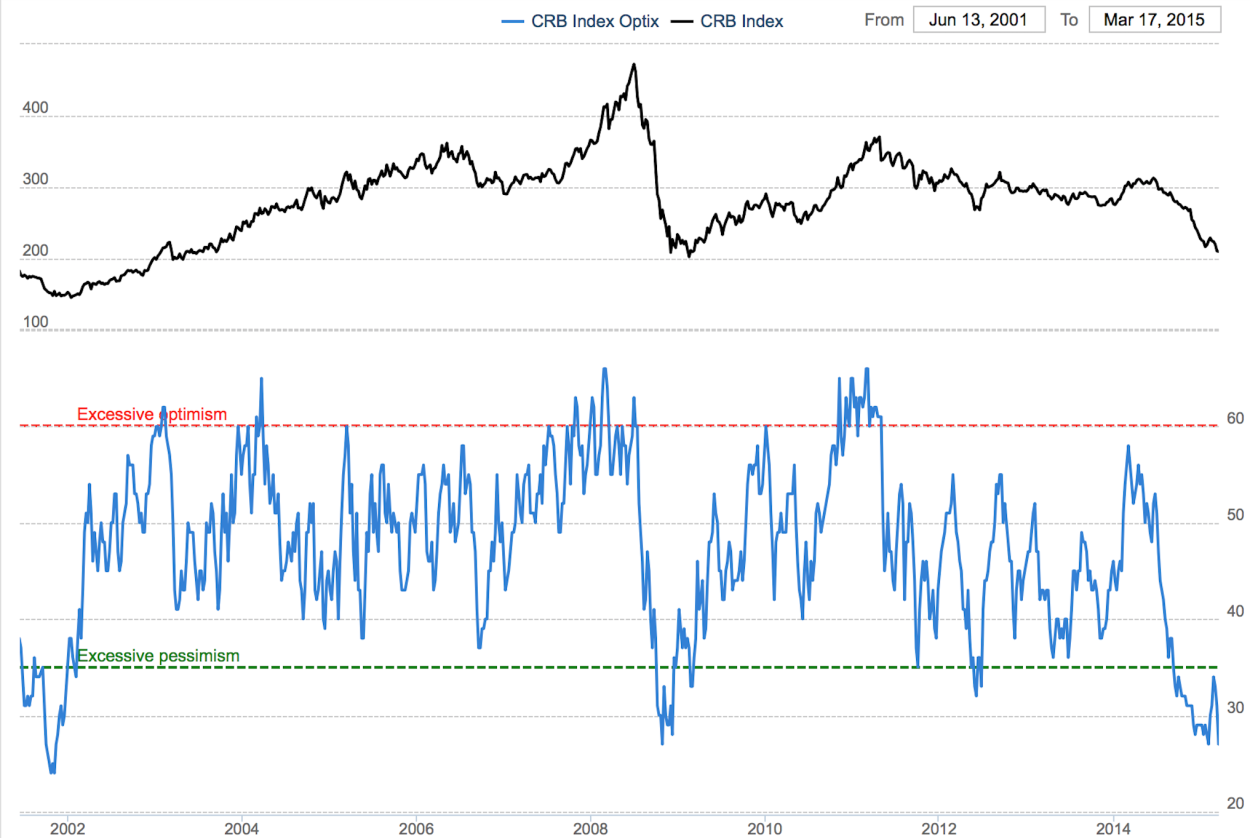

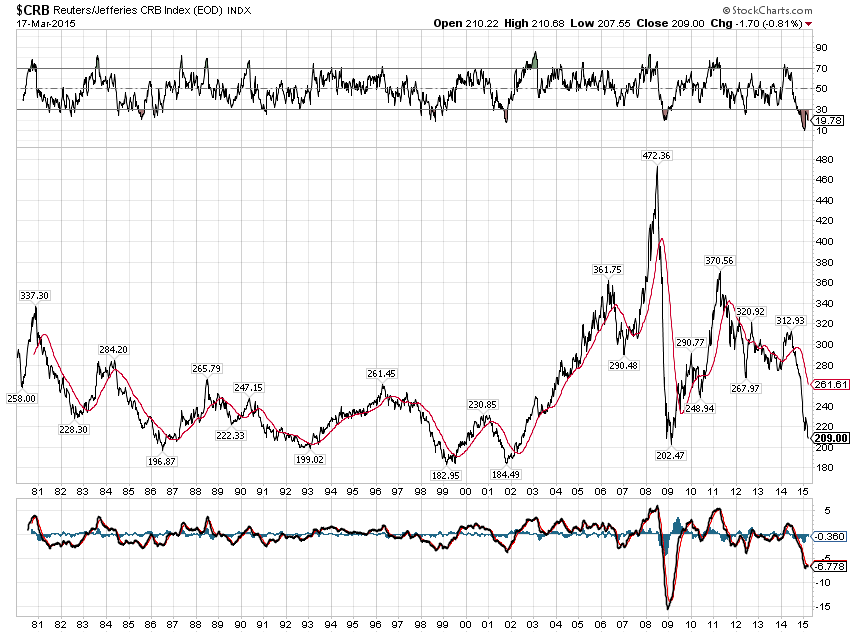

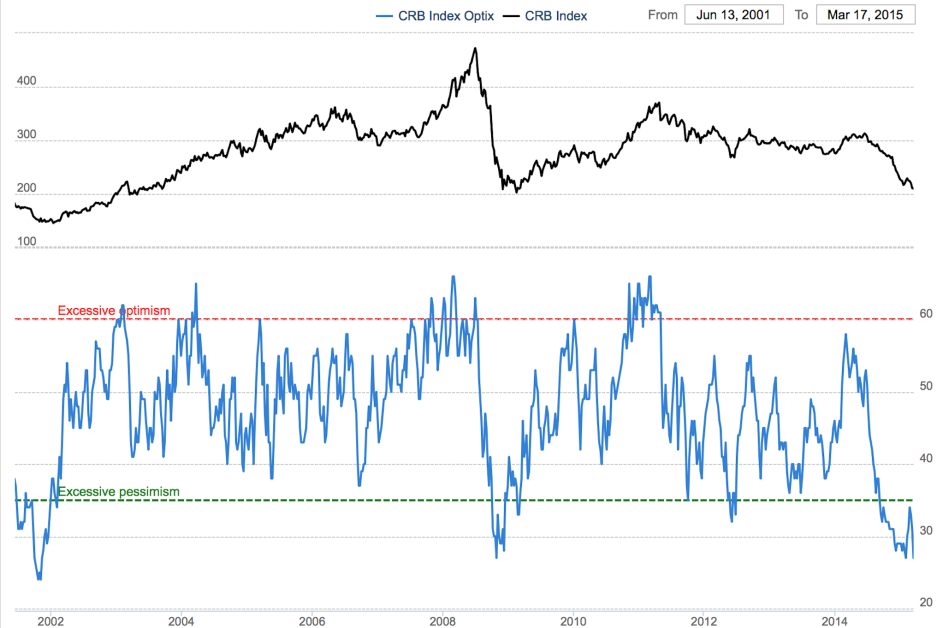

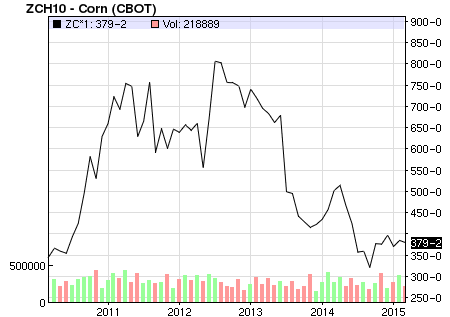

Commodities (CRB Index) fall back to a 40-year support zone ($185/$205)

while:

As global commodities prices plummet, it’s incredibly convenient to pronounce the commodities super-cycle dead, isn’t it? Yet banks from Goldman Sachs to Citigroup to Deutsche Bank are on record as saying it’s over. http://www.wallstreetdaily.com/2014/12/08/jim-rogers-commodities-interview/

The point is not to follow the “experts” but search where there is carnage. I am looking at Templeton’s Russian and Eastern Europe Fund TRF Semi Annual Report because:

Hated Countries (Russia, Ukraine)

Currencies Down,

Commodity Exporters and

trading at a 10% discount so the 1.4% management fee is covered for six years.

Poor performance for the past few years

Things can and will probably get worse. So please don’t follow the blind (me) off the cliff. This is meant as an example of a SEARCH STRATEGY.

—

More on Reversion to the Mean and the Growth Illusion

We are beating this subject to death but you can’t understand how investing in bargains works without grasping these concepts.

Contrarian Strategy Extrapolation and Risk Abstract: Value strategies yield higher returns because these strategies exploit the sub-optimal behavior of the typical investor and not because these strategies are fundamentally riskier. Yes, this is an academic paper, but worth reading to understand WHY and HOW value (buying stocks with low expectations/and low price to business metrics like earnings, cash flow, EBITDA, etc.) provide better returns.

Growth Illusion

The Two Percent Dilution It is widely believed that economic growth is good for stockholders. However, the cross-country correlation of real stock returns and per capita GDP growth over 1900–2002 is negative. Economic growth occurs from high personal savings rates and increased labor force participation, and from technological change. If increases in capital and labor inputs go into new corporations, these do not boost the present value of dividends on existing corporations. Technological change does not increase profits unless firms have lasting monopolies, a condition that rarely occurs. Countries with high growth potential do not offer good equity investment opportunities unless valuations are low.

Our last lesson was in Mean Reversion (Chapter 5 in Deep Value) discussed http://wp.me/p2OaYY-2Ju View this video on a very MEAN Reversion.

We must understand full cycles and reversion to the mean. Let’s move on to reading Chapter 2: A Blueprint to a better Quantitative Value Strategy in Quantitative Value.

Investors should be skeptical of history-based models. Constructed by a nerdy-sounding priesthood using esoteric terms such as beta, gamma, sigma and the like, these models tend to look impressive. Too often, though, investors forget to examine the assumptions behind the symbols. Our advice: Beware of geeks bearing formulas. -Warren Buffett, Shareholder Letter, 2000.

A WONDERFUL BUSINESS

Greenblatt defined Buffett’s definition of a good business as a high Return on Capital (ROC) – EBIT/Capital

Capital is defined as fixed asses + working capital (current assets minus current liabilities) minus excess cash.

ROC measures how efficiently management has used the capital employed in the business. The measure excludes excess cash and interest-bearing assets from this calculation to focus only on those assets actually used in the business to generate the return.

A BARGAIN PRICE

High earning yield = EBIT/TEV

TEV + Market Cap. + Total debt – minus excess cash + Preferred Stock + minority interests, and excess cash means cash + current assets – current liabilities.EBIT/TEV enables and apples-to-apples comparison of stock with different capital structures.

Improving on the Magic Formula?

ROC defined as Gross profitability to total assets.

GPA = (Revenue – Cost of Goods Sold)/Total Assets

GPA is the “cleanest” measure of true economic profitability.

The authors found GPA outperformed as a quality measure the magic formula. Note on page 48, Table 2.3: Performance Stats for Common Quality Measures (1964 – 2011) that most simple quality measures do NOT provide any differentiation from the market!

The authors found that analyzing stocks along price and quality contours using the Magic Formula and its generic academic brother Quality and Price can produce market beating results

The authors: “Our study demonstrates the utility of a quantitative approach to investing. Relentlessly pursuing a small edge over a long period of time, through booms and busts, good economies and bad, can lead to outstanding investment results.”

Ok, let’s come back to quality and avoiding value/death traps in the later chapters (3 and 4) in Quantitative Value. We are just covering material in Chapter 2.

INVESTORS BEHAVING BADLY

Investors and the Magic Formula

Adding Your Two Cents May Cost a Lot Over the Long Term by Joel Greenblatt

01-18-2012 (Full article: Adding Your Two Cents

Gotham Asset Management managing partner and Columbia professor Joel Greenblatt explains why investors who ‘self-managed’ his Magic Formula using pre-approved stocks underperformed the professionally managed systematic accounts.

So, what happened? Well, as it turns out, the self-managed accounts, where clients could choose their own stocks from the pre-approved list and then follow (or not) our guidelines for trading the stocks at fixed intervals didn’t do too badly. A compilation of all self-managed accounts for the two-year period showed a cumulative return of 59.4% after all expenses. Pretty darn good, right? Unfortunately, the S&P 500 during the same period was actually up 62.7%.

“Hmmm….that’s interesting”, you say (or I’ll say it for you, it works either way), “so how did the ‘professionally managed’ accounts do during the same period?” Well, a compilation of all the “professionally managed” accounts earned 84.1% after all expenses over the same two years, beating the “self managed” by almost 25% (and the S&P by well over 20%). For just a two-year period, that’s a huge difference! It’s especially huge since both “self-managed” and “professionally managed” chose investments from the same list of stocks and supposedly followed the same basic game plan.

Let’s put it another way: on average the people who “self-managed” their accounts took a winning system and used their judgment to unintentionally eliminate all the outperformance and then some! How’d that happen?

1. Self-managed investors avoided buying many of the biggest winners.

How? Well, the market prices certain businesses cheaply for reasons that are usually very well-known (The market is a discounting mechanism). Whether you read the newspaper or follow the news in some other way, you’ll usually know what’s “wrong” with most stocks that appear at the top of the magic formula list. That’s part of the reason they’re available cheap in the first place! Most likely, the near future for a company might not look quite as bright as the recent past or there’s a great deal of uncertainty about the company for one reason or another. Buying stocks that appear cheap relative to trailing measures of cash flow or other measures (even if they’re still “good” businesses that earn high returns on capital), usually means you’re buying companies that are out of favor.

These types of companies are systematically avoided by both individuals and institutional investors. Most people and especially professional managers want to make money now. A company that may face short-term issues isn’t where most investors look for near term profits. Many self-managed investors just eliminate companies from the list that they just know from reading the newspaper face a near term problem or some uncertainty. But many of these companies turn out to be the biggest future winners.

2. Many self-managed investors changed their game plan after the strategy under-performed for a period of time.

Many self-managed investors got discouraged after the magic formula strategy under-performed the market for a period of time and simply sold stocks without replacing them, held more cash, and/or stopped updating the strategy on a periodic basis. It’s hard to stick with a strategy that’s not working for a little while. The best performing mutual fund for the decade of the 2000’s actually earned over 18% per year over a decade where the popular market averages were essentially flat. However, because of the capital movements of investors who bailed out during periods after the fund had underperformed for a while, the average investor (weighted by dollars invested) actually turned that 18% annual gain into an 11% LOSS per year during the same 10 year period.[2]

3. Many self-managed investors changed their game plan after the market and their self-managed portfolio declined (regardless of whether the self-managed strategy was outperforming or underperforming a declining market).

This is a similar story to #2 above. Investors don’t like to lose money. Beating the market by losing less than the market isn’t that comforting. Many self-managed investors sold stocks without replacing them, held more cash, and/or stopped updating the strategy on a periodic basis after the markets and their portfolio declined for a period of time. It didn’t matter whether the strategy was outperforming or underperforming over this same period. Investors in that best performing mutual fund of the decade that I mentioned above likely withdrew money after the fund declined regardless of whether it was outperforming a declining market during that same period.

4. Many self-managed investors bought more AFTER good periods of performance.

You get the idea. Most investors sell right AFTER bad performance and buy right AFTER good performance. This is a great way to lower long-term investment returns.

Go-where-it-is-darkest-when-company.html(Vale-Brazilian Iron Ore Producer). Prof. Damordaran values Vale and Lukoil on Nov. 20, 2015. I am looking at Vale because they have some of the lowest cost assets of Iron Ore in the world. They have good odds of surviving the downturn but where the trough is–who knows.

I think the author at least knew of the risks, but underestimated the extent of the cycle due to massive distortions caused by the world’s central banks. It did get darker..as iron prices fell another 10% and still falling.

Month

Price Iron Ore

Change

Aug 2014

92.63

–

Sep 2014

82.27

-11.18 %

Oct 2014

80.09

-2.65 %

Nov 2014

73.13

-8.69 %

Dec 2014

68.80

-5.92 %

Jan 2015

67.39

-2.05 %

Feb 2015

62.69

-6.97

Damodaran: I have not updated my valuation of Vale (as of Feb. 20th), but I have neither sold nor added to my position. It is unlikely that I will add to my position for a simple reason. I don’t like doubling down on bets, even if I feel strongly, because I feel like I am tempting fate.

Prof. Damodaran is responding to a poster who is asking about Vale’s plummeting stock price. If you are a long-term bull you want declining prices to bankrupt weak companies in the industry so as to rationalize supply.

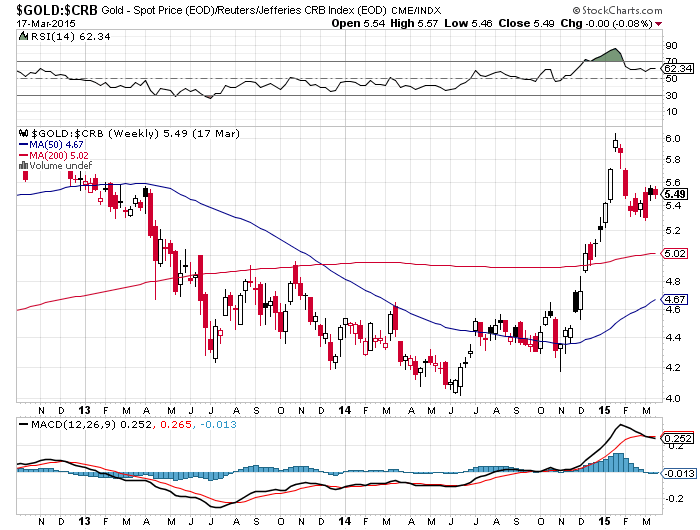

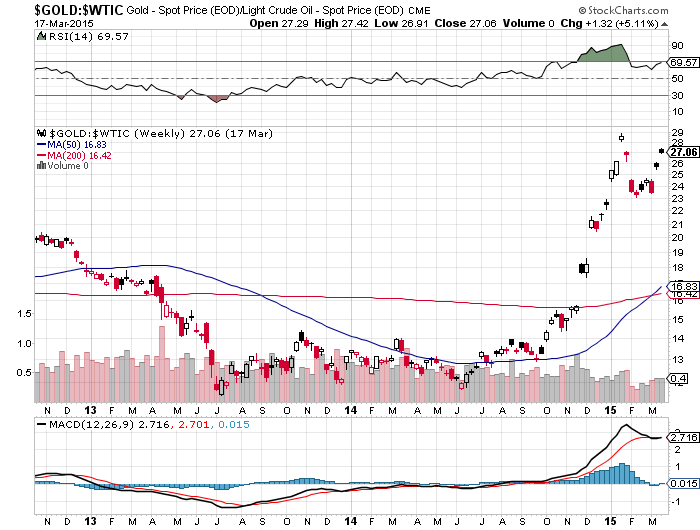

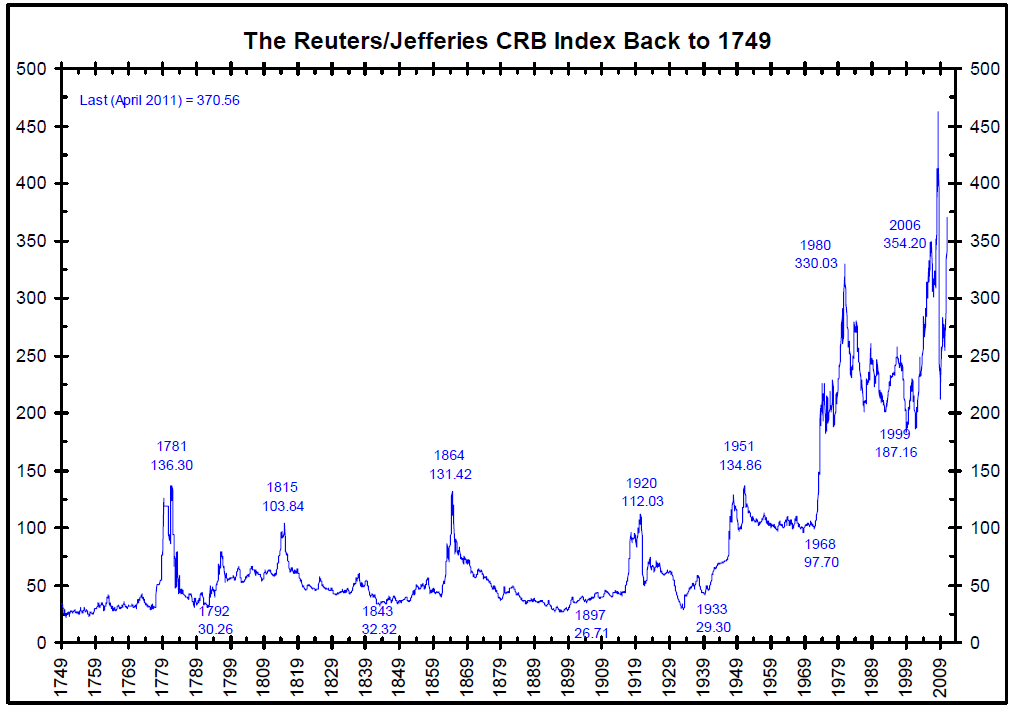

An early sign of a turn: Gold vs. the Commodity Research Bureau Index (CRB). Since gold is commodity money it is much more sensitive to changes in financial conditions than consumable commodities.

I like to take note of extremes. However, the amount of central bank monetary distortion is so huge (note negative interest rate on government debt, huge deficits, QE, etc.) that extremes can go to new levels but when investors are on one side of the boat–be careful.

Also, visit www.hussmanfunds.com

PS: Once I clear my backlog, I will return to our lessons in Deep Value and Quantitative Value. Plus post the links to the videos of valua investing classes.

As an example, if you want to invest with more (RELATIVE) safety in the cyclical oil service business, you would want a company like this: RPC Inc (RES)

Note balance sheet and good operating metrics. It doesn’t mean that RPC, Inc. can’t go materially lower in price, just that the company has a high probability of surviving through this down cycle compared to competitors.

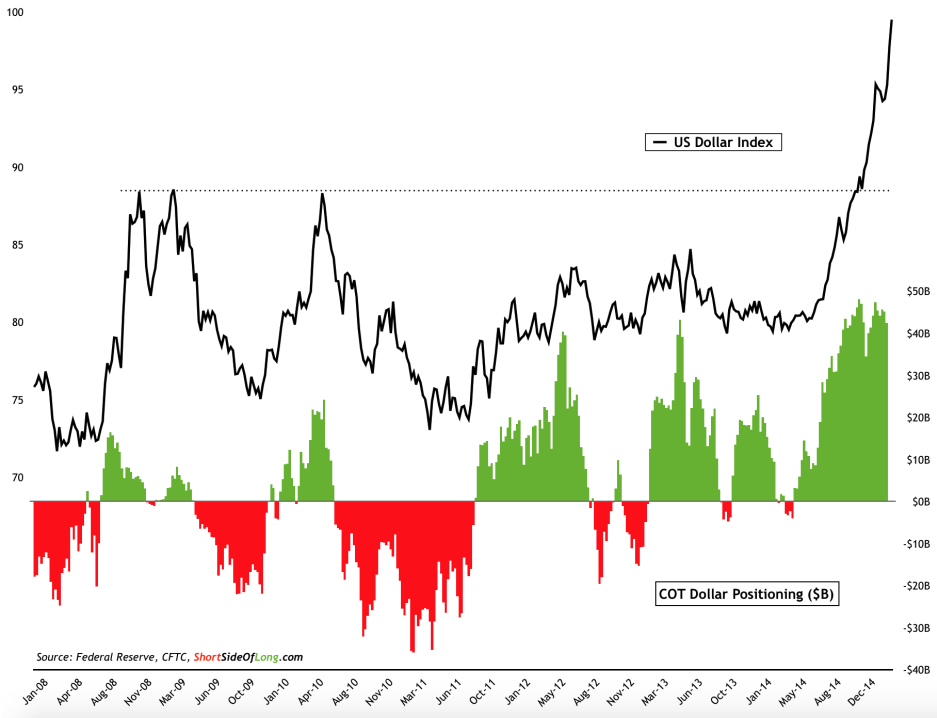

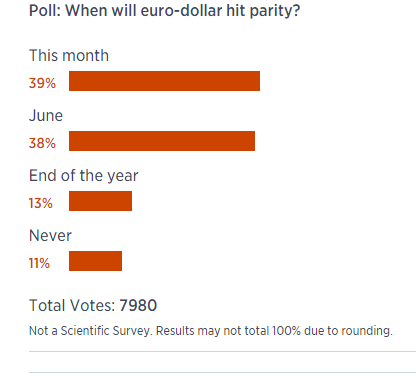

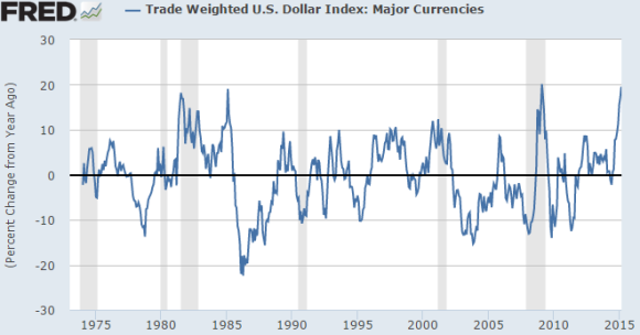

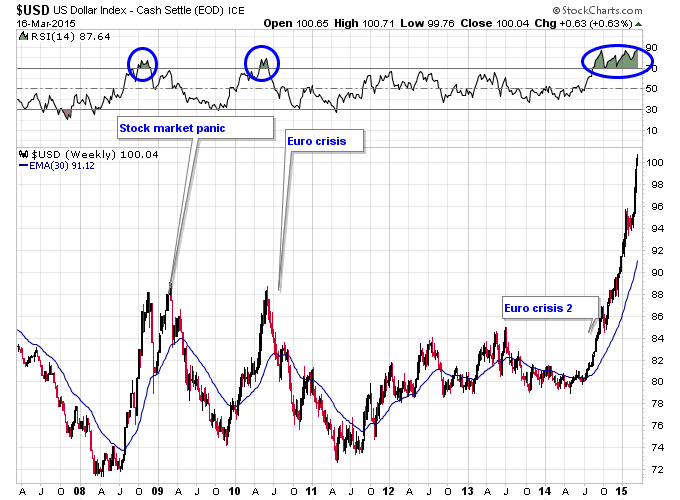

Oil service, oil producers, mining companies etc. are being hammered by a dollar “shortage.” Opportunity may be knocking. Remember what Klarman said about forced selling.

An overview of the situation: Dollar Shortage. With money supply rising in the US there is no dollar “shortage”, but there is a fear of inter-bank lending.

A Reader’s Question on Valuation Ratios. This sheet may be good as a guide to go through an annual report, but none of those ratios means anything without context. Is growth good? It depends. Only profitable growth within a franchise. How about asset turnover? For some companies like Costco asset turnover is critical but not for Boeing (gross margin). Why not take those ratios and work through the financials of these trucking companies. Which company is doing the best? Why? Follow the money! Those ratios may help you structure the information you pull out from the financials. But first focus on how does the company provide a service to its customers and then trace the financial effects back to your returns as an investor.

We will get back to Deep Value next week and I will post links to valuation class videos. Have a great weekend and if you do try to emulate someone, then:

Times are hard. Your family has been struggling to make the mortgage payments on your farm since the 50% decline in corn prices.

Your lucky day! You get a call from a friend’s neighbor that he (The Pigeon King) desperately needs breeders for his growing pigeon business. With a $125,000 investment financed with a second mortgage against your farm you can buy 360 pairs of pigeons at $165 a pair. Then he offers to buy back the newly bred pigeons for $40 each (pigeons breed prolifically) with a ten-year contract. He says these pigeons are for racing. Then he gives you a list of five farmers in your state who are breeding pigeons for him. Take your time and do your due-diligence, he says.

You check his credit ratings–all good. No criminal or civil complaints. He owns his farm free and clear–he is a farmer like you! After meeting with three of the pigeon farmers who confirm with check stubs that he has been paying them on time and as promised. The returns are good–in excess of 80% to 100% in terms of food and overhead to raise the chicks. Considering your time to look over your pigeons, you figure you can net a 50% pre-tax return on your capital. Plus, your contract allows you to sell whatever you produce at the stipulated price, so growth will be profitable.

Times are hard. What do you do? Before you decide, you are inspired by

You gotta have dreams and the will to believe!

You remember what you learned as a deep value investor over at csinvesting.org and you_________? Why? What INVESTING/BUSINESS principles help you in your decision?

This article, The Pigeon King (same as the link above but with additional commentary for easier reading) is one of the most amazing stories–a farce, a tragedy, a comedy AND chock full of lessons for the investor. You may think you are too smart to be a pigeon or a bird-brain (sorry!) but ANYONE can be blind. What checklist items stop you (besides it’s too good to be true?).

I enjoyed reading Berkshire -Past, Present and Future, pages 24-28 2014ltr

Mr. Buffett’s anger at Stanton’s chiseling cost dearly because he didn’t sell at the first puff of the “cigar-butt” (Berkshire’s Textile Division). Buffett suffered in a value trap.

Notably, Buffett’s cigar-butt strategy worked well when managing small sums–the best of Buffett’s life in terms of relative and absolute investment performance. However, cigar-butt investing was not scalable or enduring with larger sums. Buffett then turned towards buying wonderful businesses at fair prices or, in other words, franchises with honest and able management.

His investment in See’s Candies was a turning point because the company generated high returns on invested capital which Buffett could then redeploy into other businesses. Note that See’s could only grow profitably within a defined region (Calif.?). A powerful brand coupled with economies of scale makes for a great business.

Berkshire Today (page 29) provides a description of Conglomerates and the mania that occurred in the 1960s with ponzi-scheme pooling of interests accounting and ever-rising P/E multiples–until the game crashed.

Buffett points out the folly of spin-offs, whereby the owning company loses purported “control-value” without any compensating payment. Investment bankers and private equity buccaneers were heartily savaged by Mr. Buffett’s pen.

Before we dig deeper into Chapter Five in Deep Value, I thought we should read Chapter 2 in Quantitative Value so as to not skip over several important points. I will make sure new students receive a link to the books in the course.

Decades ago, Ben Graham pinpointed the blame for investment failure, using a quote from Shakespeare: “The fault, dear Brutus, is not in our stars, but in ourselves.”

Comments on the Berkshire Hathaway 2014 letter, Part 1

Note the plug (page 6) for Where Are the Customers’ Yachts by Fred Schwed. That along with the Money Game by Adam Smith will teach you the ways of Wall Street. Also, see:

Intrinsic Value: Buffett reiterates that it is not a precise number for Berkshire nor, in fact for ANY stock.

GEICO delivers savings to its customers because it is a low-cost operation (source of structural competitive advantage). The company’s low costs create a moat—an enduring one—that competitors are unable to cross. Note Buffett’s comment on the animated gecko, a LOW-COST spokesperson.

TESCO

Here’s how he explained it:

“In 2013, I soured somewhat on the company’s then-management and sold 114 million shares, realizing a profit of $43 million. My leisurely pace in making sales would prove expensive. Charlie calls this sort of behavior “thumb-sucking.” (Considering what my delay cost us, he is being kind.)

“During 2014, Tesco’s problems worsened by the month. The company’s market share fell, its margins contracted and accounting problems surfaced. In the world of business, bad news often surfaces serially: You see a cockroach in your kitchen; as the days go by, you meet his relatives.”

Buffett said the dawdling resulted in an after-tax loss of $444 million by the time Berkshire was no longer a Tesco shareholder. That, he added, is about 0.2% of Berkshire’s net worth. Only three times in 50 years has Berkshire recorded losses from a sale equal to more than 1% of its net worth.

Unfortunately, we don’t learn what exactly caused the loss. How did Buffett miscalculate intrinsic value? Did management worsen, but if so, then how can an investor sidestep that? I believe the economics changed as customers had more in-home deliveries and other choices coupled with poor store execution from Tesco. I was disappointed with this explanation of the Tesco loss, but Buffett would reply that it was only 1/5 of 1%.

Nominal vs. Real Returns

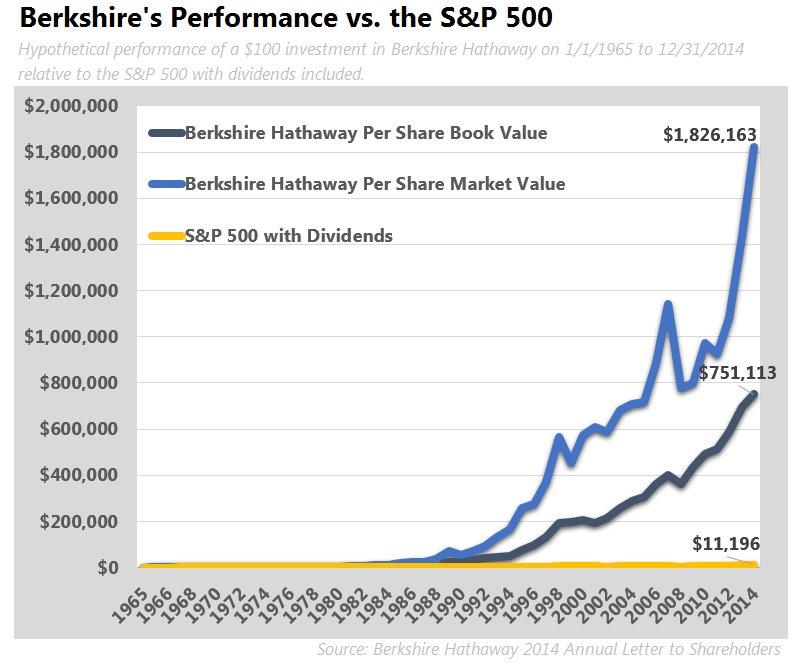

During the 1964-2014 period, the S&P 500 rose from 84 to 2,059, which, with reinvested dividends, generated the overall return of 11,196% shown on page 2. Concurrently, the purchasing power of the dollar declined a staggering 87%. That decrease means that it now takes $1 to buy what could be bought for 13 cents in 1965 as measured by the CPI (Flawed or whats wrong with cpi)

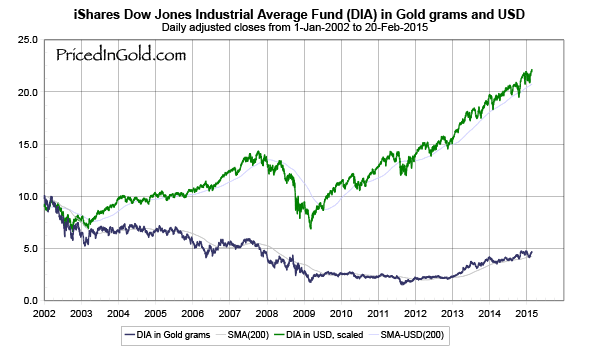

I prefer measuring in gold grams, because gold is a store of value and market-based rather than concocted by Federal bureaucrats.

There is an important message for investors in that disparate performance between stocks and dollars. Think back to our 2011 annual report, in which we defined investing as the transfer to others of purchasing power now with reasoned expectation of receiving more purchasing power–after taxes have been paid on nominal gains—in the future.” (I wonder why Mr. Buffett makes no mention of the financial repression of ZIRP and NIRP? It is the elephant in the room because of the devastating effect it has on savers and on calculating discount rates for investment.)

The unconventional, but inescapable, conclusion to be drawn from the past fifty years is that it has been far safer to invest in a diversified collection of American businesses than to invest in securities—Treasuries, for example—whose values have been tied to American currency. That was also true in the preceding half century, a period including the Great Depression and two world wars. Investors should heed this history. To one degree or another it is almost certain to be repeated during the next century. Buffett’s comments are backed up by history as shown here:and triumph_of_the_optimists

Stock prices will always be far more volatile than cash equivalent holdings. Over the long term, however, currency-denominated instruments are riskier investments—far riskier investments. Than widely –diversified stock portfolios that are bought over time and that are owned in a manner invoking only token fees and commissions. That lesson has not customarily been taught in business schools, where volatility is almost universally used as a proxy for risk. Though this pedagogic assumption makes for easy teaching, it is dead wrong. Volatility is far from synonymous with risk. Popular formulas that equate the two terms lead students, investors and CEOs astray.

It is true, of course, that owning equities for a day or a week or a year is far riskier (in both nominal and purchasing power terms) than leaving funds in cash-equivalents. That is relevant to certain investors-say, investment banks—whose viability can be threatened by declines in asset prices and which might be forced to sell securities during depressed markets. Additionally, any party that might have meaningful near-term needs for funds should keep appropriate sums in Treasuries or insured bank deposits.

For the great majority of investors, however, who can—and should—invest with a multi-decade horizon, quotational declines are unimportant. Their focus should remain fixed on attaining significant gains in purchasing power over their investing lifetime. For them, a diversified equity portfolio, bought over time, will prove far less risky than dollar-based securities.

Note the multi-decade horizon. Stocks were unchanged from 1964-1981, please see page 79: A Study of Market History through Graham Babson Buffett and Others. Read what Buffett has to say about stock markets. Some say it is Time to exit because of high valuations for big-cap stocks in the U.S. market. So even if stocks decline for a decade but your holding period is MULTI-Decade, then hold tight. Tough to do, but history seems to bear his thesis out: valuing-growth-stocks-revisiting-the-nifty-fifty. I prefer to act like the pig farmer in A Study of Market History (see link above).

If the investor, instead, fears price volatility, erroneously viewing it as a measure of risk, he may, ironically, end up doing some very risk things. Recall, if you will, the pundits who six years ago bemoaned falling stock prices and advised investing in “safe” Treasury bills or bank certificates of deposit. People who heeded this sermon (to panic) are now earning a pittance on sums they had previously expected would finance a pleasant retirement. (The S&P 500 was then below 700; now it is about 2,100.) If not for their fear of meaningless price volatility, these investors could have assured themselves of a good income for life by simply buying a very low-cost index fund whose dividends would trend upward over the years and whose principal would grow as well (with many ups and downs, to be sure).

Investors, of course, can, by their own behavior, make stock ownership highly risky. And many do. Active trading, attempts to “time” market movements, inadequate diversification, the payment of high and unnecessary to managers and advisors and the use of borrowed money can destroy the decent returns that a life-long owner of equities would otherwise enjoy. ….Anything can happen anytime in markets. And no advisor, economist, or TV commentator–and definitely not Charlie nor I–can tell you when chaos will occur. Market forecasters will fill your ear but will never fill your wallet.

A plug for Jack Bogle’s The Little Book of Common Sense Investing. Basically, Buffett is saying keep it simple, think and hold L O N G – T E R M, avoid high fees and commissions, and don’t use leverage.

Next, let’s look at Berkshire–Past, Present and Future in Part II

When an investor turns to the research on regression to the mean and investors overreacting to poor company performance/bad news in Richard Thaler research, he or she sees that prices of the winner and loser portfolios take three-to-seven years to revert. See also The New Finance: The Case Against Efficient Markets by Robert A. Haugen and Inefficient Markets by Andrei Schleifer.

Search Strategy: Go where the outlook is bleakest (John Templeton). Keep his wisdom by your side: Sixteen Rules for Investment Success_Templeton

Search Strategy: Go where the outlook is bleakest (John Templeton). Keep his wisdom by your side: Sixteen Rules for Investment Success_Templeton