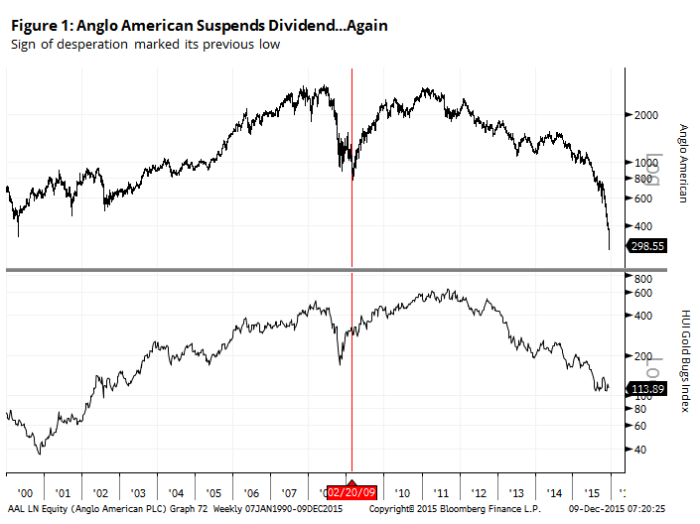

Anglo Suspends Dividend (Ringing a bell) We are watching collective capitulation by shareholders and management (a sign of the beginning of the end of the bear trend).

At lows, commodity price narrative is pure supply and demand with LIMITLESS SUPPLY (oil) and anemic demand (China slowdown) while at highs the narrative for commodities is driven by financial speculation (China boom/Commodity Super Cycle). Buy low and sell high.

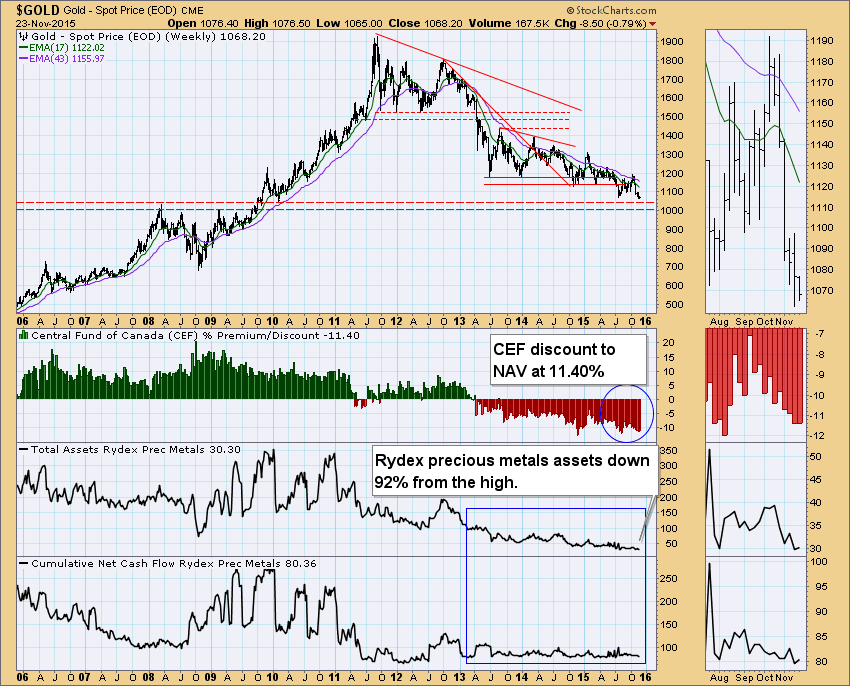

Note that CEF in the above chart trades at an 11% discount to its 60%/40% holding of gold and silver bullion after a four year down-trend–note that this is either hyper-bearishness or massive extrapolation of trend-following. Apple’s cash hoard could buy the entire public mining sector. Gold stocks are cheap for a reason: poor capital allocation, poor cost control, and dilution of shareholders revealed in the five-year long bust from an epic boom from 2001 to 2011 caused investors to flee. Since then many managements have gained religion on cost control and capital discipline (Note Barrick, ABX). All cycles turn, but when? If we knew, then no opportunity.

I always hear investors or analysts ask, “So what is the catalyst?” If the market is at all efficient–and I would say that it is except at major inflection points–then if we knew the catalyst, then the opportunity would be arbitraged away. How about the law of low prices or the law of supply and demand.

Ironically, as gold has declined in US dollar terms, it has risen in real terms versus commodities showing its mettle in a credit contraction. TSI BLOG

The HUI, a gold stock index, is showing relative strength versus gold. However, certain gold stocks like Novagold (NG), Sabina Gold (SGSVF) or Agnico-Eagle (AEM) are in incipient uptrends or, at least, vastly outperforming their indexes such as GDX or GDXJ. You must diversify amongst the highest quality producers, developers, and explorers.

This post is not a recommendation but a historical reference point for a hated asset class. I see much less RISK in a terrible industry such as gold mining than wonderful businesses such as Amazon, CRM, or GE.

Climbers say that when you are over 24,000 feet, you enter the “Death Zone. Mistakes become lethal.

The death zone is the name used by mountain climbers for high altitude where there is not enough oxygen for humans to breathe. This is usually above 8,000 metres (26,247 feet).[1] Most of the 200+ climbers who have died on Mount Everest have died in the death zone.[1] Due to the inverse relationship of air pressure to altitude, at the top of Mount Everest the average person takes in about 30% of the oxygen in the air that he or she would take in at sea level; a human used to breathing air at sea level could only be there for a few minutes before they became unconscious.[1] Most climbers have to carry oxygen bottles to be able to reach the top. Visitors become weak and have inability to think straight and struggle making decisions, especially under stress. WIKI

So what does this have to do with investing? When you pay too much for growth or quality, you may never recover. VALUATIONS MATTER ALWAYS!

First review the Nifty-Fifty Era when fifty stocks were “must own” for institutions in the 1970s due to their growth and quality. Money managers herded into them similar to this: Money Managers Herding Video.

valuing-growth-stocks-revisiting-the-nifty-fifty (Note page 22, you as an investor would have eventually broke even, but almost no one would have been able to seat through the 1980’s UNDER-PERFORMING a declining stock market!

Nifty Fifty Ignore the second half of these notes.

Now think about how the pattern repeated in the Internet years of 1996 to 2000 when MSFT and INTC were the must own stocks of their era.

Congratulations! If you bought back in 1999/2000 when the press was lauding these “must own” stock for the future, you are now in the black.

Even if you pay too much for stable, high quality companies, you can lose even as the companies grow sales, cash flows and earnings year after year after year. Note: KO_VL_Jan 2013 (See P/E ratio as a proxy for investor enthusiasm and compare to financial metrics). What is not to like? So why did the price go sideways for almost a decade after 1998? Investors adjusted their expectations.

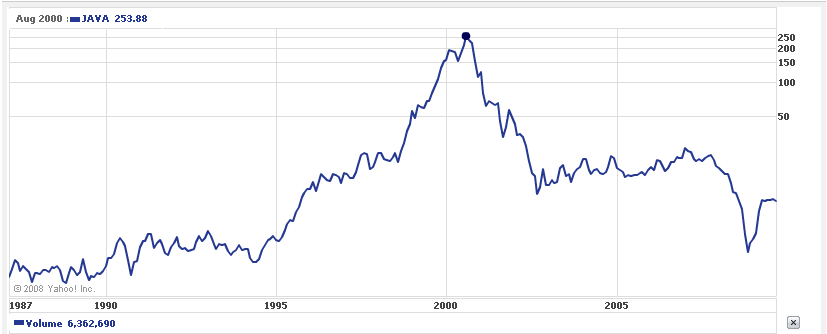

Sun MicroSystems Case Study

One thing to never forget is that the market is mostly efficient but not ALWAYS efficient or correct. 2 plus 2 equals 4 not 10. The last Internet frenzy gives a perfect case study in Sun Microsystems (SUN).

Sun Microsystems has always intrigued me. For a number of years, it seemed as if the company could do no wrong. During the early 1990′s, Sun occupied the top position in high performance computer workstations, a category of computing that has since virtually disappeared thanks to advances in PC hardware. Despite desperate attempts to unseat it from its leadership position by worthy competitors like HP, DEC, and IBM, Sun was able to prevail.

If you had purchased Sun stock in May of 1994, you’d have seen it skyrocket to nearly 100 times its value by August of 2000, just 6 years later. Had you kept it at the historical high price of $253/share, you’d have seen your investment lose more than 98% of its value when it came back down to just $3.17 a share by October 2008.

SUNW/JAVA stock price meteoric 100x rise and fall

It is easy to pull out a historical chart and say, “Look at the bubble popping.” But note what the CEO had to say about the price of his company’s stock in 2002:

Q: Sun’s stock hit a high of $64 or adjusted in the chart above of $250. Did you think what tech stocks were doing two years ago was too good to be true? (Date of the interview was March 2002).

A: No, she trained me well, and the stock made a nice move since we got married. But two years ago (2000) we were selling at 10 times revenues when we were at $64. At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?

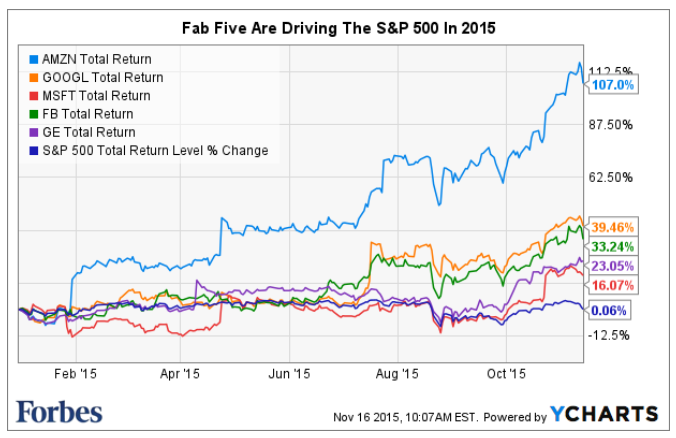

Now, the same music is playing but the players have changed.

Are now driving the performance of the general stock indexes:

The Fab Five are “NEED TO OWN” stocks for money managers who wish to NOT underperform in the short-term.

GE_VL certainly the the financial metrics, growth, and rising stocks prices make these easy “one-decision” stocks.

Let’s take AMZN because this company has a dominant position in retail that seems to be growing.

Amazon Key Stats

Trailing PE: 950.63

Forward PE: 117.65

Market Cap: $311.04 billion

Book Value: $26.50 per share

Share Price: $663.54

Price/Book: 24.27

Read more at How Amazons Long Game Yielded a Retail Juggernaut. Can’t you see many Americans becoming addicted to Amazon’s Prime service? Poor Wal-Mart and other retailers. However, IFAMZN doubles in market cap over the next 10yrs or a 7% annual return, and ends up trading at 21.9x earnings (current SPX p/e) in 2025, it needs to grow net income 55%/yr! Since 1973, 0.28% of companies have grown earnings at 55% for 10 years (Source: O’Shaughnessy). Do you like those odds? Or are you so smart that you can tell that AMZN will win the lottery?

While valuation augur for CAUTION for stocks IN GENERAL:

A few years ago Larry approached his Guadalajara neighbours and announced that he would buy monkeys for $10 each. The neighbours, seeing that there were many monkeys around, went out to the forest and started catching them. Larry bought thousands at $10 and, as supply started to diminish, the neighbours stopped their effort. He next announced that he would now buy monkeys at $20 each. This renewed the efforts of his neighbours and they started catching monkeys again. Soon the supply diminished even further and people started going back to their farms. The offer increased to $25 each and the supply of monkeys became so scarce it was an effort to even find a monkey, let alone catch it!

Larry now announced that he would buy monkeys at $50 each! However, since he had to go into town on some business, Darren, his son, would buy on his behalf. In the absence of Larry, Darren told the neighbours: “Look at all these monkeys in the big cage that my dad has already collected. I will sell them to you at $35 and when Dad returns from the city, you can sell them to him for $50 each.” The villagers rounded up all their savings and bought all the monkeys. They never saw Larry or Darren again, only lots and lots of monkeys! Now you have a better understanding of how the stock market works.

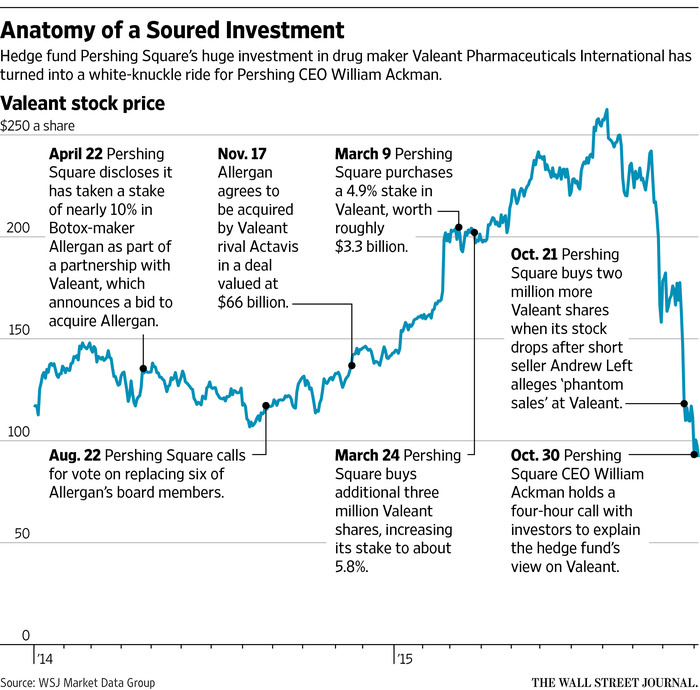

Part II on Valeant Let’s pretend you are asked to evaluate the situation for Mr. Ackman. He is in deep #$%^& and has brought in fresh eyes to advise him. Pershing Square has had to install two hotlines–Hotline 1: for investor suicide calls and Hotline 2: for investors who wish to phone-in death threats.

All bad joking aside, you have a huge pile of information to present the critical issues. Do you advise Mr. Ackman to buy more, sell immediately, sell down to a “more reasonable amount,” or hold? Use reason not opinion or emotion to guide you.

Step back and ask what are the important issues? What is Valeant worth? Can you know that? Pretend you are an investigative journalist trying to uncover the story.

What does Valeant do? Does Valeant have assets or a business method that gives the company a higher sustainable return on capital? What roll-ups/acquisition firms have been very successful in the past and how was success achieved?

Then you can read all the rumours and commentary swirling around Valeant, but be quick to focus on what you determine to be important. There are several links in the documents for you to follow further.

You can follow the reactions of investors and analysts at Seeking Alpha.

Hedge Fund Herding The psychological aspects of following others and the pressures of the short-term performance derby. Lesson: Never cease to do YOUR own thinking and analysis.

Readers should share if they believe there are actionable lessons here for investors in terms of psychology, portfolio management and analysis. Time is precious so we need to learn the important lessons.

And that ladies and gentlemen is called a permanent loss of capital IF investors paid too much for growth in a company doing roll-ups of commodity-like products (generic drugs) at unsustainable retail prices (competition and insurer push-back will cap price gains).

—

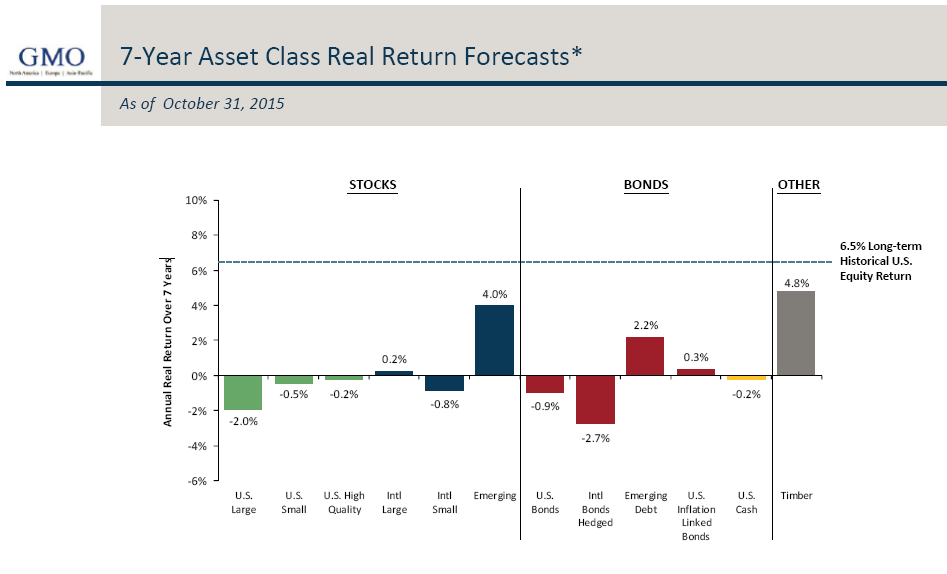

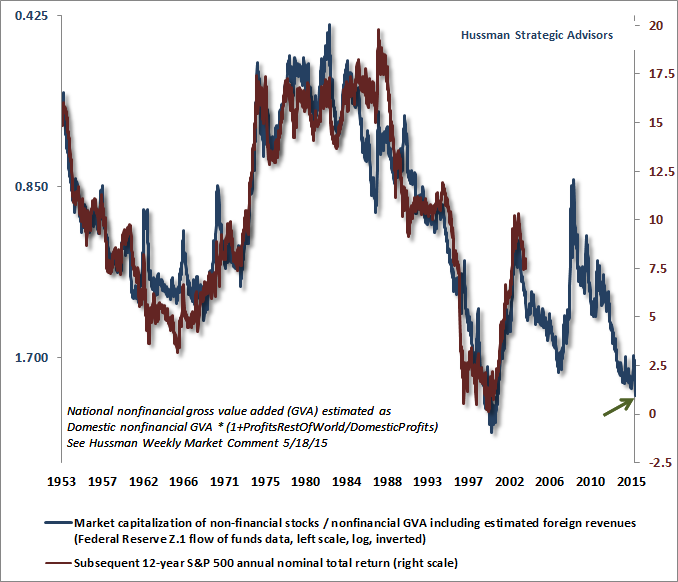

Meanwhile, investors face the second most overvalued equity market in history (Source: Hussman Funds).

Stoics understood that if negative emotions such as anger, envy, greed, fear, and grief plague your life, then soundness and peace of mind will elude you. Serentiy in the midst of adversity–which is hardly the same thing as the modern, Western and secular notion of “happiness”–is a necessary condition of a well-lived life.

{kind=link}