRX_Update_StillOverpriced_2016-03-15 and EV_EBITDA_Misses_the_Point (View video on valuation and ROIC below for more context). The beneficiary of medical care does not DIRECTLY pay ALL of the costs. Who would be willing to accept a $1,000 tube of anti-fungal cream for their itchy feet if a third-party didn’t pay? See Dying with dignity.

The above article should be a sobering reminder of how difficult it is to choose exceptional stocks. Remember when reading about great compounding machines like Wal-Mart in its early days (1970 to 1999) that you must take into account survivorship and hindsight bias.

From his introduction to Capital Returns: Investing Through the Capital Cycle: A Money Manager’s Reports 2002-15, which was released in hardcover today (Dec. 2015):

Typically, capital is attracted into high-return businesses and leaves when returns fall below the cost of capital. This process is not static, but cyclical – there is constant flux. The inflow of capital leads to new investment, which over time increases capacity in the sector and eventually pushes down returns. Conversely, when returns are low, capital exits and capacity is reduced; over time, then, profitability recovers. From the perspective of the wider economy, this cycle resembles Schumpeter’s process of “creative destruction” – as the function of the bust, which follows the boom, is to clear away the misallocation of capital that has occurred during the upswing.

The key to the “capital cycle” approach – the term Marathon uses to describe its investment analysis – is to understand how changes in the amount of capital employed within an industry are likely to impact upon future returns. Or put another way, capital cycle analysis looks at how the competitive position of a company is affected by changes in the industry’s supply side. In his book, Competitive Advantage, Professor Michael Porter of the Harvard Business School writes that the “essence of formulating competitive strategy is relating a company to its environment.” Porter famously described the “five forces” which impact on a firm’s competitive advantage: the bargaining power of suppliers and of buyers, the threat of substitution, the degree of rivalry among existing firms and the threat of new entrants. Capital cycle analysis is really about how competitive advantage changes over time, viewed from an investor’s perspective.

“Bull markets are born on pessimism,” he declared, they“grow on skepticism, mature on optimism, and die on euphoria.” –John Templeton

John Templeton paid attention to the emotion of the stock market. The first half of his philosophy was “The time of maximum pessimism is the best time to buy.” When everyone else was selling, he bought low during the Depression and in 1939 at the onset of World War II . . . and he made millions.

The second half of his philosophy was “the time of maximum optimism is the best time to sell.” He sold high during the Dot.com boom when everyone else was still buying. Founded in the 1950s, his Templeton Growth Fund averaged 13.8% annual returns between 1954 and 2004, consistently beating the S&P 500.

—

I think there are a few ways to make many times (10x to 100x +) your money over a long period of time. The first would be to own emerging growth companies that have owner-operators who are both excellent operators and capital allocators who grow the company profitably at a high rate over decades. The business generates high returns on capital while being able to deploy capital into further growth. Think of owning Wal-Mart in the early 1970s or Amazon after its IPO or 2001. There will be a post on 100 to 1 baggers soon. I prefer this approach.

The second way would be to buy distressed assets and then improve those assets or create efficiencies by creating economies of scale. Carlos Slim, Mexican Billionaire, would be an example of this type of investor. Think activist investing. Note that Carlos Slim has operated at times as a monopolist in a government protected market. Most of us do not have his options.

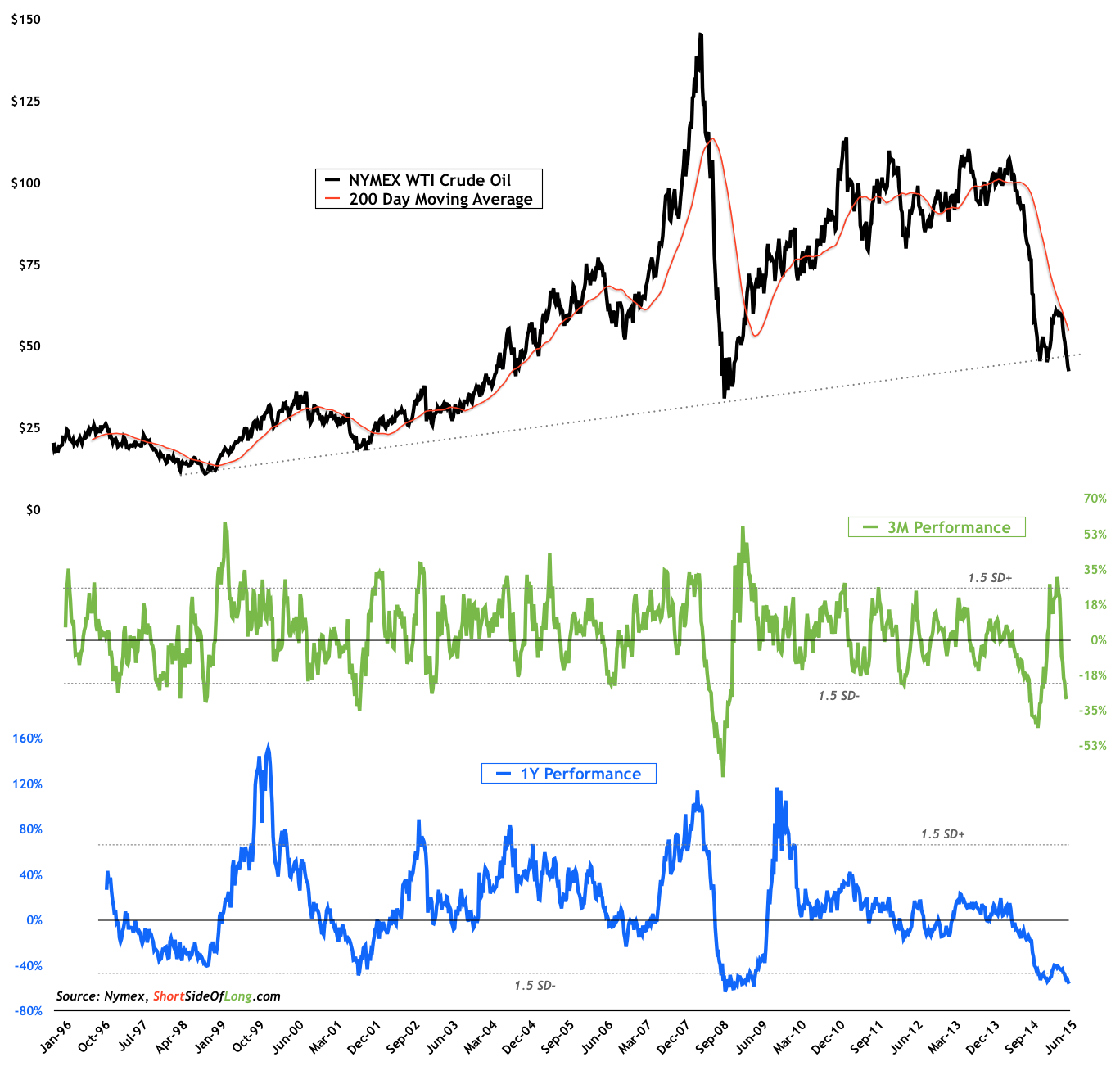

The third way would be to buy deeply-distressed, out of favor, cyclical assets and then resell upon the top of the next cycle. Gold mining is a difficult, boom/bust business, for example–see Barrons Gold Mining Index below. All businesses are somewhat cyclical, but commodity producers are hugely cyclical with long multi-year cycles due to the nature of mining-it takes years and high expense to reopen a mine and even if I gave you $2 billion and several years, you and your expert team may not be able to find an economic deposit. Note the five-to-ten year cycles below.

We are focusing on the third way, but in no way do I suggest that this is for you. You need to be your own judge. There is a big catch in this approach, you need to choose quality assets and/or companies with managements that do not over-leverage their firms during good times or overpay for acquisitions during the booms (or you could choose leveraged firms but be aware of the added risk and size accordingly becasue when a turn occurs, the leveraged firms rise the most). You also need to seek out a period of MAXIMUM pessimism which is difficult to do. How do you know that the market has FULLY discounted the bad news? Finally, YOU must be prepared to invest with a five-to-ten year horizon while expecting declines of over 50%. That concept alone will make you unique. Probably most will turn away from such requirements.

We last studied Dave Iben, a global contrarian investor, in this post: http://csinvesting.org/tag/david-iben/. You should read, Its Still Rock and Roll To Me at http://kopernikglobal.com/content/news-viewsand listen to the last few conference calls at the right side of the web-page. Note Mr. Iben’s philosophy, approach, and Holdings. His portfolio is vastly different than most money managers or indexers. But being an contrarian takes fortitude and patience. Kopernik Global performance since inception:

Next preview the readings below.

First you need to understand Austrian Business Cycle Theoryto grasp how massive mal-investment occurs. Why does China have newly built ghost cities? Distortion of interest rates causes mal-investment (the boom) then the inevitable correction because the boom was not financed out of real savings.

Why is the bust so severe for mining/commodity producers? Read Skousen’s book on the structure of production. Think of a swing fifty feet off the ground and 200 feet long. If you are sitting near the center of the swing’s fulcrum (nearest the consumer), then the ups and downs are much less than being on the end of the swing furthest from the consumer (the miners and commodity producers).

Then Throwing in the towel on Vale. I am not picking on Prof. Damordaran because we all make mistakes, and he graciously has provided a case study for us. Study the posts and the comments.

Can you think of several research errors he made (BEFORE) he invested?

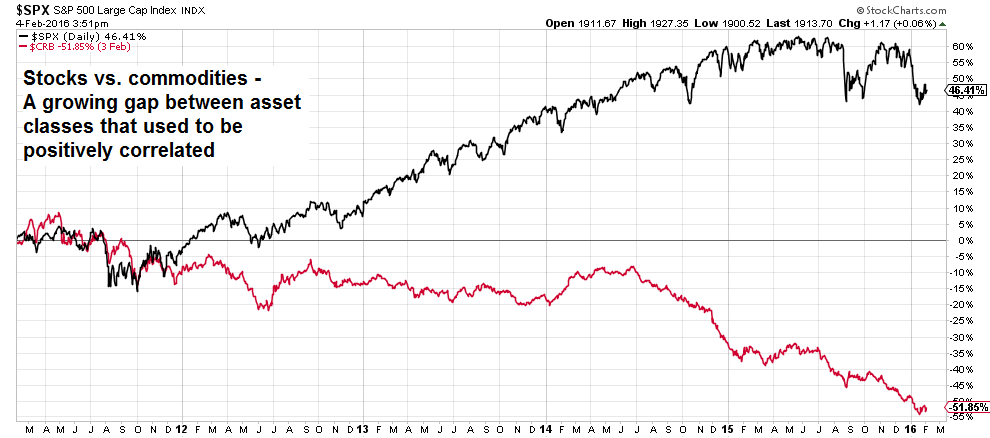

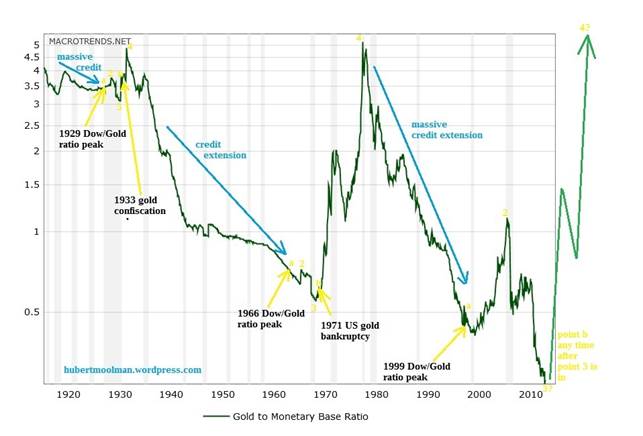

Remember in the prior post, the long-term chart of the CRB index showing commodities at 41-year lows since the CRB Index is below 175 or back to 1975 prices? Then why, if gold is a commodity, doesn’t gold trade at $200 or at least down to $500 to $700 as the gold chart from that time shows?

Why, if gold is money, doesn’t gold trade in US Dollars at $15,000 or the estimated price to back US Dollars by 100% in gold? You can change the amount to $10,000 or $20,000, but you get the idea.

Try thinking through those questions. Can we use what we learned from gold to value oil?

—

I will continue with Part III once readers have had several days to digest the readings and at least three readers try to answer at least one question. Until then……………………….be a contrarian not contrary.

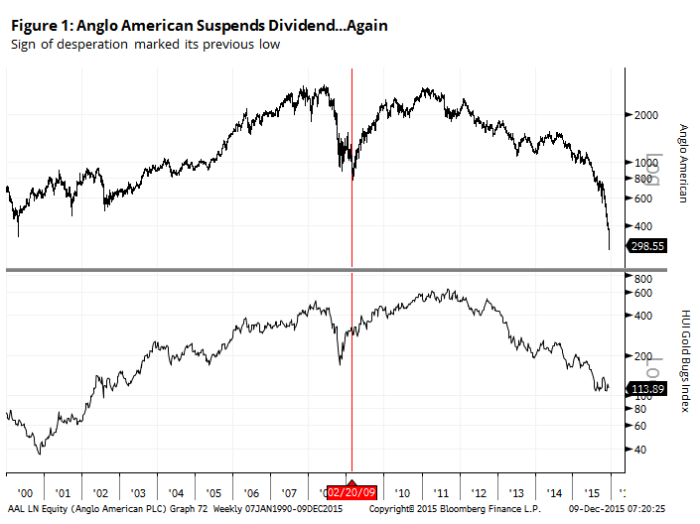

Anglo Suspends Dividend (Ringing a bell) We are watching collective capitulation by shareholders and management (a sign of the beginning of the end of the bear trend).

At lows, commodity price narrative is pure supply and demand with LIMITLESS SUPPLY (oil) and anemic demand (China slowdown) while at highs the narrative for commodities is driven by financial speculation (China boom/Commodity Super Cycle). Buy low and sell high.

Climbers say that when you are over 24,000 feet, you enter the “Death Zone. Mistakes become lethal.

The death zone is the name used by mountain climbers for high altitude where there is not enough oxygen for humans to breathe. This is usually above 8,000 metres (26,247 feet).[1] Most of the 200+ climbers who have died on Mount Everest have died in the death zone.[1] Due to the inverse relationship of air pressure to altitude, at the top of Mount Everest the average person takes in about 30% of the oxygen in the air that he or she would take in at sea level; a human used to breathing air at sea level could only be there for a few minutes before they became unconscious.[1] Most climbers have to carry oxygen bottles to be able to reach the top. Visitors become weak and have inability to think straight and struggle making decisions, especially under stress. WIKI

So what does this have to do with investing? When you pay too much for growth or quality, you may never recover. VALUATIONS MATTER ALWAYS!

First review the Nifty-Fifty Era when fifty stocks were “must own” for institutions in the 1970s due to their growth and quality. Money managers herded into them similar to this: Money Managers Herding Video.

valuing-growth-stocks-revisiting-the-nifty-fifty (Note page 22, you as an investor would have eventually broke even, but almost no one would have been able to seat through the 1980’s UNDER-PERFORMING a declining stock market!

Nifty Fifty Ignore the second half of these notes.

Now think about how the pattern repeated in the Internet years of 1996 to 2000 when MSFT and INTC were the must own stocks of their era.

Congratulations! If you bought back in 1999/2000 when the press was lauding these “must own” stock for the future, you are now in the black.

Even if you pay too much for stable, high quality companies, you can lose even as the companies grow sales, cash flows and earnings year after year after year. Note: KO_VL_Jan 2013 (See P/E ratio as a proxy for investor enthusiasm and compare to financial metrics). What is not to like? So why did the price go sideways for almost a decade after 1998? Investors adjusted their expectations.

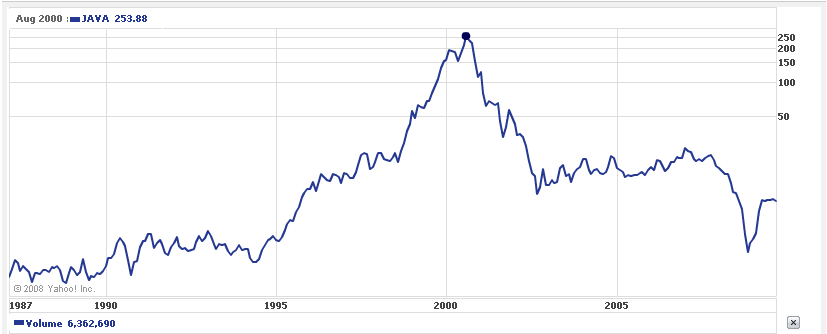

Sun MicroSystems Case Study

One thing to never forget is that the market is mostly efficient but not ALWAYS efficient or correct. 2 plus 2 equals 4 not 10. The last Internet frenzy gives a perfect case study in Sun Microsystems (SUN).

Sun Microsystems has always intrigued me. For a number of years, it seemed as if the company could do no wrong. During the early 1990′s, Sun occupied the top position in high performance computer workstations, a category of computing that has since virtually disappeared thanks to advances in PC hardware. Despite desperate attempts to unseat it from its leadership position by worthy competitors like HP, DEC, and IBM, Sun was able to prevail.

If you had purchased Sun stock in May of 1994, you’d have seen it skyrocket to nearly 100 times its value by August of 2000, just 6 years later. Had you kept it at the historical high price of $253/share, you’d have seen your investment lose more than 98% of its value when it came back down to just $3.17 a share by October 2008.

SUNW/JAVA stock price meteoric 100x rise and fall

It is easy to pull out a historical chart and say, “Look at the bubble popping.” But note what the CEO had to say about the price of his company’s stock in 2002:

Q: Sun’s stock hit a high of $64 or adjusted in the chart above of $250. Did you think what tech stocks were doing two years ago was too good to be true? (Date of the interview was March 2002).

A: No, she trained me well, and the stock made a nice move since we got married. But two years ago (2000) we were selling at 10 times revenues when we were at $64. At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?

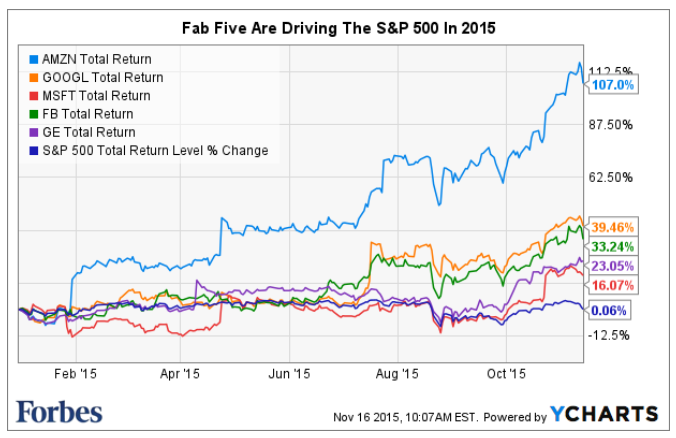

Now, the same music is playing but the players have changed.

Are now driving the performance of the general stock indexes:

The Fab Five are “NEED TO OWN” stocks for money managers who wish to NOT underperform in the short-term.

GE_VL certainly the the financial metrics, growth, and rising stocks prices make these easy “one-decision” stocks.

Let’s take AMZN because this company has a dominant position in retail that seems to be growing.

Amazon Key Stats

Trailing PE: 950.63

Forward PE: 117.65

Market Cap: $311.04 billion

Book Value: $26.50 per share

Share Price: $663.54

Price/Book: 24.27

Read more at How Amazons Long Game Yielded a Retail Juggernaut. Can’t you see many Americans becoming addicted to Amazon’s Prime service? Poor Wal-Mart and other retailers. However, IFAMZN doubles in market cap over the next 10yrs or a 7% annual return, and ends up trading at 21.9x earnings (current SPX p/e) in 2025, it needs to grow net income 55%/yr! Since 1973, 0.28% of companies have grown earnings at 55% for 10 years (Source: O’Shaughnessy). Do you like those odds? Or are you so smart that you can tell that AMZN will win the lottery?

While valuation augur for CAUTION for stocks IN GENERAL:

I started at page one [of these manuals-Moody’s and Value-Line] and went through every company that traded, from A to Z. When I was done I knew something about every company in the book.

I like businesses that I can understand. Let’s start with that. That narrows it down by 90%. There are all types of things I don’t understand, but fortunately, there is enough I do understand. You have this big wide world out there and almost every company is publicly owned. So you have all American business practically available to you. So it makes sense to go with things you can understand.

First, you need two piles. You have to segregate businesses you can understand and reasonably predict from those you don’t understand and can’t reasonably predict. An example is chewing gum versus software. You also have to recognize what you can and cannot know. Put everything you can’t understand or that is difficult to predict in one pile. That is the too-hard pile. Once you know the other pile, then it’s important to read a lot, learn about the industries, get background information, etc. on the companies in those piles. Read a lot of 10Ks and Qs, etc. Read about the competitors. I don’t want to know the price of the stock prior to my analysis. I want to do the work and estimate a value for the stock and then compare that to the current offering price. If I know the price in advance it may influence my analysis. We’re getting ready to make a $5 billion investment and this was the process I used.

You have to turn over a lot of rocks to find those little anomalies. You have to find the companies that are off the map – way off the map. You may find local companies that have nothing wrong with them at all

Most people get interested in stocks when everyone else is. The time to get interested is when no one else is. You can’t buy what is popular and do well.

I don’t look to jump over 7-foot bars: I look around for 1-foot bars that I can step over.

If we were to do it over again, we’d do it pretty much the same way. The world hasn’t changed that much. We’d read everything in sight about businesses and industries we think we’d understand. And, working with far less capital, our investment universe would be far broader than it is currently.

7 Gems from Buffet on Analyzing Stocks

You don’t need to be an expert in order to achieve satisfactory investment returns. But if you aren’t, you must recognize your limitations and follow a course certain to work reasonably well. Keep things simple and don’t swing for the fences. When promised quick profits, respond with a quick “no.”

There’s nothing different, in my view, about analyzing securities today vs. 50 years ago.

We favor businesses where we really think we know the answer. If we think the business’s competitive position is shaky, we won’t try to compensate with price. We want to buy a great business, defined as having a high return on capital for a long period of time, where we think management will treat us right. We like to buy at 40 cents on the dollar, but will pay a lot closer to $1 on the dollar for a great business.

Munger: Margin of safety means getting more value than you’re paying. There are many ways to get value. It’s high school algebra; if you can’t do this, then don’t invest.

If you’re going to buy a farm, you’d say, “I bought it to earn $X growing soybeans.” It wouldn’t be based on what you saw on TV or what a friend said. It’s the same with stocks. Take out a yellow pad and say, “If I’m going to buy GM at $30, it has 600 million shares, so I’m paying $18 billion,” and answer the question, why? If you can’t answer that, you’re not subjecting it to business tests.

Capital-intensive industries outside the utility sector scare me more. We get decent returns on equity. You won’t get rich, but you won’t go broke either. You are better off in businesses that are not capital intensive.

No formula in finance tells you that the moat is 28 feet wide and 16 feet deep. That’s what drives the academics crazy. They can compute standard deviations and betas, but they can’t understand moats. Maybe I’m being too hard on the academics.

7 Nuggets from Buffett on Valuing Stocks

When Charlie and I buy stocks which we think of as small portions of businesses our analysis is very similar to that which we use in buying entire businesses. We first have to decide whether we can sensibly estimate an earnings range for five years out, or more. If the answer is yes, we will buy the stock (or business) if it sells at a reasonable price in relation to the bottom boundary of our estimate. If, however, we lack the ability to estimate future earnings which is usually the case we simply move on to other prospects. In the 54 years we have worked together, we have never foregone an attractive purchase because of the macro or political environment, or the views of other people. In fact, these subjects never come up when we make decisions.

In 1986, I purchased a 400-acre farm, located 50 miles north of Omaha, from the FDIC. It cost me $280,000, considerably less than what a failed bank had lent against the farm a few years earlier. I knew nothing about operating a farm. But I have a son who loves farming, and I learned from him both how many bushels of corn and soybeans the farm would produce and what the operating expenses would be. From these estimates, I calculated the normalized return from the farm to then be about 10%. I also thought it was likely that productivity would improve over time and that crop prices would move higher as well. Both expectations proved out.

Intrinsic value is terribly important but very fuzzy. We try to work with businesses where we have fairly high probability of knowing what the future will hold. If you own a gas pipeline, not much is going to go wrong. Maybe a competitor enters forcing you to cut prices, but intrinsic value hasn’t gone down if you already factored this in. We looked at a pipeline recently that we think will come under pressure from other ways of delivering gas [to the area the pipeline serves]. We look at this differently from another pipeline that has the lowest costs [and does not face threats from alternative pipelines]. If you calculate intrinsic value properly, you factor in things like declining prices.

Investors making purchases in an overheated market need to recognize that it may often take an extended period for the value of even an outstanding company to catch up with the price they paid.

We use the same discount rate across all securities. We may be more conservative in estimating cash in some situations.

Just because interest rates are at 1.5% doesn’t mean we like an investment that yields 2-3%. We have minimum thresholds in our mind that are a whole lot higher than government rates. When we’re looking at a business, we’re looking at holding it forever, so we don’t assume rates will always be this low.

The appropriate multiple for a business compared to the S&P 500 depends on its return on equity and return on incremental invested capital. I wouldn’t look at a single valuation metric like relative P/E ratio. I don’t think price-to-earnings, price-to-book or price-to-sales ratios tell you very much. People want a formula, but it’s not that easy. To value something, you simply have to take its free cash flows from now until kingdom come and then discount them back to the present using an appropriate discount rate. All cash is equal. You just need to evaluate a business’s economic characteristics.

More Reading

Most of these quotes came from Buffett FAQ which contains the Q&A from shareholder meetings and goes beyond what you’ll find in the annual letters.

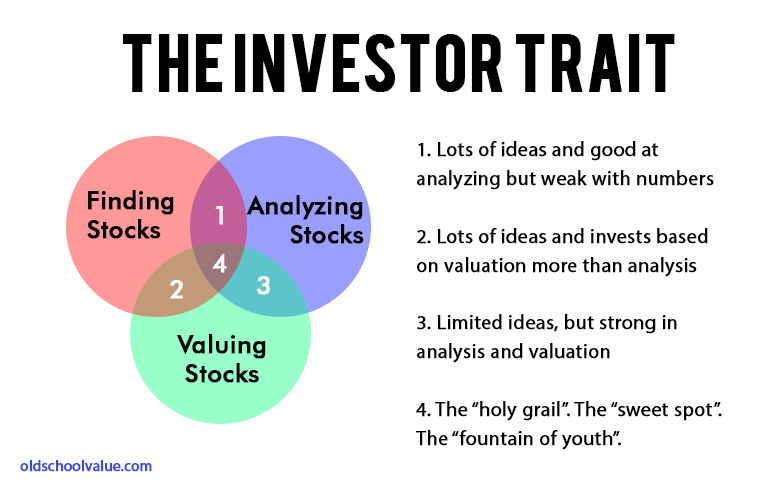

Just from these small selection of quotes, you can see how Buffett manages to dance in zone 4.

{kind=link}